- Executive Summary

- Global RTD/High Strength Premixes Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Food & Beverage Industry Outlook

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Global RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global RTD/High Strength Premixes Market Outlook: Product

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- Market Attractiveness Analysis: Product

- Global RTD/High Strength Premixes Market Outlook: Packaging

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Packaging, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- Market Attractiveness Analysis: Packaging

- Global RTD/High Strength Premixes Market Outlook: Sales Channel

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Sales Channel, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- Market Attractiveness Analysis: Sales Channel

- Global RTD/High Strength Premixes Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- North America Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- North America Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- Europe RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- Europe Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- Europe Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- East Asia RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- East Asia Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- East Asia Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- South Asia & Oceania RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- Latin America RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- Latin America Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- Latin America Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- Middle East & Africa RTD/High Strength Premixes Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Spirit based RTD

- Wine based RTD

- Malt based RTD

- High Strength Premixes

- Middle East & Africa Market Size (US$ Bn) Forecast, by Packaging, 2026-2033

- Cans

- Bottles

- Others

- Middle East & Africa Market Size (US$ Bn) Forecast, by Sales Channel, 2026-2033

- Modern Trade

- Specialty Stores

- Online Retail

- Duty-Free Stores

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Diageo

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Suntory Holdings

- Anheuser-Busch InBev

- Pernod Ricard

- Bacardi Limited

- Brown-Forman

- Asahi Group Holdings

- Mark Anthony Brands

- Molson Coors Beverage Company

- Campari Group

- Takara Holdings

- Phusion Projects

- Diageo

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Beverages

- RTD/High Strength Premixes Market

RTD/High Strength Premixes Market Size, Share, and Growth Forecast 2026 - 2033

RTD/High Strength Premixes Market by Product (Spirit-based RTD, Wine-based RTD, Malt-based RTD, High Strength Premixes), Packaging (Cans, Bottles, Others), Sales Channel (Modern Trade, Specialty Stores, Online Retail, Duty-Free Stores), by Regional Analysis, 2026 - 2033

Key Industry Highlights:

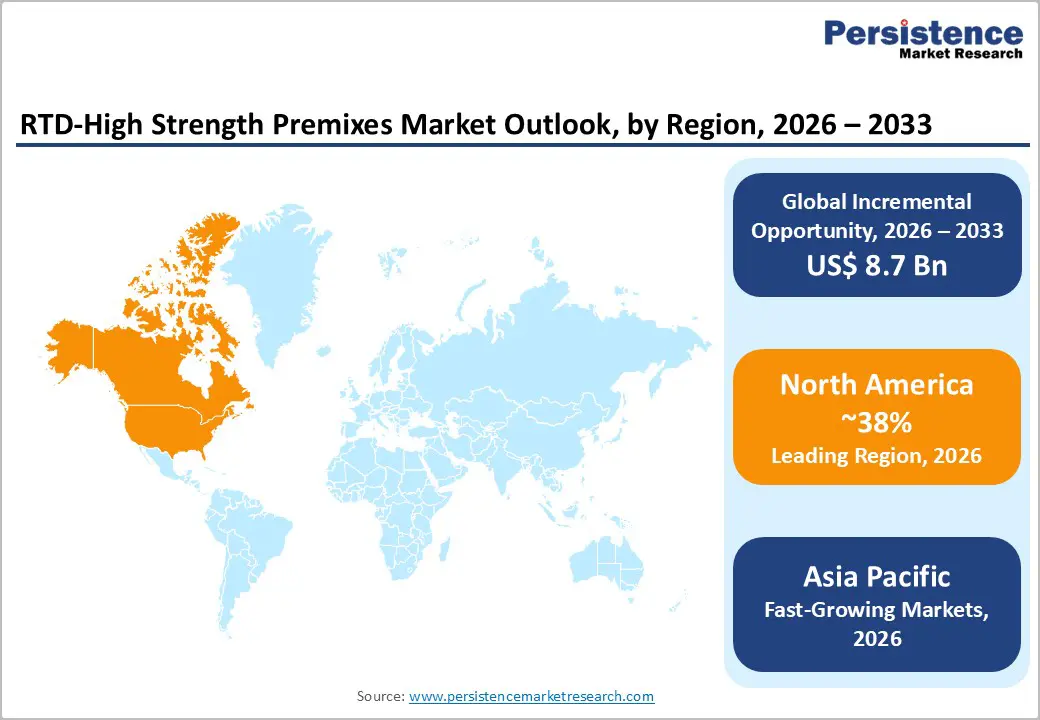

- North America is the leading region in the RTD/High Strength Premixes market, accounting for an estimated 38% share of global value in 2025, supported by high RTD penetration, strong retailer engagement, and sustained investments by major players in canned cocktails and premium spirit-based premixes.

- Asia Pacific is the fastest-growing regional market from 2025 - 2032, driven by the entrenched popularity of Japan’s chuhai and highball RTDs, rising middle-class incomes in China and ASEAN, and the rapid expansion of e-commerce and on-demand delivery for alcoholic beverages.

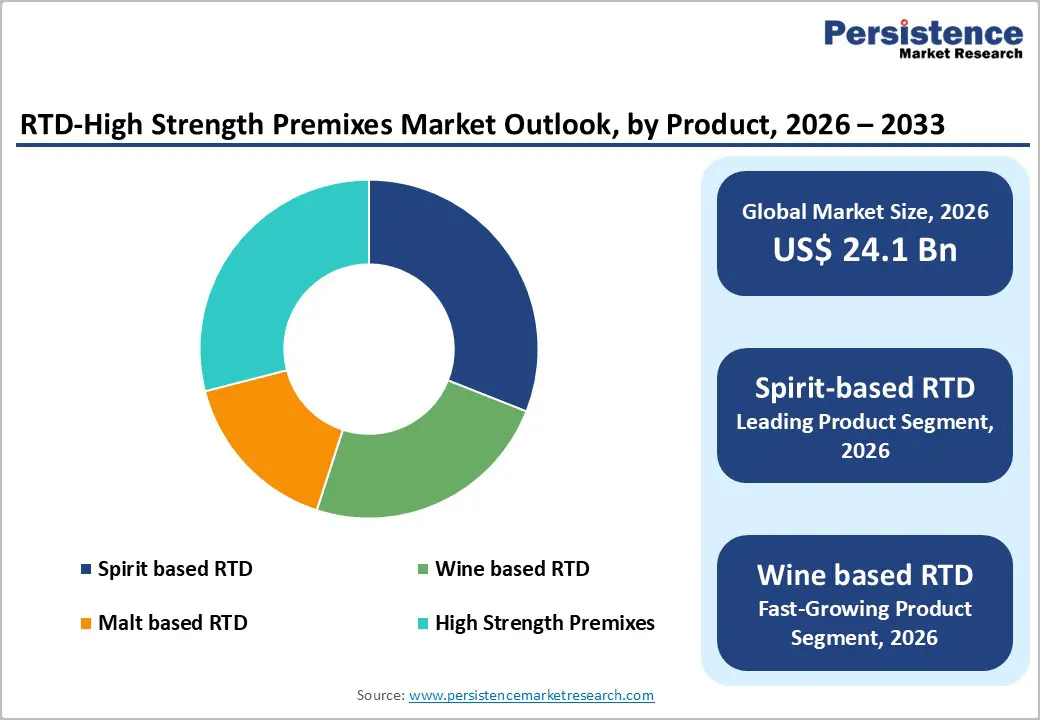

- By product, Spirit-based RTD is the dominant segment with around 31% share in 2025, leveraging powerful trademarks such as Smirnoff, Johnnie Walker, Tanqueray, and other global brands to drive premiumization and to migrate cocktail occasions from bars into at-home and on-the-go settings.

- By packaging, Cans are both the leading and fastest-growing segment, benefitting from strong consumer preference for portable, chill-quick formats, retailer support, and sustainability advantages associated with lightweight, fully recyclable aluminum in RTD and high-strength premix applications.

| Key Insights | Details |

|---|---|

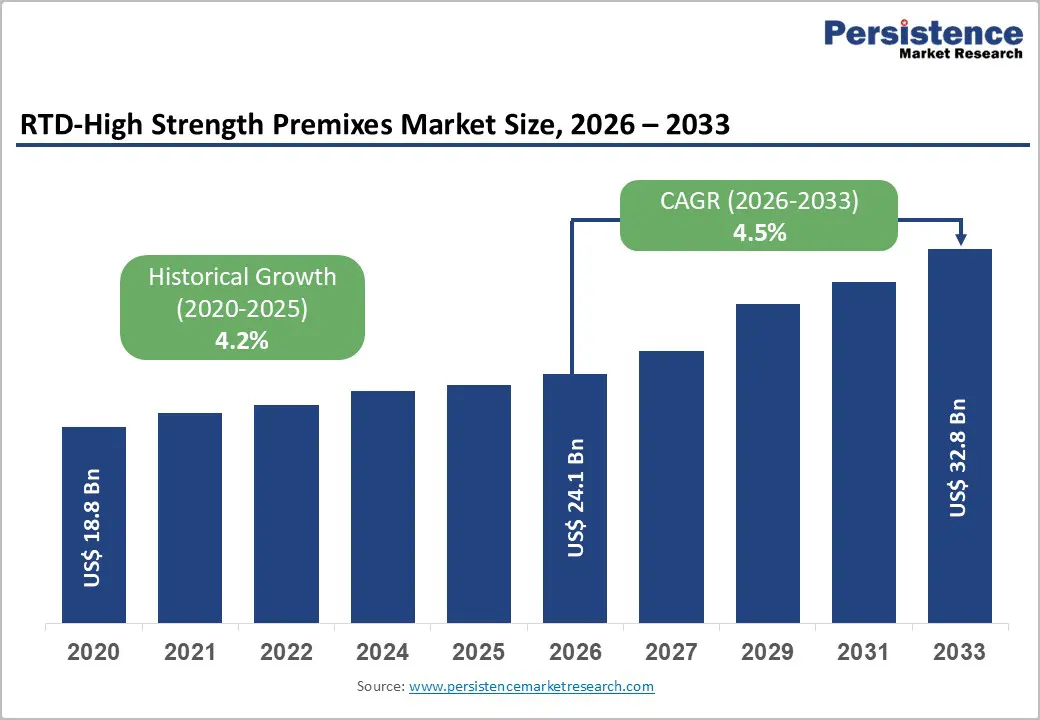

| RTD/High Strength Premixes Market Size (2026E) | US$ 24.1 billion |

| Market Value Forecast (2033F) | US$ 32.8 billion |

| Projected Growth CAGR (2026 - 2033) | 4.5% |

| Historical Market Growth (2020 - 2025) | 4.2% |

DRO Analysis

Drivers - Convenience, at-home mixology, and bar-quality experiences

A core growth driver for the RTD/High Strength Premixes market is the demand for bar-quality cocktails and mixed drinks in convenient, portable formats. Industry analysis from IWSR highlights that RTDs were the “star” of global beverage alcohol in 2023, the only major category to grow in volume while others declined, and are projected to grow by about 12% between 2023 and 2027 on a volume basis. In the United States, RTDs expanded from less than 3% of total beverage alcohol volume ten years ago to nearly 12% by 2022, making the segment larger than the total wine market by volume, as consumers increasingly substitute beer, wine, and spirits with convenient ready-to-drink offerings. Premium spirit-based canned cocktails and high-strength premixes from brands such as Diageo, Anheuser-Busch InBev’s Cutwater, Campari Group, and Suntory Holdings provide consistent taste, controlled portion sizes, and easy portability for at-home occasions, outdoor events, and on-the-go consumption, reinforcing their role as a modern alternative to traditional mixed drinks.

Premiumization and shift toward spirit-based RTDs

Another powerful growth engine is the premiumization of RTDs, especially spirit-based cocktails and high-strength premixes. According to IWSR, the RTD category has seen the largest year-on-year increase in average price per serving among alcohol categories, driven by the rapid expansion of the cocktail/long-drink and super-premium segments. Between 2018 and 2021, super-premium RTDs recorded a CAGR of about 71%, outpacing premium (about 48%) and standard tiers as consumers traded up to higher-quality, spirit-forward recipes. In the United States, spirits-based RTDs are expected to dominate RTD volume growth through 2029, with IWSR projecting that RTDs will account for roughly 9% of total U.S. beverage alcohol share by that year, up from about 2% in 2019 and 8% in 2021 across major markets. Launches such as Diageo’s Johnnie Walker Old Fashioned, Tanqueray Negroni, and Cîroc Cosmopolitan, bottled and canned RTDs, and premium canned cocktails from Cutwater and Campari Group, demonstrate how global players are using brand equity and craft-style positioning to justify higher price points in RTD and high-strength premix formats.

Restraints - Regulatory scrutiny on alcohol strength, labeling, and marketing

The RTD/High Strength Premixes market faces regulatory headwinds related to alcohol strength, responsible marketing, and labeling. Authorities are increasingly attentive to how high-ABV premixes and spirit-based RTDs are positioned, particularly when packaged in formats familiar from soft drinks or energy drinks. In the United Kingdom, the Office for Health Improvement and Disparities (OHID) launched a consultation in 2023 to update guidance on “alcohol-free” and low-alcohol descriptors, ABV disclosures, and health information on labels, aiming to ensure that consumers clearly understand alcoholic strength and associated risks. Similar policy discussions across markets encourage accurate ABV labeling, restrictions on youth-targeted imagery, and a clearer distinction between alcoholic RTDs and no/low alternatives. For manufacturers of high-strength premixes, this adds compliance complexity and may limit certain flavor, packaging, or marketing approaches.

Health concerns and moderation trends in alcohol consumption

Growing awareness of alcohol-related health risks and government campaigns promoting moderation can temper long-term volume growth for RTD and high-strength premix products. Scientific reviews of drinking patterns during and after the COVID-19 pandemic show that while some consumers increased at-home alcohol intake, others reduced consumption or shifted to no/low-alcohol alternatives, driving mixed impacts across segments. Public health agencies in many countries promote low-risk drinking guidelines and highlight the calorie and sugar content of flavored alcoholic beverages, which can dissuade heavy consumption of sweet, high-ABV premixes. As a result, producers must balance indulgent, flavor-forward offerings with lower-calorie, lower-sugar, and moderated-strength formats, adding formulation and portfolio complexity while responding to evolving consumer expectations around wellness and responsible drinking.

Opportunities - Expansion of wine-based RTDs and cocktail-style innovations

There is a substantial opportunity in wine-based RTDs, spritzes, and aperitif-inspired premixes, which are emerging as the fastest-growing product subsegment from 2025 to 2032. Industry commentary notes that RTD cocktails and long drinks are expected to post the highest RTD growth rates, leveraging established spirits and wine brands in convenient formats. Global groups such as Campari Group are already benefiting from strong demand for aperitif brands like Aperol, which achieved triple-digit growth in some channels and regions, and from rapid expansion in global travel retail, where net sales in that channel climbed by about +126.5% in 2022-2023. Collaborations between major soft drink and spirits companies to create RTD spritz, spritzer, and wine-based cocktails, alongside flavored high-strength premixes for social and outdoor occasions, will help this subcategory gain share as consumers seek lighter, flavor-driven alternatives to hard seltzers and traditional mixed drinks.

Category-wise Analysis

Packaging Insights

In packaging, Cans are the leading segment and are also the fastest-growing format for RTD/High Strength Premixes, with an estimated global share in the mid-40% range in 2025. Analysis of beverage packaging trends from Beverage Marketing Corporation shows that aluminum cans are gaining share across several beverage alcohol categories due to their light weight, recyclability, and suitability for fast-growing segments such as RTDs. Industry case studies highlight that canned cocktails sales jumped by about +42% in 2021, reaching roughly US$ 1.6 billion in revenue, with growth expected to continue as brands expand portfolios and invest in more distinctive can designs. RTD packaging specialists note that brands are using specialty can sizes, custom graphics, and enhanced printing effects to stand out on the shelf and communicate premium positioning, while cans offer robust protection, rapid chilling, and portion control that align well with outdoor, travel, and at-home occasions. These functional and marketing advantages underpin the leadership of cans over Bottles and Others in the RTD and high-strength premix space.

Sales Channel Insights

Among sales channels, Modern Trade (including supermarkets, hypermarkets, and large convenience chains) is the leading distribution segment for RTD/High Strength Premixes, while Online Retail is the fastest-growing channel from 2025 to 2032. Large modern trade retailers are allocating more shelf space to RTDs and premixed cocktails, positioning them alongside beer and flavored malt beverages to capture impulse purchases and planned entertaining occasions. At the same time, IWSR’s e-commerce analysis shows that online alcohol sales value in the United States grew by nearly +80% in 2020 and +15% in 2021, and is expected to grow at about +11% value CAGR through 2026, even though online still represents only around 3.5% of total alcohol sales today. Academic research documenting +234% year-on-year growth in online alcohol sales in March 2020 and +400% growth for Drizly in May 2020 underscores how digital channels became an entrenched habit for many consumers. Together, these trends support modern trade’s current leadership given its volume scale while positioning online retail as the most dynamic channel for discovery, premiumization, and direct-to-consumer RTD offerings.

Regional Insights

North America RTD/High Strength Premixes Market Trends and Insights

North America is the leading regional market, accounting for an estimated 38% share of global RTD/High Strength Premixes value in 2025, supported by high disposable incomes, a strong culture of experimentation with new drinks, and robust distribution networks. In the United States, IWSR data show that RTDs expanded from less than 3% of total beverage alcohol volume to almost 12% by 2022, making the category larger than the domestic wine market by volume. RTDs are forecast to continue gaining share, with their portion of U.S. total beverage alcohol expected to reach around 9% by 2029, driven especially by spirits-based products, hard teas, and pre-mixed cocktails that compete directly with traditional spirits and beer. Major brand owners, including Diageo, Anheuser-Busch InBev, Molson Coors Beverage Company, and Mark Anthony Brands (owner of White Claw), have invested heavily in RTD innovation and capacity, reinforcing the region’s leadership.

The regulatory framework in North America combines state-level alcohol control systems with federal rules on labeling and marketing, enabling significant innovation in RTD and high-strength premix formats while encouraging clear ABV disclosure and responsible messaging. E-commerce has emerged as a complementary growth engine: IWSR reports that U.S. online alcohol value sales grew nearly 80% in 2020, 15% in 2021, and are expected to log a value CAGR of about 11% through 2026, offering a powerful platform for premium RTDs and cocktail subscriptions. As on-premise channels recover and off-premise remains strong, North America’s integrated ecosystem of bars, retail, duty-free, and online platforms positions the region to sustain its leading role in RTD and high-strength premix adoption.

Asia Pacific RTD/High Strength Premixes Market Trends and Insights

The Asia Pacific RTD and high-strength premixes market is emerging rapidly, driven by urbanization, rising disposable incomes, and evolving drinking preferences among younger consumers. Countries like Japan, Australia, China, and India are witnessing strong demand for convenient, flavored alcoholic beverages that align with social and on-the-go consumption trends. The growing influence of Western drinking culture, along with increasing participation of women consumers, is further supporting market expansion. Premiumization is a key trend, with brands introducing craft-inspired, spirit-based RTDs and higher-alcohol premixes to cater to experimental tastes. Additionally, e-commerce and modern retail channels are expanding product accessibility, especially in urban centers. Regulatory easing in certain markets and increased product innovation, such as low-sugar and natural-ingredient offerings, are also contributing to growth. Overall, the Asia-Pacific is positioned as the fastest-growing region, supported by a large young population and shifting lifestyle patterns.

Competitive Landscape

The RTD / High Strength Premixes market is highly competitive, characterized by the presence of global beverage giants alongside regional and emerging players. Major companies leverage strong brand portfolios, extensive distribution networks, and continuous product innovation to maintain their market position. Competition is primarily driven by flavor innovation, premiumization, and targeted marketing toward younger consumers. Strategic initiatives such as mergers, acquisitions, and partnerships are widely adopted to expand geographic reach and strengthen product offerings.

Key Developments:

- In February 2025, Suntory Holdings announced the expansion of its ready-to-drink (RTD) portfolio in the United States with the launch of “MARU-HI,” a Japanese-inspired sparkling cocktail. Introduced initially in California, the product drew inspiration from traditional Chu-hi beverages and featured citrus-based flavors with moderate alcohol content.

- In February 2024, Diageo launched “The Cocktail Collection” premium bottled RTDs in the U.K., featuring Johnnie Walker, Tanqueray, and Cîroc-based cocktails, later expanding into 100 ml cans to capture at-home and on-the-go occasions.

Companies Covered in RTD/High Strength Premixes Market

- Diageo, Suntory Holdings

- Anheuser-Busch InBev

- Pernod Ricard

- Bacardi Limited

- Brown-Forman

- Asahi Group Holdings

- Mark Anthony Brands

- Molson Coors Beverage Company

- Campari Group

- Takara Holdings

- Phusion Projects

- Constellation Brands

- Heineken N.V.

- Kirin Holdings Company

Frequently Asked Questions

The global RTD/High Strength Premixes market is projected to reach around US$ 24.1 billion in 2026, reflecting steady growth as consumers increasingly favor convenient, bar-quality canned cocktails, wine-based RTDs, and high-strength premixes across both on-trade and off-trade channels.

A key demand driver is consumers’ desire for convenient, consistent, and premium bar-quality drinks at home and on the go, supported by strong growth in spirit-based RTDs, cocktail-style innovations, and premiumization across canned and bottled premixes in major markets worldwide.

North America currently leads the global RTD/High Strength Premixes market, with an estimated 38% share of world value in 2025, driven by rapid RTD adoption in the United States, strong retailer support, and heavy investment from leading brewers and spirits companies.

A major opportunity lies in integrating premium RTD and high-strength premix portfolios with rapidly growing online retail and omnichannel ecosystems, including subscription packs, cocktail discovery platforms, and travel-retail-exclusive lines that tap into demand for convenient, elevated drinking experiences at multiple touchpoints.

Key players include Diageo, Suntory Holdings, Anheuser-Busch InBev, Pernod Ricard, Bacardi Limited, Brown-Forman, Asahi Group Holdings, Mark Anthony Brands, Molson Coors Beverage Company, Campari Group, Takara Holdings, and Phusion Projects, alongside additional global brewers and regional RTD specialists.