- Communication Infrastructure & Services

- Refurbished and Used Mobile Phones Market

Refurbished and Used Mobile Phones Market Size, Share, and Growth Forecast, 2026 - 2033

Refurbished and Used Mobile Phones Market by Product (Refurbished Phones, Used Phones [Trade-ins, Buyback]), Price Range (Low-Priced, Mid-Priced, Premium), Sales Channel (Online/ E-commerce, Offline [Brick-and-Mortar, Third-Party]), and Regional Analysis for 2026 - 2033

Refurbished and Used Mobile Phones Market Size and Trends Analysis

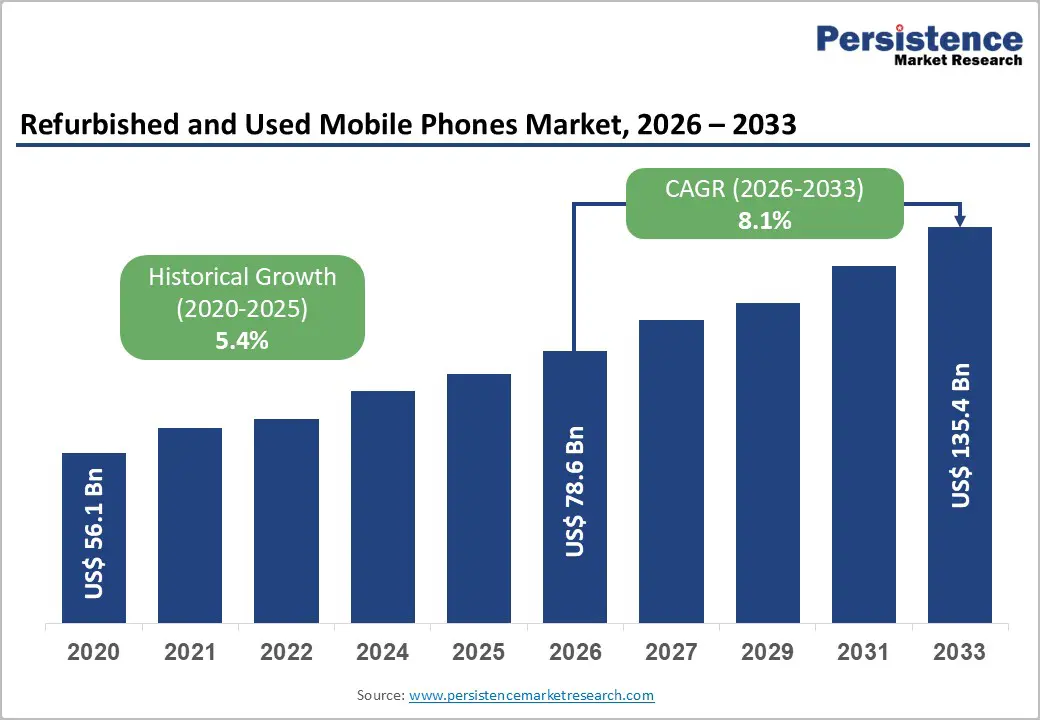

The global refurbished and used mobile phones market size is likely to be valued at US$78.6 billion in 2026 and expected to reach US$135.4 billion by 2033 growing at a CAGR of 8.1% during the forecast period from 2026 to 2033.

This market expansion is primarily driven by rising consumer demand for cost-effective smartphone alternatives, increasing environmental awareness regarding electronic waste reduction, rapid smartphone replacement cycles in developed economies, growing smartphone penetration in emerging markets, regulatory frameworks mandating circular economy practices, technological improvements in device refurbishment processes, and expanding e-commerce infrastructure that enables broader market accessibility.

Key Industry Highlights:

- Leading Product: Refurbished phones dominate with over 58% market share in 2026 and are expected to surpass US$ 45.6 Bn, driven by affordability, certified quality, and warranty-backed trust. Used phones are expected to grow at a CAGR of 6.7% due to rising affordability needs and sustainability awareness, while trade-in programs are expected to channel over 70% of secondary devices through structured, certified channels by 2026.

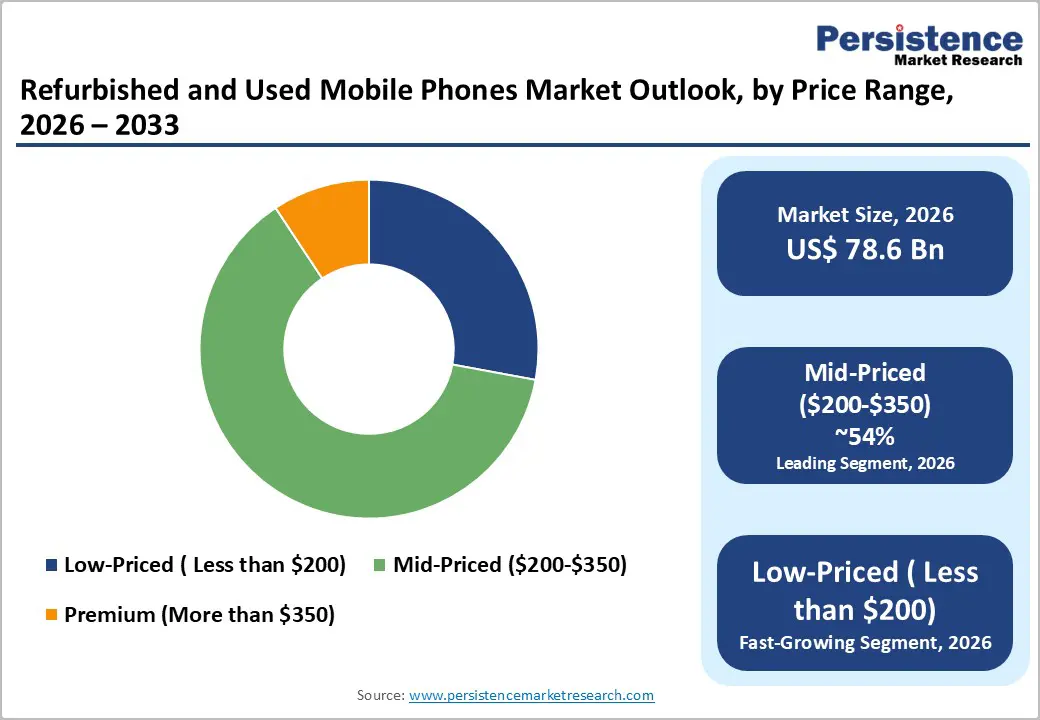

- Leading Price Range: Mid-priced ($200–$350) lead with over 54% market share in 2026, offering an optimal balance of affordability, performance, and features. Low-priced devices (<$200) grow rapidly among first-time buyers, students, and entry-level consumers, supported by digital inclusion programs.

- Leading Sales Channel: Online and e-commerce channels dominate with over 62% market share in 2026, projected to exceed US$ 88.2 Bn by 2033, providing transparent grading, warranties, flexible payments, doorstep delivery, and wide model availability. Offline channels remain significant due to preferences for hands-on inspection and repair support. Third-party distribution channels are expected to hold over 71% market share in 2026, including independent refurbishers, aggregator platforms, and informal dealers.

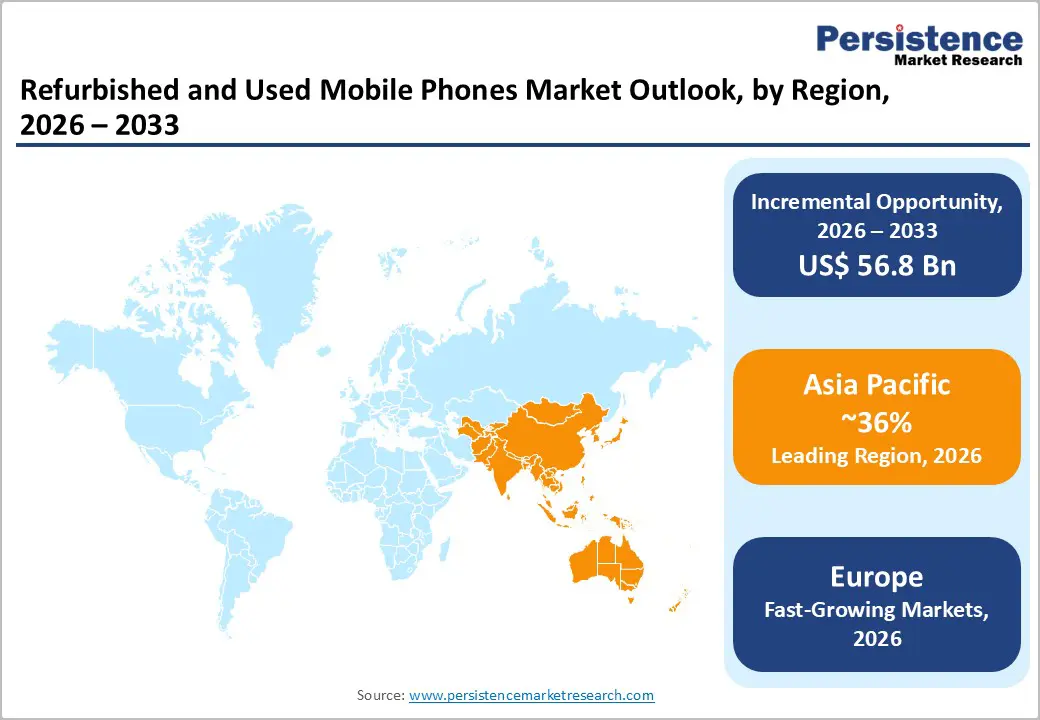

- Leading Region: Asia Pacific leads with ~36% share in 2026, valued at US$ 28.3 Bn, driven by rising smartphone penetration and formal collection programs. India is expected to have a CAGR 14.5% from 2026 to 2033. China’s market is projected to surpass US$ 23 Bn by 2033, supported by e-waste regulations. Latin America is growing rapidly at an 8.5% CAGR and is expected to exceed US$ 14 Bn by 2033.

| Key Insights | Details |

|---|---|

|

Refurbished and Used Mobile Phones Market Size (2026E) |

US$78.6 Bn |

|

Market Value Forecast (2033F) |

US$135.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Dynamics

Driver - Cost-Conscious Consumer Behavior and Premium Device Accessibility

The shift toward refurbished and used mobile phones is fundamentally rooted in consumer economics and aspirational purchasing patterns. Refurbished devices typically offer 40-60% cost savings compared to new flagship models, enabling broader demographic segments to access premium smartphone features that were previously unavailable at entry-level price points. The average consumer smartphone replacement cycle has compressed to 2-3 years in developed markets, generating substantial secondary inventory. Rising smartphone prices, with flagship models exceeding $1,200, have created compelling value propositions for refurbished alternatives. Developing market consumers, particularly in the Asia Pacific region, increasingly prioritize device affordability alongside functional specifications, accelerating the adoption of pre-owned smartphones.

Regulatory Frameworks and Circular Economy Mandates

Government regulations and international environmental standards are key enablers, with initiatives like the EU Circular Economy Action Plan mandating sustainable device lifecycle management and promoting refurbishment networks. Similar frameworks in North America, Japan, and the Asia-Pacific region provide tax incentives and compliance requirements, thereby legitimizing refurbished devices as part of national environmental strategies. Rising e-waste, 62 million tonnes in 2022, up 82% from 2010 and projected to reach 82 million tonnes by 2030, highlights the urgency, as only 1% of rare earth element demand is met through recycling. Compliance costs for new device production further enhance the competitiveness of refurbished phones, while certification programs and quality standardization reduce consumer hesitancy regarding pre-owned devices.

Restraint - Counterfeit Device Proliferation and Authentication Challenges

Counterfeit refurbished smartphones pose a significant challenge to market legitimacy and consumer trust, with estimated counterfeit rates reaching 15-25% in some regions, particularly affecting offline retailers. Inconsistent authentication processes and supply chain opacity in informal markets increase operational costs and legal liabilities for distributors and manufacturers. According to OECD/EUIPO, counterfeit goods accounted for ~2.3% of global trade in 2021, while the European Commission reports they make up ~5% of EU imports, with electronics among the most targeted. In 2023, EU authorities seized 152 million counterfeit products worth over US$4 billion, over half of which originated in Italy, with China, Turkey, and Hong Kong as major sources. These challenges constrain profitability and slow market expansion in the refurbished mobile segment.

Battery Degradation and Hardware Obsolescence Concerns

Battery degradation remains a key barrier, as lithium-ion batteries typically lose efficiency after 300–500 charge cycles, leaving refurbished devices with 70–80% capacity. Rapid hardware obsolescence further limits functionality, as older models do not support new software or advanced features. Consumers are price-sensitive toward devices with visible hardware limitations, reducing retail margins, while costs for extended warranties or battery replacements erode the perceived savings, especially in premium refurbished segments. For example, high-end smartphones refurbished after two years face both performance and battery issues, which can affect buyer confidence.

Opportunity - Certified Refurbishment Standards and Subscription Models

The adoption of standardized refurbishment certifications, including ISO 14001 and manufacturer-backed quality programs from Apple, Samsung, and Google, is creating a market opportunity by elevating refurbished phones to trusted, quality-assured alternatives. Third-party certification ecosystems and AI-driven diagnostics enhance device longevity and reduce counterfeit risks, consolidating consumer confidence. Subscription-based access models from companies like Grover, Recommerce, and Fairphone are rapidly gaining traction, particularly among younger Europeans, by lowering upfront costs and enabling easy device upgrades. This shift from ownership to flexible access is driving demand, promoting tech reuse, and supporting the circular economy.

AI-Driven Refurbishment Unlocking Market Opportunities

Advancements in AI-driven refurbishment technologies are creating significant opportunities by enhancing device reliability, quality, and consumer trust. Programs like Apple’s Certified Refurbished (2023) and trade-in initiatives by brands such as Samsung are expanding the supply of high-quality pre-owned devices. Automated diagnostics, battery reconditioning, firmware optimization, and AI-based grading technologies, exemplified by solutions like Phonecheck, ensure consistent performance, accurate fault detection, and improved aesthetics, narrowing the gap with new devices. Coupled with certified data wiping and security protocols, these innovations make refurbished phones a credible, affordable, and environmentally sustainable alternative, positioning manufacturers and resellers to capture growing market demand.

Category-wise Analysis

By Product Insights

Refurbished phones are expected to account for over 58% of the market in 2026, with values exceeding US$ 45.6 billion. It directly addresses core consumer needs of affordability, reliability, and trust. They offer 30–60% lower prices than new devices while maintaining assured functionality through professional testing, certified repairs, and battery replacement, reducing performance risk. Growing demand for warranty-backed devices, especially among price-sensitive yet quality-conscious buyers, favors refurbished over unverified used phones.

Used phones are expected to grow at a CAGR of 6.7% due to rising affordability needs among price-sensitive consumers seeking smartphones at lower costs. Growing awareness of sustainability and electronic waste reduction also drives adoption. Faster technology turnover and structured trade-in programs, which are expected to hold over 70% of the market share by 2026, increase the supply of used devices and further boost market growth.

By Price Range Insights

The mid-priced ($200-$350) segment is expected to account for over 54% market share in 2026, driven by its ability to meet core consumer needs for affordability, reliable performance, and modern features at a reasonable cost. These devices offer strong value-for-money by balancing battery life, camera quality, and software support without the high price of premium models. They are widely available in the secondary market because of frequent upgrades by original users, ensuring a steady supply.

Low-priced (less than $200) products are growing rapidly due to increasing smartphone adoption among first-time buyers, students, and entry-level consumers in developed markets. These devices offer basic functionality and meet needs for communication, internet access, or secondary/backup use. Growth is supported by government initiatives promoting affordable device access as part of digital inclusion programs. Consumers prioritize functionality over brand, creating strong demand for budget-friendly options.

By Sales Channel Insights

Online and e-commerce channels dominate with over 62% market share in 2026 and projected valuations exceeding US$ 88.2 Bn by 2033. These platforms meet buyer needs through transparent device grading, warranties, easy returns, and competitive pricing, along with wider model availability, doorstep delivery, and flexible payment options. Inventory aggregation, consumer reviews, and personalized recommendations enhance trust, reduce information asymmetry, improve purchase efficiency, drive higher conversion rates, and support overall market growth.

Offline channels are expected to grow significantly due to consumers’ preference for hands-on experience to assess device condition, battery health, and functionality. Retailers provide immediate availability, repair support, and flexible pricing to address the need for convenience and reliability in used devices. Third-party distribution channels, which hold over 71% market share in 2026, include independent refurbishers, aggregator platforms, and informal dealers, offering operational flexibility, diverse inventory, and competitive price positioning compared to authorized dealers.

Regional Insights

Asia Pacific Refurbished and Used Mobile Phones Market Trends

Asia Pacific dominates the global refurbished and used mobile phones market, with over 36% share in 2026 and a valuation of US$ 28.3 Bn, driven by rising smartphone penetration in emerging markets. China’s environmental regulations and e-waste initiatives support refurbishment growth, while India’s market is expected to grow at a CAGR of 14.5% from 2026 to 2033, fueled by digital payments expansion via UPI and a mobile broadband subscriber base of ~969 million noted by TRAI in March 2025, enabling e-commerce access to refurbished devices across urban and rural areas. E-waste volumes in the region remain high, with only ~12.8% properly recycled in 2022, underscoring the region's circular economy potential. China, India, and South Korea’s formal collection programs further boost the refurbishment ecosystem, with China Refurbished and Used Mobile Phones Market alone expected to surpass US$ 23 Bn by 2033.

Latin America Refurbished and Used Mobile Phones Market Trends

Latin America is the fastest-growing region, with a projected CAGR of 8.5% and expected to exceed US$14 Bn by 2033. In Brazil, the market is expected to surpass US$6.5 Bn by 2033, driven by rising device prices, inflation, and a large population with constrained budgets; 88.9% of people aged 10+ (≈167.5 million) owned a mobile phone in 2024, fueling demand for certified refurbished devices. In Mexico, 81.7% of individuals aged 6+ used cellphones in 2024, many of whom relied on prepaid plans, making high-quality refurbished phones a cost-effective upgrade for 4G/5G capabilities and better cameras. Argentina’s policy changes on taxes, import rules, and line formalization push price-sensitive buyers toward certified second-hand channels, reducing informal market flows. Affordability, functionality, and regulatory nudges are key drivers shaping demand.

Europe Refurbished and Used Mobile Phones Market Trends

The European refurbished and used mobile phones market is a mature ecosystem, projected to grow at a CAGR of 10.1% from 2026 to 2033, led by Germany with ~24% regional share, followed by France and the rest of Europe. High smartphone penetration (85–90%), strong consumer protection standards, and a developed e-commerce infrastructure underpin market stability. The UK emphasizes carrier-partnership channels, while France specializes in certified refurbishment and premium devices; Spain and Italy are emerging growth markets aligned with EU circular economy regulations. Environmental awareness drives demand for sustainable devices, supported by blockchain-based authentication and standardized EU warranties. Technological integration, AI diagnostics, and automation in refurbishment facilities enhance operational efficiency, with new access channels emerging through partnerships with automotive connectivity ecosystems.

Competitive Landscape

The refurbished and used mobile phones market is highly fragmented, with numerous OEM-authorized refurbishers, independent refurbishing companies, e-commerce platforms, and local dealers competing simultaneously. Companies focus on price differentiation and quality assurance by offering graded devices, certified testing, and warranty-backed products to build trust. Manufacturers are investing in automation, AI-based diagnostics, and centralized refurbishing hubs to reduce costs and improve scale efficiency, while emphasizing sustainability credentials to differentiate themselves from informal sellers.

Key Industry Developments

- In January 2025, Samsung Electronics launched the New Galaxy AI Subscription Club, which offers up to a 50% refund on used smartphones. Subscribers can return their Galaxy S25 series devices after 12 months for a 50% refund or after 24 months for a 40% refund, making premium devices more affordable.

- In January 2025, Samsung Electronics launched a year-round Galaxy Trade-In Program that allows customers to trade in used Galaxy devices on Samsung.com without purchasing a new phone. Piloting in Korea and France and expanding globally through 2025, the program supports a circular economy by increasing the supply of refurbished and used smartphones.

- In October 2024, Google launched its Certified Refurbished Phone program, offering up to 40% off select Pixel models. Discounts include the Pixel 6a for $249, the Pixel 6 for $339, the Pixel 6 Pro for $539, the Pixel 7 for $429, and the Pixel 7 Pro for $629, making premium devices more affordable.

Companies Covered in Refurbished and Used Mobile Phones Market

- Apple

- Samsung

- Huawei Technologies Co., Ltd.

- Xiaomi Inc.

- Lenovo Group Ltd.

- Walmart Inc.

- Amazon.com Inc.

- eBay Inc.

- Alibaba Group Holding Ltd.

- Cashify

- Swappie

- Others

Frequently Asked Questions

The global refurbished and used mobile phones market is projected to be valued at US$78.6 Bn in 2026.

The need for affordable smartphone access, as consumers seek reliable devices at significantly lower prices amid rising new-phone costs, is a key driver of the market.

The market is expected to witness a CAGR of 8.1% from 2026 to 2033.

The growing supply of trade-in and upgrade programs, increasing the availability of quality pre-owned devices, is creating strong growth opportunities.

Apple, Samsung, Google, Huawei Technologies Co., Ltd., Xiaomi Inc., and Lenovo Group Ltd. are among the leading key players.