- Executive Summary

- Global Professional Service Robots Maket Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Professional Service Robots Maket Outlook: Robot Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Robot Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- Market Attractiveness Analysis: Robot Type

- Global Professional Service Robots Maket Outlook: Mobility

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Mobility, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- Market Attractiveness Analysis: Mobility

- Global Professional Service Robots Maket Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- Market Attractiveness Analysis: Application

- Global Professional Service Robots Maket Outlook: Usage Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Usage Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- Market Attractiveness Analysis: Usage Type

- Global Professional Service Robots Maket Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- Europe Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- East Asia Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- South Asia & Oceania Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- Latin America Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- Middle East & Africa Professional Service Robots Maket Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Robot Type, 2026-2033

- Inspection & Maintenance Robots

- Medical & Healthcare Service Robots

- Logistics & Delivery Robots

- Cleaning & Sanitation Robots

- Agricultural Service Robots

- Security & Surveillance Robots

- Education & Entertainment Robots

- Customer Service & Reception Robots

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Mobility, 2026-2033

- Mobile Robots

- Stationary Robots

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Healthcare & Surgery

- Retail & Hospitality

- Logistics & Warehousing

- Manufacturing Support

- Agriculture & Farming

- Public Safety & Security

- Education & Research

- Domestic & Personal Assistance

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Usage Type, 2026-2033

- Land-based

- Water-based

- Wearable Robots

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- ABB Ltd.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Blue Ocean Robotics

- Boston Dynamics, Inc.

- Cyberdyne USA Inc.

- Daifuku Co., Ltd.

- Fanuc Corporation

- Gecko Robotics, Inc.

- Honda Motor Co., Ltd

- Intuitive Surgical, Inc.

- iRobot Corporation

- KUKA AG

- SoftBank Robotics Group

- Diligent Robotics, Inc.

- Harvest CROO Robotics LLC

- Aethon Inc.

- Medtronic (Hugo RAS)

- Amazon (Vulcan)

- CMR Surgical (Versius)

- ABB Ltd.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automation & Robotics

- Professional Service Robots Market

Professional Service Robots Market Size, Share, and Growth Forecast 2026 - 2033

Professional Service Robots Market by Robot Type (Inspection & Maintenance Robots, Medical & Healthcare Service Robots, Logistics & Delivery Robots, Cleaning & Sanitation Robots, Agricultural Service Robots, Security & Surveillance Robots, Education & Entertainment Robots, Customer Service & Reception Robots), Mobility (Mobile Robots, Stationary Robots), Application (Healthcare & Surgery, Retail & Hospitality, Logistics & Warehousing, Manufacturing Support, Agriculture & Farming, Public Safety & Security, Education & Research, Domestic & Personal Assistance), Usage Type and Regional Analysis 2026 - 2033

Professional Service Robots Market Size and Trend Analysis

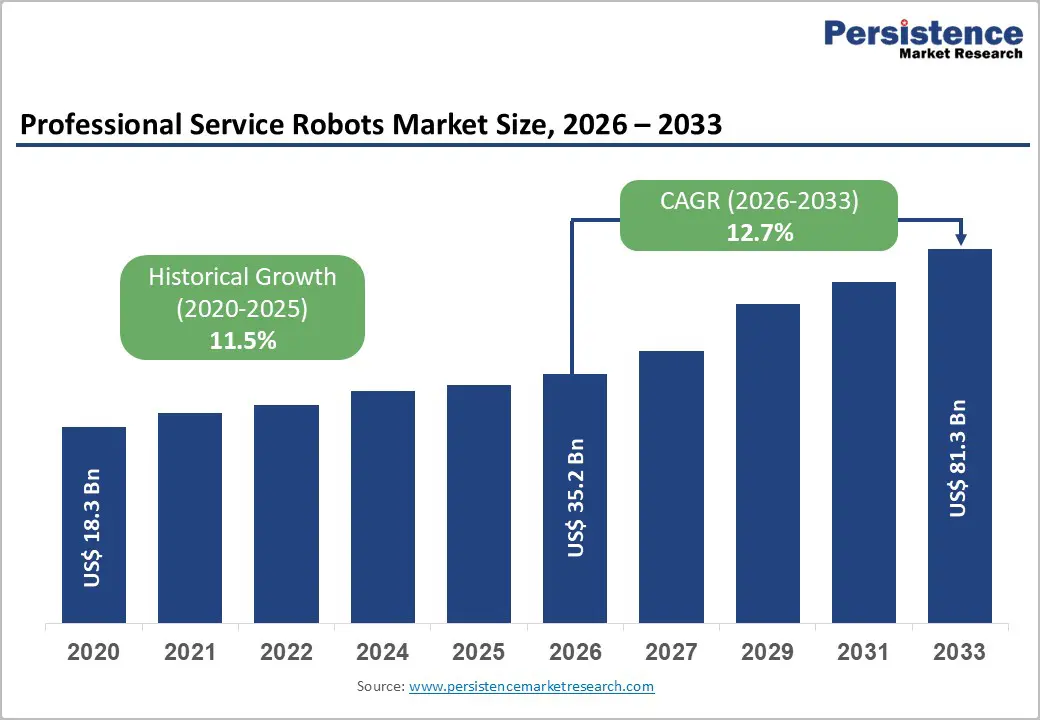

The global professional service robots market size is expected to be valued at US$ 35.2 billion in 2026 and projected to reach US$ 81.3 billion by 2033, growing at a CAGR of 12.7% between 2026 and 2033.

Market expansion is driven by three structural forces rather than incremental automation. First, persistent labor shortages, including 2.1 million unfilled U.S. manufacturing jobs by 2030, 57% of supply chain leaders citing workforce constraints, and 5.6% annual warehouse labor cost inflation, are making automation a permanent operational necessity. Second, surgical robotics is becoming standard clinical infrastructure, with 2.63 million U.S. robotic procedures in 2024, 17% year-over-year growth, and 362 new systems deployed. Third, logistics automation offers a major upside, as under 8% of U.S. warehouses use AMRs despite projected 31% annual shipment growth, unlocking a US$ 30+ billion market opportunity.

Key Industry Highlights:

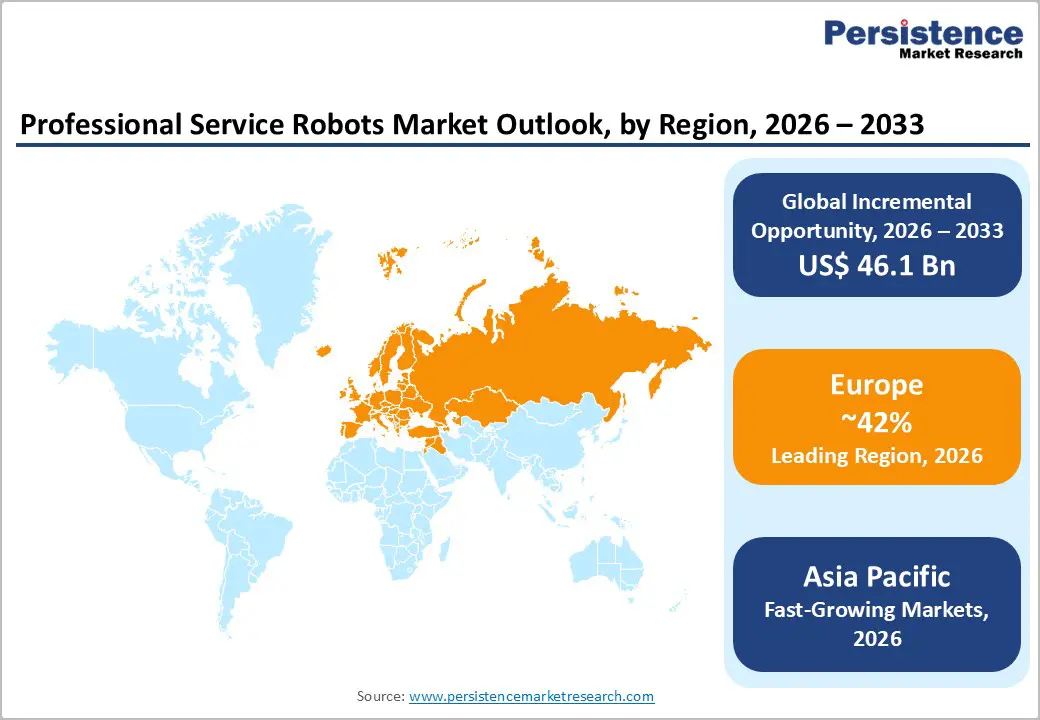

- Leading Region: Europe leads the global market with a 42% share in 2025, supported by advanced industrial infrastructure, strong healthcare systems, high surgical robot adoption, and policy-driven automation initiatives such as the NHS England target of 500,000 robotic surgeries per year and EU Farm to Fork subsidies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region through 2032 - 2033, driven by manufacturing cost convergence, government-led automation programs, China’s biotech zones, Japan’s aging population fueling eldercare robot demand, and India’s US$ 10 billion warehouse automation investment.

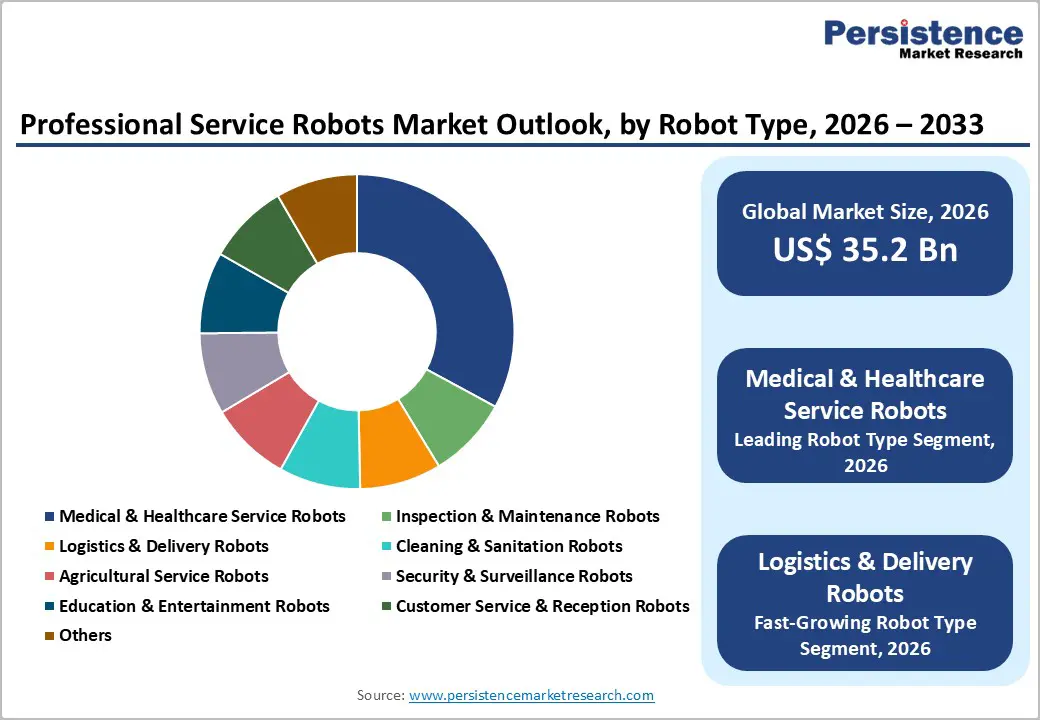

- Dominant Robot Type Segment: Medical and healthcare service robots dominate with a 36% market share in 2025, underpinned by surgical robotics leadership with 60% share and 2.63 million procedures in 2024, alongside growing non-surgical medical applications.

- Fastest-Growing Robot Type Segment: Logistics and delivery robots are the fastest-growing segment driven by labor shortages and e-commerce expansion.

- Key Market Opportunity: Warehouse logistics automation represents the largest growth opportunity, as low penetration rates, India’s US$ 10 billion investment pipeline, and a projected 31% annual growth rate create sustained, multi-year demand for autonomous robotics solutions.

| Global Market Attributes | Key Insights |

|---|---|

| Professional Service Robots Market Size (2026E) | US$ 35.2 billion |

| Market Value Forecast (2033F) | US$ 81.3 billion |

| Projected Growth CAGR (2026 - 2033) | 12.7% |

| Historical Market Growth (2020 - 2025) | 11.5% |

Market Dynamics

Labor Shortages Driving Structural Shift Toward Automation Across Core Service Industries

The Professional Service Robots Market is expanding rapidly as global labor shortages evolve into long-term structural deficits across manufacturing, logistics, and healthcare. With an estimated 2.1 million U.S. manufacturing jobs expected to remain unfilled by 2030 and more than half of supply chain executives reporting workforce constraints, organizations are increasingly adopting robots to sustain output and service levels. Rising warehouse wages, growing at over 5% annually, combined with accelerating e-commerce volumes, are strengthening the return-on-investment case for autonomous mobile robots in material handling and fulfillment operations.

In healthcare, shortages of nurses, caregivers, and specialists, alongside aging populations and rising rehabilitation needs, are driving adoption of service robots for eldercare, mobility support, telepresence, and infection control. Persistent skill gaps in specialized surgery further reinforce reliance on robotic systems, transforming service robots from optional automation tools into essential operational infrastructure.

Clinical Validation and Regulatory Maturity Accelerating Surgical Robotics Adoption

Surgical robotics is emerging as a major growth driver as robotic-assisted minimally invasive surgery becomes a standard of care across healthcare systems. Strong clinical validation, demonstrated by millions of annual procedures globally, has reinforced the effectiveness of robotic platforms across urology, gynecology, cardiothoracic, and general surgery. Regulatory standardization and clearer approval pathways across major markets have reduced adoption risk, enabling hospitals to commit capital toward long-term robotic infrastructure.

Government-led initiatives and public healthcare programs are further institutionalizing robotic surgery through large-scale deployment targets, training investments, and reimbursement support. Documented clinical benefits, including improved precision, reduced recovery times, shorter hospital stays, and lower complication rates, are increasing patient and surgeon preference for robotic-assisted procedures. Integration of AI-driven analytics, procedural optimization tools, and performance feedback systems is deepening surgeon dependence on robotic platforms, creating technology lock-in and recurring demand for software, upgrades, and service contracts, thereby sustaining long-term market growth.

Restraints - High Capital Costs and Integration Complexity Restricting Adoption Among Smaller Operators

The Professional Service Robots Market faces adoption constraints due to high upfront capital requirements and complex system integration, particularly for small and mid-sized healthcare providers and logistics operators. Surgical robotic systems typically require multi-million-dollar investments, supplemented by substantial annual maintenance and service contracts, making them financially inaccessible for rural hospitals and resource-constrained healthcare facilities.

In logistics, autonomous mobile robot deployments often necessitate warehouse redesigns, software integration with existing management systems, and specialized workforce training, significantly increasing total ownership costs. Integration challenges related to software interoperability, equipment compatibility, and vendor lock-in further slow deployment timelines and raise operational risk. Additionally, inconsistent regulatory requirements across regions prolong approval cycles and increase compliance costs, limiting the ability of smaller vendors and buyers to scale robotic adoption efficiently.

Technological Limitations and Safety Concerns in Complex Operating Environments

Technological capability gaps continue to restrain professional service robot adoption in unstructured, human-centric environments. Current robotic systems face limitations in handling variable object shapes, delicate materials, and rapidly changing surroundings, reducing effectiveness in applications such as fresh produce harvesting and mixed-SKU logistics operations. No single robotic platform offers universal functionality, often requiring multiple systems that increase operational complexity and investment.

Safety and liability concerns related to autonomous operation near humans, especially in hospitals and public spaces, create regulatory hesitation and customer reluctance. Dependence on machine-learning models that require frequent retraining across diverse conditions further increases maintenance complexity and skilled labor needs. These technological and safety challenges collectively limit scalability and slow broader market penetration.

Opportunity - Logistics Automation Penetration Gap Creating Scalable Growth Opportunities Through Accelerated AMR Adoption

Logistics automation represents a major growth opportunity for the Professional Service Robots Market, driven by extremely low warehouse robot penetration levels and rising fulfillment complexity. Less than 8% of warehouses in major economies currently deploy robotics, creating substantial headroom for Autonomous Mobile Robot adoption as e-commerce volumes, omnichannel retail models, and same-day delivery expectations intensify.

Persistent labor shortages and steady warehouse wage inflation strengthen the economic case for AMRs, with typical payback periods of under two years. Emerging markets, particularly in Asia Pacific, offer incremental growth as supply chains modernize and automation investments accelerate. Vendors offering integrated AMR platforms across picking, pallet handling, and sorting, combined with flexible Robots-as-a-Service financing models, can unlock adoption among cost-sensitive operators and rapidly scale addressable demand.

Collaborative Robots Enabling SME Automation and Broad-Based Industrial Adoption

Collaborative robots present a transformative opportunity by lowering automation barriers for small and mid-sized enterprises previously excluded from robotics adoption. Affordable entry pricing, fast return on investment, and simplified deployment enable widespread use across manufacturing, healthcare, agriculture, and service industries. The shift toward human-robot collaboration improves workforce acceptance and supports flexible automation in labor-constrained environments.

Expanding applications such as inspection, welding, harvesting, and service assistance demonstrate growing cross-industry relevance. Technological advances in AI-enabled vision, intuitive programming, and adaptive learning reduce dependence on specialized robotics expertise. Enhanced precision, improved quality outcomes, and certified safe human interaction strengthen value propositions, driving strong adoption momentum and long-term market expansion.

Category-wise Analysis

Robot Type Insights

Medical and healthcare service robots remain the leading robot type, accounting for an estimated 36% market share in 2025, primarily due to the entrenched dominance of surgical robotics. Robotic-assisted minimally invasive surgery has become a standard of care across major specialties, supported by strong clinical evidence of reduced recovery time, lower complication rates, and improved procedural precision. High procedural volumes and continuous system placements reinforce recurring demand for surgical platforms, instruments, and service contracts.

Beyond surgery, healthcare robots are expanding into patient care and rehabilitation, addressing long-term care needs arising from aging populations and chronic disease prevalence. Clear regulatory precedents and structured hospital procurement pathways further strengthen adoption, ensuring sustained capital allocation toward medical robotics infrastructure.

Mobility Insights

Mobile robots dominate the mobility segment with approximately 78% market share in 2025, driven by widespread adoption of Autonomous Mobile Robots in logistics and industrial environments. Their ability to navigate dynamically, operate continuously, and scale across facilities makes them the preferred automation solution for warehouses facing labor shortages and rising fulfillment complexity.

Mobile robots deliver strong economic returns through productivity gains, reduced labor dependency, and flexible deployment compared to fixed automation systems. Hardware robustness, payload capacity, and battery endurance remain key purchasing criteria for operators prioritizing throughput reliability. As e-commerce volumes grow and warehouse modernization accelerates, mobile robots are expected to remain the primary mobility platform underpinning professional service robot demand.

Application Insights

Healthcare and surgery represent the largest application segment, holding roughly 33% market share in 2025, supported by sustained growth in robotic-assisted surgical procedures. High procedure volumes and expanding surgeon familiarity reinforce long-term adoption across hospitals and specialty centers. Robotic systems enable consistent clinical outcomes, shorter hospital stays, and improved patient throughput, aligning with healthcare system efficiency goals.

Beyond operating rooms, healthcare applications increasingly include rehabilitation, patient mobility, telepresence, and disinfection, expanding the overall addressable market. Aging demographics and rising chronic disease burdens further support demand for automation in care delivery. Together, clinical validation and healthcare infrastructure investments secure healthcare’s position as the anchor application segment.

Usage Type Insights

Land-based robots overwhelmingly dominate usage types, capturing about 87% market share in 2025, driven by extensive deployment in healthcare facilities, warehouses, factories, and commercial environments. Wheeled land-based platforms offer superior stability, energy efficiency, payload handling, and ease of maintenance, making them ideal for indoor and semi-structured settings. Their adaptability across multiple tasks, such as transport, inspection, cleaning, and assistance, supports high utilization rates and faster return on investment. Compared to aerial or aquatic alternatives, land-based robots benefit from mature navigation technologies and established safety frameworks. As automation expands across service and industrial sectors, land-based robots will continue to represent the core operational backbone of the market.

Regional Insights

North America Professional Service Robots Market Trends and Insights

North America demonstrates strong growth supported by regulatory clarity, innovation leadership, and acute labor shortages. The United States anchors regional demand through FDA-defined approval pathways, evidenced by da Vinci 5 clearance in March 2024 and Medtronic Hugo RAS validation, accelerating hospital procurement cycles. Robotic-assisted surgeries reached 2.63 million procedures in the U.S. during 2024, reflecting 17% year-over-year growth and reinforcing recurring demand for systems, instruments, and service contracts.

Government-backed innovation via NSF and NIST sustains R&D intensity across intelligent robotics and automation. Structural labor shortages, including 2.1 million projected unfilled U.S. manufacturing jobs by 2030, drive automation adoption across healthcare, logistics, and manufacturing. In warehousing, less than 8% AMR penetration combined with rapid e-commerce expansion underpins strong growth potential, with the International Federation of Robotics projecting 31% annual growth in warehouse robot shipments through 2025.

Europe Professional Service Robots Market Trends and Insights

Europe retains a leading position with 42% global market share in 2025, supported by advanced industrial infrastructure, strong healthcare systems, and regulatory harmonization. Germany dominates with a 24.7% regional share, reflecting its precision manufacturing base and leadership in high-quality robotics production. The United Kingdom holds 15.8% share, driven by NHS England’s nationwide robotics initiative targeting 500,000 robotic-assisted surgeries annually by 2035, creating sustained demand for surgical systems and training services.

France accounts for 14.6% share, supported by healthcare automation, humanoid robot deployments, and patient assistance applications. EU policy support, including “Farm to Fork” subsidies, accelerates agricultural robot adoption across Spain, France, Italy, and the Netherlands. Mandatory infection-control investments and UV-C disinfection robot procurement further reinforce demand, sustaining premium pricing and long-term market stability.

Asia Pacific Professional Service Robots Market Trends and Insights

Asia Pacific emerges as the fastest-growing region, supported by government-backed automation, large addressable populations, and manufacturing cost advantages. China leads through “Made in China 2025” initiatives, extensive robotics manufacturing capacity, and biotech clusters in Shanghai, Shenzhen, and Beijing, strengthening domestic adoption and export competitiveness. Japan’s aging demographics, with 38% of the population projected to be over 65 by 2030, drive strong demand for surgical, rehabilitation, and eldercare robots addressing caregiver shortages.

India represents a high-growth market, with logistics and manufacturing automation attracting nearly US$ 10 billion in warehouse automation investments over the next five years. ASEAN countries including Vietnam, Thailand, and Singapore contribute incremental demand through healthcare modernization, smart manufacturing programs, and agricultural automation, positioning Asia Pacific as the primary volume-growth engine through 2033.

Competitive Landscape

The professional service robots market is characterized by a moderately to highly consolidated structure, where a limited number of established players control a significant share through scale advantages, mature product portfolios, and long-term customer contracts. Market leaders pursue vertical integration strategies encompassing hardware engineering, proprietary software platforms, data analytics, and lifecycle services, creating high switching costs and recurring revenue streams. Platform-based business models anchored in bundled sales of equipment, consumables, maintenance, and software subscriptions strengthen customer lock-in and support premium pricing.

Competitive differentiation increasingly centers on application-specific optimization rather than generalized robotics, with niche-focused participants targeting healthcare, logistics, sanitation, and human-assistance use cases through specialized functionality and regulatory alignment. Strategic mergers, acquisitions, and partnerships are used to expand technological capabilities, accelerate entry into adjacent applications, and consolidate fragmented subsegments, signaling market maturation. Additionally, new entrants from adjacent technology domains are reshaping competitive dynamics by leveraging scale, advanced AI capabilities, and alternative go-to-market models, intensifying pricing pressure and accelerating innovation cycles across the professional robotics ecosystem.

Key Developments

- May 2025: Amazon launched Vulcan tactile-sensing autonomous mobile robot in German warehouses, demonstrating advanced manipulation capability handling 75% of SKU profiles and 20-hour daily operating capacity, validating commercial viability of next-generation warehouse automation and threatening traditional logistics robotics supplier market positioning through technology leadership and aggressive market penetration.

- June 2025: National Health Service England established a comprehensive robotic surgery program committing to 500,000 robotic-assisted surgical procedures annually by 2035, representing governmental structural commitment to surgical robotics adoption at scale and establishing permanent healthcare infrastructure investment in professional surgical robots, validating long-term market growth trajectory.

- January 2026: Boston Dynamics unveiled production-ready electric Atlas humanoid robot for industrial tasks, featuring fast learning, adaptability, and autonomous operation, partnering with Google DeepMind to integrate Gemini AI for enhanced perception, reasoning, and interaction to revolutionize industries.

Companies Covered in Professional Service Robots Market

- ABB Ltd.

- Blue Ocean Robotics

- Boston Dynamics, Inc.

- Cyberdyne USA Inc.

- Daifuku Co., Ltd.

- Fanuc Corporation

- Gecko Robotics, Inc.

- Honda Motor Co., Ltd

- Intuitive Surgical, Inc.

- iRobot Corporation

- KUKA AG

- SoftBank Robotics Group

- Diligent Robotics, Inc.

- Harvest CROO Robotics LLC

- Aethon Inc.

- Medtronic (Hugo RAS)

- Amazon (Vulcan)

- CMR Surgical (Versius)

Frequently Asked Questions

The market is projected to reach approximately US$ 35.2 billion in 2026.

Growth is driven by structural labor shortages, rapid adoption of surgical robotics, and low logistics automation penetration below 8%.

Europe leads the market with about 42% share in 2025.

Warehouse logistics automation offers the largest opportunity due to low penetration and strong AMR shipment growth.

The Professional Service Robots Market is dominated by Intuitive Surgical, ABB, KUKA, Fanuc, Boston Dynamics, and others.