- Biotechnology

- Precision Medicine Market

Precision Medicine Market Size, Share, and Growth Forecast 2026 - 2033

Precision Medicine Market by Product & Service (Instruments, Consumables & Reagents, Software, Services), by Application (Oncology, Neurology, Immunology, Cardiovascular, Rare Diseases, Infectious Diseases, Others), by Technology (Gene Sequencing / NGS, Bioinformatics & Data Analytics, PCR & Molecular Diagnostics, Pharmacogenomics, AI-based Platforms), by End User (Hospitals & Clinics, Diagnostic Laboratories, Pharma & Biotech Companies, Research Institutes), by Regional Analysis, 2026-2033

Precision Medicine Market Size and Trend Analysis

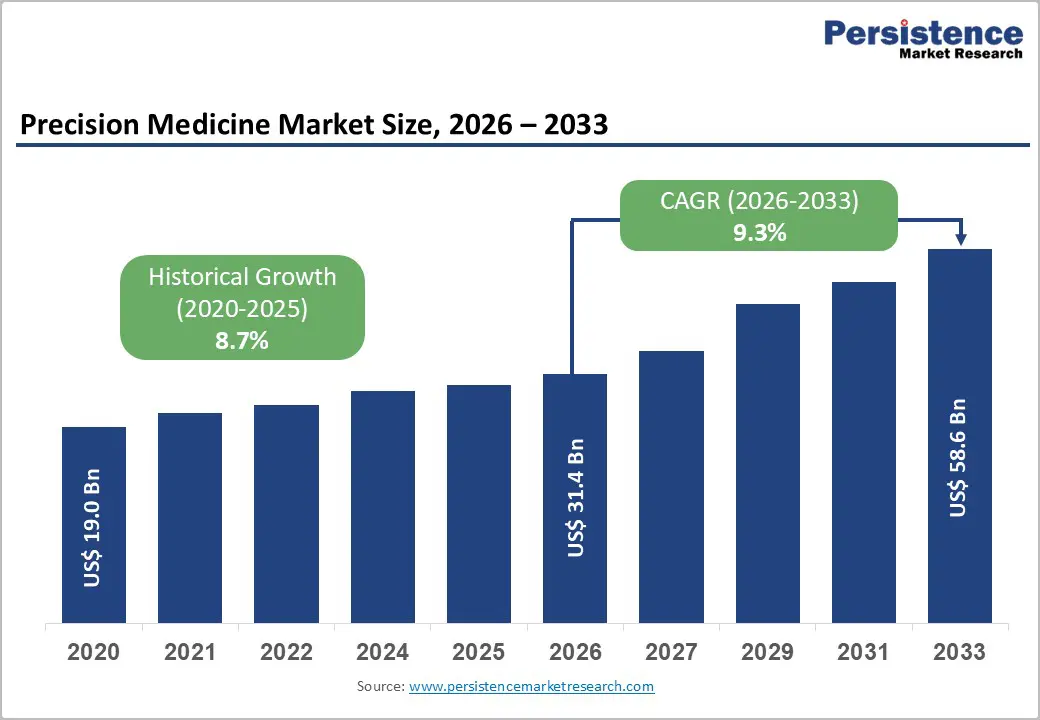

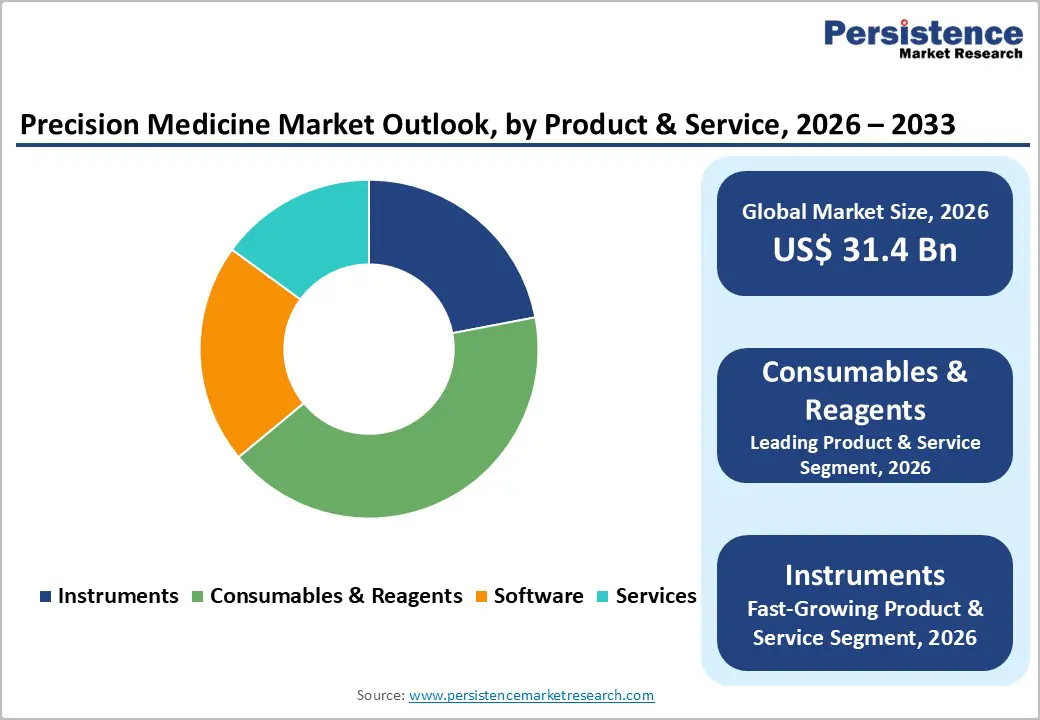

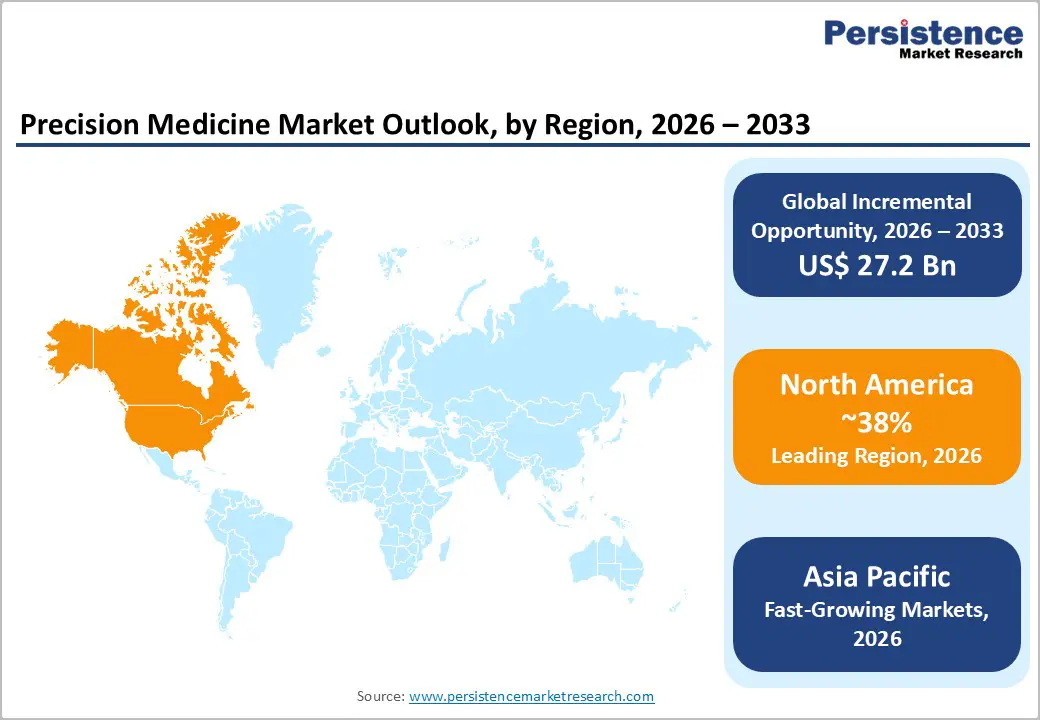

The global precision medicine market size is expected to be valued at US$ 31.4 billion in 2026 and projected to reach US$ 58.6 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

This robust expansion reflects the convergence of advanced genomic technologies, artificial intelligence-driven diagnostics, and targeted therapeutic platforms that are fundamentally transforming personalized healthcare delivery. The market's momentum is driven by increasing cancer incidence worldwide with approximately 20 million new cancer cases reported globally in 2022, according to the International Agency for Research on Cancer (IARC), and the proven clinical efficacy of biomarker-matched therapies that demonstrate 30-40% higher response rates compared to traditional treatment approaches as documented by NHS England. Furthermore, government initiatives such as the NIH's All of Us Research Program, which has enrolled over 297,000 participants and supported research by more than 2,300 researchers, underscore the strategic commitment to precision medicine infrastructure development across developed markets.

Key Market Highlights

- North America leads the precision medicine market (~38% share in 2025) due to NIH funding (All of Us Program), advanced healthcare infrastructure, and supportive regulatory frameworks.

- Asia Pacific is the fastest-growing region with highest CAGR through 2032, driven by government genomics initiatives (China, India), expanding middle class, and cost advantages for locally produced therapeutics.

- Consumables & Reagents hold market leadership (42% share in 2025) because of recurring demand in NGS and molecular diagnostics, with providers like Illumina supplying reagents for millions of tests annually.

- AI-based Platforms are the fastest-growing technology, enhancing genomic data analysis, reducing diagnostic errors (~20%), and enabling real-time predictive treatment optimization.

| Global Market Attributes | Key Insights |

|---|---|

| Precision Medicine Market Size (2026E) | US$ 31.4 Billion |

| Market Value Forecast (2033F) | US$ 58.6 Billion |

| Projected Growth CAGR (2026-2033) | 9.3% |

| Historical Market Growth (2020-2025) | 8.7% |

Market Dynamics

Market Growth Drivers

Accelerating Integration of Next-Generation Sequencing Technologies and Declining Genomic Testing Costs

Accelerating integration of next-generation sequencing (NGS) technologies and declining genomic testing costs is a major growth driver for the precision medicine market. Continuous improvements in sequencing speed, accuracy, and automation have made whole-genome, whole-exome, and targeted panel testing increasingly feasible in routine clinical practice rather than limited to research settings. At the same time, falling per-sample sequencing costs and reduced data-analysis expenses are lowering financial barriers for hospitals, diagnostic laboratories, and healthcare systems, enabling broader patient access to genomic profiling. This affordability supports earlier disease detection, improved risk stratification, and more precise selection of targeted therapies, particularly in oncology, rare genetic disorders, and pharmacogenomics. Integration of NGS into clinical workflows is also stimulating demand for companion diagnostics, bioinformatics platforms, and molecular testing services, creating a multiplier effect across the value chain. As governments and healthcare providers expand genomic programs and reimbursement coverage, NGS-driven testing is expected to further accelerate adoption of personalized treatment approaches globally.

Rising Prevalence of Chronic Diseases and Proven Efficacy of Companion Diagnostics in Treatment Optimization

Rising prevalence of chronic diseases such as cancer, cardiovascular disorders, diabetes, autoimmune conditions, and rare genetic illnesses is strongly accelerating adoption of precision medicine worldwide. Conventional “one-size-fits-all” therapies often show variable effectiveness and higher risk of adverse events, pushing healthcare systems toward more targeted treatment approaches. Precision medicine uses genetic, molecular, and biomarker information to stratify patients, enabling clinicians to select therapies most likely to deliver clinical benefit. Companion diagnostics play a central role in this shift by identifying specific mutations, protein expressions, or pathway activations that predict treatment response or resistance. Their proven ability to guide drug selection, dosing, and therapy sequencing improves outcomes, reduces trial-and-error prescribing, and helps avoid costly ineffective treatments. Growing clinical evidence, expanding regulatory approvals for biomarker-guided therapies, and payer interest in value-based care further reinforce demand. Together, the chronic disease burden and validated companion diagnostic utility create a strong, sustained growth engine for the global precision medicine market.

Market Restraints

High Implementation Costs and Infrastructure Requirements for Advanced Diagnostic Technologies

The capital-intensive nature of precision medicine implementation presents a significant barrier to widespread adoption, particularly in resource-constrained healthcare systems. Establishing comprehensive genomic testing facilities requires substantial investment in next-generation sequencing platforms, bioinformatics infrastructure, and specialized personnel training with initial setup costs often exceeding $5 million for full-service genomic laboratories. The manufacturing complexity of personalized therapies, exemplified by CAR-T cell treatments that involve labor-intensive ex vivo cell modification processes, results in treatment costs ranging from $373,000 to $475,000 per patient according to current market pricing. These economic barriers limit accessibility, creating healthcare inequity concerns highlighted by the fact that while North America commands over 50% of the global precision medicine market share, many emerging economies lack the diagnostic infrastructure for routine genomic testing.

Market Opportunities

Expanding Applications in Oncology Through CAR-T Cell Therapies and Multi-Omics Integration

Expanding applications in oncology through CAR-T cell therapies and multi-omics integration represent a major growth opportunity for the precision medicine market. CAR-T treatments rely on detailed genomic and immune profiling to identify suitable patients, design personalized cell constructs, and monitor response and toxicity, directly increasing demand for sequencing platforms, biomarker assays, and advanced analytics software. At the same time, multi-omics approaches combining genomics, transcriptomics, proteomics, metabolomics, and epigenomics enable a more complete understanding of tumor biology, resistance mechanisms, and disease progression, supporting highly tailored therapeutic strategies. This integrated data environment encourages pharmaceutical and biotechnology companies to invest in companion diagnostics, AI-driven interpretation tools, and real-time clinical decision-support systems. Hospitals and cancer centers are also upgrading laboratory infrastructure to support complex testing workflows, driving recurring revenues from consumables, reagents, and services. Together, CAR-T adoption and multi-omics profiling are accelerating the shift from one-size-fits-all oncology treatments toward individualized regimens, expanding both the clinical scope and commercial potential of precision medicine worldwide.

Artificial Intelligence-Driven Diagnostics and Real-World Data Integration for Treatment Optimization

Artificial intelligence and machine learning technologies are creating transformative opportunities for precision medicine by enabling rapid analysis of vast genomic and clinical datasets to generate actionable therapeutic insights. AI-powered diagnostic platforms have demonstrated the capability to reduce diagnostic errors by 20% according to the European Alliance for Personalised Medicine, while accelerating biomarker discovery and patient stratification processes that traditionally required months of manual analysis. Leading technology companies, including IBM Watson Health, are partnering with European hospitals to analyze electronic health records and predict treatment responses, exemplifying the commercial potential of AI-diagnostics integration.

Category-wise Insights

Product & Service Analysis

Consumables & Reagents dominate the precision medicine product & service segment, commanding approximately 42% market share in 2025, driven by their essential role in the recurring operational workflows of genomic testing laboratories and research institutions. This segment encompasses sequencing reagents, assay kits, sample preparation materials, and quality control consumables required for next-generation sequencing, polymerase chain reaction, and immunohistochemistry applications that form the backbone of precision diagnostics. The high-throughput nature of modern genomic testing facilities generates consistent demand for consumables, with leading providers like Illumina reporting that over 5 million genomic tests annually utilize their reagent systems. The market position is reinforced by the captive consumables business model employed by instrument manufacturers, where sequencing platforms are designed to function optimally with proprietary reagents, creating sustained revenue streams throughout equipment lifecycles.

Technology Analysis

Gene Sequencing / Next-Generation Sequencing (NGS) technology maintains market leadership with the largest share in 2025, reflecting its foundational role in enabling comprehensive genomic profiling that underpins precision medicine applications across oncology, rare diseases, and pharmacogenomics. The technology's dominant position stems from continuous performance improvements that have reduced sequencing costs by over 99.9% since the Human Genome Project, while simultaneously decreasing turnaround times and increasing data accuracy. Illumina's sequencing platforms, particularly the NovaSeq and MiSeq systems, have become the industry standard for clinical genomics, with the company serving over 4 million patients globally through precision medicine applications by 2025. The integration of NGS into newborn screening programs, exemplified by the GUARDIAN study identifying treatable conditions in 3.7% of screened infants, demonstrates the technology's expanding clinical utility beyond traditional cancer diagnostics.

End User Analysis

Hospitals & Clinics command the leading market share in the precision medicine end user segment for 2025, accounting for the majority of precision diagnostic testing and targeted therapy administration due to their comprehensive infrastructure and integrated care delivery capabilities. These institutions possess the advanced laboratory equipment, multidisciplinary care teams including molecular pathologists and genetic counselors, and electronic health record systems necessary to implement precision medicine workflows from genetic testing through treatment monitoring and outcome assessment. The segment's dominance is reinforced by the complex nature of many precision therapies, particularly CAR-T cell treatments, that require specialized administration facilities and intensive patient monitoring for cytokine release syndrome and neurotoxicity management, which limit administration to qualified hospital centers

Regional Insights

North America Precision Medicine Market Trends

North America continues to lead the precision medicine market due to its advanced healthcare infrastructure, strong biotechnology ecosystem, and early adoption of genomic and data-driven therapies. The region benefits from widespread availability of next-generation sequencing platforms, molecular diagnostics, and AI-enabled analytics that support personalized treatment decisions, particularly in oncology and rare diseases. Large-scale national genomics initiatives, growing use of companion diagnostics, and increasing clinical integration of pharmacogenomics are accelerating routine use of precision approaches across hospitals and cancer centers. Pharmaceutical and biotechnology companies in the region are heavily investing in targeted therapies, cell and gene therapies, and biomarker-based drug development, strengthening demand for integrated testing and data platforms. Supportive regulatory pathways for innovative diagnostics, expanding reimbursement coverage for genetic testing, and strong academic–industry collaborations further reinforce regional leadership. In addition, rising awareness among clinicians and patients about personalized care, along with digital health integration into clinical workflows, is positioning North America as a hub for innovation, commercialization, and large-scale adoption of precision medicine solutions.

Asia Pacific Precision Medicine Market Trends

Asia Pacific is emerging as a high-growth region in the precision medicine market, driven by expanding healthcare access, rising cancer burden, and rapid adoption of genomic technologies across major economies. Countries such as China, Japan, South Korea, India, and Australia are investing heavily in national genomics programs, biobanks, and digital health infrastructure to support population-scale sequencing and personalized treatment strategies. Increasing availability of next-generation sequencing platforms, declining testing costs, and the growth of local biotechnology startups are making precision diagnostics more accessible to hospitals and diagnostic laboratories. Pharmaceutical companies are also strengthening regional R&D and clinical trial activity, using genetic insights to develop targeted therapies suited to diverse patient populations. Government initiatives promoting innovation, regulatory modernization, and public–private collaborations are accelerating the commercialization of companion diagnostics and biomarker-based therapies. Alongside these developments, expanding oncology care networks and rising clinician awareness of individualized treatment approaches are positioning Asia Pacific as a rapidly advancing hub for precision medicine adoption and long-term market expansion.

Competitive Landscape

Market Structure Analysis

The competitive landscape of the Precision Medicine Market is dynamic and moderately concentrated, with a mix of large multinational pharmaceutical, biotechnology, and diagnostics companies shaping industry direction. Leading players such as Roche, Illumina, Thermo Fisher Scientific, Novartis, and Pfizer leverage strong R&D, broad product portfolios, and strategic collaborations to maintain market dominance and expand precision diagnostics and targeted therapies. Mid-sized firms and specialized biotech companies also compete by focusing on niche technologies like liquid biopsies, AI-driven analytics, and multi-omics platforms, fostering innovation and differentiation. The landscape is further characterized by mergers, acquisitions, and partnerships that accelerate technology integration and clinical adoption, while emerging regional players enhance competition by offering cost-effective, locally tailored solutions.

Key Market Developments

- In February 2026, SEQSTER, a leading healthcare technology company providing the data connection, collection, and orchestration layer for patient health information, and Praxis Precision Medicines, Inc., announced the expansion of their successful partnership to accelerate clinical trials, data collection, and real-world evidence generation across Praxis’s clinical development programs.

Companies Covered in Precision Medicine Market

- Pfizer Inc.

- Bristol Myers Squibb

- Hoffmann-La Roche Ltd.

- Novartis AG

- AstraZeneca

- Merck KGaA

- Eli Lilly and Company

- GlaxoSmithKline plc

- Sanofi

- Johnson & Johnson

- Amgen, Inc.

- Gilead Sciences, Inc.

- AbbVie Inc.

Frequently Asked Questions

The global precision medicine market is expected to be valued at US$ 31.4 billion in 2026.

Cancer, cardiovascular, neurological, and rare genetic disorders increase demand for personalized treatments.

North America leads the global precision medicine market with approximately 38% market share in 2025, driven by the region's unparalleled biomedical innovation ecosystem centered in the United States.

The highest growth potential in the precision medicine market lies in CAR-T cell therapies and advanced immuno-oncology treatments. This segment is expanding rapidly due to breakthroughs in allogeneic “off-the-shelf” CAR-T products, dual-antigen targeting strategies that reduce tumor escape, and regulatory approvals extending beyond hematologic cancers to solid tumors.

Leading precision medicine market players include Roche, Illumina, Thermo Fisher Scientific, Qiagen, Novartis.