- Executive Summary

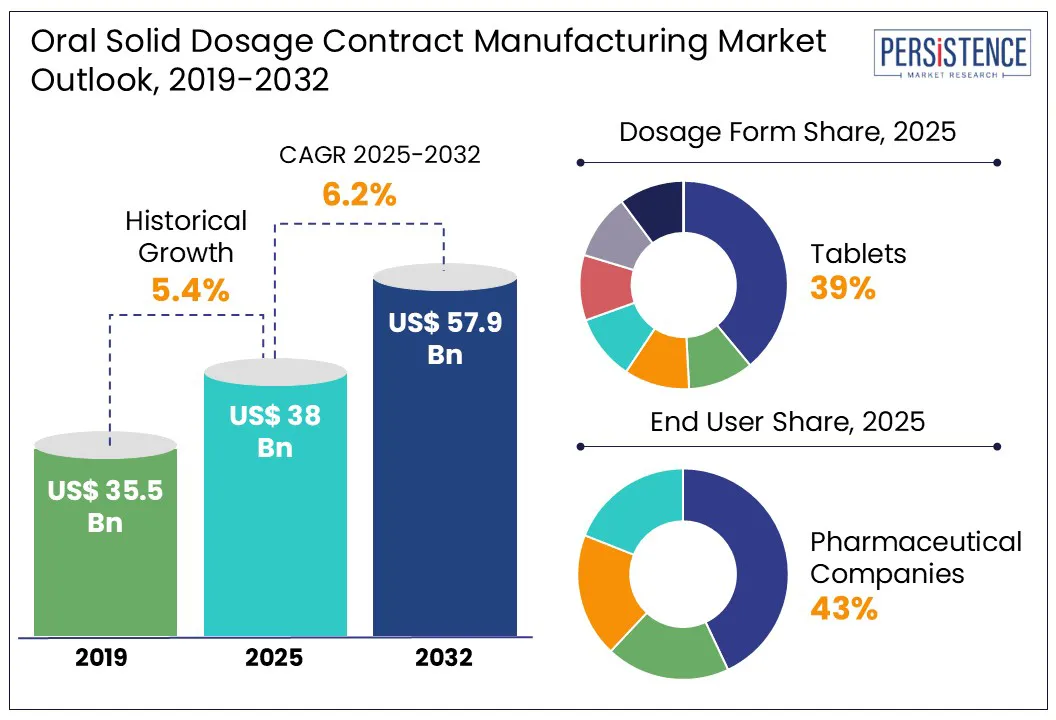

- Global Oral Solid Dosage Contract Manufacturing Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Mn

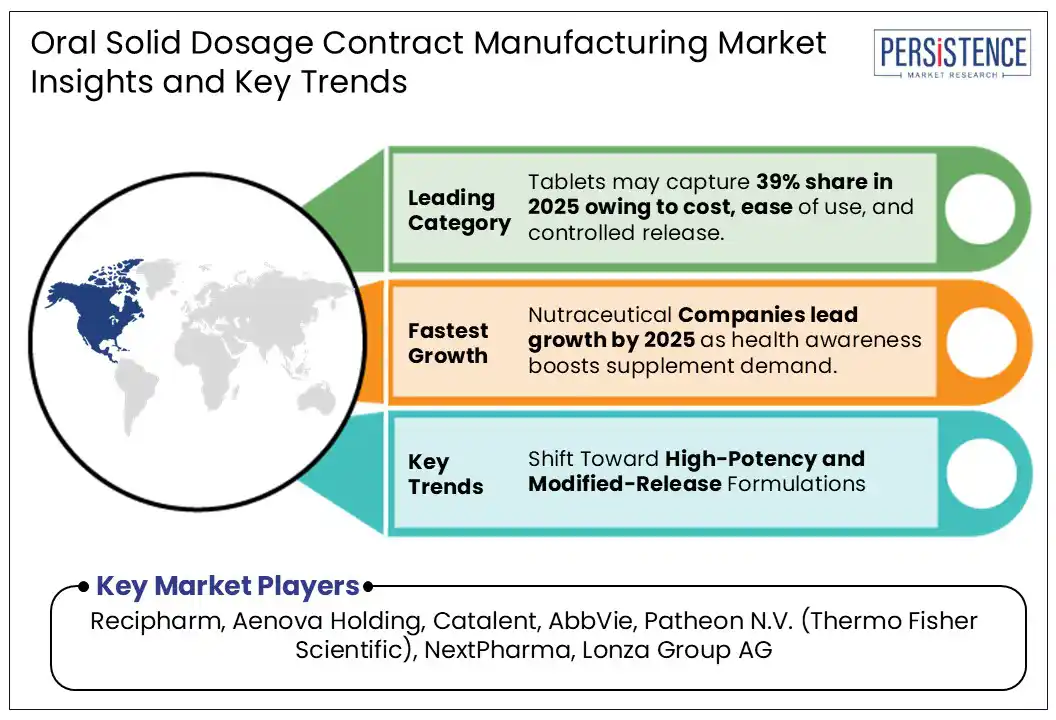

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Regulatory Landscape

- Product Adoption Analysis

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, 2025-2032

- Global Oral Solid Dosage Contract Manufacturing Market Outlook: Dosage Form

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Dosage Form, 2019 - 2024

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Attractiveness Analysis: Dosage Form

- Global Oral Solid Dosage Contract Manufacturing Market Outlook: Mechanism

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Mechanism, 2019 - 2024

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Attractiveness Analysis: Mechanism

- Global Oral Solid Dosage Contract Manufacturing Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Application, 2019 - 2024

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Attractiveness Analysis: Application

- Global Oral Solid Dosage Contract Manufacturing Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By End User, 2019 - 2024

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Oral Solid Dosage Contract Manufacturing Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Region, 2019 - 2024

- Market Size (US$ Mn) Analysis and Forecast, By Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- U.S.

- Canada

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- Europe Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- East Asia Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- China

- Japan

- South Korea

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- South Asia & Oceania Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- Latin America Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- Middle East & Africa Oral Solid Dosage Contract Manufacturing Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019 - 2024

- By Country

- By Dosage Form

- By Mechanism

- By Application

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Mn) Analysis and Forecast, By Dosage Form, 2025 - 2032

- Tablets

- Capsules

- Softgels

- Powders

- Granules

- Gummies

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Mechanism, 2025 - 2032

- Immediate Release

- Delayed Release

- Controlled Release

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025 - 2032

- Drug Product Development

- Fill & Finish Product Manufacturing

- Packaging /Labelling

- Others

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025 - 2032

- Pharmaceutical Companies

- Biopharmaceutical Companies

- Emerging/Virtual Pharma Companies

- Nutraceutical Companies

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Recipharm

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Aenova Holding

- Catalent

- AbbVie

- Patheon N.V. (Thermo Fisher Scientific)

- NextPharma

- Lonza Group AG

- Merck KGaA

- Aurobindo Pharma Limited

- Siegfried AG

- Piramal Pharma Solutions

- Corden Pharma

- HERMES PHARMA GmbH

- Medipaams India Private Limited

- Alpex Pharma

- Abaris Healthcare Pvt Ltd

- Ardena Holdings N.V

- Aphena Pharma Solutions

- Actiza Pharmaceutical Private Limited

- Sunwin Healthcare PVT. LTD

- Kosher Pharmaceuticals

- Boehringer Ingelheim BioXcellence

- Others

- Recipharm

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment