- Executive Summary

- Global Multiple Orifice Flow Control Valve Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Multiple Orifice Flow Control Valve Market Outlook: Valve Diameter

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Valve Diameter, 2020-2025

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- Market Attractiveness Analysis: Valve Diameter

- Global Multiple Orifice Flow Control Valve Market Outlook: Operation

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Operation, 2020-2025

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- Market Attractiveness Analysis: Operation

- Global Multiple Orifice Flow Control Valve Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by End User, 2020-2025

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- Market Attractiveness Analysis: End User

- Global Multiple Orifice Flow Control Valve Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Mn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- North America Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- Europe Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- Europe Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- East Asia Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- East Asia Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- South Asia & Oceania Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- South Asia & Oceania Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- Latin America Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- Latin America Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- Middle East & Africa Multiple Orifice Flow Control Valve Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Valve Diameter, 2026-2033

- Less than 4"

- 4" - 6"

- 6" - 12"

- 12" - 24"

- 24" - 40"

- Above 40"

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by Operation, 2026-2033

- Manual

- Automatic

- Electric Actuators

- Pneumatic Actuators

- Hydraulic Actuators

- Middle East & Africa Market Size (US$ Mn) and Volume (Units) Forecast, by End User, 2026-2033

- Oil & Gas

- Chemicals & Petrochemicals

- Energy & Power

- Industrial Process

- HVAC & Tankless Heaters

- Water & Wastewater

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Parker Hannifin Corp.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Emerson Electric Co.

- Metso Corporation

- BHGE (BAKER HUGHES, a GE Company)

- Kurimoto, Ltd.

- Watts Water Technologies, Inc.

- Azbil Corporation

- KUBOTA Corporation

- Flowserve Corporation

- IMI Plc.

- NOW Inc.

- Ross Valve Mfg. Co Inc.

- Rototherm Group

- AGI Industries

- Doering Company

- Cameron International Corporation

- Crane Co.

- Curtiss-Wright Corporation

- Velan Inc.

- SAMSON AG

- Parker Hannifin Corp.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automation & Robotics

- Multiple Orifice Flow Control Valve Market

Multiple Orifice Flow Control Valve Market Size, Share, and Growth Forecast 2026 - 2033

Multiple Orifice Flow Control Valve Market by Valve Diameter (Less than 4

Multiple Orifice Flow Control Valve Market Size and Trend Analysis

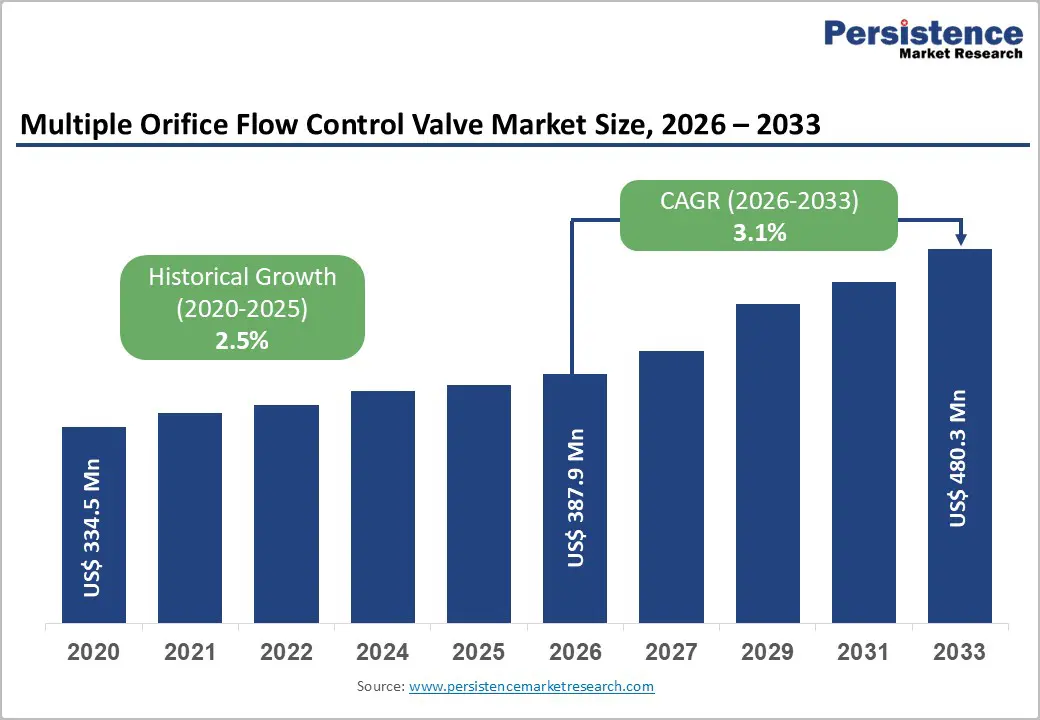

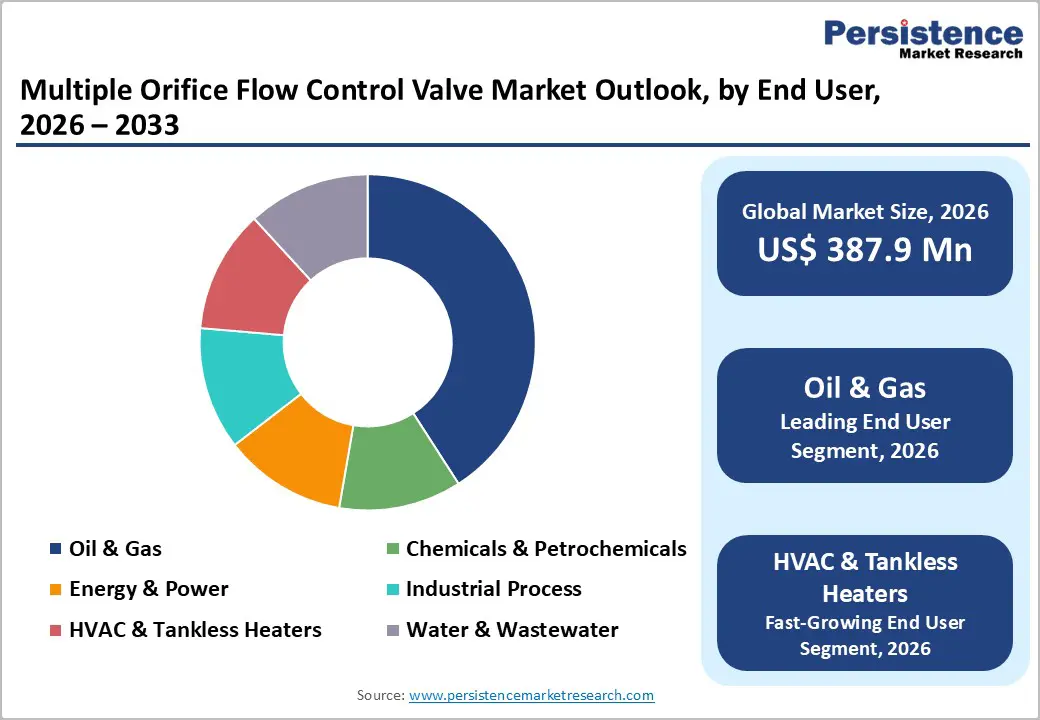

The global multiple orifice flow control valve market size is expected to be valued at US$ 387.9 million in 2026 and projected to reach US$ 480.3 million by 2033, growing at a CAGR of 3.1% between 2026 and 2033.

Market expansion is primarily driven by increased investment in oil and gas infrastructure, growing demand for energy-efficient flow-control solutions in industrial processes, and rising adoption of automated valve systems in chemical and petrochemical facilities. The proliferation of smart manufacturing initiatives and stringent regulations governing operational safety and emissions control are compelling industries to upgrade their fluid-handling systems with advanced multi-orifice flow-control valves that provide superior pressure reduction and flow-management capabilities.

Key Industry Highlights:

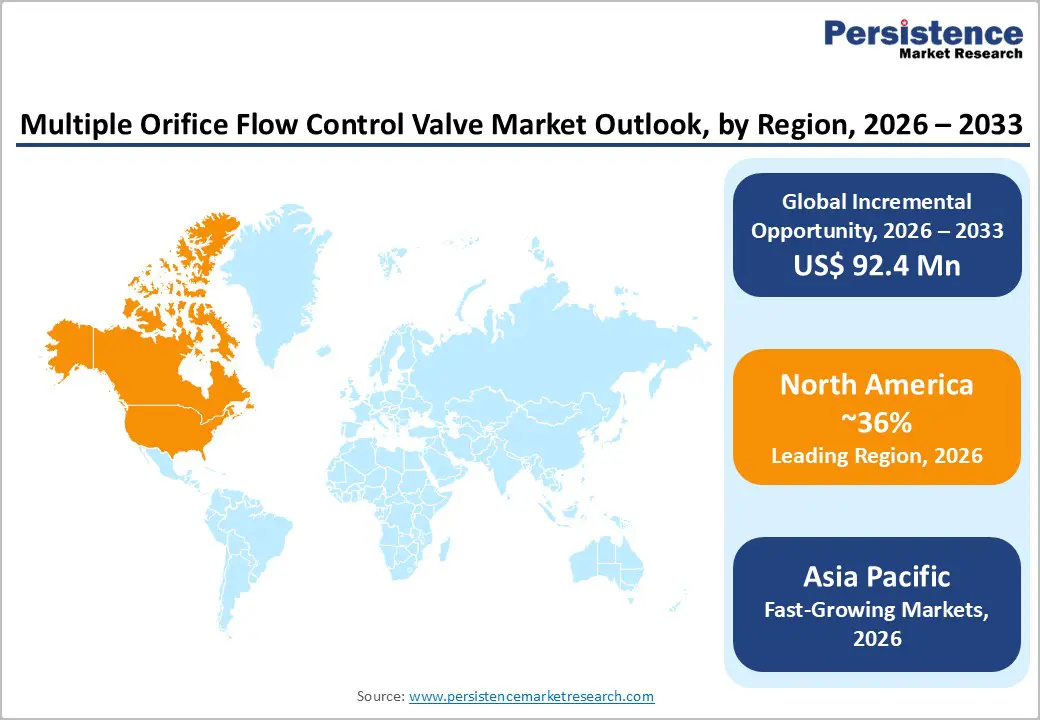

- Leading Region: North America leads the market with around 36% share in 2025, supported by extensive oil and gas pipeline networks, stringent regulatory frameworks, and sustained investments in industrial modernization and energy infrastructure across the U.S. and Canada.

- Fastest-Growing Region: Asia Pacific is projected to register a 4.5% CAGR during 2026 - 2033, driven by rapid industrialization in China and India, rising infrastructure spending, expanding chemical capacity, and increasing water treatment demand.

- Dominant Segment: The 6"-12" diameter segment accounts for nearly 32% of the market in 2025, owing to its widespread use in oil and gas transmission, chemical processing, and industrial applications that require an optimal balance between flow efficiency and installation feasibility.

- Fastest-Growing Segment: Automatic operation is the fastest-growing segment, projected to grow at a 4.2% CAGR through 2033, driven by industrial automation, Industry 4.0 adoption, remote monitoring needs, and the increasing use of electric and pneumatic actuators.

- Key Opportunity: Market opportunities are strengthened by global water infrastructure investments projected at US$1.7 trillion annually by 2030 and by the expansion of the hydrogen and renewable energy sectors, which are driving demand for advanced multi-orifice flow control valves.

| Key Insights | Details |

|---|---|

| Multiple Orifice Flow Control Valve Market Size (2026E) | US$ 387.9 million |

| Market Value Forecast (2033F) | US$ 480.3 million |

| Projected Growth CAGR (2026 - 2033) | 3.1% |

| Historical Market Growth (2020 - 2025) | 2.5% |

Market Dynamics

Drivers - Accelerating Infrastructure Development in the Oil and Gas Sector

The global oil and gas industry continues to incur substantial capital expenditures in upstream, midstream, and downstream infrastructure, driving significant demand for multiple-orifice flow-control valves. According to the International Energy Agency (IEA), global oil and gas investment reached approximately US$ 525 billion in 2024, with substantial allocations toward pipeline infrastructure and processing facilities. Multiple-orifice flow-control valves are essential components in these installations, providing precise pressure reduction across multiple stages, which is critical for maintaining system integrity and operational efficiency.

The U.S. Energy Information Administration (EIA) reported that natural gas pipeline capacity additions in North America exceeded 8 billion cubic feet per day in 2024, necessitating advanced flow control solutions. Furthermore, the expansion of liquefied natural gas terminals and offshore production platforms requires robust valve systems capable of handling high-pressure differentials, with multiple orifice valves often used for flow regulation in harsh operating environments.

Growing Emphasis on Industrial Process Automation and Efficiency

Industrial facilities worldwide are increasingly adopting automated flow control systems to enhance operational efficiency, reduce energy consumption, and minimize manual intervention. The International Society of Automation (ISA) estimates that industrial automation spending exceeded US$ 200 billion globally in 2024, with significant portions allocated to process control instrumentation, including automated valve systems. Multiple-orifice flow-control valves equipped with electric, pneumatic, or hydraulic actuators enable precise flow modulation, rapid response to process variations, and seamless integration with distributed control systems.

The International Organization for Standardization (ISO) standards for industrial automation, particularly ISO 50001 for energy management systems, are encouraging manufacturers to implement energy-efficient flow control solutions. Chemical processing plants, water treatment facilities, and power generation stations are increasingly specifying automated multiple orifice valves to achieve tighter process control, reduce operational costs, and comply with environmental regulations governing emissions and waste management.

Restraint - High Initial Investment and Maintenance Costs

Multiple-orifice flow-control valves entail a significant capital expenditure compared with conventional single-stage valves, particularly for larger-diameter configurations and automated variants. The U.S. Department of Energy notes that advanced flow control systems can account for 15-20% of total process equipment costs in industrial facilities. The complexity of multiple-orifice designs, precision manufacturing requirements, and the integration of actuator systems contribute to elevated procurement costs that can deter adoption in cost-sensitive industries.

Additionally, maintenance expenses for periodic inspections, actuator calibration, and replacement of internal components increase the total cost of ownership. Small and medium-sized enterprises in developing regions often lack the financial resources to invest in premium valve solutions and instead opt for basic manual valves despite their operational limitations. The economic uncertainty and volatile commodity prices further constrain capital investment decisions in industries such as oil and gas and chemicals.

Technical Complexity and Skilled Workforce Requirements

The installation, operation, and maintenance of multiple-orifice flow-control valves require specialized technical expertise that is increasingly scarce in industrial sectors. According to the National Association of Manufacturers, more than 77% of manufacturing companies in the United States reported difficulty attracting and retaining qualified technical personnel in 2024. Multiple orifice valves require precise sizing calculations, careful selection of trim configurations, and proper integration with control systems to achieve optimal performance. Improper installation or inadequate maintenance can lead to premature failure, process disruptions, and safety hazards.

The American Petroleum Institute (API) standards for valve installation and maintenance necessitate comprehensive training programs that many organizations struggle to implement. Furthermore, the transition from manual to automated valve systems requires workforce retraining and adaptation to digital control interfaces, creating organizational resistance and implementation delays that hinder market penetration, particularly in regions with limited access to technical education and vocational training programs.

Opportunities - Expansion in Water and Wastewater Treatment Infrastructure

Global water scarcity and aging infrastructure are driving unprecedented investment in water and wastewater treatment facilities, creating substantial opportunities for manufacturers of multiple-orifice flow-control valves. The World Bank estimates that annual investment in water infrastructure must reach US$1.7 trillion globally to meet the Sustainable Development Goals by 2030. Multiple orifice valves are essential in water treatment applications for controlling flow rates, managing pressure differentials across filtration systems, and regulating chemical dosing processes.

The United States Environmental Protection Agency (EPA) allocated US$11.7 billion under the Bipartisan Infrastructure Law in 2024 for water infrastructure improvements, with a significant portion directed to treatment plant upgrades. Desalination facilities, which are expanding rapidly in water-stressed regions, including the Middle East and North Africa, require specialized flow-control valves capable of handling corrosive seawater and high-pressure reverse-osmosis systems. Municipal water utilities are increasingly specifying automated valve systems with remote monitoring capabilities to enhance operational efficiency and reduce water losses, positioning multiple-orifice flow-control valves as critical components of modern water management infrastructure.

Emerging Demand from Renewable Energy and Hydrogen Economy

The global transition toward renewable energy sources and the development of a hydrogen economy present significant growth opportunities for specialized flow-control valve applications. According to the International Renewable Energy Agency (IRENA), global renewable energy capacity additions reached 473 gigawatts in 2024, with concentrated solar power, geothermal, and bioenergy facilities requiring sophisticated thermal management and fluid control systems. Multiple-orifice flow-control valves are particularly suited to geothermal applications, where precise pressure reduction and flow distribution are critical to system longevity and efficiency.

The emerging hydrogen sector, projected by the Hydrogen Council to represent a US$2.5 trillion market opportunity by 2050, requires specialized valve solutions for hydrogen production, storage, and distribution systems. Electrolysis facilities, hydrogen compression stations, and fuel cell applications require flow-control valves engineered for hydrogen service, with specific material selections and sealing technologies. The U.S. Department of Energy's Hydrogen Shot initiative aims to reduce clean hydrogen costs to US$1 per kilogram by 2030, thereby stimulating infrastructure development that will drive demand for specialized multi-orifice flow-control valves for hydrogen applications.

Category-wise Analysis

Valve Diameter Insights

The 6”-12” valve diameter segment holds a leading market position, with an estimated 32% share in 2025, driven by extensive use across oil and gas pipelines, chemical plants, and core industrial processes. This diameter range aligns well with standard pipeline specifications, particularly in crude oil and natural gas transmission systems, where it balances flow efficiency with manageable installation and maintenance requirements. Industry infrastructure data indicate that most transmission pipelines operate within this size range, directly driving valve demand. Additionally, chemical and petrochemical facilities favor 6”-12” valves to support system standardization, reduce inventory complexity, and optimize lifecycle costs, reinforcing the segment’s sustained dominance.

Operation Insights

The automatic operation segment dominates the market with approximately 58% share in 2025 and remains the fastest-growing category, driven by rising adoption of industrial automation and digital process control. Automated valves are increasingly specified as standard equipment in new industrial installations due to their ability to enhance operational efficiency, safety, and process consistency. This segment benefits from growing emphasis on remote operation, real-time monitoring, and predictive maintenance across energy, manufacturing, and utilities. Compliance with global automation and control standards further accelerates deployment by enabling seamless integration with distributed control systems. As industries continue to prioritize reduced manual intervention and greater reliability, automatic valves are expected to remain central to flow-control modernization strategies.

End-user Insights

The oil and gas sector leads end-user demand, accounting for around 38% of the market in 2025, reflecting its heavy reliance on robust, precise flow-control solutions. Extensive upstream, midstream, and downstream infrastructure requires valves capable of handling high pressures, fluctuating flow rates, and corrosive media. Multiple-orifice valves are critical for pressure reduction, flow regulation, and erosion control across pipelines, processing units, and refining operations. Strict adherence to international performance and safety standards further supports their adoption in this sector. Continued investments in pipeline expansion, offshore production, LNG facilities, and unconventional resource development are expected to sustain strong demand from oil and gas operators over the forecast period.

Regional Insights

North America Multiple Orifice Flow Control Valve Market Trends and Insights

North America commands the leading regional position with approximately 36% market share in 2025, driven by extensive oil and gas infrastructure, advanced industrial manufacturing capabilities, and stringent regulatory frameworks governing operational safety and environmental protection. The United States dominates regional demand, supported by the world's largest network of petroleum pipelines, which exceeds 190,000 miles, according to the Pipeline and Hazardous Materials Safety Administration (PHMSA). The U.S. Department of Energy reports continued investment in pipeline modernization and expansion projects, particularly for natural gas transportation infrastructure supporting increased liquefied natural gas export capacity.

The regulatory environment significantly influences valve specifications, with American Petroleum Institute (API) standards and American Society of Mechanical Engineers (ASME) codes mandating rigorous performance requirements for pressure-containing equipment. The U.S. Environmental Protection Agency's emission control regulations and the Occupational Safety and Health Administration's workplace safety standards require industries to implement advanced flow control systems with leak-prevention capabilities and automated shutdown features. Canada's oil sands development and expanding pipeline infrastructure contribute substantially to regional valve demand, while Mexico's energy sector reforms and industrial growth support market expansion across North America.

Europe Multiple Orifice Flow Control Valve Market Trends and Insights

Europe represents a mature market characterized by stringent regulatory harmonization, emphasis on energy efficiency, and substantial investment in industrial modernization and water infrastructure. The European Union's Industrial Emissions Directive and the Pressure Equipment Directive (PED) 2014/68/EU establish comprehensive safety and environmental standards that influence valve design and specification requirements across member states. Germany leads regional demand, leveraging its advanced chemical and automotive manufacturing sectors, which require sophisticated flow-control solutions, as evidenced by the German Engineering Federation (VDMA) reporting over €45 billion in process equipment investment in 2024.

The United Kingdom's North Sea oil and gas sector, despite maturation, continues to require specialized valve solutions for offshore platforms and subsea infrastructure, while the country's water utilities invest heavily in infrastructure renewal in response to Ofwat regulatory mandates. France demonstrates growing adoption in nuclear power applications and chemical manufacturing, with the French Alternative Energies and Atomic Energy Commission (CEA) specifying advanced flow control systems for next-generation reactor designs. Spain's expanding desalination capacity, driven by water scarcity concerns in Mediterranean regions, creates opportunities for corrosion-resistant multiple orifice valves. The European emphasis on carbon neutrality and the European Green Deal initiatives are stimulating investment in hydrogen infrastructure and renewable energy projects, which will drive future valve demand.

Asia Pacific Multiple Orifice Flow Control Valve Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market, with an anticipated CAGR of 4.5% during 2026-2033, driven by rapid industrialization, infrastructure development, and expanding energy demand in emerging economies. China dominates regional consumption, supported by massive investments in oil and gas infrastructure, chemical manufacturing capacity, and water treatment facilities as documented by the National Development and Reform Commission (NDRC), which allocated over US$ 150 billion for energy infrastructure in 2024. The country's Belt and Road Initiative continues to drive pipeline construction projects across Central Asia and Southeast Asia, creating substantial opportunities for valve procurement.

Japan's advanced manufacturing sector and its emphasis on precision engineering support demand for high-performance valve systems, as reported by the Japan Valve Manufacturers Association, which reports steady growth in industrial valve production. India represents a high-growth opportunity market, driven by government initiatives including the Jal Jeevan Mission for universal water supply coverage and ambitious targets for oil and gas infrastructure expansion announced by the Ministry of Petroleum and Natural Gas. The ASEAN region demonstrates accelerating industrialization with countries including Vietnam, Indonesia, and Thailand expanding chemical manufacturing, power generation, and water treatment infrastructure.

Competitive Landscape

The global multiple orifice flow control valve market exhibits moderate consolidation with established multinational manufacturers commanding significant market share through extensive product portfolios, global distribution networks, and strong brand recognition. Leading companies leverage technological innovation, strategic acquisitions, and regional manufacturing capabilities to maintain competitive advantages in this specialized market segment. Market participants are increasingly focusing on product customization capabilities to address specific application requirements across diverse end-user industries, while simultaneously investing in automated valve systems incorporating digital connectivity and predictive maintenance features.

The competitive environment emphasizes technical expertise, adherence to international standards including API, ASME, and ISO specifications, and the ability to provide comprehensive engineering support and after-sales service. Companies are pursuing strategic partnerships with engineering, procurement, and construction firms to secure positions on major infrastructure projects and to expand service capabilities to capture maintenance and retrofit opportunities in aging industrial facilities.

Key Developments

- January 2026 - Emerson releases DeltaV version 16.LTS is advancing its software-defined automation platform to reduce costs, enhance operational intelligence, improve enterprise data visibility, and strengthen cybersecurity across industrial control environments.

Companies Covered in Multiple Orifice Flow Control Valve Market

- Parker Hannifin Corp.

- Emerson Electric Co.

- Metso Corporation

- BHGE (BAKER HUGHES, a GE Company)

- Kurimoto, Ltd.

- Watts Water Technologies, Inc.

- Azbil Corporation

- KUBOTA Corporation

- Flowserve Corporation

- IMI Plc.

- NOW Inc.

- Ross Valve Mfg. Co Inc.

- Rototherm Group

- AGI Industries

- Doering Company

- Cameron International Corporation

- Crane Co.

- Curtiss-Wright Corporation

- Velan Inc.

- SAMSON AG

Frequently Asked Questions

The multiple orifice flow control market is expected to reach approximately US$ 387.9 million in 2026.

Demand is driven by oil and gas infrastructure expansion, rising industrial automation adoption, and increasing focus on energy-efficient flow control.

North America leads the market with about 36% share, supported by strong pipeline infrastructure and strict regulatory standards.

Key opportunities arise from water infrastructure investments, hydrogen economy development, and renewable energy expansion.

Major players include Emerson Electric, Parker Hannifin, Flowserve, Baker Hughes, Metso, IMI, Watts Water Technologies, Kubota, and Azbil.