- Media & Entertainment

- Mobile Advertising Market

Mobile Advertising Market Size, Share, and Growth Forecast 2026 – 2033

Mobile Advertising Market Size, Share, and Growth Forecast 2026 – 2033 by Ad Format (Search Ads, Display Ads, Video Ads, Native Ads, Interstitial Ads, Others), by Platform (In‑App Advertising, Mobile Web Advertising, Social Media Advertising, Mobile Search Advertising, Messaging App Advertising, Mobile Video Advertising), by Technology, by End Use, by Regional Analysis, 2026–2033

Mobile Advertising Market Size and Trend Analysis

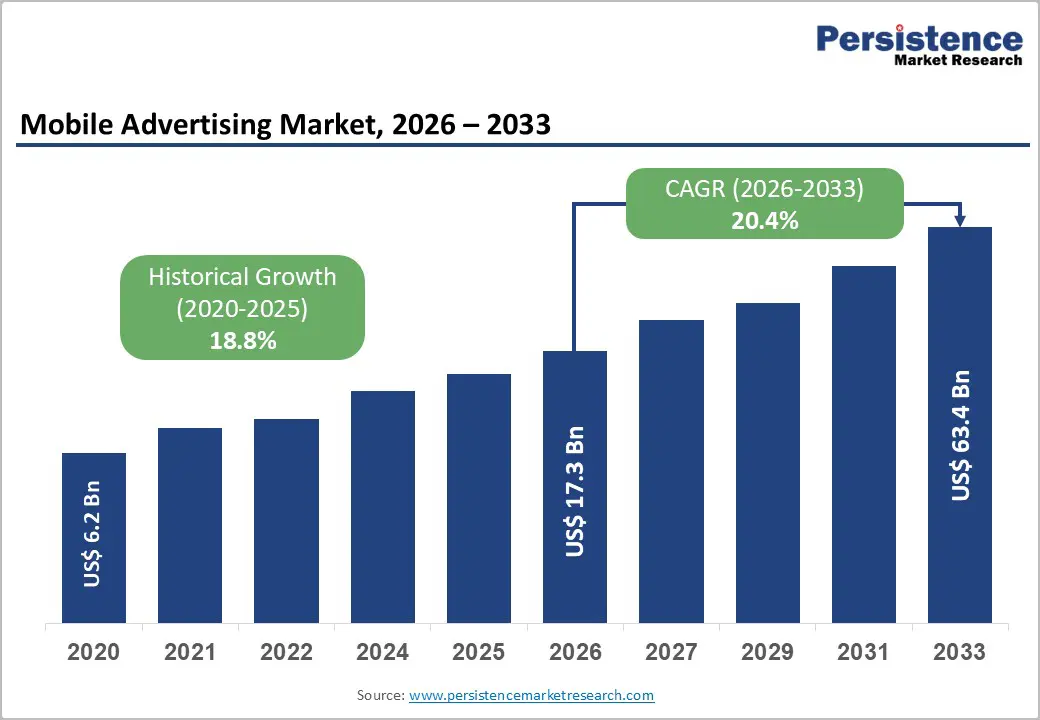

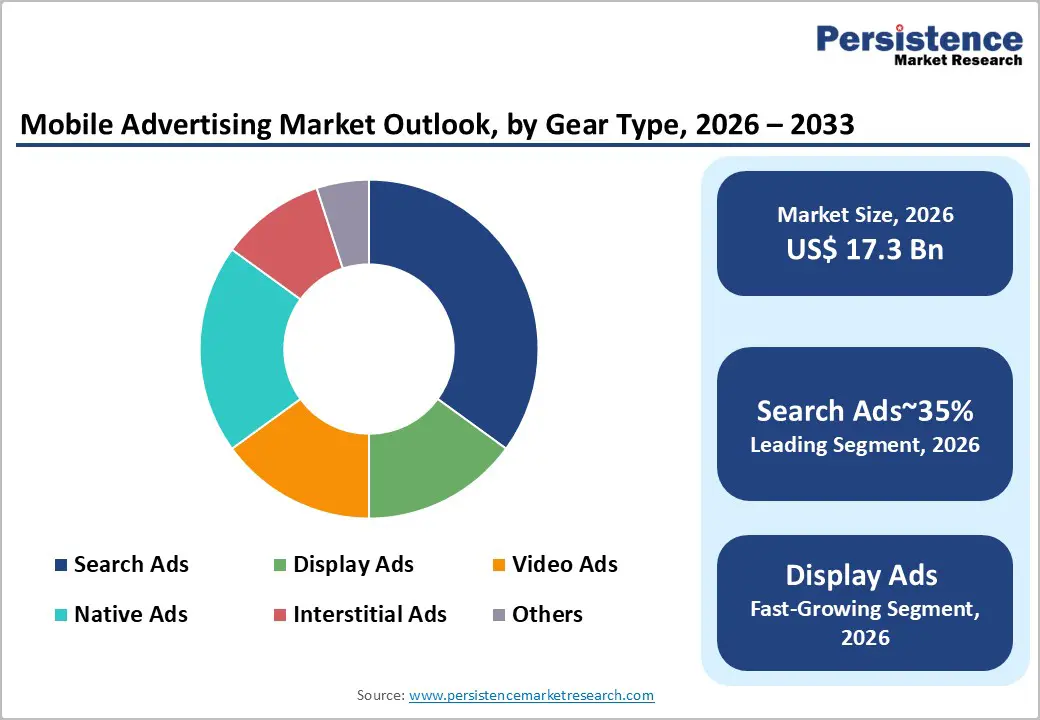

The global Mobile Advertising Market is projected to reach US$ 17.3 billion in 2026 and US$ 63.4 billion by 2033, growing at a CAGR of 20.4% over the forecast period. This explosive growth is driven by rising smartphone penetration, mobile-first consumer behavior, and the rapid expansion of in-app, social, and video advertising ecosystems.

Key Market Highlights

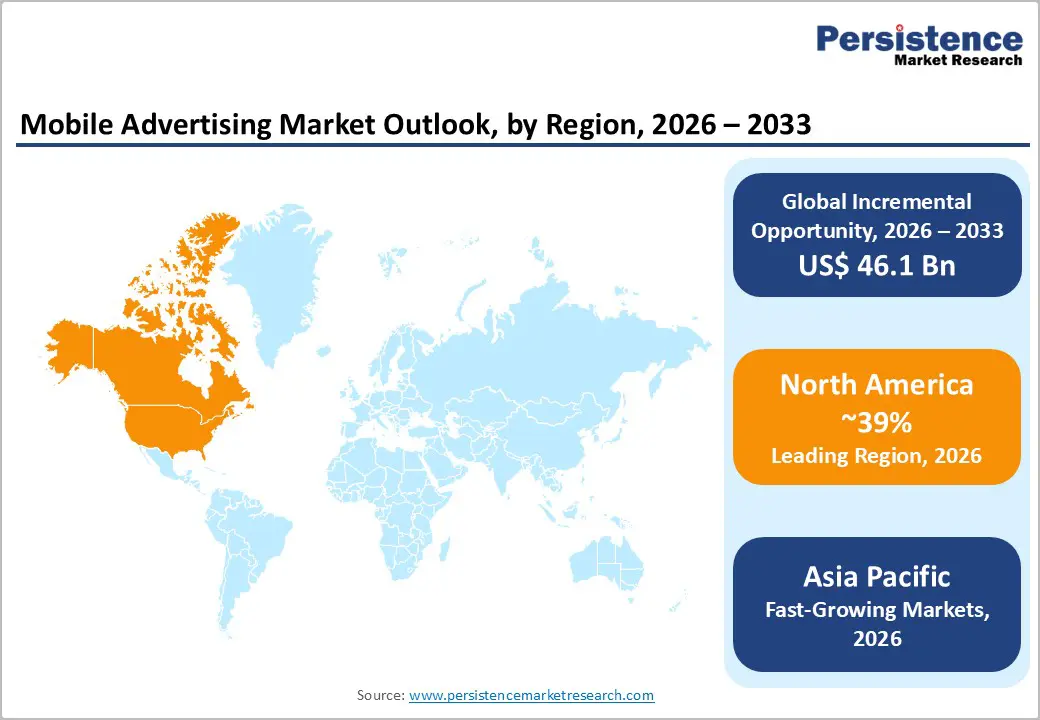

- Leading region: North America leads the Mobile Advertising Market, having 39% share, due to mature regulations, high technology adoption, and large-scale digital-advertising and e-commerce programs.

- Fastest-growing region: Asia Pacific is the fastest-growing region, with a CAGR of 25.8%, driven by rapid smartphone penetration, digital payment adoption, and e-commerce expansion in China, India, and ASEAN countries.

- Dominant segment: The Search Ads segment dominates, capturing around 35% of the market by providing high=intent, conversion-driven advertising for retail & e-commerce, travel & hospitality, and local services.

- Fastest-growing segment: The AI-Driven Advertising segment is the fastest-growing, with share expanding toward 25% as machine learning and predictive analytics enhance ad performance and targeting precision.

- Key market opportunity: The expansion of in-app and mobile video advertising presents a major opportunity, particularly in Asia Pacific and Latin America, where gaming, social media, and e-commerce.

- Commerce brands seek high-engagement, conversion-driven campaigns.

| Key Insights | Details |

|---|---|

| Mobile Advertising Market Size (2026E) | US$ 17.3 Bn |

| Market Value Forecast (2033F) | US$ 63.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 20.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.8% |

Market Dynamics

Market Growth Drivers

Rising smartphone penetration and mobile-first consumer behavior

Global smartphone adoption has surged, with Statista and GSMA reporting that over 6.8 billion people now use mobile devices and spend several hours daily on apps, social media, and video platforms. This shift has made mobile advertising the primary channel for brand discovery, consideration, and purchase, especially among millennials and Gen Z consumers.

In-app advertising and mobile search advertising have become central to retail & e-commerce, gaming, and entertainment strategies, as users increasingly research, compare, and buy products directly on their phones. The ubiquity of mobile devices, combined with high engagement rates, has driven advertisers to allocate larger shares of their budgets to mobile-centric campaigns.

Expansion of programmatic, AI-driven, and data-rich advertising ecosystems

Programmatic advertising and AI-driven targeting have transformed mobile advertising into a highly efficient, automated, and measurable channel. Real-time bidding (RTB), geolocation advertising, and contextual targeting enable advertisers to deliver personalized ads to specific audiences at scale, improving click-through rates (CTR) and conversion rates.

Industry analyses indicate that programmatic mobile advertising accounts for a significant share of mobile ad spend, particularly in North America and Europe, where ad-tech platforms such as Google AdMob, Meta Audience Network, and AppLovin dominate. The integration of machine learning and predictive analytics further enhances ad performance, making mobile advertising a preferred channel for performance-driven marketers.

Market Restraints

Privacy regulations and data-protection challenges

Stricter privacy regulations, such as the EU General Data Protection Regulation (GDPR), California Consumer Privacy Act (CCPA), and Apple’s App Tracking Transparency (ATT) framework, have limited access to user data, making behavioral targeting more challenging.

Advertisers and ad-tech platforms must now rely on first-party data, contextual targeting, and consent-based tracking, which can reduce targeting precision and campaign effectiveness. Industry reports highlight that iOS privacy changes have significantly impacted mobile-ad performance, particularly for social and in-app advertising, forcing marketers to adapt strategies and invest in alternative targeting methods.

Ad-blocker usage and consumer ad-fatigue

Growing ad-blocker adoption and consumer ad fatigue are constraining mobile ad visibility and engagement. Surveys by Pew Research Center and eMarketer indicate that a significant portion of mobile users install ad-blockers or skip video ads, reducing impression counts and revenue potential for publishers.

Intrusive interstitial ads, pop-ups, and auto-play videos are often perceived as disruptive, leading to lower click-through rates and brand-safety concerns. Advertisers must balance frequency, relevance, and user experience to maintain engagement without alienating audiences, which increases creative and optimization costs.

Market Opportunities

Growth of in-app and mobile video advertising

In-app advertising and mobile video advertising present major growth opportunities, driven by the popularity of gaming, social media, and streaming apps. Industry data show that in-app ads account for a significant share of mobile ad spend, with gaming & entertainment and retail & e-commerce brands heavily investing in rewarded video, interstitial, and native formats.

Mobile video ads, particularly short-form and shoppable videos, are gaining traction on platforms such as YouTube, TikTok, and Instagram, where high engagement and conversion rates justify premium pricing. The combination of 5G networks, high-resolution displays, and immersive formats positions in-app and mobile video advertising as key growth drivers for the mobile advertising market.

Expansion of AI-driven and programmatic advertising in emerging markets

Emerging markets in Asia Pacific, Latin America, and Africa are witnessing rapid growth in mobile-advertising adoption, driven by rising smartphone penetration, digital-payment infrastructure, and e-commerce expansion. Governments and multilateral agencies such as World Bank and International Telecommunication Union (ITU) are promoting digital-inclusion programs, which increase mobile-internet access and app usage.

AI-driven and programmatic advertising platforms are being localized to support language, currency, and regulatory requirements, enabling global brands to reach underserved audiences. This shift toward data-driven, automated advertising in emerging markets opens a significant opportunity for ad-tech companies and publishers to scale their operations.

Category-wise Insights

Ad Format Analysis

The Search Ads segment dominates the Ad Format category, with approximately 35% market share, reflecting the high-intent and conversion-potential of mobile search advertising. Search ads appear when users enter keywords into search engines, making them highly relevant to purchase decisions in retail & e-commerce, travel & hospitality, and local services. Industry analyses indicate that Google generates a significant portion of its ad revenue from mobile search ads, particularly on Android devices, where high search volume and intent-driven queries drive click-throughs and sales. The segment’s leadership is reinforced by real-time bidding, location-based targeting, and performance-tracking tools, which enable advertisers to optimize ROI and campaign efficiency.

Platform Analysis

Within the Platform category, In-App Advertising captures roughly 60% of the market share, driven by the dominance of mobile apps in gaming, social media, and e-commerce. In-app ads appear within native app environments, offering high engagement and contextual relevance, particularly for gaming & entertainment and retail & e-commerce brands. Industry reports highlight that in-app advertising accounts for a significant share of mobile ad spend, with Android leading due to its large user base and open-source ecosystem. The segment’s growth is further supported by programmatic platforms, rewarded video ads, and native formats, which enhance user experience and ad performance.

Technology Analysis

The Programmatic Advertising segment accounts for approximately 50% of the Technology market share, reflecting the dominance of automated, data-driven ad buying in mobile advertising. Programmatic platforms enable real-time bidding (RTB), AI-driven targeting, and cross-channel optimization, improving efficiency and scalability for advertisers. Industry analyses indicate that programmatic mobile advertising accounts for a significant share of mobile ad spend, particularly in North America and Europe, where ad-tech ecosystems are mature. The segment’s growth is driven by advances in machine learning, predictive analytics, and identity-resolution technologies, which enhance targeting precision and campaign performance.

End Use Analysis

The Retail & E-commerce end-use segment accounts for about 30% of the market, making it the largest single application for mobile advertising. E-commerce brands leverage search, in-app, and social media advertising to drive product discovery, consideration, and purchase, particularly during sales events and holiday seasons. Industry data show that mobile devices account for a significant share of online transactions, with retail & e-commerce brands investing heavily in mobile-centric campaigns. The segment’s leadership is reinforced by rising smartphone penetration, digital payment adoption, and social commerce trends, positioning retail & e-commerce as a key growth engine for the mobile advertising market.

Technology Analysis

The AI-Driven Advertising segment is one of the fastest-growing within the Technology category, with its share expanding to approximately 25% as machine learning and predictive analytics enhance ad performance. AI-driven platforms enable hyper-personalized targeting, dynamic creative optimization, and real-time bidding, improving click-through rates and conversion rates. Industry reports highlight that AI-driven advertising is being adopted by global brands and ad-tech companies to optimize campaigns and reduce waste. This trend positions AI-driven advertising as a key growth opportunity for mobile advertising participants.

Regional Insights

North America Mobile Advertising Market Trends

North America leads the Mobile Advertising Market in terms of technology adoption, regulatory maturity, and market size, with the United States accounting for the largest national share. The region benefits from a highly developed digital advertising ecosystem, with Google, Meta, and Amazon dominating search, social, and programmatic advertising.

U.S. mobile advertising spend is projected to grow significantly, driven by rising adoption of location-based technologies and performance-driven marketing. Major players such as Google Inc, Meta Platforms, Inc., and AppLovin Corporation are headquartered in North America, fostering a robust innovation ecosystem that drives product development and market expansion.

Europe Mobile Advertising Market Trends

Europe exhibits strong demand for privacy-compliant and data-driven mobile advertising, particularly in Germany, the United Kingdom, France, and Spain. The European Union has harmonized privacy regulations through GDPR, which shapes ad-tech practices and targeting strategies.

German and UK advertisers are notable for early adoption of programmatic and AI-driven advertising, whereas French and Spanish markets are expanding mobile advertising.centric campaigns for retail & e-commerce and travel & hospitality. EN standards and national data protection authorities are increasingly aligned with privacy-compliant advertising, thereby enabling cross-border projects and fostering a harmonized regulatory environment that supports market growth.

Asia Pacific Mobile Advertising Market Trends

Asia Pacific is the fastest-growing region for the Mobile Advertising Market, driven by rapid smartphone penetration, digital-payment adoption, and e-commerce expansion in China, Japan, India, and ASEAN countries. China and India are witnessing a surge in in-app and mobile video advertising, supported by local platforms such as WeChat, TikTok, and JioMart.

Japan is leveraging advanced mobile-advertising technologies for retail & e-commerce and gaming & entertainment, while ASEAN nations such as Singapore, Malaysia, and Indonesia are adopting mobile-centric campaigns for travel & hospitality and telecom. The region’s manufacturing advantages, cost-competitive labor, and developing logistics networks position Asia Pacific as a primary growth engine for mobile advertising participants.

Competitive Landscape

Market Structure Analysis

The Mobile Advertising Market is moderately consolidated, comprising global tech giants, ad-tech platforms, and local publishers. Leading players such as Google Inc, Meta Platforms, Inc., Alphabet, Inc., X Corp., AppLovin Corporation, InMobi Technologies Private Limited, and Smaato Inc hold significant shares through integrated ad-tech ecosystems, global distribution networks, and industry-specific solutions.

Smaller and regional firms compete on niche verticals, localized compliance, and cost-competitive bundles, particularly for SMEs and mid-market projects. Strategic trends include vertical-specialization, AI-driven targeting, programmatic platforms, and partnerships with publishers, which are reshaping competitive dynamics and driving consolidation through M&A and strategic alliances.

Key Market Developments

- In October 2025, Google Inc launched a new AI-driven mobile-advertising platform with real-time bidding and hyper-personalized targeting, targeting retail & e-commerce and gaming & entertainment brands in North America and Europe. The upgrade aims to enhance ad performance, user experience, and privacy compliance.

- In June 2024, Meta Platforms, Inc. introduced a mobile-video advertising suite with shoppable ads and augmented reality (AR) formats, designed for social media and e-commerce brands in the Asia Pacific and Latin America.

- The platform supports high-engagement, conversion-driven campaigns.

- In March 2024, AppLovin Corporation expanded its in-app advertising capabilities in India, partnering with local publishers and gaming studios to deliver rewarded video and native ads. The initiative targets mobile-first consumers and e-commerce brands seeking high-engagement campaigns.

Companies Covered in Mobile Advertising Market

- Google Inc

- Chartboost Inc.

- Twitter Inc

- Pandora Media, Inc

- Millennial Media Inc

- InMobi Technologies Private Limited

- Smaato Inc

- Tune, Inc.

- Amobee, Inc

- Epom

- Meta Platforms, Inc.

- Alphabet, Inc.

- X Corp.

- AppLovin Corporation

- The Trade Desk, Inc.

- Criteo SA

- NextRoll, Inc. (AdRoll)

- MediaMath

- Adobe Inc.

Frequently Asked Questions

The Mobile Advertising Market is projected to reach US$ 63.4 Billion by 2033, growing at a CAGR of 20.4% from 2026, driven by rising smartphone penetration, mobile‑first consumer behavior, and programmatic, AI‑driven advertising ecosystems.

Key demand drivers include rising smartphone penetration, mobile‑first consumer behavior, expansion of in‑app and mobile video advertising, and growth of programmatic, AI‑driven, and data‑rich advertising ecosystems, which push brands toward mobile‑centric campaigns.

The Search Ads segment dominates, capturing around 35% of the market by providing high‑intent, conversion‑driven advertising for retail & e‑commerce, travel & hospitality, and local services.

North America leads the global Mobile Advertising Market, supported by mature regulations, high technology adoption, and large‑scale digital‑advertising and e‑commerce programs.

A key opportunity lies in in‑app and mobile video advertising, particularly in Asia Pacific and Latin America, where gaming, social media, and e‑commerce brands seek high‑engagement, conversion‑driven campaigns.

Major players include Google Inc, Chartboost Inc., Twitter Inc, Pandora Media, Inc, Millennial Media Inc, InMobi Technologies Private Limited, Smaato Inc, Tune, Inc., Amobee, Inc, Epom, Meta Platforms, Inc., Alphabet, Inc., X Corp., and AppLovin Corporation, among others.