- Executive Summary

- Global Lime Market Snapshot 2025 and 2032

- Market Opportunity Assessment, 2025-2032, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Metal Industry Overview

- Global Chemical Industry Overview

- Global Construction Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 - 2032

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Global Lime Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Product Type, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- Market Attractiveness Analysis: Product Type

- Global Lime Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Application, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- Market Attractiveness Analysis: Application

- Global Lime Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2019-2024

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2025-2032

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- Europe Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- East Asia Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by , 2025-2032

- South Asia & Oceania Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- Latin America Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- Middle East & Africa Lime Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2025-2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2025-2032

- Quicklime

- Hydrated Lime

- Dolomitic Lime

- High-Calcium Lime

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2025-2032

- Metallurgical Processes

- Environmental Uses

- Chemical Manufacturing

- Construction

- Glass and Ceramics

- Pulp and Paper

- Others

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Carmeuse

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Graymont

- Lhoist Group

- Mississippi Lime Company

- Cheney Lime & Cement Company

- United States Lime & Minerals, Inc.

- Anhui Conch Group

- Nordkalk Corporation

- Xinjiang Zhongtai Chemical Co., Ltd.

- Jiangxi Wannianqing Cement Co., Ltd.

- Cimpor - Cimentos de Portugal

- Omya AG

- Tata Chemicals

- Shree Cement Ltd.

- Cimsa Cimento

- Carmeuse

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Bulk Chemicals

- Lime Market

Lime Market Size, Trends, Share, Growth, and Forecasts for 2025 - 2032

Lime Market by Product Type (Quicklime, Hydrated Lime, Dolomitic Lime, High-Calcium Lime, and Others), Application (Metallurgical Processes, Environmental Uses, Chemical Manufacturing, Construction, Glass and Ceramics, Others), and Regional Analysis for 2025 - 2032

Lime Market Share and Trends Analysis

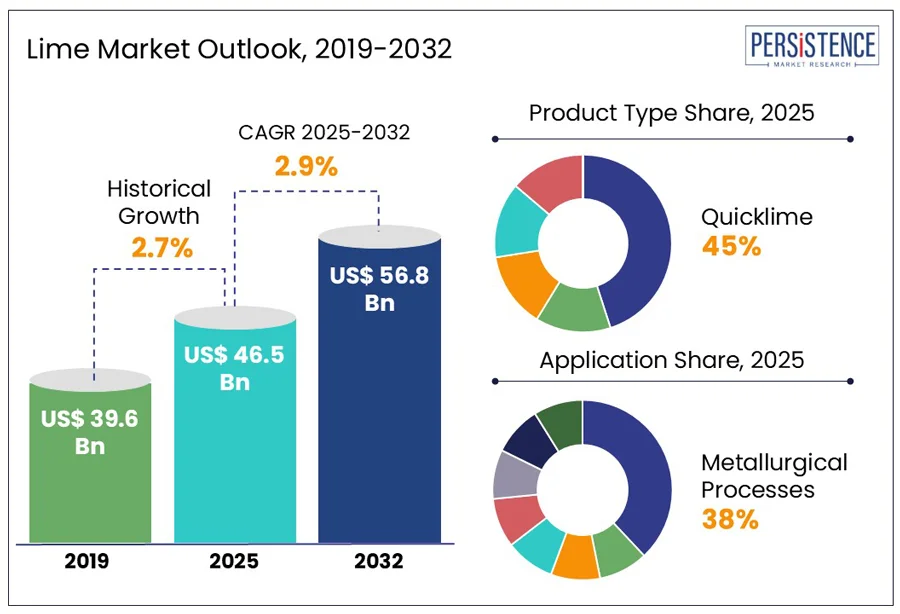

The global lime market size is expected to increase from US$ 46.5 billion in 2025 to US$ 56.8 billion by 2032. It is projected to witness a CAGR of 2.9% from 2025 to 2032. According to the Persistence Market Research report, the lime industry plays a vital role in the manufacturing sector, ranging from steel to water treatment, driven by its versatility and environmental applications. As sustainability and infrastructure demands rise, lime remains essential in shaping cleaner industrial processes, modern construction, and agricultural productivity across developed and emerging economies alike.

Key Industry Highlights

- Lime is critical in steel manufacturing, acting as a flux to remove impurities during metal refining.

- Increasing use of lime in flue gas desulfurization and wastewater treatment supports emissions control and regulatory compliance.

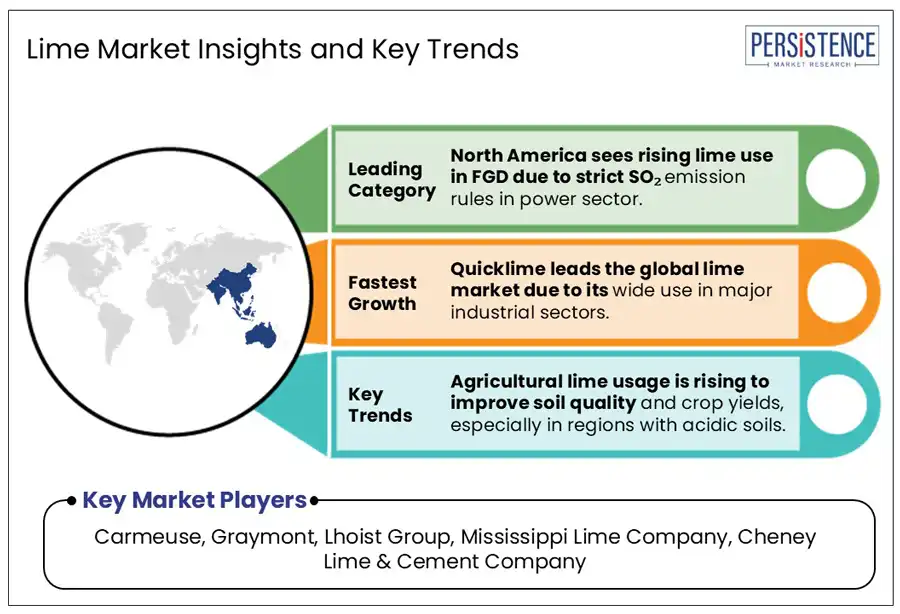

- Agricultural lime usage is rising to improve soil quality and crop yields, especially in regions with acidic soils.

- China leads global lime production and consumption, followed by the U.S. and parts of Europe.

- Quicklime remains the most consumed lime product due to its wide applicability in heavy industries.

- Demand for low-carbon lime products is growing, driving innovation in cleaner production technologies and circular applications.

|

Global Market Attribute |

Key Insights |

|

Lime Market Size (2025E) |

US$ 46.5 Bn |

|

Market Value Forecast (2032F) |

US$ 56.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

2.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.7% |

Market Dynamics

Driver - Increasing demand from the steel industry is driving lime consumption, particularly for impurity removal during metallurgical processes

Lime is an essential input in the steel manufacturing process, particularly during the refining of iron ore in both basic oxygen furnaces and electric arc furnaces.

- The steel industry is a significant consumer of lime, utilizing between 140 and 160 million tons globally.

- In the Electric Arc Furnace (EAF) route, which contributes to around 30% of global steel production, about 88 kg of limestone is used per 1,000 kg of crude steel.

It facilitates the removal of key impurities such as silica, phosphorus, and sulfur by forming slag, a byproduct that captures and separates these unwanted elements from molten metal. This results in cleaner, higher-grade steel that meets stringent quality standards across construction, automotive, and infrastructure.

As the global demand surges for steel, it is driven by rapid urbanization, industrial growth, and infrastructure development, lime consumption increases in parallel. Environmental regulations are reinforcing lime’s role in cleaner, low-emission steelmaking processes.

Restraint- Environmental regulations around CO? emissions from lime kilns are limiting production expansion in certain regions globally

Environmental regulations targeting CO? emissions from lime kilns are increasingly impacting lime production, especially in regions with stringent climate policies such as Europe and North America. Lime manufacturing involves the calcination of limestone, a high-temperature process that inherently releases significant amounts of carbon dioxide, both from fuel combustion and the limestone itself.

As governments enforce tighter emission standards and carbon pricing mechanisms, producers face increased operational costs, pressure to invest in carbon capture technologies, or limits on expansion permits. These regulatory hurdles are driving shifts toward more energy-efficient kilns, greener alternatives, and even production relocation to regions with more lenient environmental controls.

Opportunity - Expanding lime-based water and wastewater treatment solutions offers strong growth potential in emerging urban and industrial regions

Lime is crucial in modern water and wastewater treatment systems due to its chemical properties and cost-effectiveness. It efficiently neutralizes acidic waters, precipitates heavy metals such as lead and arsenic, reduces biological oxygen demand, and assists in the removal of phosphates and other contaminants.

According to the UN World Water Development Report, over 80% of wastewater globally is discharged untreated, with developing countries in Asia and Africa most affected. This creates a significant need for affordable treatment solutions such as lime.

As urban population grow and industrial sectors expand in developing regions such as Asia, Africa, and Latin America, the strain on freshwater resources and sanitation infrastructure is intensifying. This has led to a surge in demand for scalable, affordable treatment technologies. Lime’s availability, simplicity of application, and regulatory compliance advantages make it a preferred choice in municipal and industrial settings.

Category Wise Analysis

Product Type Insights

Quicklime, also known as calcium oxide, dominates the global lime market owing to its versatile applications across key industrial sectors. In steelmaking, it is essential for removing impurities and forming slag, which protects furnaces and enhances metal quality. In environmental applications, quicklime is widely used for flue gas desulfurization, helping reduce sulfur dioxide emissions from power plants and industrial sources.

The chemical industry relies on quicklime for producing calcium-based compounds and for pH control in various processes. Its high reactivity and cost-efficiency make it a preferred choice, especially in regions with expanding infrastructure and tightening environmental regulations.

Application Insights

Metallurgical processes represent the largest application segment in the lime market, primarily driven by their critical role in steel and non-ferrous metal production. In steelmaking, lime is used to remove impurities such as silica, phosphorus, and sulfur, improving the quality and strength of the final product. It also aids in slag formation which facilitates impurity separation and furnace protection.

Beyond steel, lime is used in aluminum, copper, and nickel processing to neutralize acidic waste and purify ores. As global demand for metals grows due to infrastructure development and industrialization, especially in Asia and the Middle East, lime consumption continues to rise.

Regional Insights

North America Lime Market Trends

The adoption of lime in flue gas desulfurization (FGD) systems is accelerating, driven by stringent environmental regulations targeting sulfur dioxide (SO?) emissions from the power sector. The U.S. Environmental Protection Agency's Clean Air Act and its subsequent amendments have mandated significant reductions in SO? emissions, prompting power plants to implement effective control technologies. Wet FGD systems, utilizing lime or limestone slurries, have become prevalent due to their ability to achieve over 90% SO? removal efficiency. This regulatory landscape has led to substantial investments in FGD installations and retrofits across coal-fired power plants in the region.

The production of synthetic gypsum as a by-product of lime-based FGD processes offers economic benefits, further incentivizing adoption. As the power industry continues to prioritize emission reductions, lime-based FGD systems are poised to play a critical role in meeting environmental compliance and promoting cleaner energy production.

Europe Lime Market Trends

In Europe, the shift toward sustainable construction materials significantly has boosted the use of hydrated lime in eco-friendly building applications. Hydrated lime is favored for its lower carbon footprint compared to traditional cement, emitting approximately 30% less CO? during production. Its natural properties, including breathability, moisture regulation, and antimicrobial characteristics, contribute to healthier indoor environments and improved energy efficiency. These qualities make it an ideal material for green building practices, aligning with the European Union's Renovation Wave Strategy, which aims to double the annual renovation rate of buildings by 2030 to enhance energy performance and reduce emissions.

Innovations such as hemp-lime composites are gaining traction, offering enhanced insulation and sustainability benefits. The resurgence of lime in modern architecture is evident in projects like the Grandmother House in Denmark, where lime mortar is used for its durability and aesthetic appeal. As environmental regulations tighten and the demand for sustainable building solutions grows, hydrated lime stands out as a key component in Europe's green construction movement.

Asia Pacific Lime Market Trends

Rapid industrialization and massive infrastructure development in Asia Pacific, especially in China and India, are significantly accelerating lime demand across multiple sectors. China alone consumed over 319 million tons of lime in 2024, driven by its dominant steel and construction industries. India’s lime usage is rising with government-led initiatives such as the National Infrastructure Pipeline and Smart Cities Mission.

In August 2024, Chememan Public Company Limited, in partnership with Khimsar Mine Corporation, initiated construction of a modern lime manufacturing facility in Khimsar Village, Rajasthan. The plant is scheduled for completion by early 2026, with an initial annual production capacity of 100,000 tons, and plans to expand to 500,000 tons in subsequent phases. This project marks Chememan's strategic entry into India's lime market, becoming a leading producer in the region.

The expansion of industries such as chemicals, water treatment, and metallurgy across Southeast Asia is further stimulating demand. With ongoing urbanization, economic growth, and industrial expansion, lime remains a critical raw material, positioning Asia Pacific as the primary driver of global market growth.

Competitive Landscape

The global lime market is moderately consolidated, with a mix of multinational players and regional producers competing across diverse application segments. Companies differentiate through product quality, vertical integration, geographical reach, and technological innovations in kiln efficiency and emissions control.

Market players are expanding capacity in high-growth regions such as Asia Pacific and investing in sustainable production methods to comply with tightening environmental regulations. Strategic mergers, acquisitions, and joint ventures are also common as firms to enhance distribution networks and strengthen supply chains. The competitive landscape is shaped by fluctuating raw material availability, energy costs, and evolving application-specific performance standards.

Key Industry Developments

- In April 2024, Mayur Resources, Australia-based secured full funding of US$155 million for its Central Lime Project (CLP) in Papua New Guinea. The project aims to establish a vertically integrated manufacturing facility with an annual production capacity of 400,000 tonnes of quicklime. The CLP is set to displace 100% of the country's imported lime products and position Papua New Guinea as a major exporter in the Australasian region.

- In May 2024, Singleton Birch, U.K.-based announced a substantial investment to enhance its hydrated lime production capabilities at the Melton Ross facility in the United Kingdom. The expansion, expected to be commissioned in early 2025, aims to meet rising demand in markets such as energy-from-waste, chemical processing, and battery minerals.

- In June 2024, Gloria Group announced plans to establish a new lime plant in Lima's industrial zone, with a production capacity exceeding 350,000 tonnes per year. The plant will serve both domestic and export markets, catering to the growing demand from the mining and construction sectors.

Companies Covered in Lime Market

- Carmeuse

- Graymont

- Lhoist Group

- Mississippi Lime Company

- Cheney Lime & Cement Company

- United States Lime & Minerals, Inc.

- Anhui Conch Group

- Nordkalk Corporation

- Xinjiang Zhongtai Chemical Co., Ltd.

- Jiangxi Wannianqing Cement Co., Ltd.

- Cimpor - Cimentos de Portugal

- Omya AG

- Tata Chemicals

- Shree Cement Ltd.

- Cimsa Cimento

Frequently Asked Questions

The global lime market is projected to value at 46.5 bn in 2025.

The lime market is driven by increasing demand from the steel industry, particularly for impurity removal during metallurgical processes.

The lime market is poised to witness a CAGR of 2.9% between 2025 and 2032

Expanding lime-based water and wastewater treatment solutions are the key market opportunities.

Major players in the lime market include Carmeuse, Graymont, Lhoist Group, Mississippi Lime Company, Cheney Lime & Cement Company, and others.