- Executive Summary

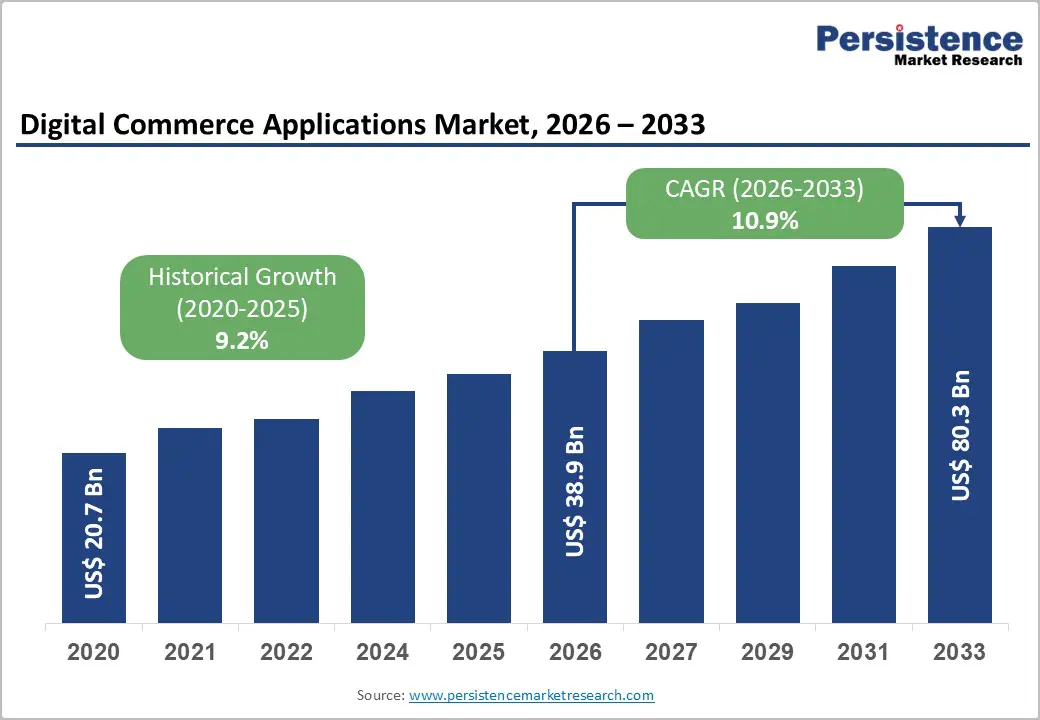

- Global Digital Commerce Applications Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 – 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Global Parent Market Overview

- Digital Commerce Applications Market: Value Chain

- List of Raw Deployment Mode Supplier

- List of Manufacturers

- List of Distributors

- List of End Use Industries

- Profitability Analysis

- Forecast Factors – Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Deployment Mode Landscape

- 3.1. Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Other Macro-economic Factors

- Price Trend Analysis, 2020 – 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Solution Type/Deployment Mode/Enterprise Size

- Regional Prices and Product Preferences

- Global Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size Analysis, 2020-2025

- Current Market Size Forecast, 2026–2033

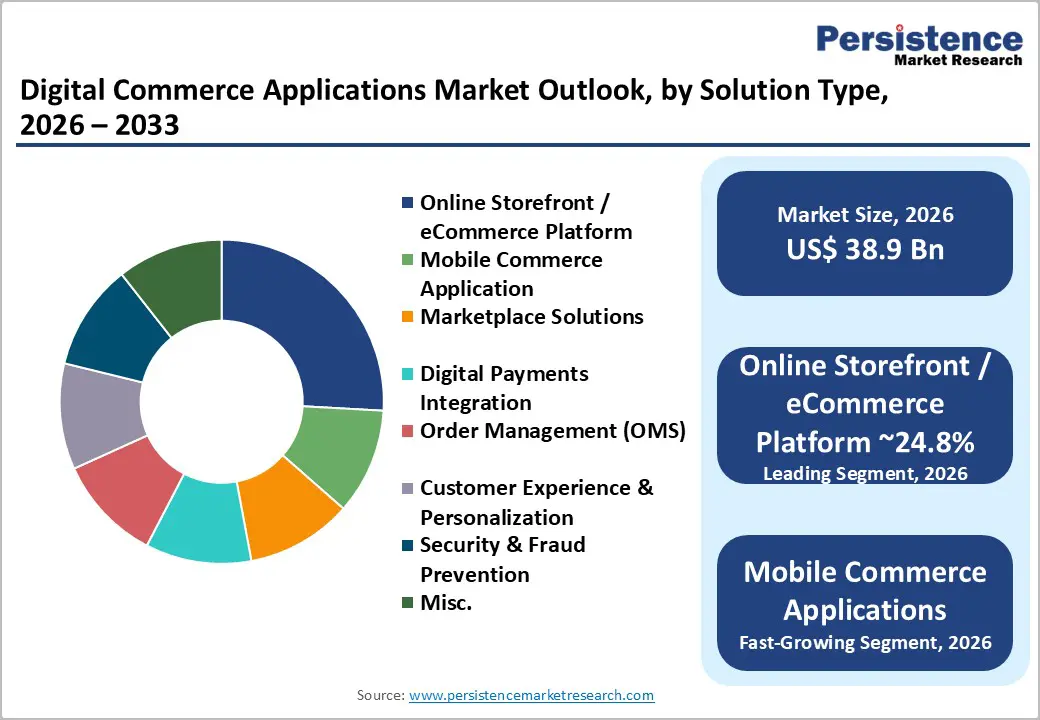

- Global Digital Commerce Applications Market Outlook: Solution Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Solution Type, 2020 – 2025

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Market Attractiveness Analysis: Solution Type

- Global Digital Commerce Applications Market Outlook: Deployment Mode

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Deployment Mode, 2020 – 2025

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Market Attractiveness Analysis: Deployment Mode

- Global Digital Commerce Applications Market Outlook Enterprise Size

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By Enterprise Size, 2020 – 2025

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Market Attractiveness Analysis: Enterprise Size

- Global Digital Commerce Applications Market Outlook End Use Industry

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis By End Use Industry, 2020 – 2025

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis: End Use Industry

- Key Highlights

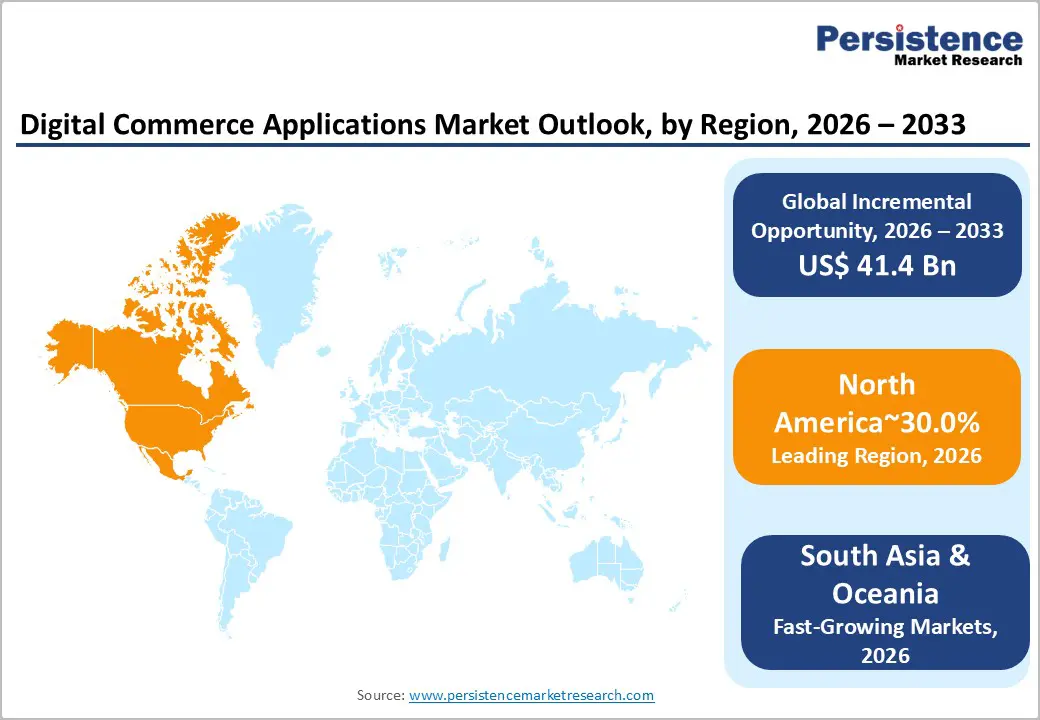

- Global Digital Commerce Applications Market Outlook Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis By Region, 2020 – 2025

- Current Market Size (US$ Mn) Forecast By Region, 2026 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- Europe Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- By Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- East Asia Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- South Asia & Oceania Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- Latin America Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- Middle East & Africa Digital Commerce Applications Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) Analysis By Market, 2020 – 2025

- By Country

- By Solution Type

- By Deployment Mode

- By Enterprise Size

- By End Use Industry

- Current Market Size (US$ Mn) Forecast By Country, 2026 – 2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Current Market Size (US$ Mn) Forecast By Solution Type, 2026 – 2033

- Online Storefront / eCommerce Platform

- Mobile Commerce Application

- Marketplace Solutions

- Digital Payments Integration

- Order Management (OMS)

- Customer Experience & Personalization

- Security & Fraud Prevention

- Misc.

- Current Market Size (US$ Mn) Forecast By Deployment Mode, 2026 – 2033

- Cloud

- On-Premise

- Hybrid

- Current Market Size (US$ Mn) Forecast By Enterprise Size, 2026 – 2033

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Current Market Size (US$ Mn) Forecast By End Use Industry, 2026 – 2033

- Retail & eTail

- Consumer Goods

- BFSI

- Telecom & IT Services

- Healthcare & Pharmaceuticals

- Manufacturing

- Misc.

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Solution Type

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Shopify

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- BigCommerce

- Adobe Commerce (Magento)

- Salesforce Commerce Cloud

- SAP Commerce Cloud

- Oracle Commerce

- VTEX

- Lightspeed Commerce

- Wix eCommerce

- Commercetools

- Elastic Path

- Spryker Systems

- Shopify

Note: List of companies is not exhaustive in Nature . It is subject to further augmentation during course of research

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations