- Retail

- Asia Pacific Mobile Protective Cases Market

Asia Pacific Mobile Protective Cases Market Size, Share, and Growth Forecast 2026 – 2033

Asia Pacific Mobile Protective Cases Market by Product Type (Back Plate Case, Folio/Flip Case, and Others), Material Type (Silicone, Genuine and PU Leather, Plastic, and Others), Price Range (Mass and Premium), Distribution Channel (Online and Offline), and Regional Analysis

Asia Pacific Mobile Protective Cases Market Size and Share Analysis

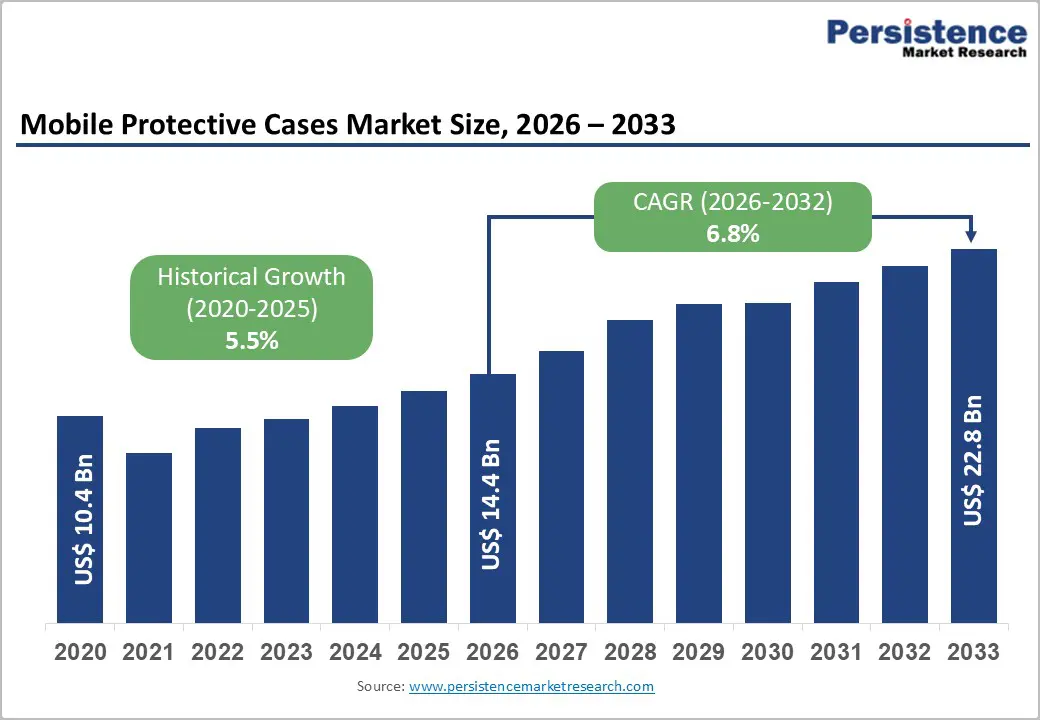

The Asia Pacific Mobile Protective Cases Market size was valued at US$ 14.4 Bn in 2026 and is projected to reach US$ 22.8 Bn by 2033, growing at a CAGR of 6.8% between 2026 and 2033. The market expansion is primarily driven by accelerating smartphone penetration across emerging economies, rising consumer demand for device protection, and a significant shift toward personalized and multifunctional accessories. With over 1.9 billion smartphone units sold annually in the Asia Pacific region and the increasing affordability of mid-range and premium devices, consumers are investing substantially in protective solutions that extend device longevity while reflecting personal style preferences.

Key Market Highlights

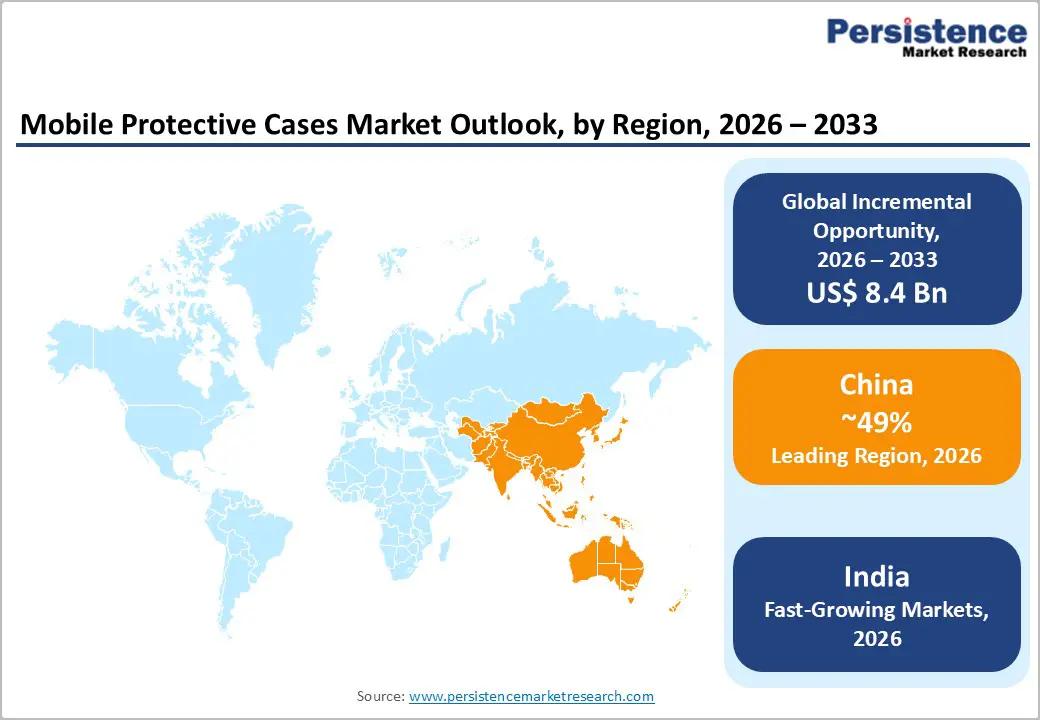

- Leading Country: China's dominance reflects 49% global market share driven by integrated manufacturing clusters in China and Vietnam, massive smartphone user bases exceeding 1.9 billion units annually, and rapid urbanization expanding middle-class purchasing power across India, Indonesia, and Southeast Asia economies.

- Fastest Growing Country: India's protective cases market expands at 10.2% CAGR through 2033, fueled by government PLI manufacturing incentives, smartphone export growth reaching US$21 billion in 2024, and expanding tier-2/tier-3 city consumer bases seeking affordable protective solutions.

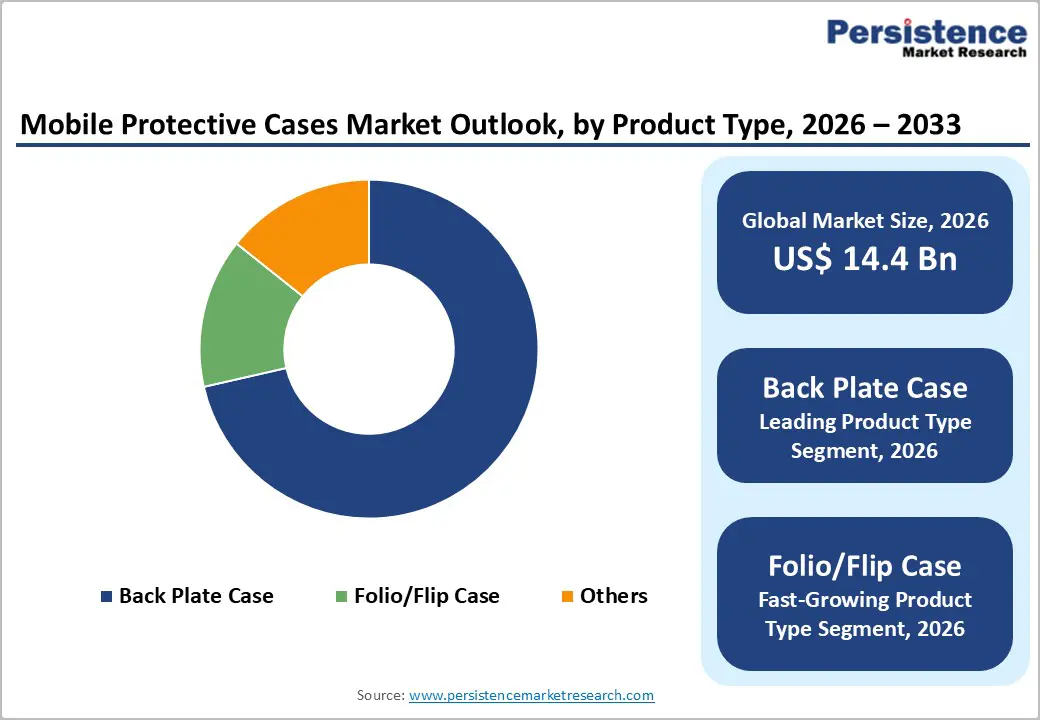

- Dominant Product Type: Back plate cases command 59.6% market share through consumer preference for slim-profile protection, wireless charging compatibility preservation, and device aesthetic showcasing without compromising protective functionality.

- Growing Product Type: Folio and flip cases register fastest growth trajectory, driven by multifunctional design integration, premium pricing power supporting margins, and expanding consumer preference for all-in-one protective solutions combining screen protection with storage functionality.

- Key Market Opportunity: Foldable smartphone protection represents a transformational growth vector with market expansion, driven by Samsung Galaxy Z-series sales acceleration, emerging Motorola Razr clamshell momentum, and specialized protective requirements enabling premium case pricing of US$30-80 per unit versus traditional US$15-40 case pricing.

| Key Insights | Details |

|---|---|

|

Asia Pacific Mobile Protective Cases Market Size (2026E) |

US$ 14.4 Bn |

|

Market Value Forecast (2033F) |

US$ 22.8 Bn |

|

Projected Growth CAGR (2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

5.5% |

Market Dynamics

Market Growth Drivers

Rapid Smartphone Penetration and Device Upgrade Cycles

The Asia Pacific region has witnessed unprecedented growth in smartphone adoption, with regional subscriber penetration reaching 63% of the population by 2024 and projected to expand further as 5G networks proliferate across China, India, Indonesia, and Southeast Asia. Consumer smartphone upgrades are occurring at accelerated rates in emerging markets, where mid-range devices priced between US$ 200-500 have become accessible to increasingly large consumer populations.

According to market intelligence, Apple achieved 15% year-over-year growth in Southeast Asia in 2024 through expanded distribution channels, while Samsung maintained leadership with the Galaxy Z Fold and Galaxy Z Flip series, driving demand for premium protective cases. The replacement cycle of protective cases occurs more frequently than that of smartphones, creating recurring revenue opportunities for manufacturers and retailers throughout the forecast period.

Rising Disposable Incomes and Premium Device Adoption

Rising middle-class populations across India, Indonesia, and Vietnam are demonstrating increased purchasing power for premium and ultra-premium smartphones, directly correlating with enhanced demand for high-quality protective accessories. India's smartphone exports reached US$ 21 billion in 2024, with Apple iPhone exports accounting for approximately 70% of total smartphone exports and generating US$ 14.39 billion in export value. In Japan, consumers continue to prioritize fashion-forward and premium protective cases, with the market valued at US$ 4.7 billion in 2025 and projected to reach US$ 8 billion by 2035 at a 5.7% CAGR.

Premium device sales in Southeast Asia grew substantially in 2024, with OPPO and vivo expanding high-end portfolios, thereby increasing addressable markets for protective case manufacturers targeting affluent consumers seeking multifunctional and aesthetically sophisticated solutions.

Market Restraints

Counterfeit Product Proliferation and Quality Concerns

The unregulated influx of counterfeit and substandard mobile protective cases represents a significant market constraint affecting both consumer trust and manufacturer profitability. In 2024, approximately 680 million counterfeit cases were detected on online platforms globally, resulting in return rates exceeding 12% and consumer complaints about material degradation, device finish damage, and safety hazards.

China's low-cost bulk manufacturing capabilities, combined with weak anti-counterfeiting enforcement in emerging markets such as Indonesia, Malaysia, and India, enable illicit producers to capture price-sensitive consumer segments. These counterfeit products typically fail to meet established safety standards and lack durability assurances, thereby diminishing brand value for legitimate manufacturers and creating regulatory pressures for stringent quality verification mechanisms across e-commerce platforms.

Market Saturation and Intense Price Competition

The Asia Pacific mobile protective cases market exhibits characteristics of maturation in developed segments, with oversupply of generic designs and mass-produced variants creating downward pricing pressure on established brands. The proliferation of regional and local manufacturers in Vietnam, Thailand, and India, combined with the entry of e-commerce-native brands using direct-to-consumer distribution models, has compressed profit margins across value tiers.

Generic back-plate cases and budget folio cases commoditize, as plastic-based variants account for approximately 52.3% of market volumes, with manufacturers competing primarily on price rather than on innovation or brand differentiation. This competitive intensity particularly affects smaller and mid-tier protective case manufacturers lacking vertical integration or proprietary technology, forcing consolidation and exit strategies within the regional market landscape.

Market Opportunities

Explosive Growth of Foldable Smartphone Protection Solutions

Foldable smartphone technology represents a transformative opportunity for protective case manufacturers, with the global foldable smartphone market expanding at an exponential CAGR between 2025 and 2033, reaching US$ 118.87 billion by 2033. Samsung's Galaxy Z Fold and Galaxy Z Flip series, combined with emerging competitors including Motorola's Razr 60 clamshells and Google's Pixel Fold, drive demand for specialized protective cases engineered for complex folding mechanisms and dual-screen protection architectures.

Foldable smartphone shipments surged 45% year-over-year in Q2 2025, with Motorola capturing one in four foldable units sold globally through innovative clamshell designs, gaining traction in North America and emerging markets. Case manufacturers developing proprietary hinge protection mechanisms, crease-resistant screen covers, and magnetic closure systems compatible with Samsung's Z-series and alternative OEM foldables can capture premium pricing power estimated at US$ 30-80 per unit compared to traditional protective cases averaging US$ 15-40, unlocking substantial revenue growth in underserved high-margin segments.

Sustainable and Eco-Friendly Case Manufacturing Expansion

The eco-friendly mobile protective cases market is experiencing accelerated adoption, projected to grow from US$ 2.1 billion in 2024 to US$ 4.5 billion by 2033 at a 9.1% CAGR, making it one of the fastest-growing segments within the overall protective cases market. Regulatory frameworks across Europe and the Asia-Pacific increasingly mandate sustainable packaging and recyclable materials, while generational preferences among Gen Z and millennial consumers drive purchasing decisions toward biodegradable options made from bamboo, recycled plastics, and compostable bioplastics.

By 2026, approximately 40% of premium protective cases are forecasted to incorporate smart materials, including self-healing polymers and temperature-responsive components, with brands such as Pela Case, OtterBox, and Lifeproof leading sustainability initiatives and capturing environmentally conscious consumer segments. Companies establishing circular economy frameworks, implementing take-back recycling programs, and developing biodegradable alternatives can differentiate through environmental storytelling while accessing government incentives, carbon credits, and premium pricing opportunities in affluent markets.

Category-wise Insights

Product Type Analysis

Back plate case dominance reflects a strong consumer preference for slim-profile protection without screen coverage. Back plate cases commanded 59.6% market share in 2024, driven by consumer demand for durable, lightweight, and easy-to-install rear protection that preserves device thinness, maintains wireless charging compatibility, and showcases premium device aesthetics. Apple iPhone users prefer backplate cases integrated with MagSafe, enabling seamless attachment of wallets, stands, and car mounts, while Samsung and Chinese device manufacturers target cost-conscious consumers seeking affordable protective solutions without bulk.

The segment's strength reflects logical consumer prioritization of drop protection for expensive device rear panels and camera modules, coupled with minimal additional weight or thickness compared to full-coverage alternatives, positioning back plate cases as the market's structural foundation across all price tiers and geographic regions.

Material Type Analysis

Silicone cases dominate the material segment with 44% market share, benefiting from superior affordability, shock-absorbing properties, durability across temperature ranges, and ease of customization through molding and color variations. Silicone's popularity extends across budget and mid-tier segments throughout Asia Pacific, where price sensitivity remains paramount, and consumers prioritize protective functionality over aesthetic differentiation. Genuine and PU leather cases represent the fastest-growing material segment, expanding at a 9.6% CAGR through 2033, driven by premium consumer demand in Japan, South Korea, and affluent urban centers across China and India, which seek luxury aesthetics combined with professional finishing.

Plastic variants, including polyurethane and polycarbonate, accounting for approximately 52.3% of market volumes, serve as cost-effective alternatives in emerging markets and budget segments, though their inferior durability leads to higher replacement frequency and lower customer satisfaction ratings.

Price Range Analysis

Mass market cases dominate in unit volumes, representing approximately 70% of total units sold across Asia Pacific at price points between US$ 5-25, driven by price-conscious consumers in India, Indonesia, the Philippines, and Vietnam prioritizing functional protection over design aesthetics. Premium segment cases, priced between US$ 35-150 per unit, are expanding fastest in developed markets and among affluent urban consumers in China and Japan, with growth exceeding 8% annually as consumers increasingly regard protective cases as fashion accessories and brand status indicators.

Premium cases featuring MagSafe compatibility, genuine leather materials, designer collaborations, and branded heritage command substantial price premiums, with the OtterBox Defender Series and luxury brands capturing 18-25% market share in North America and selected Asia-Pacific affluent segments, demonstrating consumer willingness to pay substantially for recognized quality and innovative feature integration.

Distribution Channel Analysis

Offline distribution channels dominated the market, with a 73% share in 2024, comprising mobile retail chains, department stores, electronics retailers, and independent mobile dealers, which functioned as primary consumer touchpoints across Asia Pacific cities and towns. Consumers prefer offline shopping for protective cases to physically evaluate materials, assess fit for specific smartphone models, and obtain immediate gratification and installation assistance.

Online distribution channels represent the fastest-growing segment through mobile application-based commerce in China, where platforms such as Alibaba's Taobao and JD.com offer customization, influencer collaborations, and competitive pricing. E-commerce channels are forecast to surpass offline distribution by 2026, driven by younger consumer demographics, expanding logistics networks enabling next-day delivery, virtual try-on technologies, and personalized product recommendations leveraging artificial intelligence and consumer behavior analytics.

Country Insights

China Mobile Protective Cases Trends

China, with nearly 49% share, is the largest and leading mobile protective cases market in Asia Pacific, driven by its massive smartphone user base, high device replacement rates, and deeply integrated mobile accessories ecosystem. The country benefits from strong domestic smartphone production, rapid new model launches, and a highly developed supply chain that supports both mass-market and premium protective cases. Chinese consumers display strong demand across all price tiers, ranging from low-cost silicone and TPU cases to premium shockproof, leather, and branded designer cases.

E-commerce dominance, fast-fashion–style product refresh cycles, and influencer-driven marketing further accelerate sales volume. China serves as a global manufacturing hub for mobile cases, strengthening domestic availability and price competitiveness. Despite market maturity in urban centers, continuous innovation in materials, customization, and design sustains value growth, firmly establishing China as the anchor and revenue-dominant market in the Asia Pacific region.

Japan Mobile Protective Cases Trends

Japan is a highly developed yet moderate-growth market for mobile protective cases, characterized by strong expectations for product quality, premium preferences, and stable replacement demand. Smartphone penetration is already high, limiting volume expansion, while consumer focus has shifted toward durability, craftsmanship, and minimalist design rather than frequent upgrades. Japanese consumers favor premium materials, precision engineering, and slim yet protective case designs, often aligned with domestic lifestyle and aesthetic standards.

Retail channels are well established, with a strong presence of electronics stores, specialty accessory retailers, and brand-owned outlets, complemented by steady online sales. However, slower population growth and longer smartphone usage cycles constrain rapid market expansion. As a result, Japan’s market growth is primarily value-driven, supported by premium pricing and innovation rather than volume increases, positioning it as a stable, mature market within Asia Pacific.

India Mobile Protective Cases Trends

India is widely regarded as the fastest-growing mobile protective cases market in Asia Pacific, fueled by rapid smartphone penetration, a large youth population, and increasing affordability of smartphones across income segments. The surge in first-time smartphone users and frequent device upgrades is driving strong demand for protective cases as essential accessories rather than discretionary purchases. Indian consumers are highly sensitive to price, driving strong sales of affordable silicone, TPU, and hybrid cases, while premium and branded cases are gaining traction in urban and semi-urban markets.

Expansion of organized retail, aggressive e-commerce penetration, and local manufacturing initiatives are further supporting market growth. As smartphone adoption deepens beyond major cities and consumers become more aware of device protection, India’s mobile protective cases market is expected to record the highest CAGR in the region, positioning it as the most dynamic growth market in the Asia Pacific.

Competitive Landscape for the Mobile Protective Cases Market

The Asia Pacific Mobile Protective Cases Market exhibits characteristics of moderate fragmentation with consolidated leadership among established multinational brands and accelerating competition from regional manufacturers and direct-to-consumer digital natives. OtterBox and Spigen collectively command approximately 25-30% of brand awareness and market share across premium and mid-tier segments, leveraging extensive product portfolios, recognized durability credentials, and strategic partnerships with device manufacturers and retail chains. Chinese manufacturers, including Nillkin and regional producers based in Vietnam and Taiwan, capture substantial volumes through cost leadership and rapid model compatibility, while emerging sustainability-focused brands such as Pela Case and ESR gain traction among environmentally conscious affluent consumers.

The market structure reflects increasing vertical integration, with device manufacturers such as Samsung and Apple developing proprietary case ecosystems through MagSafe integration and exclusive material partnerships, creating competitive advantages for manufacturers that achieve compatibility through innovation rather than cost replication. Distribution consolidation around e-commerce platforms, including Shopee, Lazada, and Amazon, creates new competitive dynamics favoring digital-native brands with influencer relationships and performance marketing capabilities over traditional retail-dependent competitors.

Key Market Developments

- In January 2025, OtterBox launches a comprehensive Galaxy S25 case portfolio featuring expanded Symmetry Series and redesigned Defender Series options with Cactus Leather finish variants, demonstrating rapid OEM device compatibility and design diversification addressing premium consumer aesthetics demands.

- In September 2024, Belkin announces 11 new travel-ready mobile charging and protective accessories, expanding its portfolio of portable protection solutions and integrated charging ecosystem functionality, reflecting a strategic emphasis on multifunctional accessories that support remote work and mobile lifestyles.

- In January 2024, Spigen introduces MagSafe-compatible case collection, engineered for seamless integration with Apple's proprietary magnetic ecosystem and accessory compatibility, capturing expanding demand among iPhone users upgrading to MagSafe-enabled models.

Companies Covered in Asia Pacific Mobile Protective Cases Market

- Apple Inc (Cupertino)

- Samsung Electronics Co Ltd (Seoul)

- Reiko Wireless Inc (New Jersey)

- Pelican Products Inc (Torrance)

- Moshi (San Francisco)

- Otter Products LLC (Fort Collins)

- Griffin Technology Inc (Nashville)

- Belkin International Inc (Los Angeles)

- CG Mobile Ltd (Hong Kong)

- Incipio LLC (Culver City)

- Spigen Inc (Seoul)

- Urban Armor Gear UAG (Los Angeles)

- Casetify (Hong Kong)

- ESR (Shanghai)

- Nillkin (Shenzhen)

Frequently Asked Questions

The Asia Pacific Mobile Protective Cases Market is projected to reach US$ 22.8 billion by 2033 from US$ 14.4 billion in 2026, representing a 6.8% CAGR during the forecast period, driven by accelerating smartphone penetration, rising device costs, and expanding consumer demand for multifunctional protective accessories.

Premium smartphone adoption, particularly Samsung Galaxy Z-series foldables and Apple iPhone ecosystem expansion, combined with rising disposable incomes across India and Southeast Asia, e-commerce platform accessibility, and 5G network rollout enabling device upgrade cycles, serve as primary demand drivers sustaining above-average growth trajectories throughout the forecast period.

Back plate cases command 59.6% market share due to consumer preference for slim-profile protection, wireless charging compatibility, and device aesthetic preservation, alongside rapid adoption of MagSafe-compatible back plate variants among Apple iPhone users seeking magnetic accessory integration without full-coverage design constraints.

India represents the fastest-growing regional market with 10.2% CAGR through 2033, propelled by government manufacturing incentives, smartphone export expansion exceeding US$21 billion in 2024, and expanding middle-class populations across tier-2 and tier-3 urban centers seeking affordable protective solutions.

Foldable smartphone protection emerges as the transformational opportunity, with the foldable smartphone market expansion, enabling premium case pricing of US$30-80 per unit compared to traditional protective cases averaging US$15-40, supported by Samsung Galaxy Z-Fold, Google Pixel Fold, and Motorola Razr competitive acceleration.

OtterBox and Spigen command consolidated leadership through complementary strategies: OtterBox emphasizes extreme durability and premium features commanding 15-18% brand share, while Spigen dominates mid-market and e-commerce through rapid compatibility and affordable pricing capturing 12-15% market share on Amazon and regional e-commerce platforms.