1. Executive Summary

1.1. Global Alopecia Treatment Market Snapshot, 2025 and 2032

1.2. Market Opportunity Assessment, 2025 – 2032, US$ Bn

1.3. Key Market Trends

1.4. Future Market Projections

1.5. Premium Market Insights

1.6. Industry Developments and Key Market Events

1.7. PMR Analysis and Recommendations

2. Market Overview

2.1. Market Scope and Definition

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Opportunity

2.2.4. Challenges

2.2.5. Key Trends

2.3. Macro-Economic Factors

2.3.1. Global Sectorial Outlook

2.3.2. Global GDP Growth Outlook

2.4. COVID-19 Impact Analysis

2.5. Forecast Factors – Relevance and Impact

3. Value Added Insights

3.1. Regulatory Landscape

3.2. Product Adoption Analysis

3.3. Value Chain Analysis

3.4. Key Deals and Mergers

3.5. PESTLE Analysis

3.6. Porter’s Five Force Analysis

4. Global Alopecia Treatment Market Outlook:

4.1. Key Highlights

4.1.1. Market Size (US$ Bn) and Y-o-Y Growth

4.1.2. Absolute $ Opportunity

4.2. Market Size (US$ Bn) Analysis and Forecast

4.2.1. Historical Market Size (US$ Bn) Analysis, 2019-2023

4.2.2. Current Market Size (US$ Bn) Analysis and Forecast, 2025–2032

4.3. Global Alopecia Treatment Market Outlook: Treatment Type

4.3.1. Introduction / Key Findings

4.3.2. Historical Market Size (US$ Bn) Analysis, By Treatment Type, 2019 – 2023

4.3.3. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

4.3.3.1. Topical Drugs

4.3.3.1.1. Creams

4.3.3.1.2. Oils

4.3.3.1.3. Gels

4.3.3.1.4. Shampoo

4.3.3.1.5. Lotion

4.3.3.1.6. Foam

4.3.3.2. Oral Drugs

4.3.3.3. Injectable

4.3.3.3.1. Platelet Rich Plasma

4.3.3.3.2. Steroid Injections

4.3.3.3.3. Injectable Filler

4.3.3.4. Hair Transplant Services

4.3.3.5. Low-Level Laser Therapy

4.3.4. Market Attractiveness Analysis: Treatment Type

4.4. Global Alopecia Treatment Market Outlook: End User

4.4.1. Introduction / Key Findings

4.4.2. Historical Market Size (US$ Bn) Analysis, By End User, 2019 – 2023

4.4.3. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

4.4.3.1. Hospitals

4.4.3.2. Dermatologic and Trichology Clinics

4.4.3.3. Home Care Settings

4.4.3.4. Aesthetic Clinics

4.4.4. Market Attractiveness Analysis: End User

5. Global Alopecia Treatment Market Outlook: Region

5.1. Key Highlights

5.2. Historical Market Size (US$ Bn) Analysis, By Region, 2019 – 2023

5.3. Current Market Size (US$ Bn) Analysis and Forecast, By Region, 2025 – 2032

5.3.1. North America

5.3.2. Europe

5.3.3. East Asia

5.3.4. South Asia and Oceania

5.3.5. Latin America

5.3.6. Middle East & Africa

5.4. Market Attractiveness Analysis: Region

6. North America Alopecia Treatment Market Outlook:

6.1. Key Highlights

6.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

6.2.1. By Country

6.2.2. By Treatment Type

6.2.3. By End User

6.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

6.3.1. U.S.

6.3.2. Canada

6.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

6.4.1. Topical Drugs

6.4.1.1. Creams

6.4.1.2. Oils

6.4.1.3. Gels

6.4.1.4. Shampoo

6.4.1.5. Lotion

6.4.1.6. Foam

6.4.2. Oral Drugs

6.4.3. Injectable

6.4.3.1. Platelet Rich Plasma

6.4.3.2. Steroid Injections

6.4.3.3. Injectable Filler

6.4.4. Hair Transplant Services

6.4.5. Low-Level Laser Therapy

6.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

6.5.1. Hospitals

6.5.2. Dermatologic and Trichology Clinics

6.5.3. Home care settings

6.5.4. Aesthetic Clinics

6.6. Market Attractiveness Analysis

7. Europe Alopecia Treatment Market Outlook:

7.1. Key Highlights

7.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

7.2.1. By Country

7.2.2. By Treatment Type

7.2.3. By End User

7.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

7.3.1. Germany

7.3.2. France

7.3.3. U.K.

7.3.4. Italy

7.3.5. Spain

7.3.6. Russia

7.3.7. Türkiye

7.3.8. Rest of Europe

7.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

7.4.1. Topical Drugs

7.4.1.1. Creams

7.4.1.2. Oils

7.4.1.3. Gels

7.4.1.4. Shampoo

7.4.1.5. Lotion

7.4.1.6. Foam

7.4.2. Oral Drugs

7.4.3. Injectable

7.4.3.1. Platelet Rich Plasma

7.4.3.2. Steroid Injections

7.4.3.3. Injectable Filler

7.4.4. Hair Transplant Services

7.4.5. Low-Level Laser Therapy

7.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

7.5.1. Hospitals

7.5.2. Dermatologic and Trichology Clinics

7.5.3. Home care settings

7.5.4. Aesthetic Clinics

7.6. Market Attractiveness Analysis

8. East Asia Alopecia Treatment Market Outlook:

8.1. Key Highlights

8.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

8.2.1. By Country

8.2.2. By Treatment Type

8.2.3. By End User

8.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

8.3.1. China

8.3.2. Japan

8.3.3. South Korea

8.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

8.4.1. Topical Drugs

8.4.1.1. Creams

8.4.1.2. Oils

8.4.1.3. Gels

8.4.1.4. Shampoo

8.4.1.5. Lotion

8.4.1.6. Foam

8.4.2. Oral Drugs

8.4.3. Injectable

8.4.3.1. Platelet Rich Plasma

8.4.3.2. Steroid Injections

8.4.3.3. Injectable Filler

8.4.4. Hair Transplant Services

8.4.5. Low-Level Laser Therapy

8.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

8.5.1. Hospitals

8.5.2. Dermatologic and Trichology Clinics

8.5.3. Home care settings

8.5.4. Aesthetic Clinics

8.6. Market Attractiveness Analysis

9. South Asia & Oceania Alopecia Treatment Market Outlook:

9.1. Key Highlights

9.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

9.2.1. By Country

9.2.2. By Treatment Type

9.2.3. By End User

9.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

9.3.1. India

9.3.2. Southeast Asia

9.3.3. ANZ

9.3.4. Rest of South Asia & Oceania

9.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

9.4.1. Topical Drugs

9.4.1.1. Creams

9.4.1.2. Oils

9.4.1.3. Gels

9.4.1.4. Shampoo

9.4.1.5. Lotion

9.4.1.6. Foam

9.4.2. Oral Drugs

9.4.3. Injectable

9.4.3.1. Platelet Rich Plasma

9.4.3.2. Steroid Injections

9.4.3.3. Injectable Filler

9.4.4. Hair Transplant Services

9.4.5. Low-Level Laser Therapy

9.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

9.5.1. Hospitals

9.5.2. Dermatologic and Trichology Clinics

9.5.3. Home care settings

9.5.4. Aesthetic Clinics

9.6. Market Attractiveness Analysis

10. Latin America Alopecia Treatment Market Outlook:

10.1. Key Highlights

10.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

10.2.1. By Country

10.2.2. By Treatment Type

10.2.3. By End User

10.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

10.3.1. Brazil

10.3.2. Mexico

10.3.3. Rest of Latin America

10.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

10.4.1. Topical Drugs

10.4.1.1. Creams

10.4.1.2. Oils

10.4.1.3. Gels

10.4.1.4. Shampoo

10.4.1.5. Lotion

10.4.1.6. Foam

10.4.2. Oral Drugs

10.4.3. Injectable

10.4.3.1. Platelet Rich Plasma

10.4.3.2. Steroid Injections

10.4.3.3. Injectable Filler

10.4.4. Hair Transplant Services

10.4.5. Low-Level Laser Therapy

10.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

10.5.1. Hospitals

10.5.2. Dermatologic and Trichology Clinics

10.5.3. Home care settings

10.5.4. Aesthetic Clinics

10.6. Market Attractiveness Analysis

11. Middle East & Africa Alopecia Treatment Market Outlook:

11.1. Key Highlights

11.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

11.2.1. By Country

11.2.2. By Treatment Type

11.2.3. By End User

11.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

11.3.1. GCC Countries

11.3.2. Egypt

11.3.3. South Africa

11.3.4. Northern Africa

11.3.5. Rest of Middle East & Africa

11.4. Current Market Size (US$ Bn) Analysis and Forecast, By Treatment Type, 2025 – 2032

11.4.1. Topical Drugs

11.4.1.1. Creams

11.4.1.2. Oils

11.4.1.3. Gels

11.4.1.4. Shampoo

11.4.1.5. Lotion

11.4.1.6. Foam

11.4.2. Oral Drugs

11.4.3. Injectable

11.4.3.1. Platelet Rich Plasma

11.4.3.2. Steroid Injections

11.4.3.3. Injectable Filler

11.4.4. Hair Transplant Services

11.4.5. Low-Level Laser Therapy

11.5. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

11.5.1. Hospitals

11.5.2. Dermatologic and Trichology Clinics

11.5.3. Home care settings

11.5.4. Aesthetic Clinics

11.6. Market Attractiveness Analysis

12. Competition Landscape

12.1. Market Share Analysis, 2025

12.2. Market Structure

12.2.1. Competition Intensity Mapping By Market

12.2.2. Competition Dashboard

12.3. Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

12.3.1. Elli Lilly and Company

12.3.1.1. Overview

12.3.1.2. Segments and Products

12.3.1.3. Key Financials

12.3.1.4. Market Developments

12.3.1.5. Market Strategy

12.3.2. Teva Pharmaceutical Industries Ltd.

12.3.3. Merck & Co., Inc.

12.3.4. Johnson & Johnson, Inc.

12.3.5. Dr. Reddy’s Laboratories Ltd.

12.3.6. Cipla Ltd.

12.3.7. Cellmid Ltd.

12.3.8. The Himalaya Drug Company

12.3.9. Taisho Pharmaceutical Holdings Co., Ltd

12.3.10. Shiseido Co., Ltd.

12.3.11. Zhangguang 101 Science & Technology Co., Ltd.

12.3.12. Pfizer

12.3.13. Thera dome

12.3.14. LUTRONIC

12.3.15. Curallux

12.3.16. Sun Pharmaceutical Industries Ltd.

12.3.17. GlaxoSmithKline plc

12.3.18. Fagron

12.3.19. Apple Therapeutics Private Limited

12.3.20. Aclaris Therapeutics, Inc.

12.3.21. RepliCel Life Sciences Inc.

13. Appendix

13.1. Research Methodology

13.2. Research Assumptions

13.3. Acronyms and Abbreviations

- Pharmaceuticals

- Alopecia Treatment Market

Alopecia Treatment Market Size, Share, and Growth Forecast for 2025 - 2032

Alopecia Treatment Market by Treatment Type (Topical Drugs, Oral Drugs, Injectable, Hair Transplant Services, Low-level Laser Therapy), End User (Hospitals, Dermatologic and Trichology Clinics), and Regional Analysis from 2025 to 2032

Alopecia Treatment Market Size and Share Analysis

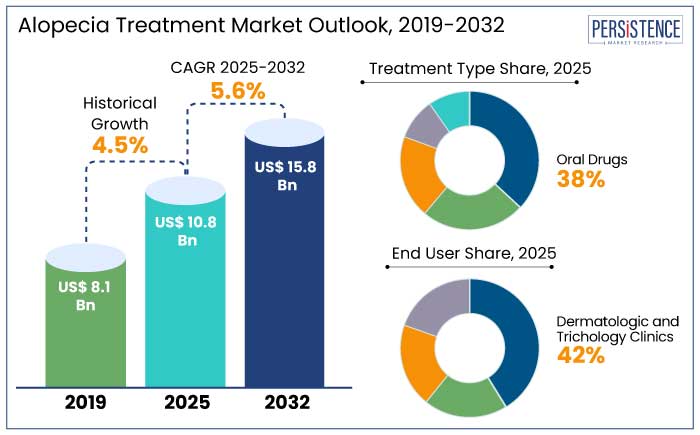

The global alopecia treatment market is projected to witness a CAGR of 5.6% during the forecast period from 2025 to 2032. It is anticipated to increase from US$ 10.8 Bn recorded in 2025 to a decent US$ 15.8 Bn by 2032.

Demand for alopecia treatment is driven by increasing awareness of treatment options and the high prevalence of hair loss. Over 95% of hair loss in men is caused by androgenetic alopecia, with nearly 40% of men experiencing some degree of hair loss by 35 years of age.

The need for treatment for androgenetic alopecia is expected to grow in revenue. Around 60% of the global population has hair thinning problems, with pattern hair loss being the most common form.

Healthcare expenditure is driving the industry due to rising consumer disposable income and a focus on aesthetic appearance in major countries. Organizations like the National Alopecia Areata Foundation and the American Hair Loss Association are promoting hair regrowth treatments, boosting healthcare expenditure, and driving market growth due to minimal side effects.

Key Highlights of the Market

- Growing prevalence of hair loss conditions worldwide is driving treatment innovations for alopecia.

- Increasing psychological impact of alopecia is driving the need for advanced treatment solutions.

- Research investments in regenerative medicine and hair restoration technologies are on the rise.

- Innovations in stem cell and gene therapy are paving the way for new market opportunities.

- In 2025, Europe is estimated to hold 29% of the global market share with surging investments in hair care research.

- North America is projected to account for 37% of the global market share in 2025 owing to its robust healthcare infrastructure and government support.

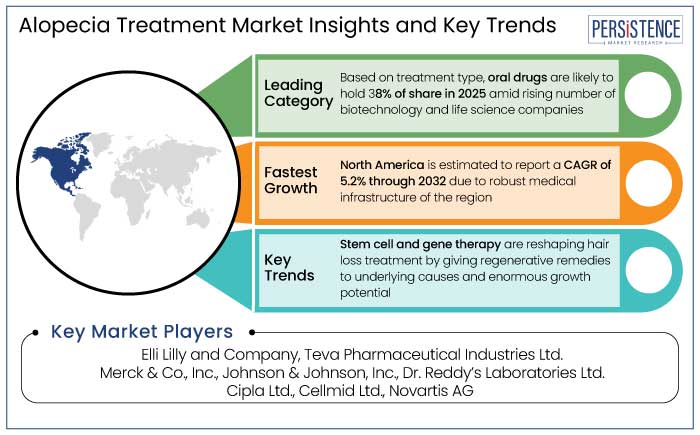

- In terms of treatment type, oral drugs are anticipated to generate a share of 38% in 2025 due to their easy to consume formulation.

- Dermatologic and trichology clinics are estimated to hold 42% of share in 2025 due to easy access to unique technologies, personalized treatments, and rising patient trust.

|

Market Attributes |

Key Insights |

|

Alopecia Treatment Market Size (2025E) |

US$ 10.8 Bn |

|

Projected Market Value (2032F) |

US$ 15.8 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

4.5% |

North America Supports Innovative Therapies for Hair Care

North America is significant in the alopecia therapy industry, accounting for 37% of the total share in 2025. This is attributed to the high prevalence of the disease, government measures, and healthcare infrastructure improvements. North America is projected to report a CAGR of 5.2% from 2025 to 2032.

Government and non-profit organizations like the National Alopecia Areata Foundation and the Canadian Alopecia Areata Foundation are also contributing to the market. For example,

- Alopecia areata, a common symptom of the autoimmune disease, affects an estimated 6.8 million patients in the U.S., affecting men and women of any ethnic origin. Alopecia areata is the second most prevalent type after androgenetic alopecia, with one in 500 to one in 1,000 Americans affected.

- Big players like Eli Lilly are developing new drugs and therapies, such as baricitinib oral pills, which were approved by the FDA in October 2022.

Europe Shows Growth Potential for Hair Restoration Solutions

In 2025, the market for hair restoration and transfiguration in Europe is estimated to hold a share of 29%. The EU's second-largest producer of active biopharmaceutical drugs is seeing growth, with a forecast CAGR of 5.9% by 2032.

The need for hair restoration and transfiguration products has increased due to urban residents in Europe using 30% more hair care products than they did five years ago. In Germany, platelet-rich plasma treatment is likewise being utilized as a secure and efficient substitute for finasteride and minoxidil.

The growing number of cases of hair loss brought on by unhealthy eating habits, smoking, high levels of stress, and lifestyle choices is propelling the alopecia treatment industry in Europe. Europe's alopecia treatment market is thriving due to Germany's established healthcare system, public awareness, top pharmaceutical corporations, and advanced research.

Development of Oral Drugs Paves the Way for Better Formulations

The need for the discovery and production of biological products, as well as the growing number of biotechnology and life science firms, are predicted to drive demand for oral drugs to 38% of market share in 2025. Patients who are having fast hair loss are advised to take oral corticosteroids; these drugs are inexpensive but may have side effects. The most often recommended medication for androgenetic alopecia, or systemic hair loss, is finasteride.

Compared to topical or non-invasive remedies, oral formulations are more readily available and offer consistent dosages. Their usage is also being encouraged by innovative compounds with improved safety profiles and new advancements in oral formulations. Oral formulations are becoming more and more popular in the global alopecia therapy market due to patient awareness and dermatologists' evolving views.

Dermatologic and Trichology Clinics Provide Specialized Treatment for Patients

Clinics that specialize in trichology and dermatology are becoming well-known because of their cutting-edge technology, individualized care, and rising patient confidence. Dermatologic and trichology clinics are anticipated to account for 42% of the market share in 2025.

The comfort and seclusion of these clinics are the main reasons for their appeal, especially in nations like China, South Korea, Japan, and Malaysia. Demand for hair loss treatments and service provider prices have benefited from the expansion of private clinics. Personalized alopecia therapy prediction systems were introduced by genetic testing firms in 2024, and these showed 70% accuracy in determining treatment response.

Market Introduction and Trend Analysis

The alopecia treatment market is growing due to the rising prevalence of hair loss, psychological effects, and investments in regenerative medicine. Consumer knowledge and a decrease in stigma also increase investments in medical and cosmetic hair restoration.

Regenerative medicine has demonstrated 65% hair follicle regeneration potential, with leading pharmaceutical companies investing US$ 380 Mn in unique hair restoration technologies. The FDA accelerated approval processes for novel alopecia treatments, with Pfizer and Johnson & Johnson launching advanced topical and oral medications.

Mental health research has highlighted the psychological impacts of hair loss, leading to increased insurance coverage for comprehensive alopecia treatment programs. Personalized medicine and solutions have emerged, with genetic testing companies launching personalized alopecia treatment prediction platforms with 70% accuracy.

Unique laser and light therapy technologies have shown 55% improvement in hair follicle stimulation, and non-invasive treatment options gained market traction. Research shows that worldwide, people are 80% more interested in all-inclusive treatments for alopecia. These options include new non-invasive techniques, customized genetic approaches, help with psychological support, and stem cell regeneration technology.

Historical Growth and Course Ahead

The global alopecia treatment market recorded a decent CAGR of 4.5% in the historical period from 2019 to 2023. Based on the post-pandemic research, Alopecia affects more than 50 million U.S. citizens, including 30 million women and 50 million men.

Rising incidence of the ailment is driving the market for alopecia therapies. About 60% of people experience pattern hair loss, with gender-specific differences in severity. For instance,

- The good outcomes of Phase 2b 3 ALLEGRO, an oral Ritlecitinib medication used once daily, were reported by Pfizer Inc. in August 2021. The medication is intended to treat alopecia areata, an autoimmune disorder that causes hair loss on the scalp.

- The first systemic treatment for alopecia, baricitinib (Olumiant), was authorized by the FDA in June 2022 to treat severe instances of alopecia areata. This medicine has been approved for Elli Lilly and Company.

- Baricitinib is the first medication of its kind to be approved by the FDA for the treatment of body-wide hair loss.

Market Growth Drivers

Prevalence of Hair Loss Conditions Boosts Demand for Hair Care Solutions

Rising prevalence of hair loss conditions, such as androgenetic alopecia and alopecia areata, is driving growth in hair loss treatments. Increasing stress, hormonal imbalances, and aging have contributed to higher incidences of hair loss, with around 50 million men and 30 million women affected in the U.S. alone. For example,

- Companies like Pfizer and Concert Pharmaceuticals are at the forefront of innovation, with Pfizer's ritlecitinib receiving FDA approval in June 2023 as a first-of-its-kind oral treatment for alopecia areata.

- Johnson & Johnson's Rogaine remains a trusted option for androgenetic alopecia.

Unique treatments like PRP therapy and stem cell-based solutions are gaining popularity due to the global demand for non-invasive, effective alopecia treatments.

Alopecia's Psychological Impact Drives Demand for Stigma-free Treatments

The psychological impact of alopecia is driving demand for novel treatment solutions, with research investments in regenerative medicine and hair restoration technologies increasing. For example,

- Mental health research has led to a 45% increase in insurance coverage for comprehensive alopecia treatment programs.

- Advanced laser and light therapy technologies have shown a 55% improvement in hair follicle stimulation, and non-invasive treatment options have gained market traction.

- International market research revealed an 80% increased interest in comprehensive alopecia treatment solutions across diverse demographics.

Genetic research is revolutionizing treatment by using personalized medicine based on individual genetic makeup. Pharmacogenomics enables clinicians to identify hair loss mutations, enabling targeted treatments and creating drugs that align with a patient's genetic characteristics, promoting efficacy and minimizing side effects.

Market Restraining Factors

Limited Efficacy of Hair Loss Solutions Affects Industry

The global market for hair loss treatments is hindered by a lack of data on their therapeutic efficacy. Topical treatments like minoxidil are considered moderately effective, but not 100% effective against alopecia.

Laser treatments are often unaffordable, especially across countries in Asia Pacific and Middle East and Africa. High treatment costs, including novel treatments like PRP therapy and hair transplant surgeries, limit accessibility for many patients. For instance,

- Treatment variability also affects success rates, with success rates ranging between 40 to 60% depending on the type and individual patient factors.

Insurance coverage disparities hinder treatment access, disproportionately affecting middle- and low-income populations. To address this, initiatives to make advanced therapies more affordable through subsidies, insurance inclusion, or cost-effective innovations are needed.

Key Market Opportunities

Innovation in Stem Cell and Gene Therapy Shows High Potential

Stem cell and gene therapy are reshaping hair loss treatment by giving regenerative remedies to underlying causes and enormous growth potential. Stem cell therapy, for example, has demonstrated the potential to stimulate hair follicle growth, with companies like Stemson Therapeutics developing unique cell-based regenerative treatments.

- In October 2023, Stemson received US$ 15 Mn in funding to boost its preclinical research. Similarly, gene therapy innovations are addressing genetic predispositions to hair loss.

- Researchers at Harvard University launched gene-editing techniques using CRISPR to manipulate hair follicle regeneration, marking a breakthrough in personalized treatments.

Such novel technologies provide long-term, minimally invasive solutions to meet the high health-conscious and aesthetics-driven consumer base.

Rising Investments in Research on Hair Treatment Present Growth Prospects

Demand for alopecia treatment solutions is anticipated to rise because of more investments in research and development with modern medications and formulations. For instance,

- Clinical research using JAK inhibitors, which have demonstrated efficacy in regrowing hair in alopecia areata patients, has received US$ 1.65 Mn from the National Alopecia Areata Foundation (NAAF).

The market will also be driven by the foundation's calculated investments in immunogenetic research and a mouse model. The demand for hair fall treatments will increase even more thanks to strategic alliances with public and private institutions.

- Unique topical and oral treatments from Pfizer and Johnson & Johnson are examples of pharmaceutical advances that have demonstrated 55% enhanced hair regeneration rates.

- Genetic testing businesses' personalized medicine platforms have shown 70% accuracy in determining therapy response.

- The stimulation of hair follicles has improved by 55% due to advanced laser and light treatment technology.

Competitive Landscape for the Alopecia Treatment Market

The alopecia treatment market is extremely competitive, with established and emerging players competing for positions in the global market. Because of their cost-effectiveness and broad patient acceptability, prominent firms are concentrating on oral formulations and creating innovative medicines.

Companies are collaborating strategically with industry leaders to remain ahead of the curve by utilizing their knowledge of formulation science, medication delivery technologies, and regulatory clearances. Pharmaceutical companies are spending money on the research and development of innovative oral formulations with enhanced bioavailability and precise distribution. To improve their alopecia treatment services, key rivals are extending business partnerships and combining through mergers and acquisitions.

?Recent Industry Developments

- In October 2024, Dr. Batra's Group introduced XOGEN, a treatment for hereditary hair loss using exosomes for targeted growth, requiring four to five sessions and a simple hair care routine.

- In September 2024, Eli Lilly and EVA Pharma agreed to extend baricitinib's access to 20,000 people in 49 low- to middle-income African countries by 2030, treating rheumatoid arthritis, alopecia areata, atopic dermatitis, and COVID-19.

- In September 2024, Amplifica Holdings Group conducted its first-in-human trial of AMP-303, a new injectable treatment for androgenetic alopecia. The study found no severe adverse events and showed significant non-vellus hair count increases.

- In July 2024, Aveda introduced the Invati Ultra Advanced Collection, a five-step anti-hair loss system combining Ayurvedic remedies and vegan ingredients, including shampoo, conditioner, serum, and foam.

- In July 2024, Kintor Pharmaceutical planned to commercialize its hair-loss product, KX-826, as an over-the-counter drug after disappointing clinical trials. The move could provide Kintor's first recurring revenue, though it may struggle to compete with regulator-approved products like Rogaine.

- In June 2024, Lumenis Be. Ltd. introduced FoLix, the first FDA-cleared proprietary fractional laser for hair loss treatment, targeting 85% of men and 50% of women. It offers 4-6 monthly sessions without chemicals, needles, anesthesia, surgery, or downtime.

- In May 2024, Researchers at MIT, Brigham and Women's Hospital, and Harvard Medical School developed a microneedle patch for alopecia areata, an autoimmune disorder causing hair loss. The treatment reduces inflammation and allows hair growth.

- In June 2023, Cipla Limited expanded its alopecia treatment portfolio by launching a generic formulation of minoxidil as a topical hair loss treatment.

Companies Covered in Alopecia Treatment Market

- Elli Lilly and Company

- Teva Pharmaceutical Industries Ltd.

- Merck & Co., Inc.

- Johnson & Johnson, Inc.

- Dr. Reddy’s Laboratories Ltd.

- Cipla Ltd.

- Cellmid Ltd.

- The Himalaya Drug Company

- Taisho Pharmaceutical Holdings Co., Ltd

- Shiseido Co., Ltd.

- Zhangguang 101 Science & Technology Co., Ltd.

- Pfizer

- Thera dome

- LUTRONIC

- Curallux

- Sun Pharmaceutical Industries Ltd.

- GlaxoSmithKline plc

- Fagron

- Apple Therapeutics Private Limited

- Aclaris Therapeutics, Inc.

- RepliCel Life Sciences Inc.

Frequently Asked Questions

The market size is set to reach US$ 15.8 Bn by 2032.

Researchers have developed a new treatment for alopecia areata, an autoimmune disorder causing hair loss, using a microneedle patch to deliver immune-regulating molecules.

In 2025, North America is set to attain a market share of 37%.

In 2025, the market is estimated to be valued at US$ 10.8 Bn.

Elli Lilly and Company, Teva Pharmaceutical Industries Ltd., Merck & Co., Inc., Johnson & Johnson, Inc., and Dr. Reddy’s Laboratories Ltd. are considered the leading players.