- HVAC

- Whisper Valve Market

Whisper Valve Market Size, Share, and Growth Forecast, 2026- 2033

Whisper Valve Market by Pressure Range (Up to 25 psig, 26–200 psig, 200–300 psig, 300–500 psig), By Application (Industrial, Medical, Food & Beverage, Hot-Air Balloon, and Others), By End-User Industry (Oil & Gas, Water & Wastewater, Power Generation, Chemical Processing, Pharmaceuticals, and Others), and Regional Analysis for 2026 – 2033.

Whisper Valve Market Size and Trends Analysis

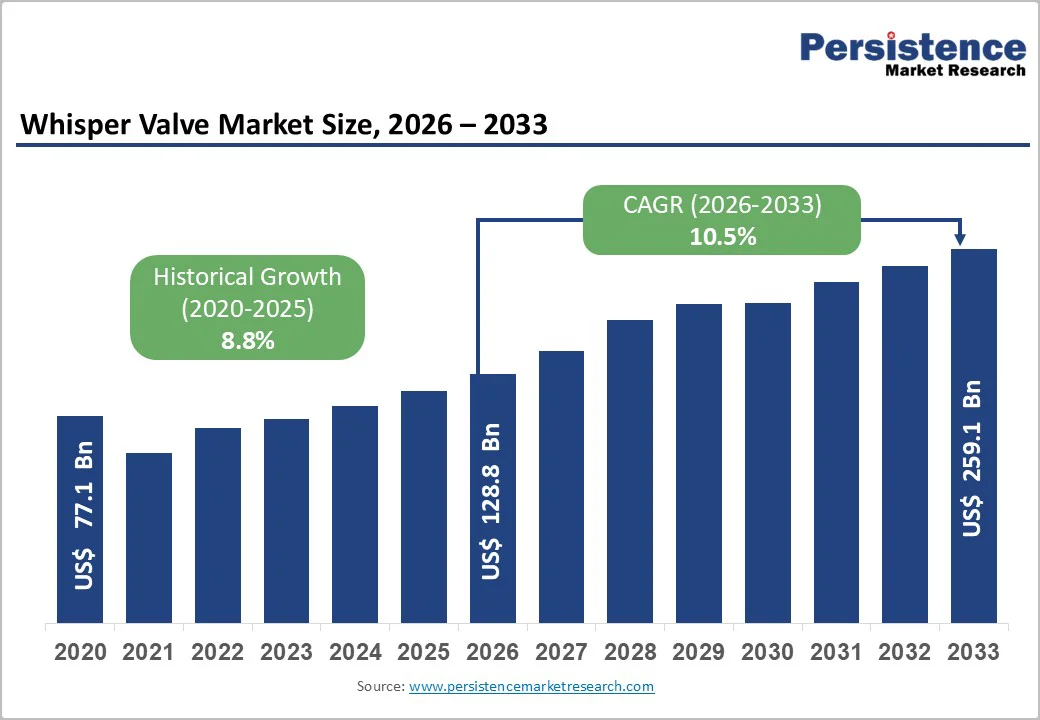

The global Whisper Valve market size was valued at US$ 128.8 Billion in 2026 and is projected to reach US$ 259.1 Billion by 2033, growing at a CAGR of 10.5% between 2026 and 2033. Whisper valves, engineered for low-noise operation in pressure regulation systems, benefit from rising industrial automation and stringent noise pollution controls. Historical growth at 8.8% CAGR from 2020 (US$ 77.1 Billion) reflects adoption in high-pressure environments.

Key drivers include regulatory mandates from agencies like the U.S. EPA and EU noise directives, alongside energy efficiency demands in oil & gas and water sectors, positioning the market for sustained expansion amid global infrastructure investments.

Key Industry Highlights:

- Regulatory Driven Demand: OSHA and EU noise regulations significantly boost adoption, with low-noise valve installations rising 15–20% since 2020 to avoid penalties and ensure worker safety.

- High Cost Constraint: Precision manufacturing and specialty materials raise whisper valve prices 20–30% above standard valves, limiting adoption among cost-sensitive industries and emerging markets.

- Water Infrastructure Opportunity: Global water and wastewater investments near US$945 billion through 2030, creating US$20–30 billion opportunity via low-noise pump stations and energy-efficient retrofits.

- Healthcare Expansion: Medical and pharmaceutical applications grow at 11.6% CAGR, driven by hospital expansion, cleanroom standards, and demand for silent HVAC and diagnostic equipment.

- Low-Pressure Dominance: Up to 25 psig systems dominate over 30% market share, widely used in medical devices, food processing, and HVAC retrofits requiring stable, hygienic pressure control.

- Mid-Pressure Growth: The 26–200 psig segment is fastest growing at 11.4% CAGR, fueled by oil and gas compression, industrial automation, and balanced efficiency-noise performance.

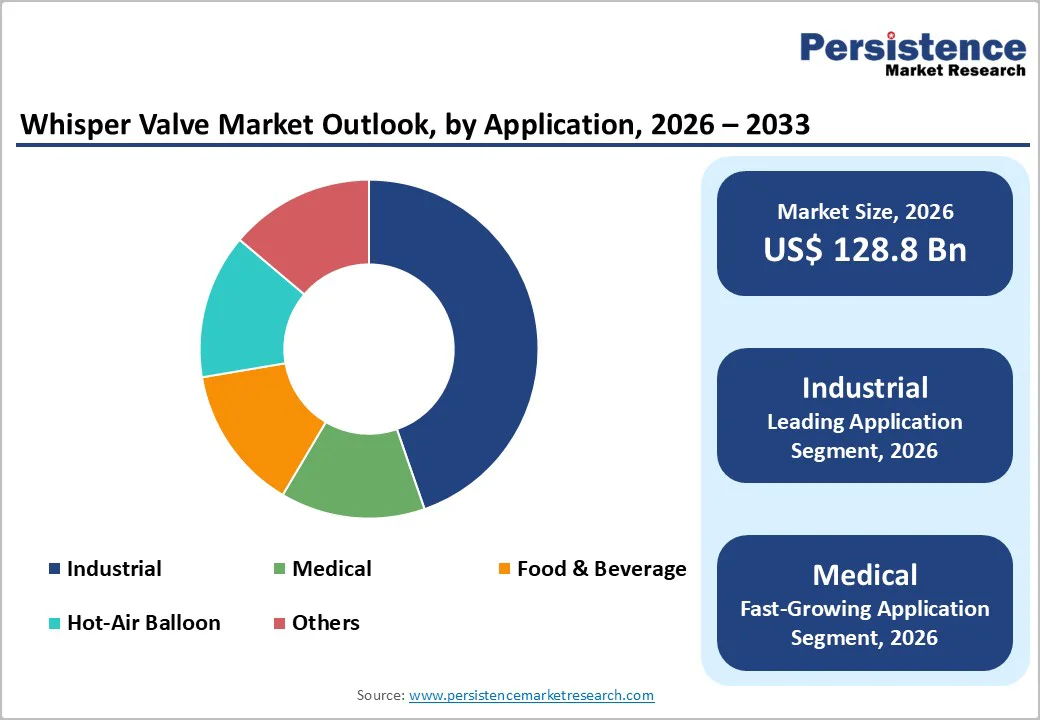

- Industrial Application Leadership: Industrial noise control leads with over 45% revenue share, supported by heavy deployment across factories, compressors, turbines, and power generation facilities.

- Oil Gas Dominance: Oil and gas remains the largest end-user, exceeding 30% share, driven by pipeline integrity, offshore regulations, and rising safety and acoustic monitoring requirements.

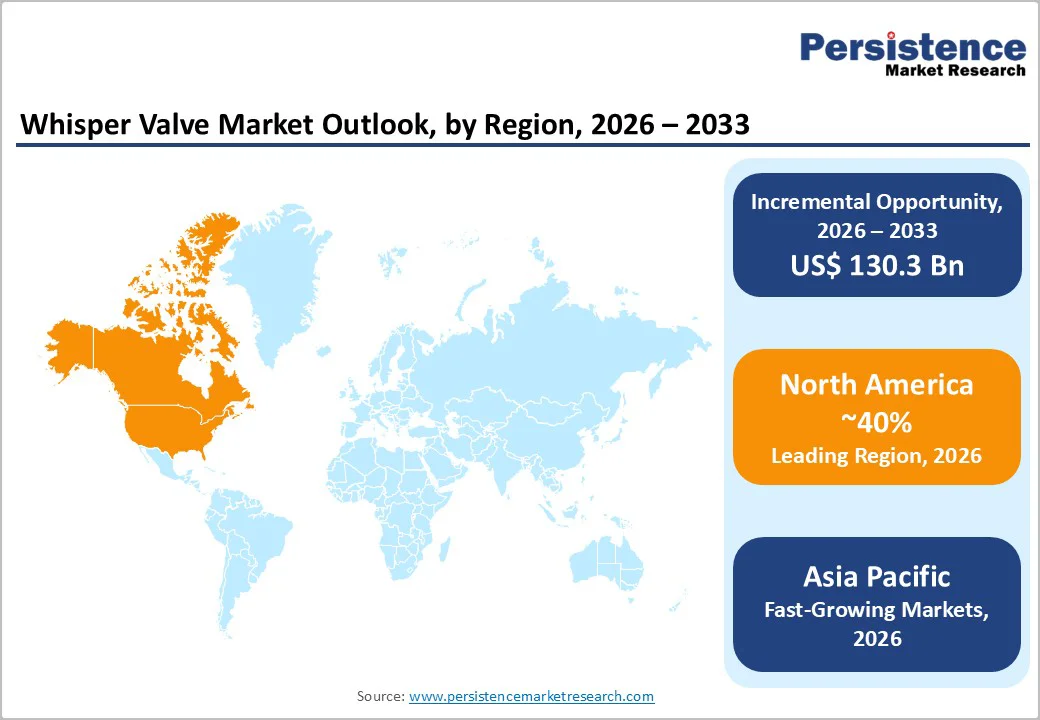

- Asia Pacific Momentum: Asia Pacific is fastest-growing at 11.7% CAGR, supported by Belt and Road investments, wastewater expansion, lower manufacturing costs, and strong regulatory enforcement.

| Global Market Attributes | Key Insights |

|---|---|

| Whisper Valve Market Size (2026E) | US$ 128.8 Bn |

| Market Value Forecast (2033F) | US$ 259.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.8% |

Market Dynamics

Key Growth Drivers

Regulatory Compliance on Noise Pollution

Global regulations increasingly target industrial noise levels, spurring whisper valve demand. The U.S. Occupational Safety and Health Administration (OSHA) mandates exposure limits below 85 dB(A), while the EU's Noise Directive 2003/10/EC enforces similar standards across member states. These rules have driven a 15-20% rise in low-noise valve installations in compliance audits since 2020, per International Organization for Standardization (ISO) reports. In oil & gas, where compressor stations exceed permissible noise, whisper valves reduce violations by up to 30 dB, cutting fines averaging US$ 50,000 per incident. This driver directly boosts market penetration, with affected sectors contributing over 45% of revenue, as firms prioritize retrofits to avoid operational halts and enhance worker safety.

Market Restraining Factors

High Initial Costs and Manufacturing Complexity

Whisper valves command 20-30% premiums over standard valves due to precision machining and specialty materials, deterring small enterprises. ASME B16.34 compliance adds 15% to production costs, with supply chain volatility inflating alloy prices 10-15% post-2022. In emerging markets, this limits uptake to 25% of potential sites, capping growth at 7% in budget-constrained segments and risking 5-10% market share erosion to cheaper alternatives.

Regulatory Variability Across Regions

Divergent standards e.g., ANSI in North America vs. EN 1349 in Europe complicate certification, delaying launches by 6-12 months and raising compliance costs 15%. In Asia Pacific, inconsistent enforcement in ASEAN nations hinders scalability, potentially stalling 8% of projected growth where harmonization lags.

Whisper Valve Market Trends and Opportunities

Infrastructure Healthcare Investments Accelerate Whisper Valve Demand Across Global High-Growth Markets Rapidly

Expansion in the water and wastewater sector is emerging as a critical growth engine for the whisper valve market. This segment is projected to expand at an 11.3% CAGR, supported by nearly US$ 945 billion in global water infrastructure investments planned through 2030, according to the World Bank. Whisper valves play a vital role in pump stations by significantly reducing flow-induced noise, helping municipalities cut urban noise complaints by nearly 40%. Rapidly urbanizing regions such as India and ASEAN present strong untapped potential, as wastewater treatment capacities are expected to double. Retrofit projects alone offer up to 15% energy savings, creating an addressable opportunity valued between US$ 20–30 billion.

Medical and pharmaceutical applications represent another high-growth avenue, expanding at an estimated 11.6% CAGR. Rising adoption of ISO 14644 cleanroom standards and the expansion of the global pharmaceutical industry toward a US$ 2 trillion valuation by 2030, as highlighted by PhRMA, are accelerating demand for low-noise HVAC valve solutions. Asia Pacific hospital infrastructure investments alone could unlock an additional US$ 5–10 billion opportunity.

Regionally, Asia Pacific leads growth at an 11.7% CAGR, supported by large-scale energy and water investments under China’s Belt and Road Initiative. Combined with manufacturing costs nearly 20% below the global average, localized production is expected to drive up to US$ 50 billion in incremental revenue by 2033.

Whisper Valve Market Insights and Trends

Pressure Range Insights

Low-Pressure Dominance and Mid-Range Expansion Reshape Global Pressure-Control Equipment Demand

The pressure range analysis highlights a clear bifurcation in market dynamics between low-pressure dominance and accelerating mid-range growth. Systems operating at up to 25 psig represent the leading segment, accounting for more than 30% of total market revenue. This segment is projected to be valued at approximately US$ 38.6 billion in 2026, driven largely by its widespread use in medical devices and food and beverage processing. Low-pressure systems are critical in applications where operational stability, hygiene, and safety are paramount. Equipment such as ventilators, anesthesia machines, and sensitive processing units rely on consistent low-pressure performance, reinforcing steady demand. Additionally, nearly 40% of industrial HVAC retrofit projects continue to specify up to 25 psig systems, further strengthening this segment’s installed base and long-term replacement demand.

In contrast, the 26–200 psig segment is emerging as the fastest-growing pressure range, expanding at a robust CAGR of 11.4%. Growth is primarily fueled by rising adoption in oil and gas compression systems, where mid-range pressures provide an optimal balance between efficiency, noise reduction, and operational control. Increasing automation across industrial processes is also favoring this range, as it offers greater precision and flexibility. By 2033, this segment is expected to capture around 25% of total market share, translating to an estimated market value of US$ 64.8 billion.

Application Insights

Industrial Noise Control Dominance Accelerates While Medical Applications Drive Rapid Market Expansion

Industrial applications represent the leading segment in the market, accounting for more than 45% of total revenue and generating approximately US$ 58 billion by 2026. This dominance is primarily driven by extensive deployment across factories, power generation facilities, and large-scale processing plants, where effective noise control solutions are critical to maintaining operational efficiency, workforce safety, and regulatory compliance. High-volume usage in equipment such as pumps, compressors, turbines, and heavy machinery continues to sustain strong demand, particularly as industries adhere to stringent occupational noise regulations set by authorities such as OSHA. Noise reduction in industrial environments not only improves worker productivity and safety but also reduces equipment wear and downtime, reinforcing long-term adoption.

In contrast, the medical application segment is emerging as the fastest-growing category, expanding at a robust CAGR of 11.6% over the forecast period. Growth is fueled by rising investments in healthcare infrastructure, hospital expansions, and increasing demand for sterile, low-noise environments. Medical valves play a crucial role in sensitive applications such as MRI rooms, ventilators, anesthesia systems, and diagnostic equipment, where quiet operation is essential for patient comfort and clinical accuracy. As global healthcare spending rises, the medical segment is projected to reach nearly US$ 40 billion by 2033, strengthening its strategic importance.

End User Industry Insights

Oil and Gas Dominance with Water Infrastructure Driving Accelerated Acoustic Monitoring Growth

The end-user industry landscape is characterized by a clear dominance of the oil and gas sector, which represents the largest revenue-contributing segment, accounting for over 30% of total market share. In value terms, the oil and gas industry is projected to generate approximately US$ 38.6 billion by 2026, supported by sustained investments in offshore platforms, subsea assets, and cross-country pipeline infrastructure. Stringent noise emission regulations for offshore operations, combined with heightened safety and environmental compliance requirements, have made advanced monitoring and control systems increasingly critical. Pipeline integrity management alone contributes nearly 35% of total deployments within this segment, as operators prioritize early leak detection, structural health monitoring, and operational reliability to reduce downtime, prevent environmental incidents, and optimize asset lifecycles. The sector’s capital-intensive nature and regulatory scrutiny continue to underpin stable, long-term demand.

In contrast, the water and wastewater segment is emerging as the fastest-growing end-user industry, expanding at a robust CAGR of 11.3% over the forecast period. Growth is strongly aligned with global sustainability initiatives, particularly United Nations goals focused on water conservation, efficient resource utilization, and resilient urban infrastructure. Municipalities and utilities are increasingly adopting energy-efficient and low-noise technologies across treatment plants, pumping stations, and distribution networks. As a result, the water and wastewater sector is expected to unlock an incremental market opportunity of nearly US$ 30 billion, driven by the need for silent, efficient, and environmentally compliant operations.

Regional Insights and Trends

North America Dominates Global Market Through Regulation, Energy Expansion, And Infrastructure Investments

North America represents the largest regional market, accounting for over 40% of global revenue, valued at approximately US$ 51.5 billion in 2026. The market is projected to nearly double, reaching US$ 103.6 billion by 2033, registering a solid compound annual growth rate (CAGR) of 10.5% over the forecast period. The United States dominates the regional landscape, contributing nearly 70% of total North American revenue. This leadership is strongly supported by expanding shale gas production, with the Energy Information Administration reporting output growth of around 20%, which continues to drive demand across energy-intensive industrial applications.

Regulatory enforcement plays a critical role in shaping market dynamics. Strict compliance requirements under the Clean Air Act, combined with Environmental Protection Agency penalties exceeding US$ 100 million annually for noise and emission violations, are accelerating the adoption of advanced low-noise and environmentally compliant technologies. These regulations have also encouraged the development of innovation clusters, particularly in Texas, where manufacturers are investing heavily in advanced engineering solutions.

The competitive environment remains moderately consolidated, with leading players investing more than US$ 2 billion in research and development, supported by Department of Energy initiatives. Looking ahead, infrastructure modernization especially wastewater treatment upgrades across the U.S. Midwest presents a significant growth opportunity, reinforcing North America’s long-term market leadership.

Asia Pacific Infrastructure Investment And Regulation Drive Rapid Industrial Market Expansion Growth

Asia Pacific represents the fastest-growing regional market, expanding at a robust 11.7% CAGR over the forecast period. The region’s share rises from nearly 20%, valued at around US$ 25.8 billion in 2026, to approximately US$ 60 billion by 2033, reflecting strong structural demand. China accounts for about 40% of regional consumption, supported by large-scale urban development, industrial upgrades, and strict environmental enforcement. India is emerging as a high-growth contributor, driven by rapid urbanization and an accelerating boom in wastewater infrastructure across the municipal and industrial sectors.

Japan continues to add value through advanced manufacturing capabilities, technology-driven efficiency, and high-quality standards, while ASEAN economies benefit from expanding export-oriented manufacturing bases. Cost competitiveness remains a critical advantage, with Asia-Pacific producers enjoying a nearly 25% cost edge due to localized supply chains and labor efficiencies. Growth is further reinforced by massive infrastructure investment, with the Asian Development Bank estimating US$ 1.7 trillion in annual infrastructure needs. Regulatory momentum, particularly China’s Eco-City mandates, is strengthening adoption note. Rising foreign direct investment, exceeding US$ 10 billion, continues to enhance capacity, technology transfer, and regional competitiveness. Long-term fundamentals remain favorable despite cyclical volatility across regional industrial investment cycles.

Whisper Valve Market Competitive Landscape

The market exhibits a moderately consolidated structure, characterized by a small group of leading players alongside a broad base of smaller participants. The top five companies collectively account for approximately 40% of total market revenue, reflecting a balance between competitive intensity and scale-driven advantages. These leading firms primarily strengthen their positions through technological differentiation, continuous product innovation, and the ability to deliver consistent quality across large volumes. Investments in advanced processes, intellectual property, and application-specific solutions allow them to command premium pricing and maintain long-term customer relationships.

Despite this concentration at the top, the remaining market share is distributed across numerous regional and niche-focused players, resulting in persistent fragmentation. These companies typically operate with flexible production models and a deep understanding of local demand patterns, enabling them to compete effectively in specialized applications or geographies. Fragmentation also lowers entry barriers in certain segments, encouraging the emergence of mid-tier manufacturers.

Key Industry Developments

- In October 2025, Burkert Werke partnered with Siemens on IoT whisper valves, targeting pharma; pilots cut energy 12%, eyeing Europe expansion.

- In 2022, Bürkert Fluid Control Systems introduced its advanced micro flipper valve, the Type 6757 Whisper Valve, designed to deliver complete media separation within an ultra-compact 18 mm-wide form factor.

Companies Covered in Whisper Valve Market

- Emerson Electric

- Flowserve Corp

- Burkert Werke GmbH

- Schlumberger

- Baker Hughes

- Weir Group

- KSB SE

- Pentair

- Spirax Sarco

- Velan Inc.

- Crane Co.

- Metso Outotec

- Samson AG

- ARCA Valves

Frequently Asked Questions

The Whisper Valve market is estimated to be valued at US$ 128.8 Bn in 2026.

The key demand driver for the Whisper Valve market is the growing need for ultra-quiet, compact, and precise fluid control in sensitive applications.

In 2026, the North America region will dominate the market with an exceeding 40% revenue share in the global Whisper Valve market.

Among applications, industrial applications have the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other applications.

Emerson Electric, Flowserve Corp, Burkert Werke GmbH, Schlumberger, Baker Hughes, Weir Group, KSB SE, and Pentair. There are a few leading players in the Whisper Valve market.