- Industrial Goods & Service

- Welded Metal Bellows Market

Welded Metal Bellows Market Size, Share, and Growth Forecast, 2026 - 2033

Welded Metal Bellows Market by Product Type (Welded Bellows, Formed Bellows, Electroformed Bellow), Material Type (Stainless Steel Alloys, Nickel Alloys, Titanium Alloys, Others), Application (High Vacuum Seals, Leak-Free Motion Feedthroughs, Flexible Joints, Volume Compensators and Temperature Actuators), and Regional Analysis for 2026 - 2033

Welded Metal Bellows Market Size and Trends Analysis

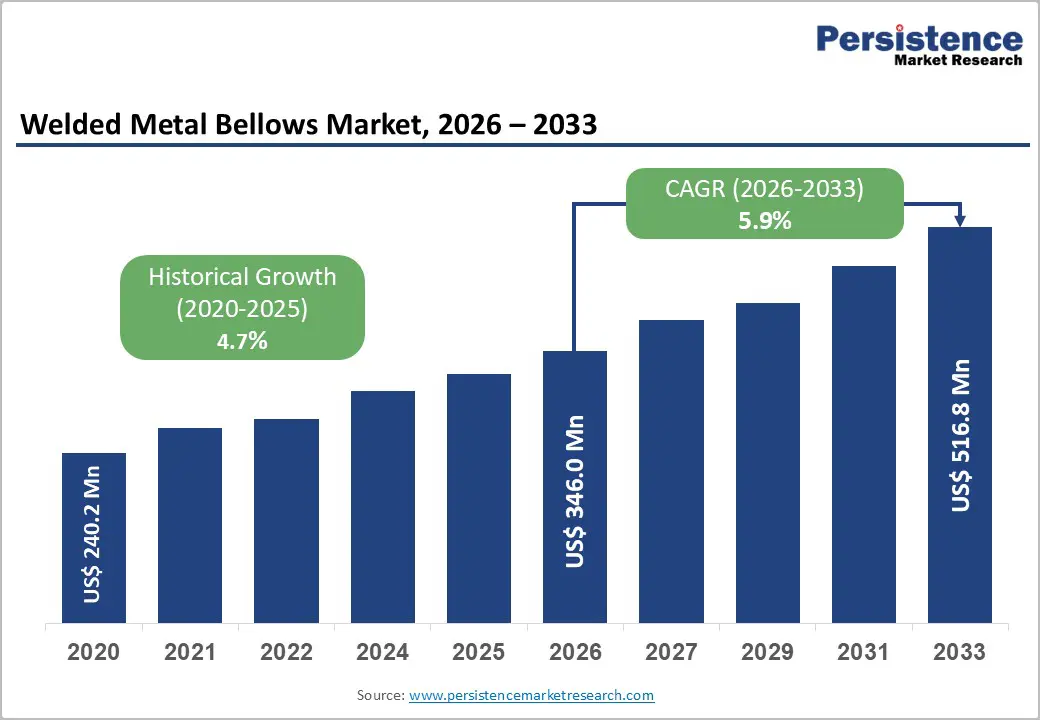

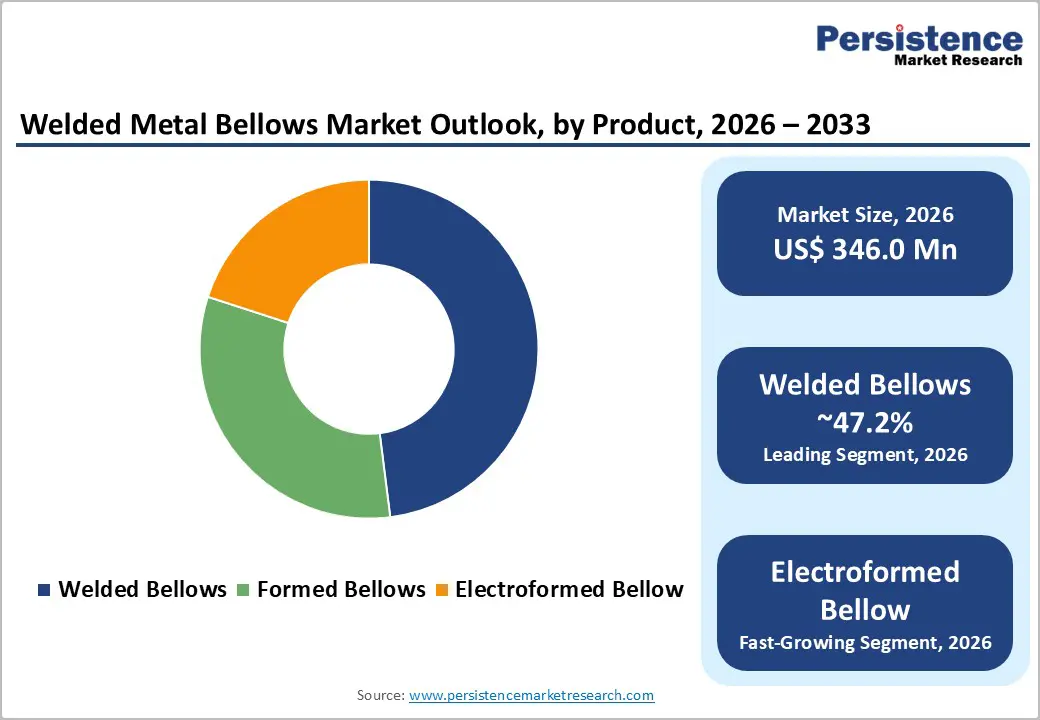

The global welded metal bellows market size is likely to be valued at US$ 346.0 million in 2026 and is projected to reach US$ 516.8 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033. This expansion reflects systematic advancements in aerospace and defense component requirements, the progressive complexity of semiconductor manufacturing processes that require precision vacuum-sealing solutions, and industrial equipment modernization, thereby driving a proportional demand for bellows.

Key Industry Highlights:

- Leading Product Type: Welded bellows dominate with 47.2% market share, driven by proven manufacturing maturity; Electroformed bellows are the fastest-growing at 8% CAGR, driven by miniaturization capabilities and precision manufacturing.

- Dominant Material Type: Stainless steel alloys command 62.3% of the market share due to their corrosion resistance and cost-effectiveness; Nickel alloys are the fastest-growing, with an 8-11% CAGR, driven by extreme-temperature aerospace applications.

- Leading Application: Flexible joints maintain 32.4% market share through their prevalence in industrial motion control; High-vacuum seals are the fastest-growing segment at a 7% CAGR, driven by semiconductor equipment and space exploration demand.

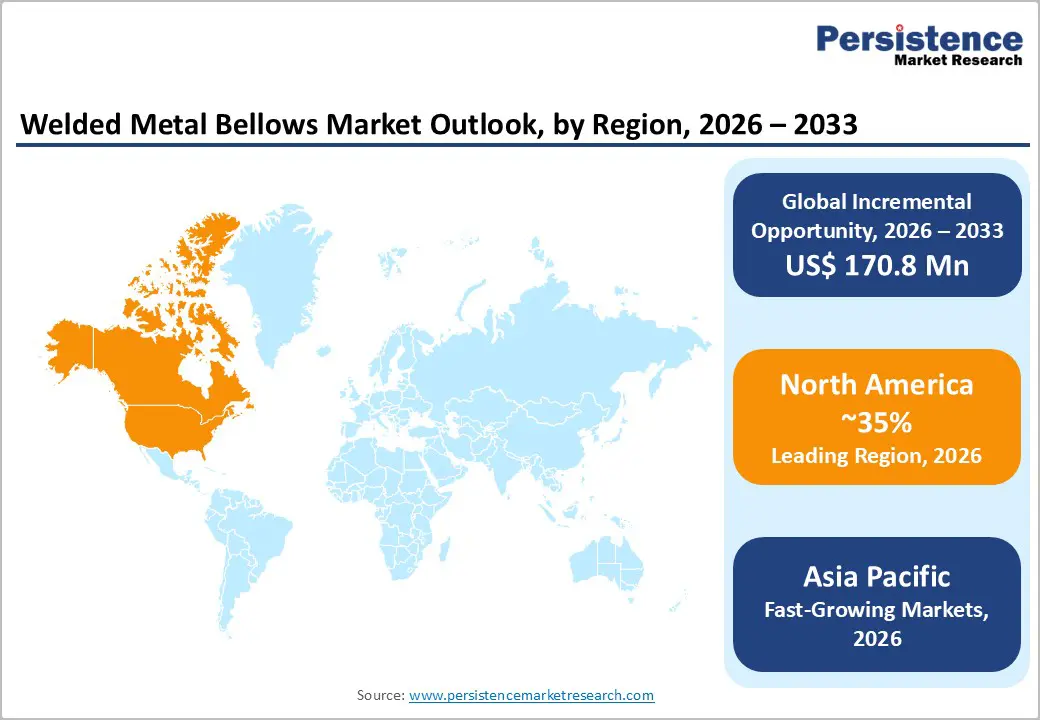

- Regional Market Dominance and Growth: North America maintains 35% global market share, driven by aerospace and semiconductor leadership; Asia Pacific demonstrates the fastest regional growth at an 8% CAGR, expanding from its current 25% share to 35% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 55% market share (Trelleborg, Senior Aerospace, Flexonics leading); Electroforming technology advancing to sub-millimeter precision; Nickel alloy capability extended to 1,200°C operation; Advanced welding techniques improving fatigue performance by 20%.

| Key Insights | Details |

|---|---|

|

Welded Metal Bellows Market Size (2026E) |

US$ 346.0 Mn |

|

Market Value Forecast (2033F) |

US$ 516.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.9% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.7% |

Market Dynamics

Drivers - Wave in Renewable Energy Projects

The rise in renewable energy projects is a significant trend, especially in solar and wind. As the world moves towards cleaner energy sources, there’s a growing demand for advanced and durable materials capable of withstanding high temperatures and extreme pressures.

Welded metal bellows are playing a crucial role in this transition, finding applications in solar thermal systems and wind turbines. Their robust design ensures reliability and efficiency in these demanding environments, contributing to the overall growth of the welded metal bellows market. For instance, there are currently over 400 onshore and offshore wind farms at various stages of planning, with around 163 already having received contracts and 81 recently gaining government approval. This shows the sustainability efforts and the importance of innovative materials in renewable energy technologies.

Increasing Industrialization Remains a Significant Market Driving Factor

The demand for the welded metal bellows market is on the rise as various industries expand, including power generation, automotive, semiconductors, and oil & gas, among others. Manufacturers worldwide are increasingly focused on improving their economic competitiveness while remaining environmentally conscious by using materials with a lower operational impact.

As end-user preferences evolve, manufacturers are focusing on production in regions such as Europe, North America, and the Asia Pacific, where demand is particularly high. For example, Technetics Group specializes in designing and manufacturing high-precision bellows that incorporate complex mechanical systems serving industries such as aerospace, semiconductors, oil & gas, and healthcare.

Bellows play a crucial role in sealing refrigerant compressors in the oil & gas industry, helping maintain diverse tensile strength in refrigerants and ultimately reducing the costs associated with compressor replacement.

Restraint - Lack of Substitutes and Fragile Industrial Environment

Manufacturers typically produce welded metal bellows based on customer needs. However, these small components can fail due to high temperatures at the weld joints, weakening the metal and shortening its lifespan. The lack of substitutes in the welded metal bellows market, given the custom nature of metal bellows, drives up raw material costs for spot manufacturing. This makes it challenging to find instant replacements for welded bellows when breakdowns occur in manufacturing plants.

The effectiveness of bells largely depends on their environment. Unfortunately, some industries, like food and beverage, often select metal bellows without fully understanding their design limitations. The convoluted shapes can trap contaminants, making them hard to clean during operation.

Complex Technologies and Strict Regulations

Designing and manufacturing for the welded metal bellows market requires meeting the unique standards and performance requirements of various industries, which can be quite complex. This process often requires specialized machinery and a skilled workforce, which makes production difficult. The necessity for precise engineering and adherence to strict industry regulations can lead to delays and complications, ultimately impacting market growth.

As companies strive to create high-quality bellows tailored for specific applications, the demand for technical expertise and advanced equipment becomes crucial. Addressing these challenges is essential to ensuring timely delivery and maintaining market competitiveness.

Opportunity - Compact Designs and Use in Medical Devices

As industries such as electronics and medical devices increasingly embrace smaller and more compact designs, the demand for miniaturized welded metal bellows is on the rise. These tiny components must deliver reliable performance even in confined spaces, which is pushing manufacturers to innovate and refine their designs.

The ability to create efficient, miniaturized bellows not only meets the specific needs of these industries but also enhances the overall functionality of the devices they use. These welded metal bellows market trends are fostering new advancements in materials and manufacturing techniques, ultimately driving growth and innovation within the market as companies strive to keep up with evolving requirements.

Use of Advanced Materials

The use of high-performance alloys and superalloys in the manufacturing of welded metal bellows is becoming increasingly popular. These advanced materials are specifically chosen for their exceptional durability and ability to withstand extreme conditions, such as high temperatures and corrosive environments. By incorporating these alloys into their designs, manufacturers can significantly enhance the performance and lifespan of bellows, making them suitable for a wider range of applications across industries such as aerospace, oil and gas, and medical devices. This shift not only improves reliability but also opens new welded metal bellows market opportunities for innovation and growth.

Category-wise Analysis

Material Type Insights

The welded metal bellows market is categorized into several segments, including stainless steel, high nickel alloys, and others such as copper bellows. Stainless steel led the market and is projected to account for 57.9% market revenue share in 2024. These bellows are widely recognized for their availability and ability to endure extremely low temperatures. Their remarkable flexibility and pressure resistance stem from superior tensile strength, allowing for maximum stroke while minimizing package size.

Key applications of stainless-steel welded bellows include electrical interrupters, power transmission systems, and industrial control mechanisms. Given these advantages, demand for stainless steel bellows is expected to rise, thereby driving market growth throughout the forecast period.

Product Type Insights

The welded bellows segment holds 47.2% market share, driven by manufacturing maturity and long-standing qualifications in the aerospace and semiconductor industries. Proven reliability, with over three decades of deployment in critical vacuum and aerospace systems, ensures predictable performance and fatigue life. Standardized welding processes enable consistent quality, scalable production, and cost efficiency. Welded bellows support an exceptionally wide operating range, from ultra-high vacuum (10?? Torr) to pressures exceeding 500 bar, making them suitable for diverse industrial environments. High customization flexibility, including variable convolutions and material selection, allows optimization for specific pressure, temperature, and motion requirements.

The electroformed segment is the fastest-growing, expanding at a 6.4% CAGR through 2033. Growth is driven by demand for miniaturization, ultra-tight tolerances, material efficiency, and the ability to handle complex geometry, particularly in medical devices and advanced semiconductor equipment.

Application Insights

Flexible joints hold 32.4% of the application market share, driven by widespread industrial motion control and standardized equipment demand. Industrial automation relies on flexible joints to accommodate misalignment, absorb vibration, and protect robotic and production equipment across large-scale factory installations. HVAC systems use flexible joints to isolate vibration, reduce noise transmission, and protect ducts and machinery. In industrial piping networks, flexible joints manage thermal expansion and dynamic stress, preventing leaks and structural fatigue. Pumps and compressors further depend on flexible joints to minimize vibration transfer and extend equipment life.

High-vacuum seals are the fastest-growing application, expanding at a % CAGR through 2033. Growth is driven by advanced semiconductor fabrication requiring ultra-high vacuum integrity, expanding space exploration programs, and rising demand from research, fusion energy, and particle accelerator applications. Critical performance requirements support premium pricing and long-term supplier partnerships.

Component Insights

Landing gear steering systems account for 41.3% of component market share, driven by high cost, system complexity, and growing technology content. Advanced steering assemblies account for 35% of total landing gear cost and integrate actuators, sensors, and control electronics. Enhanced control precision reduces ground handling incidents by 20%, justifying premium OEM specifications. Increasing adoption of electronically controlled steering enables automated taxiing and tighter integration with fly-by-wire systems, while retrofit programs for narrow-body fleets prioritize steering electrification. Steering systems dominate nose landing gear value, reinforcing revenue concentration and market leadership.

Actuation systems are the fastest-growing component segment (17% CAGR through 2033), driven by the shift from hydraulic to electro-mechanical systems. Electric actuation delivers 16% weight reduction, 25% lower maintenance costs, smart diagnostics for predictive maintenance, and standardization across next-generation aircraft platforms, accelerating adoption.

Regional Insights

North America Welded Metal Bellows Market Analysis

North America commands approximately 35% of the global welded metal bellows market share, valued at approximately US$ 110.7 million in 2026, with projections approaching US$ 165 million by 2033. The United States represents a dominant regional market contributor, accounting for 80% of the North American market value, driven by aerospace leadership and semiconductor manufacturing concentration.

Aerospace OEM concentration, with major aerospace manufacturers (Boeing, Lockheed Martin, Northrop Grumman, Collins Aerospace) and defense contractors maintaining North American manufacturing, establishing specification leadership and high-value below demand. Semiconductor manufacturing dominance, with leading-edge fab facilities (Intel, TSMC Arizona, Samsung) concentrating advanced manufacturing capacity requiring proportionate precision below component demand. Defense spending leadership, with US military modernization programs and space force development, is establishing sustained defense contractor demand for advanced aerospace below. Precision manufacturing ecosystem, with North American aerospace and semiconductor suppliers maintaining technology leadership and specialized manufacturing capabilities supporting innovation advancement.

Europe Welded Metal Bellows Market Share

Europe represents approximately 25% of the global welded metal bellows market share, valued at approximately US$ 103.8 million in 2026. Germany, the United Kingdom, France, and Switzerland collectively represent 75% of the European market value, reflecting aerospace manufacturing concentration and precision engineering specialization.

Aerospace manufacturing concentration, with Airbus and Airbus suppliers (Safran, Liebherr, Eaton) maintaining significant European facilities, establishing below specification leadership. Industrial equipment specialization, with German, Swiss, and Italian manufacturers leading precision equipment and vacuum system innovation requiring proportionate bellows component demand. Sustainability focus, with an emphasis on European environmental standards driving lightweight component development and advancing material efficiency in bellows design.

Asia Pacific Welded Metal Bellows Market Trends

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 40% by 2033. The region, valued at approximately US$ 114.5 million in 2026, is anticipated to reach US$ 180 million by 2033, making it the fastest-growing regional market with an estimated CAGR of 6.1%.

Semiconductor manufacturing expansion, with China, Taiwan, South Korea, and emerging facilities in India, has established a comprehensive semiconductor manufacturing capacity, driving huge demand. The industrial equipment modernization, followed by expansion in the chemical processing, power generation, and petroleum refining industries across the Asia Pacific, is creating a niche requirement for thermal sealing and motion control.

Competitive Landscape

The global welded metal bellows market demonstrates moderate consolidation with established precision component suppliers and specialized manufacturers maintaining competitive positions. The top 10 suppliers, including Trelleborg (Freudenberg), Senior Aerospace, Flexonics International, Technoflex, Witzenmann, Amtec Inc., Aeroflex Connectors, and specialized bellows manufacturers, collectively control approximately 55-70% of global market share, reflecting technology leadership, manufacturing specialization, and aerospace/semiconductor relationships.

Market structure reflects bifurcation between multinational industrial suppliers offering comprehensive component portfolios and specialized manufacturers focusing exclusively on bellows technology and manufacturing.

Key Industry Developments:

- In February 2024, EagleBurgmann launched the Flexibilis® Series of metal bellows, designed for high-temperature and high-pressure applications. These new bellows offer enhanced flexibility, longer lifespan, and improved resistance to harsh chemicals and extreme conditions. This development highlights the industry's focus on creating more durable and efficient solutions to meet evolving customer needs.

- In March 2024, Technetics Group announced new engineering solutions for edge-welded metal bellows, focusing on enhancing performance and reliability in critical applications. These bellows offer a wide range of materials, high spring rate, low magnetic permeability, and corrosion resistance, and can withstand vacuum pressure and cryogenic temperatures up to 1800°F. They also offer contract assembly services, a certified Class 100/1000 cleanroom environment, and ISO 9001 certification.

Companies Covered in Welded Metal Bellows Market

- ITT Enidine

- Flowserve

- Helical Products Company

- Flexicraft Industries

- Pyramid Industries, Inc.

- Universal Bellows

- AOT Precision Metals

- Caplugs

- Stellar Industries

- M Industries

- Others Key Players

Frequently Asked Questions

The Welded Metal Bellows market is estimated to be valued at US$ 346.0 Mn in 2026.

The key demand driver for the Welded Metal Bellows market is the increasing requirement for high-precision sealing and motion control in critical industrial and high-purity applications.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Welded Metal Bellows market.

Among the Product Type, Welded Bellows holds the highest preference, capturing beyond 47.2% of the market revenue share in 2026, surpassing other Product Type.

The key players in Welded Metal Bellows are ITT Enidine, Flowserve, Helical Products Company, Flexicraft Industries, and Pyramid Industries, Inc.