- Healthcare Services

- U.S. Assisted Reproductive Technology (ART) Market

U.S. Assisted Reproductive Technology (ART) Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

U.S. Assisted Reproductive Technology (ART) Market by Technique (In vitro Fertilization (IVF), Intracytoplasmic Sperm Injection (ICSI), Frozen Embryo Transfer (FET), Intrauterine Insemination (IUI)), By Procedure (Fresh Donor, Fresh non-Donor, Frozen Donor, Frozen non-Donor), End-user (Fertility Clinics, Hospitals, Research Centers), and Regional Analysis from 2026 to 2033

U.S. Assisted Reproductive Technology Market Share and Trends Analysis

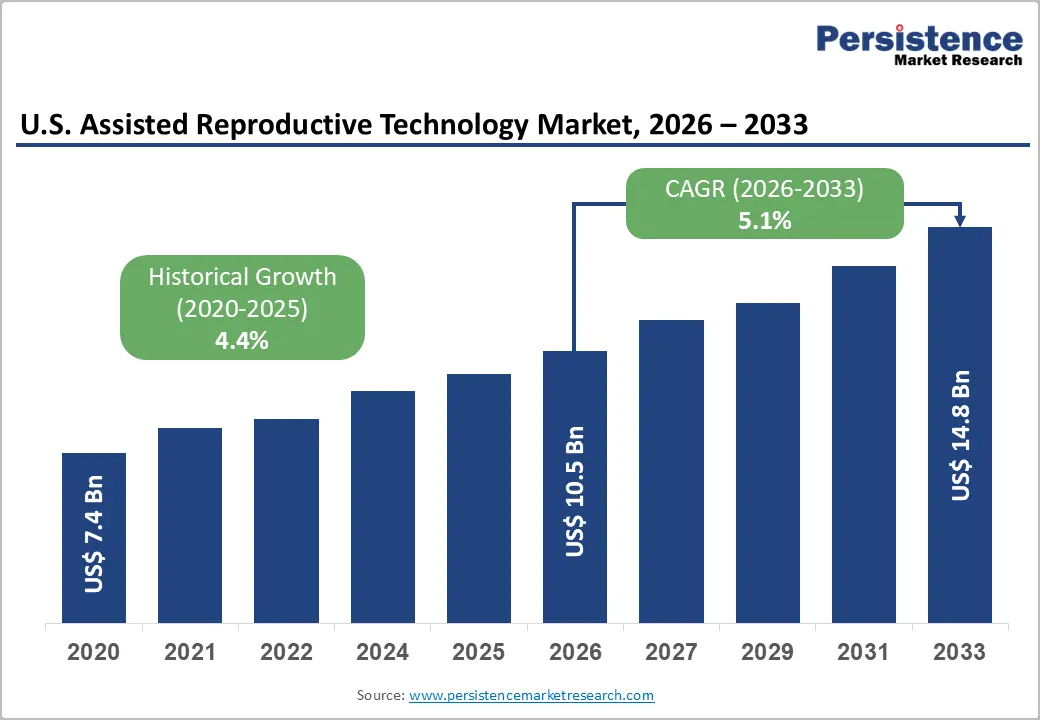

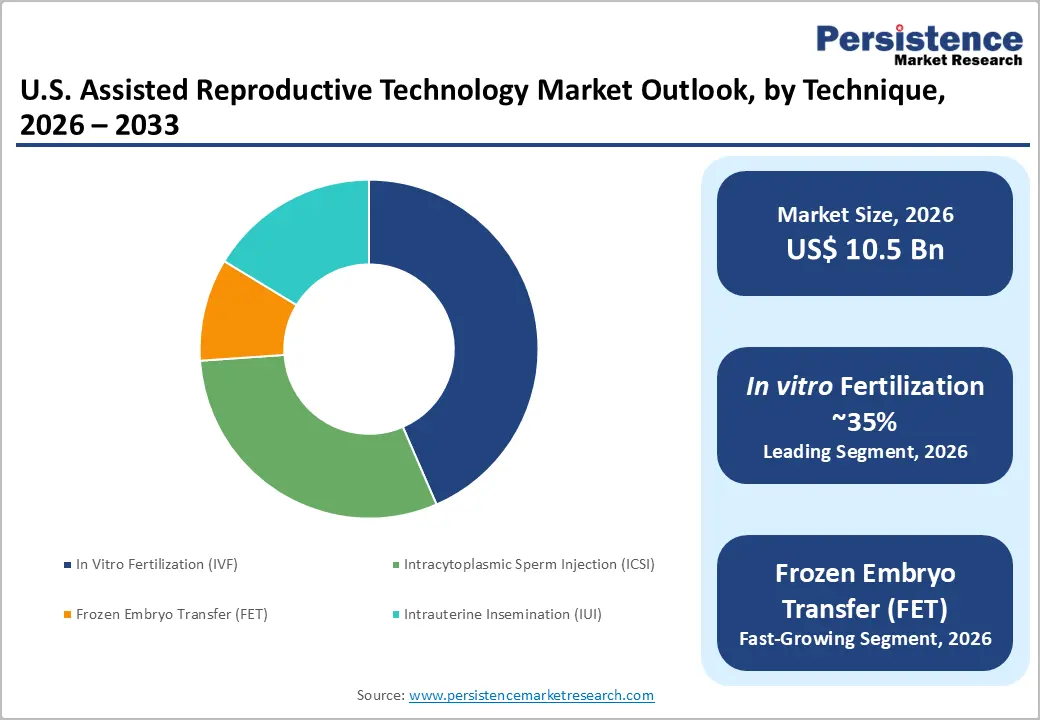

The U.S. assisted reproductive technology market is estimated to grow from US$10.5 billion in 2026 to US$14.8 billion by 2033. The market is projected to grow at a CAGR of 5.1% from 2026 to 2033.

Advanced procedures and innovations support individuals and couples in overcoming infertility drive the market growth. Key treatments include in vitro fertilisation (IVF), intracytoplasmic sperm injection (ICSI), cryopreservation, and genetic testing. Rising infertility rates, postponed parenthood, and growing awareness of fertility solutions are fueling demand for assisted reproductive technology in the U.S. Major industry players provide culture media, lab equipment, consumables, and full-service ART offerings, while fertility clinics and hospitals expand nationwide access and availability of these reproductive services.

Key Industry Highlights:

- Dominant Technique: In vitro fertilization (IVF) remains the most widely adopted ART procedure, followed by ICSI, cryopreservation, and GIFT/ZIFT procedures.

- Fastest-Growing Technique: Frozen Embryo Transfer (FET) is anticipated to be an emerging technique in the U.S. due to higher success rates, safer protocols, improved cryopreservation, patient preference, and expanded clinic adoption.

- Dominant Procedure: Frozen non-donor embryo transfers lead U.S. ART, driven by cryopreservation advances, safety, flexibility, genetic testing, convenience, and improved outcomes

- Leading End-user: Fertility centers remain the core hubs of ART innovation and patient care in the U.S. ART market, owing to specialized expertise, advanced technology, personalized care, and superior success rates, while expanding access nationwide. Hospitals and research institutes play supportive roles, but fertility centers.

- Recent innovations in assisted reproductive technology, including time-lapse embryo imaging, AI-driven embryo selection, advanced sperm sorting, and improved cryopreservation methods, have significantly enhanced success rates and patient outcomes in the U.S.

| Key Insights | Details |

|---|---|

| U.S.Assisted Reproductive Technology Market Size (2026E) | US$10.5 Bn |

| Market Value Forecast (2033F) | US$14.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver - Rising Infertility Rate alongside Growing Adoption of Elective Egg Freezing

The U.S. assistive reproductive technology market is expanding rapidly due to rising infertility rates and technological breakthroughs. With nearly 270,000 IVF cycles annually, and ICSI used in 60-70% of them, patients are increasingly confident in ART as a reliable pathway to parenthood. The U.S. assisted reproductive technology (ART) market is being reshaped by a combination of cultural, clinical, and technological forces, with elective procedures such as egg freezing standing out as a major catalyst. Increasing numbers of women are choosing to delay parenthood in favor of career advancement, financial stability, or personal priorities, and egg freezing provides a practical solution to preserve fertility potential. This trend reflects broader cultural acceptance of non-traditional family planning timelines and highlights how reproductive choices are evolving in modern society. Changes in demographics and health have thus created a steady pipeline of patients seeking medical interventions to conceive.

Restraints - Rising Demand Fuels Ethical Concerns Amid Donor Sperm Shortage

The U.S. assisted reproductive technology market faces constraints owing to ethical debates around embryo selection, genetic testing, and cryopreservation, which adds regulatory scrutiny, slowing the adoption of newer technologies. Demand for donor eggs and sperm has risen sharply due to delayed parenthood, higher infertility rates, and increased use of assisted reproductive technologies like IVF and ICSI. However, supply has not kept pace. Egg donation requires invasive medical procedures, discouraging many potential donors, while sperm donation faces declining participation among younger men due to privacy concerns and stricter screening regulations. Uneven access to the treatment is another hurdle, with advanced labs and AI-driven embryo selection concentrated in large urban fertility networks, leaving rural patients underserved. Additionally, the physical and emotional burden of repeated cycles discourages continuation; nearly 30% of patients discontinue after one failed attempt, thereby limiting overall market growth.

Opportunity - Oncofertility programs to offer cancer patients proactive fertility solutions

Oncofertility preservation programs in the U.S. are expanding to support cancer patients facing fertility risks from treatment. According to the American Society of Clinical Oncology (ASCO) each year, about 90,000 adolescents and young adults (ages 15-39) are diagnosed with cancer, yet only half are informed about fertility preservation options. Several leading medical centers offer oncofertility preservation programs that integrate reproductive technologies such as egg and embryo freezing, sperm banking, and ovarian tissue preservation to help cancer patients safeguard their fertility before treatment. These programs are expanding nationwide, supported by collaborations between oncology and reproductive specialists. Centers such as MD Anderson, UCSF, and UConn’s Center for Advanced Reproductive Services are leading examples, offering integrated care, advanced cryopreservation, and genetic testing to secure reproductive futures for oncology patients.

Recent initiatives highlight the importance of patient education, as studies show that less than 50% of young cancer patients are informed about fertility risks before treatment. Advocacy groups and oncology societies are pushing for standardized fertility counseling across all cancer centers. With survival rates improving, the demand for fertility preservation in the U.S. continues to grow, ensuring that cancer survivors retain the possibility of parenthood and long-term quality of life.

Category-wise Analysis

By Technique, In vitro Fertilization remains the foundational ART procedure, followed by ICSI

In the U.S., IVF leads the assisted reproductive technology (ART) market because it is the most widely adopted procedure, generating the highest revenue and offering broad applicability across infertility cases. Rising infertility rates, delayed parenthood, and technological advances make IVF the cornerstone of ART services nationwide. Availability of add-on services that enhance success rates and increase overall treatment value further boosts the demand for IVF. Add-on procedures such as preimplantation genetic testing (PGT) allow clinicians to screen embryos for chromosomal abnormalities, improving implantation outcomes and reducing miscarriage risks. Similarly, cryopreservation techniques enable patients to store embryos for future use.

Intracytoplasmic Sperm Injection (ICSI) follows the IVF procedures as it directly addresses male-factor infertility, which accounts for a significant portion of ART cases nationwide. By injecting a single healthy sperm into the egg, ICSI ensures higher fertilization rates even when sperm count, motility, or morphology is compromised. Beyond male infertility, clinics employ ICSI for couples with prior IVF failures, diminished ovarian reserve, advanced maternal age, or unexplained infertility, making it broadly applicable and widely adopted.

By End-user, Fertility Clinics are Leading

Fertility clinics in the U.S. hold the largest market share because they are highly specialized centers focused exclusively on reproductive care, unlike general hospitals, which balance multiple medical priorities. These clinics deliver comprehensive, end-to-end services ranging from diagnostics and IVF stimulation cycles to embryology labs, genetic testing, counseling, and cryopreservation, all within a single integrated setup, which drives higher patient volumes. Their infrastructure is tailored specifically to IVF workflows, enabling precise cycle monitoring, faster turnaround times, and more personalized clinical attention. U.S. fertility clinics also invest significantly in advanced embryology technologies, incubators, culture media, and digital tracking systems, which contribute to stronger perceived success rates.

Since most infertility treatments in the U.S. are elective, privately financed, and time-sensitive, patients tend to favor clinics that offer confidentiality, flexible scheduling, and transparent pricing models. Moreover, the rapid growth of private IVF networks across the country has further cemented the dominance of specialized fertility clinics in the American assisted reproductive technology market.

Regional Insights

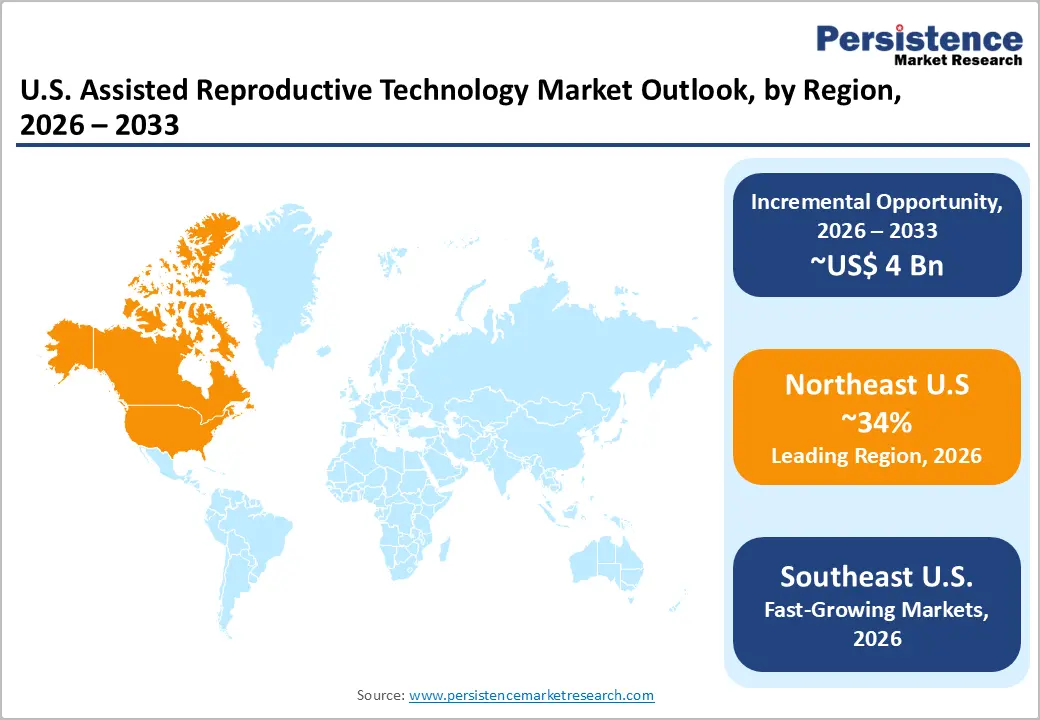

Northeast U.S. Assisted Reproductive Technology Market Trends

The Northeast leads the U.S. in assisted reproductive technologies because of its unique mix of strong insurance mandates, dense networks of fertility clinics, and world-class medical research institutions. The Northeast’s combination of policy support, medical infrastructure, and patient demand makes it the dominant region in shaping national trends in fertility care. In states such as Massachusetts and New York, access to infertility treatment is significantly greater than in many other parts of the U.S. Massachusetts is frequently regarded as the benchmark, thanks to its extensive insurance mandate that requires coverage for IVF and related procedures. This policy substantially lowers the financial barriers for patients, encouraging wider use of assisted reproductive technologies. Similarly, New York has expanded its insurance coverage, making treatments such as IVF, ICSI, FET, and IUI more accessible to a larger share of residents without incurring excessive costs.

Beyond insurance, the Northeast is home to prestigious academic medical centers such as Harvard-affiliated hospitals in Boston and major research hubs in New York City. These institutions not only provide state-of-the-art clinical care but also drive innovation in reproductive medicine, from advanced embryo-freezing techniques to genetic screening. The region’s high population density further supports many specialized fertility clinics, creating competition that fosters quality improvements and higher success rates.

Southeast U.S. Assisted Reproductive Technology Market Trends

The assisted reproductive technology (ART) sector in the Southeast U.S. is experiencing significant expansion, with in vitro fertilization (IVF) remaining the leading treatment option. Fertility centers in states such as Florida and Georgia are increasingly incorporating preimplantation genetic testing (PGT) to enhance pregnancy outcomes and lower the likelihood of miscarriages. Elective egg freezing is increasingly prevalent across the Southeastern U.S., reflecting shifting cultural values and career-focused lifestyles. Women in cities like Atlanta and Miami are choosing fertility preservation to balance professional ambitions with family planning. This trend underscores broader acceptance of delayed parenthood and growing demand for advanced reproductive options.

Male infertility solutions, particularly intracytoplasmic sperm injection (ICSI), are becoming increasingly common in fertility clinics across North Carolina and Tennessee. This technique, which involves injecting a single sperm directly into an egg, is helping couples overcome severe male-factor infertility and achieve higher success rates. The growing demand reflects both improved awareness and the availability of advanced reproductive technologies in the region.

Patients from other U.S. regions, including the Northeast and West Coast, travel to Florida clinics due to lower treatment costs, bundled service packages, and shorter wait times. Florida’s reputation for providing high-quality care at lower costs has positioned it as a destination for couples seeking accessible ART options. This trend is further supported by the presence of internationally recognised fertility centres in cities such as Miami and Jacksonville, which attract patients not only from across the U.S. but also from Latin America and the Caribbean.

Competitive Landscape

Success in the U.S. assistive reproductive technology market depends on balancing innovation with patient-centered care, expanding reach through networks and collaborations, and maintaining competitive pricing models that make advanced reproductive solutions more accessible to a wider population. The competition is also shaped by geographic expansion and the creation of extensive clinic networks that improve accessibility for patients across diverse regions.

Many providers emphasize integrated, patient-centric services, combining medical expertise with counseling, wellness programs, and digital platforms to create a holistic treatment experience. Pricing strategies and customized treatment packages are increasingly used to attract patients, offering flexibility and affordability in what is often a high-cost medical journey. Partnerships with hospitals, universities, and research institutions further differentiate providers, enabling them to leverage cutting-edge science and broaden their referral base.

Key Industry Developments:

- In October 2025, Overture Life announced the opening of its Dallas facility. The site offers non-invasive, CLIA-licensed embryo-assessment testing that analyzes molecules in the fluid surrounding embryos (metabolomics) with machine-learning support, providing fertility teams with objective data to inform embryo selection without a biopsy.

- In September 2025, Conceivable Life Sciences secured $50 million in Series A funding led by Advance Venture Partners to accelerate development of its AI-powered automated IVF laboratory platform with advanced robotic precision. Existing investors ARTIS Ventures, Stride, and ACME participated in the round, bringing total funding to $70 million.

- In August 2025, a US-based reproductive health biotech firm secured US$44 million in Series C funding led by Overwater Ventures, raising its total investment to US$127 million.

- In April 2025, IVI RMA North America partnered with TMRW Life Sciences to digitize the management and storage of IVF Specimens across all clinics. TMRW will safely store the eggs and embryos of tens of thousands of IVI RMA North America patients, both onsite across its 22+ IVF labs and offsite at TMRW’s state-of-the-art biorepositories.

Companies Covered in U.S. Assisted Reproductive Technology (ART) Market

- The Fertility Institutes

- Shady Grove Fertility

- Pacific Fertility Centre

- Boston IVF

- Cleveland Clinic Fertility Centre

- Reproductive Medicine Associates of New Jersey (RMANJ)

- Columbia University Fertility Centre

- Mayo Clinic Fertility Centre

- Texas Fertility Centre

- UCSF Centre for Reproductive Health

- Bloom IVF Centre

- California Cryobank

- Others

Frequently Asked Questions

The U.S. assisted reproductive technology market is projected to be valued at US$10.5 Bn in 2026.

Increasing infertility among couples due to delayed parenthood, lifestyle changes, stress, pollution, and medical conditions fuels demand for ART treatments.

The U.S. assisted reproductive technology market is poised to witness a CAGR of 5.1% between 2026 and 2033.

Adoption of AI-assisted embryo selection, lab automation, and digital monitoring can improve success rates and operational efficiency.

Northeast region of the U.S. is the leading zone in the U.S. Assisted Reproductive Technology Market.