- Automotive Components & Materials

- Tensioner Pulley Market

Tensioner Pulley Market Size, Share, and Growth Forecast, 2026 – 2033

Tensioner Pulley Market by Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), Application (Engine Timing System, Alternator System, Power Steering System, Air Conditioning System, Water Pump System), and Regional Analysis for 2026 – 2033

Tensioner Pulley Market Size and Trends Analysis

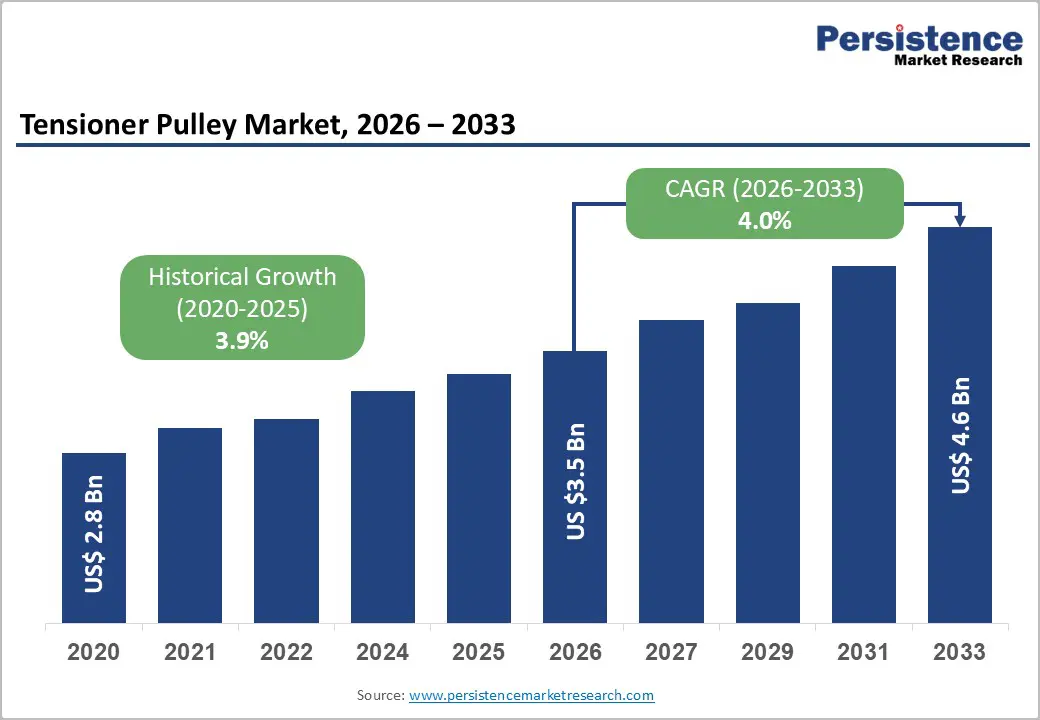

The global tensioner pulley market size is likely to be valued at US$3.5 billion in 2026 and is expected to reach US$4.6 billion by 2033, growing at a CAGR of 4.0% during the forecast period from 2026 to 2033, driven by stable vehicle production, a growing installed vehicle base driving aftermarket replacements, and incremental efficiency improvements in belt-drive systems for internal combustion engine (ICE) vehicles.

Key growth drivers include strong demand for durable accessory drive systems, longer vehicle lifespans, and stricter fuel-efficiency and emissions regulations promoting optimized belt tensioning. While electrification is a long-term shift, the market continues to grow steadily, aligning more with conventional powertrains and hybrids than facing abrupt demand changes.

Key Industry Highlights:

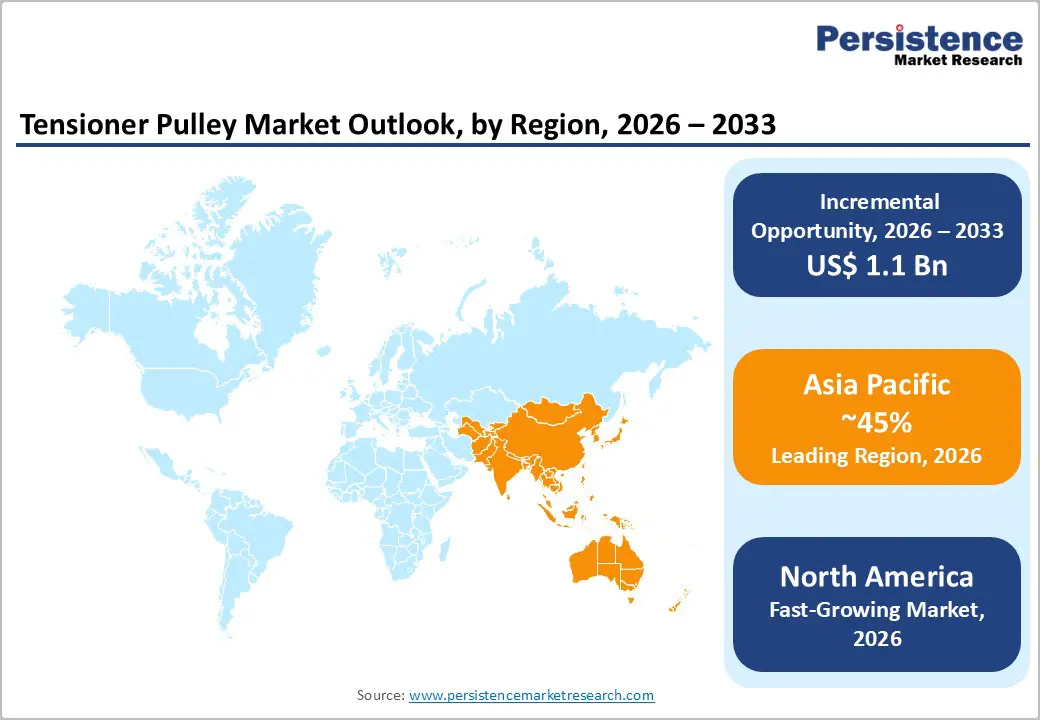

- Leading Region: Asia Pacific is expected to be the leading region, accounting for 45% in 2026, driven by high vehicle production, commercial fleet growth, and cost-efficient manufacturing.

- Fastest-growing Region: North America is expected to be the fastest-growing region for tensioner pulleys in 2026, driven by high vehicle ownership, strong OEM production, and robust aftermarket demand.

- Leading Vehicle Type: Passenger vehicles are projected to account for 60% of revenue in 2026, driven by high production volumes, an expanding vehicle parc, and sustained demand for reliable accessory drive systems in conventional and hybrid automobiles.

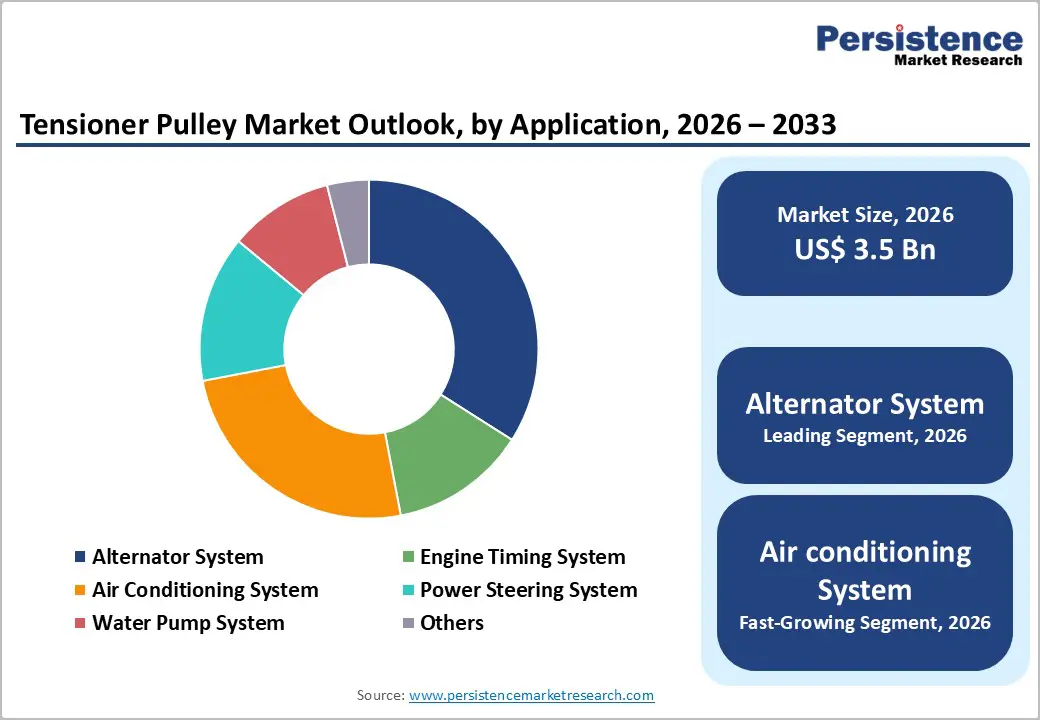

- Leading Application: The alternator system is expected to be the leading application, accounting for over 35% of revenue in 2026, driven by sustained demand for charging efficiency in ICE and hybrid vehicles.

| Key Insights | Details |

|---|---|

| Tensioner Pulley Market Size (2026E) | US$3.5 Bn |

| Market Value Forecast (2033F) | US$4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Vehicle Production

Every internal combustion and hybrid vehicle requires multiple belt-driven systems for reliable operation. Rising production of passenger and commercial vehicles directly increases OEM demand for tensioner pulleys used in engine timing, alternator, air conditioning, power steering, and water pump systems. Emerging economies in Asia Pacific continue to scale automotive manufacturing due to urbanization, income growth, and infrastructure development. Even as electrification progresses, the continued dominance of ICE and hybrid vehicles in output sustains consistent demand for high-quality tensioning components.

Higher vehicle production expands the vehicle parc, which strengthens long-term aftermarket demand for tensioner pulleys. As vehicles age, belt drive components require periodic replacement to maintain efficiency and prevent system failures. Manufacturers are also focusing on improved durability, noise reduction, and lightweight materials to meet stricter fuel-efficiency and emission regulations. This combination of rising production volumes and longer vehicle lifecycles creates a stable replacement cycle. Increasing vehicle production supports both short-term sales growth and long-term market stability for tensioner pulley suppliers.

Rise in High-Performance Vehicles

These vehicles demand advanced, durable, and precision-engineered belt drive components. High-performance passenger cars, premium SUVs, and performance-oriented commercial vehicles operate at higher engine speeds, deliver higher torque, and experience greater thermal loads, which place additional stress on accessory drive systems. To ensure stable belt tension, reduced vibration, and consistent power transmission, manufacturers increasingly adopt high-quality automatic tensioner pulleys. Growth in premium vehicle sales across North America, Europe, and parts of the Asia Pacific is therefore directly supporting demand for technologically advanced tensioner pulleys.

High-performance and premium vehicles emphasize noise, vibration, and harshness (NVH) reduction, reliability, and efficiency, driving innovation in tensioner pulley design and materials. Manufacturers are incorporating lightweight alloys, advanced polymers, and improved bearing technologies to enhance durability and minimize friction losses. These vehicles often integrate multiple accessory systems, increasing the number of tensioner pulleys per vehicle. Performance-oriented hybrid vehicles retain complex belt systems, supporting market growth. Consumer preference is shifting toward powerful yet fuel-efficient vehicles, and demand for high-performance tensioner pulleys continues to grow.

Barrier Analysis - Rising Adoption of Battery Electric Vehicles (BEVs)

BEVs do not rely on traditional internal combustion engines or belt-driven accessory systems. Core applications such as engine timing, alternators, and conventional power steering are being replaced with electric systems, directly reducing OEM demand for tensioner pulleys. Increasing government incentives, stricter emission regulations, and automaker commitments to electrification across major markets such as Europe, China, and North America are accelerating BEV penetration. This structural shift limits long-term volume growth for conventional tensioner pulley manufacturers.

The growing share of BEVs is gradually reshaping the aftermarket dynamics of the tensioner pulley market. As BEVs enter the vehicle parc, replacement cycles for belt-driven components decline, reducing recurring aftermarket revenue over time. While mild hybrids and plug-in hybrids continue to support partial demand, the growing preference for fully electric drivetrains creates uncertainty for suppliers heavily dependent on ICE platforms. Manufacturers face pressure to diversify product portfolios or invest in alternative drivetrain components to offset demand erosion. As BEV adoption accelerates, this restraint increasingly shapes long-term market strategies.

Durability and Heat Tolerance Limitations

Modern engines operate at higher temperatures and under increased load conditions. Downsized turbocharged engines, start-stop systems, and high-performance applications subject belt drive components to greater thermal stress, vibration, and continuous operation. Inadequate heat resistance can accelerate wear of bearings, springs, and polymer pulleys, leading to premature failure. This raises reliability concerns for OEMs and end users, increases warranty costs and replacement costs, and constrains broader adoption of cost-effective tensioner pulley designs in demanding automotive applications.

Durability challenges limit material flexibility and design optimization within the tensioner pulley market. While lightweight polymers and composite materials help reduce friction and improve fuel efficiency, they may underperform in extreme thermal environments compared to metal alternatives. Manufacturers must balance cost, weight reduction, and long-term performance, often resulting in increased development and validation costs. In the aftermarket, inferior-quality components can damage brand trust and reduce repeat demand. These durability and heat-tolerance constraints slow innovation cycles and create barriers to new entrants, reinforcing the dominance of established suppliers with proven high-performance solutions.

Opportunity Analysis - Expansion in Emerging Markets and Commercial Vehicle Segments

Countries across Asia Pacific, Latin America, the Middle East, and Africa are witnessing increased demand for affordable passenger vehicles and light commercial vehicles. Growing middle-class populations and improving road networks are supporting higher vehicle ownership, directly boosting OEM demand for belt-driven accessory systems. In these regions, internal combustion and hybrid vehicles continue to dominate new-vehicle sales, ensuring sustained demand for tensioner pulleys across engine timing, alternator, and air-conditioning applications.

The growth of commercial vehicle segments strengthens market opportunities, driven by higher utilization rates and frequent maintenance cycles. Trucks, buses, and delivery vehicles operate under heavy loads and extended driving hours, accelerating belt system wear and increasing replacement demand. Expanding logistics, e-commerce, and construction activities in emerging economies are driving fleet expansion, supporting both OEM and aftermarket sales. Regulatory focus on fuel efficiency and emissions in commercial fleets encourages the adoption of advanced, durable tensioner pulleys.

Technological Convergence in Hybrid and Mild-Hybrid Systems

These powertrains retain belt-driven architectures while integrating electric assistance. Mild-hybrid and full-hybrid vehicles commonly use belt-integrated starter generators (BISG) and advanced alternator systems, which place higher dynamic loads on belts and pulleys. This increases the need for high-performance automatic tensioner pulleys capable of handling frequent start-stop cycles, torque fluctuations, and regenerative braking loads. As automakers expand hybrid portfolios to meet emission regulations, demand for advanced tensioning solutions continues to rise steadily.

Hybrid systems require improved noise, vibration, and harshness (NVH) control and higher efficiency to optimize fuel savings, driving innovation in tensioner pulley materials and designs. Lightweight alloys, enhanced bearing technologies, and optimized spring mechanisms are increasingly adopted to ensure durability and precision under variable operating conditions. Unlike battery-electric vehicles, hybrids retain long-term relevance for belt-driven components, making them a transitional growth platform. Adoption of mild-hybrid vehicles accelerates; this technological convergence supports sustained OEM and aftermarket opportunities for tensioner pulley manufacturers.

Category-wise Analysis

Vehicle Type Insights

Passenger vehicles are expected to lead the tensioner pulley market, accounting for approximately 60% of revenue in 2026, driven by their high production volumes and expansive vehicle parc worldwide. These vehicles rely heavily on belt-driven systems such as alternators, air conditioning compressors, power steering pumps, and water pumps, all of which require precise and reliable tensioning for efficient operation. For example, mid-size sedans and compact SUVs typically integrate multiple accessory drive systems, creating consistent demand for high-quality tensioner pulleys throughout the vehicle lifecycle.

Electric vehicles are likely to represent the fastest-growing segment in 2026, supported by the rapid adoption of mild-hybrid and hybrid electric vehicles that retain belt-driven architectures. Unlike pure battery-electric vehicles, mild-hybrid systems commonly use belt-integrated starter generators, which impose higher dynamic loads on belts and pulleys and increase the need for robust tensioning solutions. For example, 48V mild-hybrid passenger cars, which rely on enhanced alternator and accessory drive systems, ensure continued relevance and growth opportunities for tensioner pulley manufacturers despite the broader electrification trend.

Application Insights

The alternator system is projected to lead the market, capturing approximately 35% of revenue in 2026, supported by its critical role in maintaining the electrical power supply in internal combustion and hybrid vehicles. Alternators operate continuously under varying load conditions, making precise belt tension essential for charging efficiency, system reliability, and reduced wear. As modern vehicles integrate more electronic features, including advanced infotainment, safety systems, and onboard sensors, the demand for stable alternator performance increases. For example, hybrid passenger vehicles that use alternator-based systems to support regenerative charging and auxiliary power require high-performance tensioner pulleys to ensure consistent belt alignment and a long service life across diverse driving conditions.

The air conditioning system is likely to be the fastest-growing application in 2026, driven by rising consumer expectations for comfort and increasing regulatory focus on energy efficiency. As climate control systems become standard across vehicle categories, particularly in emerging markets, demand for reliable belt-driven air-conditioning compressors continues to grow. Modern designs emphasize reduced energy consumption and improved thermal management, placing greater importance on optimized tensioner pulleys that minimize friction and vibration. For example, compact passenger cars sold in Asia Pacific markets, where air conditioning systems are standard equipment, support sustained growth in tensioner pulley demand linked to fuel-efficient and comfort-oriented vehicle designs.

Regional Insights

North America Tensioner Pulley Market Trends

North America is likely to be the fastest-growing region in the tensioner pulley in 2026, driven by a strong automotive manufacturing base, mature vehicle parc, and robust aftermarket ecosystem. The region holds a significant share of tensioner pulley revenue, supported by high vehicle ownership, extensive annual mileage, and a well-established maintenance culture that drives replacement demand. For example, Gates Corporation has introduced next-generation polymer tensioner pulleys optimized for hybrid vehicles to enhance durability and reduce weight, reflecting OEM focus on performance improvements and regulatory compliance.

Another key trend in North America is the shift toward lighter, more efficient tensioner pulley designs and increased adoption of hybrid powertrain components, driven by consumer preferences for fuel economy and technological sophistication. Aftermarket trends show a growing emphasis on components that combine durability with low noise and vibration, as vehicle owners increasingly seek long-lasting, high-performance replacements. For example, Litens Automotive Group expanded its aftermarket SKUs in North America, adding hybrid-specific tensioner pulleys for popular models such as the Ford F-Series and Audi A-series, demonstrating supplier responsiveness to evolving powertrain requirements.

Europe Tensioner Pulley Market Trends

Europe is likely to be a significant market for tensioner pulleys in 2026, due to stringent environmental regulations and a strong focus on fuel efficiency, shaping demand and innovation. The region accounts for a significant share of the market, supported by well-established automotive manufacturing clusters in Germany, France, the U.K., and Italy, where OEMs demand high-precision belt drive systems that enhance emissions performance and reduce noise, vibration, and harshness (NVH). European standards such as Euro 7 are driving the integration of advanced automatic tensioner pulleys designed for lightweight, low-friction operation in both ICE and hybrid vehicles, supporting ongoing component upgrades and engineering excellence.

A notable trend in Europe is supplier innovation and diversification, as companies adapt to evolving powertrain architectures and performance requirements. For example, Continental AG has been expanding its automotive components portfolio in Europe with engineered tensioner pulley solutions that support hybrid systems and improved accessory drive efficiency, reflecting automaker preferences for components that balance durability with emissions compliance. European markets are also experiencing pressure from electrification, which, while reducing demand for some traditional belt systems, accelerates the need for specialized pulleys in hybrid applications.

Asia Pacific Tensioner Pulley Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the tensioner pulley market in 2026, driven by high vehicle production volumes and growing aftermarket demand across China and India. As the largest regional contributor to market revenue, Asia Pacific benefits from strong automotive manufacturing hubs, cost-effective supply chains, and increasing passenger and commercial vehicle production. OEMs in the region are integrating advanced tensioner pulley systems into ICE and hybrid powertrains to meet rising fuel efficiency and emissions requirements.

A notable trend in the region is localized manufacturing and supplier expansion to meet regional demand and shorten lead times. For example, NSK Ltd. has been enhancing its production capabilities in Asia Pacific, particularly in China and India, to supply automotive belt tensioner pulleys tailored for local OEM requirements and aftermarket needs. This strategic localization helps reduce logistics costs and improve responsiveness to diverse vehicle specifications in regional markets. A shift toward lightweight materials and low-noise pulley designs is gaining traction, driven by OEMs' focus on improving fuel efficiency and cabin comfort.

Competitive Landscape

The global tensioner pulley market exhibits a moderately fragmented structure, driven by the presence of numerous regional manufacturers that compete across OEM and aftermarket channels. Competition is shaped by ongoing innovation in materials, precision engineering, durability enhancement, and partnerships with major vehicle manufacturers. Key suppliers are focusing on low-friction bearings, lightweight composite pulleys, and advanced designs that meet stringent fuel-efficiency and emissions norms.

With key leaders including Continental AG, Dayco Products LLC, SKF Group, Schaeffler Group, NTN Corporation, Litens Automotive Group, BorgWarner Inc., and NSK Ltd., the competitive landscape balances scale with specialization. These players compete through extensive R&D investments, expanded manufacturing footprints, and deep OEM relationships that secure long-term contracts across passenger, commercial, and hybrid vehicle segments. Strategic expansion into high-growth regions, aftermarket network strengthening, and adaptive product portfolios intensify rivalry within the market.

Key Industry Developments:

- In January 2025, Industrias Dolz launched the SKD250A Auxiliary Drive Kit for hybrid vehicles. The kit, designed for the DW10 HY Hybrid engine and BSG system, included a Poly-V belt, auxiliary drive belt tensioner, and deflection pulleys, ensuring professional assembly and reliable operation of key accessories under varying engine loads.

- In May 2024, BorgWarner launched its electric Torque Vectoring and Disconnect (eTVD) system for battery electric vehicles (BEVs), starting with the Polestar 3 SUV. The eTVD system, part of BorgWarner’s electric Torque Management System (eTMS) portfolio, combines torque vectoring, differential replacement, and on-demand axle disconnect, enhancing stability, performance, and traction while reducing brake and tire wear.

Companies Covered in Tensioner Pulley Market

- BorgWarner

- Continental

- Dayco Products

- Gates

- Litens Automotive Group

- NSK Automation

- NTN

- Schaeffler Group

- SKF Group

- Tsubakimoto Chain

Frequently Asked Questions

The global tensioner pulley market is projected to reach US$3.5 billion in 2026.

The tensioner pulley market is driven by rising vehicle production, increasing vehicle parc, and growing demand for efficient and durable belt-driven accessory systems in ICE and hybrid vehicles.

The tensioner pulley market is expected to grow at a CAGR of 4.0% from 2026 to 2033.

Key market opportunities lie in the growth of hybrid and mild-hybrid vehicles, expanding commercial vehicle segments, and rising demand in emerging markets.

BorgWarner, Continental, Dayco Products, Gates, and Litens Automotive Group are the leading players.