- Pharmaceuticals

- Sublingual Drugs Market

Sublingual Drugs Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Sublingual Drugs Market by Drug Form (Tablets, Films, Drops, Sprays), Drug Class (Antianginals, Antihypertensives, Analgesics, Bronchodilators), Indication (GI ulcers, Digestive diseases), and Regional Analysis for 2026 - 2033

Sublingual Drugs Market Share and Trends Analysis

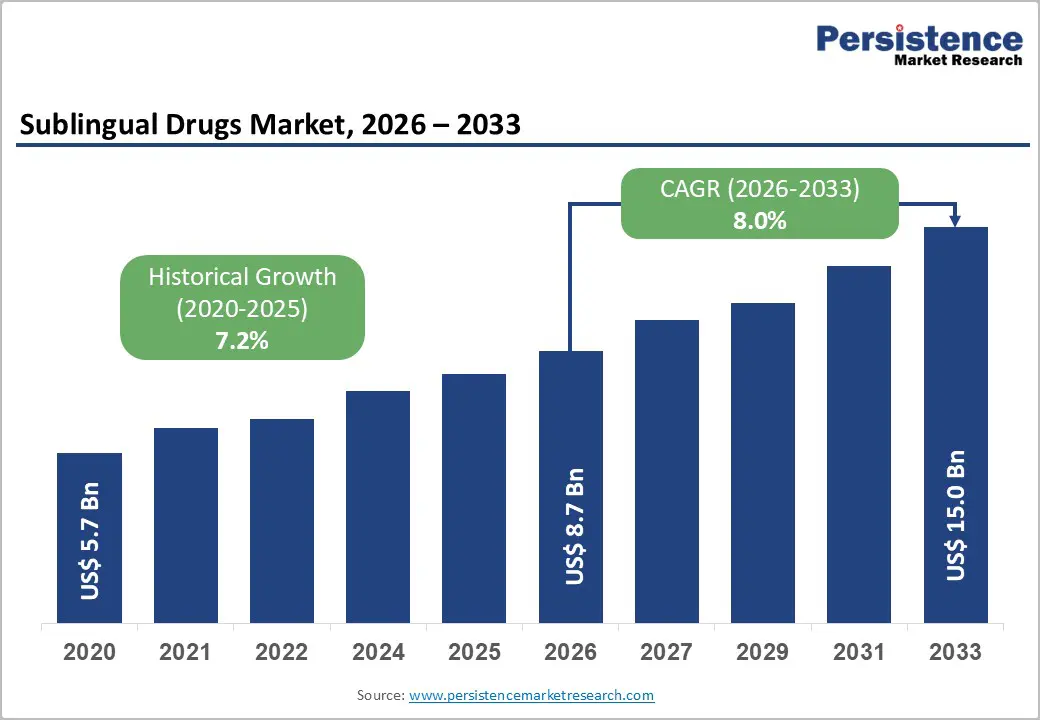

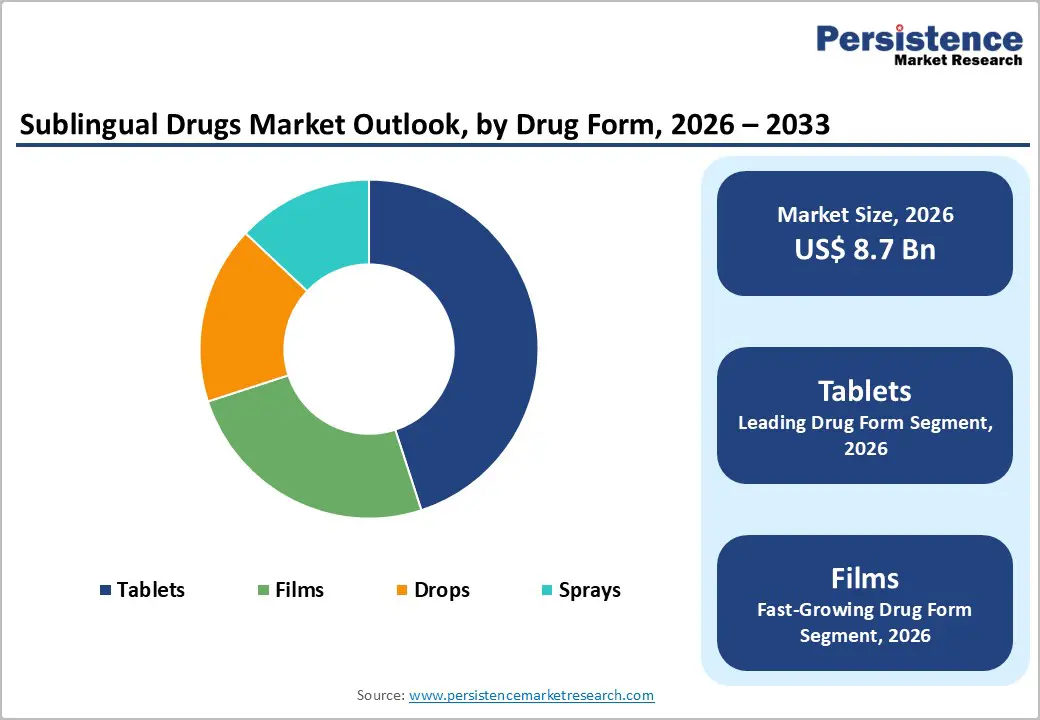

The global sublingual drugs market size is likely to be valued at US$ 8.7 billion in 2026 and is projected to reach US$15.0 billion by 2033, growing at a CAGR of 8.0% during the forecast period 2026 - 2033.

The sublingual drug delivery route, in which pharmaceuticals are absorbed directly through the mucosa beneath the tongue into the systemic circulation, offers a compelling pharmacokinetic advantage: faster onset of action, avoidance of hepatic first-pass metabolism, and superior bioavailability compared with conventional oral formulations. These attributes are fueling adoption across cardiovascular, pain management, central nervous system (CNS), and hormonal therapy indications. The market is further bolstered by ongoing R&D into film- and spray-based sublingual technologies, which improve patient adherence and expand the application scope.

Key Industry Highlights

- Dominant Region: North America is expected to command about a 44% market share in 2026, supported by extensive pharmaceutical infrastructure, high healthcare investment, and a supportive regulatory framework.

- Fastest-growing Region: The Asia Pacific market is the fastest-growing during the forecast period, due to the regional growth through rapid hospital expansion.

- Leading & Fastest-growing Drug Form: Tablets currently dominate the segment, commanding approximately 45% of total market revenue; films are likely to be the fastest-growing segment during the 2026 - 2033 forecast period.

- Leading & Fastest-growing Drug Class: Antianginals represent the dominant segment, capturing approximately 35% of market revenue share in 2026. Analgesics are expected to be the fastest-growing segment over the 2026 - 2033 forecast period.

- In February 2026, BioNxt Solutions received a milestone Decision to Grant from the European Patent Office for European Patent No. 4539857, covering its proprietary sublingual cladribine oral thin film (ODF) drug-delivery technology for the treatment of multiple sclerosis.

| Key Insights | Details |

|---|---|

| Sublingual Drugs Market Size (2026E) | US$8.7 Bn |

| Market Value Forecast (2033F) | US$15.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Cardiovascular Diseases and Chronic Pain

Sublingual nitroglycerin and other nitrate formulations are continuing to dominate the treatment landscape for acute angina attacks. These therapies provide rapid relief by dilating blood vessels and improving oxygen delivery to the heart, reinforcing their role as a standard-of-care option. According to the World Health Organization (WHO), an estimated 19.8 million people died from CVDs in 2022, representing approximately 32% of all global deaths. Of these deaths, 85% were due to heart attack and stroke. Healthcare providers are increasingly relying on these medications for immediate symptom management, ensuring steady prescription volumes and a consistent market demand.

Pharmaceutical companies are also focusing on refining these formulations to enhance patient convenience and adherence, such as developing fast-dissolving tablets and more precise dosing options. This focus is strengthening the position of sublingual nitrates in cardiovascular treatment protocols and creating predictable growth for manufacturers. Sublingual opioid analgesics, including buprenorphine and fentanyl, are increasingly supporting patients with chronic pain conditions by offering rapid onset relief and better dosing control. Medical practitioners in palliative care and oncology are adopting these therapies to manage complex pain profiles effectively. As populations are aging and the prevalence of cardiovascular disease and chronic pain rises, demand for both sublingual nitrates and opioid analgesics is expanding.

Pharmacokinetic Advantages and Enhanced Bioavailability

Sublingual drug delivery provides significant advantages over traditional oral administration by bypassing gastrointestinal degradation and first-pass hepatic metabolism. These mechanisms allow medications to achieve substantially higher bioavailability, thereby increasing therapeutic efficiency for select drug classes. Patients are experiencing faster symptom relief because sublingual administration produces measurable effects within minutes, compared with the longer onset times of oral tablets. Emergency departments and acute-care settings are increasingly integrating sublingual formulations into treatment protocols because rapid action can be critical for patient outcomes.

Investment in sublingual platforms is continuing to grow as healthcare providers recognize the advantages of rapid-onset therapies. Researchers and formulators are designing solutions that maintain stability while allowing precise dosing and predictable absorption. The growing interest is shaping a pipeline of innovative treatments addressing both acute and chronic medical needs. Drug companies are also exploring sublingual delivery for pain management and other time-sensitive conditions, ensuring that patients receive relief when it is most needed. Combining faster therapeutic action with improved bioavailability, these platforms are enhancing clinical outcomes and strengthening prescribers' confidence.

Manufacturing Complexity and Higher Production Costs

Sublingual drug manufacturing requires advanced production capabilities to ensure consistent quality and performance. Facilities are implementing specialized equipment and strict environmental controls, including precise humidity and temperature management, to preserve drug stability and maintain the integrity of sublingual films. Expertise in excipients is becoming essential as formulators design solutions that dissolve quickly while maintaining uniform dosing. Manufacturers are also optimizing processes to minimize variability and improve shelf life, which is reinforcing the reliability of sublingual products for both acute and chronic care applications. These operational requirements are shaping a highly technical production environment that is distinct from conventional tablet manufacturing.

Higher production complexity is contributing to rising per-unit costs, influencing pricing strategies across global markets. Pharmaceutical companies are carefully evaluating cost structures and supply chain efficiencies to balance affordability and profitability. In emerging markets, elevated pricing may limit patient access and create challenges during payer negotiations. Developers are investing in process innovations and scale-up efficiencies to reduce costs over time, which is expected to make sublingual therapies more competitive. These efforts are establishing a framework for sustainable market growth while supporting broader adoption in diverse healthcare settings.

Competition from Alternative Novel Drug Delivery Systems

Encountering increasing competition from alternative delivery platforms, including transdermal patches, intranasal sprays, injectable biologics, and pulmonary inhalers. These options offer comparable or even superior bioavailability for certain drug classes, encouraging healthcare providers to explore multiple routes of administration. Patients seeking convenience and sustained therapeutic effect are increasingly adopting wearable devices and long-acting injectable therapies. Pharmaceutical companies are responding by reallocating research and development (R&D) resources toward these innovative platforms, which is influencing prescribing patterns and slowing the expansion of sublingual formulations in some therapeutic areas.

The rise of transdermal and other non-oral technologies is creating strategic pressure on sublingual drug developers. Companies are investing in product differentiation, such as improving dissolution speed, taste masking, and patient adherence, to maintain market relevance. Future sublingual therapies are expected to focus on niche indications and acute-use scenarios where rapid onset provides a clear advantage. Emphasizing unique clinical benefits and patient-centric features, sublingual platforms are reinforcing their role within a diverse treatment ecosystem while navigating competitive challenges from rapidly evolving delivery technologies.

Expansion in Opioid Use Disorder (OUD) Treatment

Sublingual buprenorphine formulations, such as Suboxone, Subutex, and their generic equivalents, are experiencing rapidly growing demand due to the ongoing opioid crisis. Healthcare providers are increasingly adopting these therapies to treat opioid use disorder (OUD) because they offer controlled dosing, improved patient compliance, and reduced risk of misuse compared with other opioid treatments. This change enables more patients to begin treatment quickly, reduces barriers to care and increases overall treatment penetration across urban and rural populations. Pharmaceutical companies are responding by scaling production and supporting telehealth integration to reach a broader patient base.

Opioid dependency is also driving interest in sublingual buprenorphine outside the United States. Markets in Europe and the Asia Pacific are showing growing adoption as healthcare systems prioritize early intervention and long-term treatment strategies. Developers are focusing on improving formulation convenience and adherence while supporting healthcare providers with educational programs and monitoring tools. Combining regulatory flexibility with patient-centric design, sublingual buprenorphine is reinforcing its role as a cornerstone therapy for OUD and is creating a sustainable growth trajectory across multiple regions.

Technological Innovation in Film and Spray Formulations

Advances in oral thin-film (OTF) technology are transforming the possibilities for sublingual drug delivery. Complex biologics, peptides, and controlled-release drug candidates are now being formulated in sublingual formats that were previously considered impractical. These innovations are improving drug stability, enhancing patient convenience, and enabling rapid onset of action. Companies adopting these technologies are positioning themselves to meet evolving clinical needs while offering differentiated products that stand out in competitive markets.

The growth of sublingual films is attracting significant investment from leading contract development and manufacturing organizations (CDMOs) and specialized drug delivery companies. Developers are expanding their capabilities to support scalable production, quality consistency, and novel formulation designs. Healthcare providers increasingly recognize the benefits of fast-acting, patient-friendly therapies, and sublingual oral thin films are gaining traction across multiple therapeutic areas. Continued innovation in platform technologies is expected to drive strong commercial adoption, broaden treatment applications, and reinforce sublingual films as a strategic growth segment within the oral thin-film drug delivery market.

Category-wise Analysis

Drug Form Insights

Tablets are currently dominating commanding 45% of total revenue, due to widespread prescriber familiarity, well-established manufacturing processes, and strong clinical evidence supporting efficacy. They are preferred for acute treatments such as angina and rapid-onset pain relief because of their consistent dosing and ease of distribution. Healthcare providers and patients trust tablets for reliability, storage stability, and cost-effectiveness. Large-scale production capabilities and existing regulatory approvals reinforce their dominant market share. Tablets continue to anchor sublingual therapy portfolios while providing a stable revenue base that supports ongoing innovation in alternative delivery formats.

Films are likely to be the fastest-growing segment during the 2026 - 2033 forecast period, because of their convenience, rapid onset of action, and adaptability for complex molecules such as peptides and biologics. Oral thin-film (OTF) technology enables precise dosing, improved patient adherence, and customization through advanced methods such as nanotechnology and 3D printing. Films are increasingly preferred for acute- and chronic-care applications where rapid absorption is critical. Pharmaceutical companies are heavily investing in film formulations, making them a high-growth area with significant potential to capture market share from traditional tablets while supporting personalized and innovative therapy approaches.

Drug Class Insights

Antianginals are the dominant segment, capturing approximately 35% of the market in 2026. Sublingual nitroglycerin provides rapid relief by dilating blood vessels and improving cardiac oxygenation, making it indispensable in emergency and outpatient settings. Physicians and patients rely on their predictable onset, consistent dosing, and established safety profile. The well-developed manufacturing processes and extensive clinical validation further reinforce their market dominance. Antianginals are sustaining strong prescription volumes and forming a stable foundation for the market, supporting both healthcare outcomes and commercial continuity.

Analgesics are expected to be the fastest-growing segment in the forecast period, driven by increasing demand for rapid-onset pain management in chronic and palliative care. Medications such as buprenorphine and fentanyl offer precise dosing, quick absorption, and enhanced patient adherence. Aging populations and rising prevalence of chronic pain conditions are expanding the patient pool, while telemedicine regulations are increasing accessibility for opioid-based therapies. Pharmaceutical companies are investing in innovative formulations and sublingual delivery technologies to differentiate products.

Regional Insights

North America Sublingual Drugs Market Trends

North America is set to command a significant portion of the sublingual drugs market share at approximately 44% in 2026, reinforced by the United States’ extensive pharmaceutical infrastructure, high healthcare investment, and supportive regulatory framework. The U.S. Food and Drug Administration (FDA) is actively reviewing and approving sublingual drug applications, while the country’s opioid use disorder (OUD) treatment programs are expanding rapidly. Telehealth-enabled prescribing of buprenorphine is increasing patient access, and the aging population with elevated cardiovascular disease risk is creating steady demand for rapid-onset therapies. Canada is contributing to regional growth through its universal healthcare system, which includes sublingual generics in national formularies, and Health Canada’s approval process is supporting market expansion.

The competitive landscape in North America reflects a mix of large integrated pharmaceutical companies, such as AbbVie and Pfizer, alongside specialized drug-delivery innovators, such as BioDelivery Sciences and Assertio. Increasing penetration of generics is creating pricing pressure on branded originator products, encouraging lifecycle management strategies and formulation innovation. Pharmaceutical companies are investing in research and development (R&D) to enhance delivery platforms, improve patient adherence, and develop differentiated therapies. These combined factors are sustaining North America’s market leadership while supporting future growth opportunities in sublingual drug adoption and innovation.

Europe Sublingual Drugs Market Trends

Europe is the second-largest regional market for sublingual drugs, driven by strong healthcare infrastructure and regulatory support. Germany is leading regional growth with its statutory health insurance system (GKV), high density of healthcare providers, and established pharmaceutical manufacturing capabilities. The United Kingdom is sustaining adoption through National Health Service (NHS) formulary inclusion and adherence to National Institute for Health and Care Excellence (NICE) guidelines for cardiovascular and pain therapies. France and Spain are experiencing growing demand as aging populations and expanding reimbursement frameworks for opioid use disorder (OUD) treatments are increasing patient access.

The European Medicines Agency’s (EMA) regulatory harmonization is streamlining multi-country approvals, enabling faster market entry for sublingual products across the continent. European generics manufacturers, particularly in Germany, Poland, and Spain, are becoming increasingly competitive with Asian producers through cost-efficient production. Pharmaceutical companies and biotech firms are investing in biosimilar sublingual formulations and central nervous system (CNS) pipelines, while several are advancing sublingual peptide therapeutics through clinical trials. These developments are enhancing product differentiation, supporting faster adoption, and reinforcing Europe’s position as a high-potential sublingual drug market. Continued investment in innovation and regulatory alignment is expected to drive sustainable growth in multiple therapeutic areas.

Asia Pacific Sublingual Drugs Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing sublingual drugs market. China is leading regional growth through rapid hospital expansion, a large patient population, and initiatives under the Healthy China 2030 plan that are promoting pharmaceutical innovation. Japan remains a high-value market, with strong prescribing of sublingual cardiovascular therapies and a technologically advanced domestic pharmaceutical sector. India is becoming a key manufacturing hub, with cost-advantaged generics producers meeting both domestic and international demand, while ASEAN countries such as Indonesia, Thailand, and the Philippines are increasing pharmaceutical spending and incorporating sublingual opioid use disorder (OUD) treatments into regulatory frameworks.

The manufacturing advantages in China and India, including significantly lower labor costs compared with U.S. and European facilities, are positioning the region as a global center for sublingual generic production. Pharmaceutical companies are investing in process optimization, regulatory compliance, and formulation innovation to capture regional growth opportunities. Expansion of local R&D capabilities is enabling the development of differentiated sublingual therapies, particularly for acute cardiovascular events and chronic pain management. These trends are reinforcing Asia Pacific’s strategic importance in the global sublingual drug market while supporting cost-effective production, broader patient access, and faster time-to-market for emerging therapies.

Competitive Landscape

The global sublingual drugs market structure is moderately consolidated, dominated by leading players such as AbbVie, Pfizer, Indivior, BioDelivery Sciences International, and Mylan. These players collectively capture 35-42% of the market share. The regional generics manufacturers, specialty pharmaceutical companies, and emerging biotechnology firms. Branded innovation segments are exhibiting moderate market concentration, with a few key players driving product development and clinical adoption. The global generics tier is highly fragmented, with numerous manufacturers competing on cost and efficiency. Indian and Chinese producers are exerting significant pricing influence, leveraging lower production costs and scale advantages to maintain competitive positioning. This dynamic is shaping the market structure, balancing innovation-led growth with price-driven competition across different sublingual therapy categories.

Key Industry Developments:

- In March 2026, BioNxt Solutions announced its entry into the commercialization phase for its sublingual drug delivery platform, bolstered by newly granted global patents, including European Patent No. 4539857 (covering 39 states) and Eurasian Patent No. 051510. The patents protect BNT23001, a fast-dissolving oral film of cladribine targeting multiple sclerosis and myasthenia gravis, alongside a U.S. Track One fast-track filing expected to yield protection within 9-12 months.

- In January 2026, Bial launched KYNMOBI (apomorphine hydrochloride), the UK's first sublingual film therapy, for adults with Parkinson’s disease experiencing intermittent "OFF" episodes not controlled by oral medications. Administered by placing the film under the tongue until it dissolves, it bypasses first-pass metabolism for rapid symptom relief and motor function restoration.

- In August 2025, the FDA approved Tonmya (cyclobenzaprine HCl sublingual tablets), a non-opioid analgesic, as the first new fibromyalgia treatment in over 15 years. This once-daily, bedtime-dosed formulation from Tonix Pharmaceuticals rapidly absorbs under the tongue to reduce chronic widespread pain, outperforming placebo in two phase 3 trials involving nearly 1,000 patients.

Companies Covered in Sublingual Drugs Market

- AbbVie Inc.

- Pfizer Inc.

- Indivior plc

- Viatris Inc.

- Johnson & Johnson

- Teva Pharmaceutical Industries

- BioDelivery Sciences International

- Assertio Holdings

- Hikma Pharmaceuticals

- Sun Pharmaceutical Industries

- Dr. Reddy's Laboratories

- Alvogen

- Solco Healthcare

- Glenmark Pharmaceuticals

Frequently Asked Questions

The sublingual drugs market is projected to reach US$8.7 Bn in 2026.

The market is driven by the rising prevalence of chronic and neurological disorders, plus patient preference for rapid-onset, non-invasive delivery.

The sublingual drugs market is poised to witness a CAGR of 8.0% from 2026 to 2033.

Major opportunities lie in advancements in nanotechnology formulation science and expansion into personalized medicine & home healthcare.

AbbVie, Pfizer, Indivior, BioDelivery Sciences International, and Mylan. are among the key players.