- Specialty & Fine Chemicals

- Specialty Surfactants Market

Specialty Surfactants Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Specialty Surfactants Market by Source (Synthetic, Bio-based), Product Type (Anionic, Cationic, Nonionic, Amphoteric, Silicone, Others), Function (Emulsifiers, Wetting Agents, Dispersants, Foaming Agents, Defoamers, Detergents, Conditioning Agents, Other), Application (Household Soap and Detergent, Personal Care, Lubricants and Fuel Additives, Other), and Regional Analysis for 2026 - 2033

Specialty Surfactants Market Size and Trend Analysis

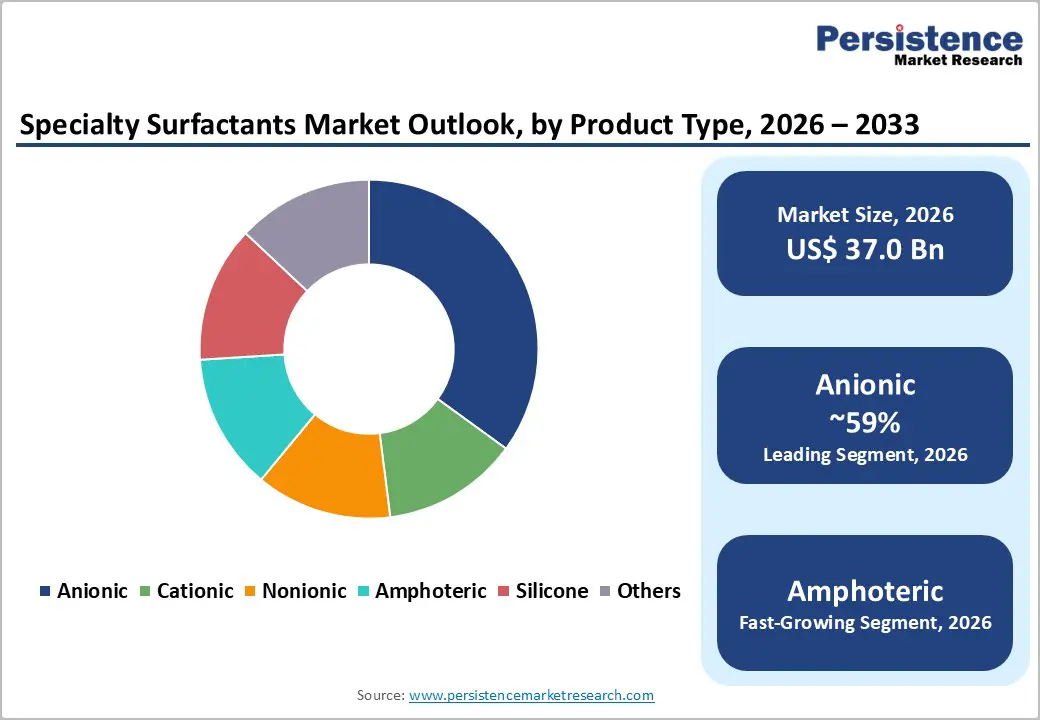

The global specialty surfactants market is valued at US$ 37.0 billion in 2026 and is projected to reach US$ 49.7 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The market is driven by a confluence of structural demand shifts across personal care, household cleaning, and industrial applications, supported by accelerating sustainability mandates globally. Rising consumer preference for mild, biodegradable, and performance-driven formulations is compelling manufacturers to innovate across both synthetic and bio-based specialty surfactant portfolios. The growing penetration of personal care products in emerging economies, combined with regulatory tailwinds incentivizing green chemistry in developed markets, forms a robust dual-engine growth platform.

Key Market Highlights

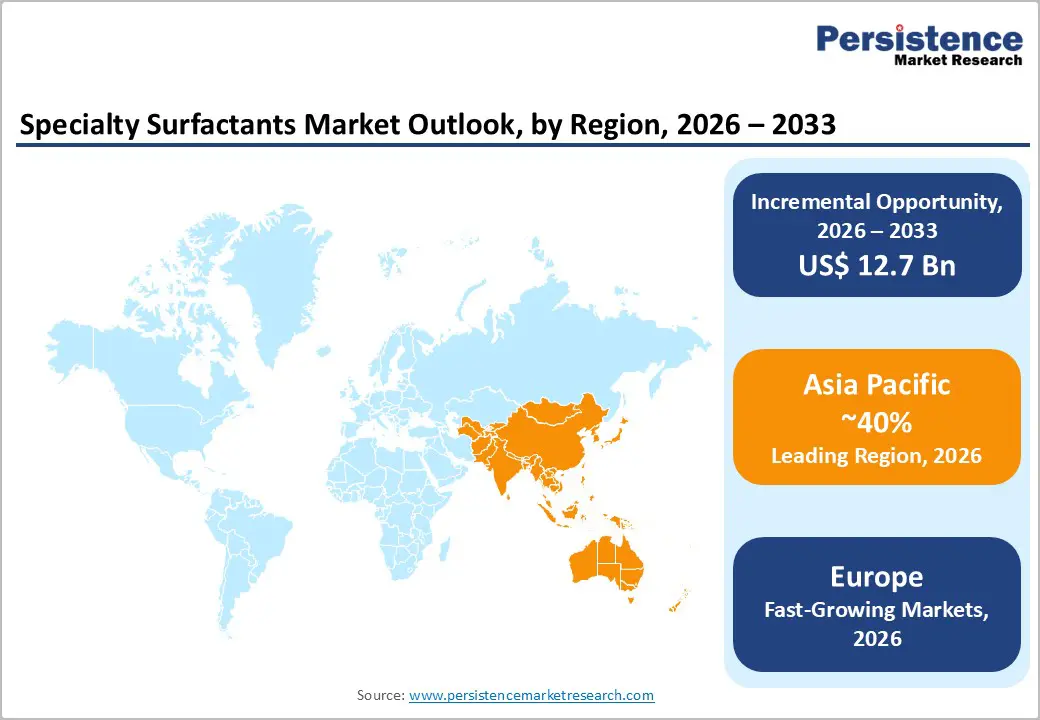

- Leading Region: Asia Pacific dominates the global specialty surfactants market, holding approximately 40% share, driven by China’s large household and personal care industries, India’s rapidly growing chemicals sector, and a cost-advantaged oleochemical feedstock base.

- Fastest Growing Region: Europe is the fastest growing region, shaped by stringent environmental regulations, a strong sustainability orientation, and a well-established specialty chemicals and biotechnology manufacturing base.

- Dominant Segment: Anionic Surfactants command approximately 35% of the global specialty surfactants market, underpinned by the dominance of LAS and AES in household detergents, with global LAS volumes exceeding 4 million tons annually.

- Fastest Growing Segment: Bio-based specialty surfactants are growing at a CAGR of approximately 5.8%, driven by sustainability commitments from global FMCG brands, regulatory mandates, and breakthrough commercial-scale biosurfactant production by players like Evonik.

- Key Market Opportunity: Food processing represents the fastest-growing application vertical, with specialty surfactant emulsifiers and wetting agents increasingly critical to processed food quality, plant-based protein formulations, and biopharmaceutical fermentation processes.

| Key Insights | Details |

|---|---|

| Specialty Surfactants Market Size (2026E) | US$ 37.0 Bn |

| Market Value Forecast (2033F) | US$ 49.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.3% |

| Historical Market Growth (2020-2025) | 3.6% |

Market Dynamics

Driver- Surging Demand in Personal Care and Household Cleaning Products

The personal care and household cleaning sectors represent the primary sources of demand for specialty surfactants on a global scale. The personal care industry, including hair care, skin care, oral care, and body wash products, depends extensively on mild and multifunctional surfactants to deliver effective emulsification, foaming, and conditioning performance. As reported by the Confederation of Indian Industry (CII), India’s beauty and personal care market is projected to surpass USD 20 billion by 2025, highlighting strong growth momentum in a major emerging economy.

Concurrently, the global household detergent and cleaning products industry continues to require high-performance anionic and nonionic surfactants as essential functional ingredients. Moreover, the accelerating shift toward premium, concentrated, and sulfate-free formulations, particularly among millennial and Gen Z consumers, is prompting formulators to adopt advanced specialty surfactant solutions that achieve both performance efficiency and enhanced safety standards.

Expanding Industrial and Institutional Cleaning Along with Oilfield Applications

Rapid industrialization across Asia Pacific, the Middle East, and Latin America is significantly increasing demand for specialty surfactants in industrial and institutional (I&I) cleaning applications. These applications require surfactants capable of delivering consistent and superior performance under demanding conditions such as elevated temperatures, hard water environments, and complex soil loads, thereby favoring advanced specialty grades over conventional commodity substitutes.

In parallel, the oilfield chemicals sector constitutes a critical demand catalyst. According to the International Energy Agency, steady growth in global oil demand is encouraging upstream operators to enhance operational efficiency and optimize enhanced oil recovery (EOR) processes, in which specialty surfactants play a vital role by improving crude recovery rates and minimizing operational downtime. The expanding scale and complexity of oilfield activities, particularly in the Middle East and North America, are consequently generating sustained incremental demand for high-performance specialty surfactant formulations.

Restraints - Volatility in Raw Material Prices and Supply Chain Disruptions

Specialty surfactants are predominantly derived from either petrochemical feedstocks or bio-based oleochemicals such as palm oil, coconut oil, and fatty alcohols. Fluctuations in crude oil prices and edible oil markets directly impact production costs. For instance, the Food and Agriculture Organization (FAO) reported significant volatility in vegetable oil price indices in recent years, with palm oil prices experiencing swings of over 40% in a single year during the 2021 - 2022 period. Such volatility compresses profit margins for surfactant manufacturers and forces end-users to seek cost optimization strategies, which can constrain premium specialty surfactant adoption and slow market momentum, particularly among price-sensitive buyers in developing regions.

Stringent Environmental Regulations and Compliance Costs

While sustainability mandates are also a growth driver, they simultaneously pose a significant restraint for legacy manufacturers. Compliance with the European Union's REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation imposes substantial administrative and financial burdens, particularly on smaller producers. Surfactants that do not meet REACH biodegradability standards face phase-out timelines, compelling companies to invest heavily in reformulation.

The U.S. Environmental Protection Agency (EPA) also continuously updates its Safer Choice criteria, restricting certain anionic and ethoxylated surfactant chemistries. These regulatory dynamics increase R&D expenditures and time-to-market cycles, acting as a meaningful constraint on profitability and innovation speed for mid-sized and smaller market participants.

Opportunities - Bio-based and Biosurfactant Innovation as a High-Growth Frontier

The shift toward bio-based specialty surfactants constitutes a significant strategic opportunity within the global specialty surfactants market over the 2026-2033 forecast horizon. Major consumer goods companies and FMCG manufacturers are increasingly formalizing commitments to reduce reliance on fossil-derived raw materials, thereby accelerating structural demand for sustainable surfactant alternatives. Unilever’s USD 1 billion program aimed at eliminating fossil-based surfactants from its cleaning product portfolio by 2030 exemplifies this transition and is expected to create sustained, long-term demand for bio-based suppliers.

Furthermore, the commissioning of Evonik Industries AG’s first industrial-scale rhamnolipid biosurfactant facility in Slovakia in early 2024 represents a pivotal milestone in the commercial scalability of next-generation biosurfactants. As a result, producers capable of scaling fermentation-based technologies while achieving cost competitiveness are well positioned to capture value across personal care, home care, and institutional cleaning applications, where regulatory and consumer emphasis on biodegradability and clean-label formulations continues to intensify.

Food Processing and Agricultural Chemicals as Emerging Demand Verticals

The food processing and agricultural chemicals sectors offer significant untapped growth potential for specialty surfactant manufacturers. In food processing, surfactants functioning as emulsifiers and wetting agents are critical for product texture, stability, and shelf life in applications ranging from bakery goods to dairy analogs and plant-based proteins. Global processed food consumption continues to surge, particularly in the Asia Pacific.

In agricultural chemicals, specialty surfactants serve as adjuvants that enhance the efficacy of herbicides, insecticides, and fungicides by improving spray coverage, absorption, and rainfastness. BASF SE demonstrated this opportunity through the 2023 launch of Agnique HP 450, a biodegradable, plant-based agricultural adjuvant that increased crop protection effectiveness by 8% and harvest production by 14% in field tests, illustrating the compelling performance and commercial case for specialty surfactants in this vertical.

Category-wise Analysis

Source Insights

Synthetic surfactants continue to dominate the global specialty surfactants market, accounting for approximately 75% of total demand. This leadership is underpinned by mature and well-integrated petrochemical supply chains, superior cost efficiency at scale, consistent performance reliability, and broad compatibility across a wide range of end-use applications. Synthetic surfactants, including linear alkylbenzene sulfonates (LAS), alcohol ether sulfates (AES), and nonylphenol ethoxylates, remain indispensable in high-volume household detergent and industrial cleaning formulations where price-to-performance optimization is critical.

Major producers such as BASF SE and Dow Inc. leverage vertically integrated petrochemical value chains to supply competitively priced synthetic grades. Nevertheless, the bio-based segment represents the fastest-growing category, projected to expand at a CAGR of 5.8% over the forecast period, driven by tightening environmental regulations, corporate sustainability commitments, and growing consumer preference for naturally derived and biodegradable ingredients in personal and home care products.

Product Type Insights

Anionic surfactants constitute the leading product category within the global specialty surfactants market, accounting for an estimated 35% of total market share. Their dominance is primarily attributable to superior cleaning efficiency, strong foaming capability, and effective emulsification performance, which make them indispensable across household detergent, industrial cleaning, and personal care applications. Global volumes of linear alkylbenzene sulfonates (LAS) have surpassed 4 million tons in recent years, supported by favorable cost economics and a well-established global supply chain.

Nonionic surfactants represent the second-largest segment, with an approximate 29% market share, valued for their mildness, pH stability, and suitability for sensitive skin and food-grade applications. Amphoteric surfactants, although smaller in overall volume, are experiencing the fastest growth, driven by increasing demand in baby care, facial cleansers, and premium personal care formulations due to their excellent skin compatibility and formulation versatility.

Function Insights

Among functional categories, emulsifiers hold the leading position within the specialty surfactants market, accounting for approximately 28% of total functional demand. Emulsifiers are integral to a wide range of end-use products, including creams, lotions, food dressings, agrochemical formulations, and industrial process fluids, where their ability to form stable oil-in-water and water-in-oil systems is technologically indispensable.

Wetting agents and dispersants constitute the second-largest functional segment, driven by their essential roles in textile processing, agricultural spray formulations, and paints and coatings. Conditioning agents are experiencing accelerated growth, particularly in hair care products, where cationic surfactants enhance manageability, smoothness, and substantivity on chemically or mechanically damaged hair fibers.

Application Insights

Household soap and detergent continues to represent the largest application segment within the global specialty surfactants market, accounting for approximately 34% of total market revenue. The extensive worldwide consumption of laundry detergents, dishwashing liquids, surface cleaners, and hand hygiene products ensures sustained, high-volume demand for specialty surfactants.

Personal care represents the second largest and fastest-growing application segment, projected to expand at a CAGR of approximately 5.5% during the forecast period. Formulations across hair care, skin care, and body wash applications increasingly rely on mild amphoteric and nonionic surfactants, with a growing shift toward bio-based and sulfate-free alternatives.

Regional Insights

North America Specialty Surfactants Trends

North America represents one of the most mature and technologically advanced markets for specialty surfactants globally, with the United States accounting for approximately 18.8% of the total market share. The region benefits from a strong innovation and manufacturing ecosystem supported by leading producers such as Dow Inc. and Ashland Inc. Regulatory frameworks administered by the U.S. Environmental Protection Agency (EPA) and the USDA BioPreferred Program are progressively steering the market toward greener and more sustainable surfactant chemistries.

The EPA Safer Choice certification is increasingly influencing procurement decisions among institutional buyers and major consumer brands. Key growth areas include sulfate-free personal care formulations, mild baby care products, high-efficiency laundry detergents, and industrial degreasers. Volatility in global crude supply has further encouraged diversification of feedstock sourcing and increased adoption of bio-based alternatives.

Europe Specialty Surfactants Trends

Europe represents a strategically important market for specialty surfactants, shaped by stringent environmental regulations, a strong sustainability orientation, and a well-established specialty chemicals and biotechnology manufacturing base. Germany, France, the United Kingdom, and Spain function as the region’s principal production and consumption hubs. The EU REACH regulation serves as the core compliance framework, mandating rigorous biodegradability, toxicity, and safety assessments for all surfactants commercialized within the European Economic Area.

Europe is also at the forefront of bio-based surfactant adoption, highlighted by Evonik’s commissioning of the world’s first industrial-scale rhamnolipid biosurfactant facility in Slovakia in 2024. Furthermore, continued capacity investments, such as Lonza Group AG’s approved nonionic surfactant plant in Antwerp, underscore sustained regional commitment to sustainable surfactant production.

Asia Pacific Specialty Surfactants Trends

Asia Pacific represents the largest regional market for specialty surfactants, accounting for approximately 40% of global market share and demonstrating the strongest growth outlook through 2033. China remains the region’s largest national market, supported by high consumption volumes of household cleaning and personal care products, rising disposable incomes, and rapid urbanization. Government-led investments in precision fermentation infrastructure and industrial bio-parks are further strengthening the country’s position in bio-based surfactant scale-up.

India is emerging as the fastest-growing market within the region, driven by expanding domestic manufacturing, growth in food and biotechnology sectors, and supportive policy frameworks such as the India Chemicals Policy 2030. Additionally, accelerating demand in ASEAN economies, particularly Indonesia and Vietnam, combined with proximity to palm and coconut oil feedstocks, provides regional producers with a structural cost advantage in oleochemical-derived specialty surfactants.

Competitive Landscape

The global specialty surfactants market is characterized by a moderately consolidated competitive structure, with the leading five to seven participants, namely BASF SE, Evonik Industries AG, Dow Inc., Clariant, Croda International Plc, and Kao Corporation, collectively accounting for over 65% of total market revenue. These established players benefit from vertically integrated value chains, extensive global distribution capabilities, and substantial research and development resources, which serve as key sources of competitive advantage. Strategic initiatives increasingly focus on expanding bio-based and biosurfactant portfolios, investing in production capacity across the Asia Pacific, and securing long-term supply agreements with major consumer goods manufacturers.

Key Developments:

- March 2026: BASF Hannong Chemicals Solutions (BHCS), the joint venture between BASF and Hannong Chemicals, has officially inaugurated its new non-ionic surfactant (NIS) production site at the Daesan Industrial Complex in Seosan, Chungcheongnam-do, South Korea. The site merges BASF’s advanced technology and product innovation with Hannong Chemicals’ efficient manufacturing capabilities, enabling a reliable supply of high-quality non-ionic surfactants across Asia. Future expansions will include specialty surfactants, further strengthening BASF’s global production network.

- November 2025: Clariant unveiled its newly expanded state-of-the-art facilities at Daya Bay, China, which substantially boost Clariant's manufacturing capabilities in one of its key growth markets. The strategic expansion significantly enhances Clariant's manufacturing capabilities in pharmaceutical excipients and specialty chemicals for personal and home care applications.

- March 2025: Evonik entered into an exclusive agreement with the Cleveland-based Sea-Land Chemical Company for the distribution of its cleaning solutions in the U.S. The agreement builds on a long-standing relationship with the distributor and expands the reach of Evonik’s cleaning solutions to the entire U.S. region. Evonik provides home care, vehicle care, and industrial and institutional cleaning markets with innovative cleaning solutions, many of which have a strong sustainability profile.

Top Companies in Specialty Surfactants

- BASF SE (Ludwigshafen, Germany) is the world’s largest specialty chemicals company and a dominant force in the global surfactants market. The company’s surfactant portfolio spans anionic, nonionic, amphoteric, and bio-based grades under brands including Plantapon®, Dehyton®, and Lutensol®. BASF leverages its vertically integrated petrochemical and oleochemical supply chains and has expanded its RSPO-certified bio-based surfactant range to over 150 SKUs.

- Evonik Industries AG (Essen, Germany) is a global specialty chemicals leader with a strong position in high-performance and bio-based surfactants. The company’s Care Solutions business line offers the REWOFERM™, Tego® Betain, and Rewocare® product series, widely used in personal care and I&I cleaning. Evonik’s inauguration of the world’s first industrial-scale rhamnolipid plant in Slovakia in 2024 establishes a technology moat in next-generation biosurfactants.

- Croda International Plc (Snaith, U.K.) is a British specialty chemicals leader renowned for its high-performance, bio-based surfactants targeting personal care, pharmaceuticals, crop care, and industrial specialties. Its portfolio includes the Tween™, Span™, and Brij™ surfactant series. With operations across 39 countries and more than 6,000 employees, Croda differentiates through innovation in biodegradable and plant-derived surfactant chemistries, zero-palm and non-GMO credentials, and deep regulatory expertise in pharmaceutical-grade emulsifiers, making it a preferred partner for premium personal care and life sciences customers globally.

Companies Covered in Specialty Surfactants Market

- 3M

- Nouryon

- Arkema

- Ashland Inc.

- BASF SE

- Clariant

- Croda International Plc

- Dow Inc.

- Elementis Plc

- Evonik Industries AG

- Huntsman International LLC

- Innospec

- Kao Corporation

- Godrej Industries Ltd.

- KLK Oleo

- Stepan Company

Frequently Asked Questions

The global Specialty Surfactants market is valued at US$ 37.0 Bn in 2026 and is projected to reach US$ 49.7 Bn by 2033, registering a CAGR of 4.3% during the forecast period from 2026 to 2033. The historical CAGR of 3.6% between 2020 and 2025 reflects steady foundational growth, with the accelerating forecast CAGR driven by sustainability-led innovation and expanding end-use applications.

The primary demand drivers include rising global consumption of personal care and household cleaning products, accelerating adoption of bio-based and biodegradable surfactant formulations driven by sustainability mandates such as EU REACH and the EPA Safer Choice program, and expanding applications in oilfield chemicals supported by growing global oil demand per the IEA.

Anionic surfactants are the leading product type, holding approximately 35% of the global market. Their dominance is attributed to their superior cleaning, foaming, and emulsifying performance, cost-effectiveness, and widespread use in laundry detergents, dishwashing products, and shampoos. Linear alkylbenzene sulfonate (LAS) alone exceeded 4 million tons of global volume, anchoring the segment’s leadership.

Asia Pacific is the leading region, accounting for approximately 40% of the global specialty surfactant market value. China is the largest national market, supported by massive household cleaning and personal care consumption. The region’s cost-competitive oleochemical feedstock base, rapid industrialization, and growing middle class in India, Indonesia, and Vietnam reinforce its sustained regional dominance through 2033.

The growth opportunities for the market are bio-based and biosurfactant innovation, where large-scale commitments from FMCG brands like Unilever and breakthrough production technologies from Evonik Industries AG are creating a commercially viable and high-growth biosurfactant sector.

The leading companies in the global specialty surfactants market include BASF SE, Evonik Industries AG, Dow Inc., Croda International Plc, Clariant, Kao Corporation, Huntsman International LLC, Akzo Nobel N.V., Godrej Industries Ltd., KLK Oleo, Innospec, Galaxy Surfactants Ltd., and Arkema. These players collectively account for a significant majority of global specialty surfactant revenues, competing on innovation, portfolio breadth, sustainability credentials, and geographic reach.