- Medical Devices

- Sharps Container Market

Sharps Container Market Size, Share, and Growth Forecast, 2026 – 2033

Sharps Container Market by Product Type (Multipurpose Containers, Patient-Room Containers, Phlebotomy Containers, Tamperproof Containers), Container Size (1–2 gallons, 2–4 gallons, 4–8 gallons, 5+ gallons), and Regional Analysis for 2026 – 2033

Sharps Container Market Size and Trends Analysis

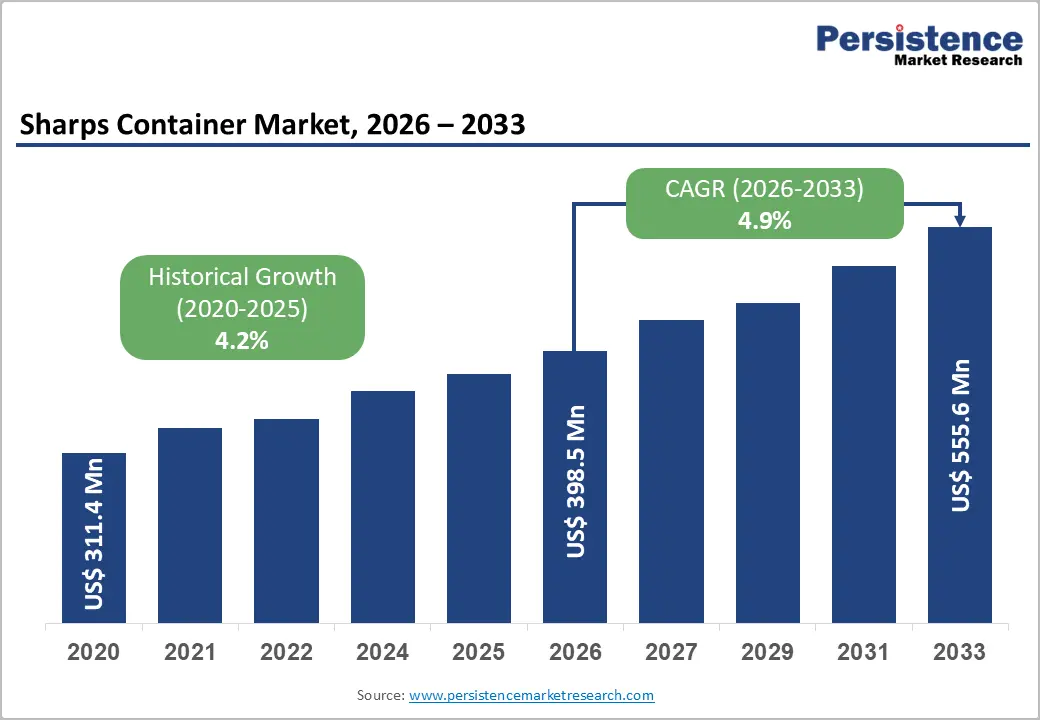

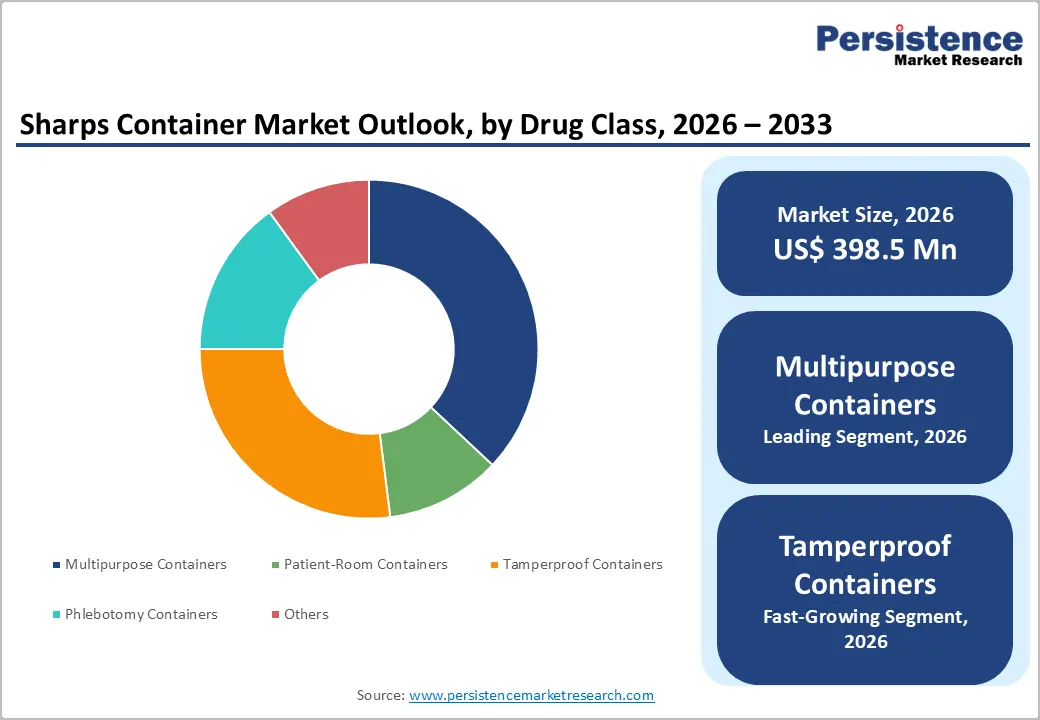

The global sharps container market size is likely to be valued at US$398.5 million in 2026 and is expected to reach US$555.6 million by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by increasing emphasis on safe healthcare waste disposal and infection prevention.

According to the World Health Organization (WHO, 2024), improper handling of sharps waste remains a key contributor to healthcare-associated infections, reinforcing demand for compliant disposal systems. The U.S. Occupational Safety and Health Administration (OSHA, updated 2024) continues to enforce strict Needlestick Safety and Prevention standards, mandating puncture-resistant and labeled sharps containers across healthcare settings. Growing surgical volumes, vaccination programs, and home-based therapies are strengthening the adoption.

Key Industry Highlights:

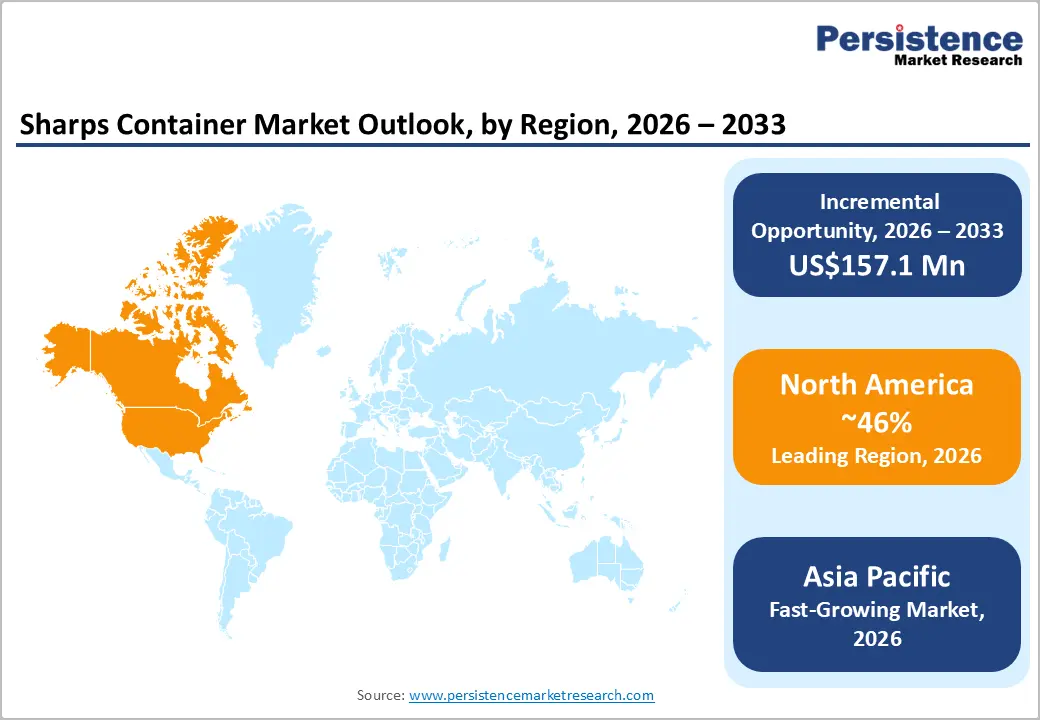

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 46% in 2026, driven by strict regulatory frameworks, advanced healthcare infrastructure, high medical procedure volumes, and strong adoption of compliant medical waste disposal systems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding healthcare infrastructure, rising surgical volumes, growing medical waste awareness, and strengthening regulatory frameworks.

- Leading Product Type: Multipurpose containers are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by increasing infection control regulations, rising healthcare procedure volumes, and growing chronic disease burden.

- Leading Container Size: 2–4 gallon containers are anticipated to be the leading container size, accounting for over 55% of the revenue share in 2026, supported by higher hospital waste volumes, increasing surgical and inpatient care demand, and the need for efficient storage capacity balance.

- Key Opportunity: The expansion of home healthcare, chronic disease self-management therapies, and increasingly stringent medical waste disposal regulations is creating substantial opportunities for innovative, safe, and sustainable sharps container solutions worldwide.

DRO Analysis

Driver - Increasing Generation of Medical Waste and Healthcare Procedures

Expanding hospital admissions, surgical interventions, vaccination programs, and diagnostic activities significantly contribute to the demand for safe disposal systems. Growth in chronic diseases such as diabetes and cancer increases injectable treatments, directly increasing sharps usage and disposal requirements across hospitals and clinical environments.

Increasing healthcare infrastructure development in emerging economies and the expansion of outpatient and ambulatory care centers are accelerating sharps waste output. The CDC (2024 infection control guidance) emphasizes safe injection practices and proper disposal to reduce needlestick injuries among healthcare workers.

Rising awareness of occupational safety standards, combined with stricter regulations in developed regions, is pushing healthcare facilities to adopt standardized sharps containers. The continuous growth in medical services, coupled with higher procedural intensity, ensures sustained demand for advanced, puncture-resistant, and regulatory-compliant sharps disposal solutions across healthcare systems.

Restraint - Competitive Threats from Alternatives and Awareness Gaps

Many healthcare facilities, particularly in cost-sensitive regions, opt for outsourced waste handling instead of investing in dedicated sharps container infrastructure. This reduces direct product adoption in some segments. Variability in regulatory enforcement across developing regions limits standardized usage, creating inconsistencies in adoption rates. While developed markets follow strict protocols, emerging economies lack uniform compliance, impacting overall market penetration of advanced sharps containment solutions.

There is a lack of awareness and training regarding proper sharps disposal practices in smaller healthcare setups and homecare environments. According to the WHO (2023), improper disposal of sharps continues to pose significant infection risks in low-resource settings. Inadequate education about needlestick injury prevention and limited access to certified disposal systems slow market growth. Cost sensitivity also restricts adoption of premium safety containers.

Opportunity - Home Healthcare and Specialized Disposal Programs

The growing shift toward home healthcare presents a major opportunity for the sharps container market, driven by increasing use of self-injection therapies for diabetes, fertility treatments, and chronic disease management. As per the CDC (2024 home care safety recommendations), safe disposal of sharps in home environments is essential to prevent accidental injuries and infections. This has led to rising demand for compact, portable, and user-friendly sharps containers designed specifically for non-hospital settings.

Governments and healthcare organizations are increasingly promoting specialized medical waste collection and return programs to support safe disposal outside clinical environments. These initiatives encourage the adoption of standardized sharps disposal kits and structured waste collection systems.

WHO guidelines also emphasize community-level awareness programs for safe injection waste handling. As home-based care expands and healthcare decentralization continues, manufacturers have significant opportunities to develop innovative, sustainable, and easy-to-use sharps container solutions tailored for personal and small-scale medical use.

Category-wise Analysis

Product Type Insights

Multipurpose containers are expected to lead, accounting for 40% of the global revenue share in 2026, due to their versatility, cost-efficiency, and wide usability across hospitals, diagnostic centers, and outpatient clinics. These containers are designed to safely dispose of multiple types of sharps waste, including needles, syringes, and surgical blades, making them the preferred choice in high-volume healthcare environments. For example, large hospital networks such as tertiary care hospitals in North America and Europe extensively deploy multipurpose sharps containers in emergency departments and surgical units.

Tamperproof containers are likely to represent the fastest-growing segment, supported by rising demand for enhanced safety, traceability, and regulatory compliance in medical waste handling. These containers are designed with secure locking mechanisms that prevent unauthorized access and accidental exposure, making them highly suitable for sensitive healthcare environments. For instance, advanced hospitals and pharmaceutical research facilities are increasingly adopting tamperproof sharps containers to ensure secure disposal of controlled or high-risk medical waste.

Container Size Insights

The 2–4-gallon container segment is expected to dominate the market, accounting for approximately 55% of total revenue in 2026. Its strong position is driven by an effective balance of capacity, convenience, and ease of handling, making it suitable for a wide range of healthcare environments. Additionally, these containers support infection control requirements while accommodating the limited storage space available in patient rooms, clinics, and treatment areas. For instance, many mid-sized hospitals across Asia and Europe commonly utilize 2–4-gallon sharps containers in hospital wards and outpatient facilities due to their practical size and functionality.

The 4–8-gallon container segment is anticipated to register the fastest growth during the forecast period, driven by rising demand from high-volume healthcare facilities, including large hospitals, surgical centers, and trauma units. These containers help minimize replacement frequency and enhance waste management efficiency in busy clinical settings. For instance, many large hospitals and surgical facilities are increasingly adopting 4–8-gallon sharps containers in operating rooms, intensive care units (ICUs), and other high-use areas to effectively manage substantial volumes of sharps waste while maintaining compliance with safety and regulatory standards.

Regional Insights

North America Sharps Container Market Trends

North America is anticipated to be the leading region, accounting for a market share of 46% in 2026, supported by stringent medical waste disposal regulations, high healthcare spending, and strong awareness regarding needlestick injury prevention. A notable example includes Daniels Health, which continues expanding its reusable Sharpsmart container programs across healthcare facilities.

U.S. Sharps Container Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 80% of the market share in 2026, driven by extensive healthcare infrastructure and strict OSHA and FDA regulations governing sharps disposal. Rising diabetes prevalence and increasing use of injectable biologics continue to generate substantial sharps waste volumes. Hospitals are investing in advanced container systems that improve safety and traceability. Growth in outpatient procedures and ambulatory care centers is supporting demand.

Canada Sharps Container Market Trends

Canada is likely to be a significant market for sharps containers, holding approximately 20% of the market share in 2026, supported by strong healthcare safety standards and increasing awareness regarding medical waste management. Provincial healthcare authorities continue to support safe disposal programs for community and home healthcare users. Growing vaccination activities and chronic disease treatment contribute to rising sharps waste generation. Canadian healthcare facilities are increasingly implementing sustainable waste management strategies to reduce environmental impact.

Europe Sharps Container Market Trends

Europe is likely to be a significant market for sharps containers in 2026, due to increasing surgical procedures, growing chronic disease burden, and strong focus on occupational safety. Healthcare facilities are prioritizing environmentally sustainable waste management practices, encouraging adoption of reusable sharps containment solutions. For instance, Stericycle, which has expanded healthcare waste management services across several European markets.

U.K. Sharps Container Market Trends

The U.K. is likely to be a significant market for sharps containers, accounting for 15% of the Europe market share in 2026, supported by strong National Health Service infection control requirements and increasing emphasis on healthcare worker safety. Demand is supported by rising outpatient care and home-based treatment programs. Safe disposal of sharps remains a priority due to growing use of injectable medications and chronic disease therapies. Healthcare organizations are expanding sustainability initiatives to reduce waste-related environmental impacts.

Germany Sharps Container Market Trends

Germany is anticipated to dominate the regional market, accounting for around 37% of the share in 2026, due to its highly developed healthcare system and strict medical waste regulations. Rising surgical procedure volumes continue to increase the demand for reliable sharps disposal solutions. Hospitals are investing in safer waste management systems to enhance infection prevention and worker safety. Sustainability remains a major priority, encouraging adoption of reusable container technologies.

Asia Pacific Sharps Container Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rapid healthcare infrastructure expansion, rising healthcare expenditure, and increasing awareness regarding biomedical waste management. Growth in hospital construction, surgical procedures, and chronic disease treatment is generating higher volumes of sharps waste across the region. For instance, Medline Industries continues expanding its healthcare product presence across Asia Pacific markets.

China Sharps Container Market Trends

China is projected to dominate the regional market, holding around a 30% share in 2026, due to rapid healthcare modernization and expanding hospital infrastructure. Increasing surgical procedures and chronic disease prevalence are driving higher sharps waste generation. Healthcare facilities are investing in safer disposal systems to comply with evolving regulations. Expansion of vaccination programs and diagnostic services is creating additional demand.

India Sharps Container Market Trends

India is expected to emerge as a significant market, accounting for approximately a 22% share in 2026, due to rising patient volumes and strengthening biomedical waste management regulations. Increasing numbers of hospitals, diagnostic laboratories, and vaccination programs are contributing to greater sharps disposal requirements. Awareness regarding needlestick injury prevention and infection control is improving among healthcare providers. Demand from home healthcare and chronic disease management is also increasing.

Competitive Landscape

The global sharps container market exhibits a moderately fragmented structure, driven by the presence of established medical waste management providers, healthcare product manufacturers, and specialized sharps disposal solution companies operating across regional and international markets. Market growth is supported by increasing regulatory requirements for safe sharps disposal, rising healthcare procedure volumes, and growing adoption of infection prevention practices.

With key leaders, including Thermo Fisher Scientific Inc., BD, Cardinal Health, Medline Industries, Stericycle, Daniels Sharpsmart Inc., BondTech Corporation (Atlas Copco AB), EnviroTain, Sharps Medical Waste Services, and GPC Medical Ltd., the competitive environment remains dynamic and innovation-focused. These players compete through product quality, safety features, regulatory compliance, distribution strength, sustainability initiatives, and integrated waste management capabilities.

Key Industry Developments:

- In June 2025, Daniels Health launched the 24L SHARPSGUARD® eco container, the world's first sharps container manufactured using recycled healthcare waste, supporting sustainability and circular healthcare waste management initiatives.

- In March 2025, Sanaway Ltd. introduced a new reusable recycled sharps container featuring a multi-use lifecycle, advanced tracking capabilities, and a reduced carbon footprint to help healthcare facilities meet sustainability targets.

- In November 2025, Stericycle expanded its SharpsRx Pro™ solution, combining sharps and non-hazardous pharmaceutical waste disposal into a single reusable container to improve efficiency and sustainability in healthcare facilities.

Companies Covered in Sharps Container Market

- Thermo Fisher Scientific Inc.

- BD

- BondTech Corporation (Atlas Copco AB)

- Cardinal Health

- Medline Industries, LP.

- EnviroTain

- Stericycle

- Sharps Medical Waste Services

- Daniels Sharpsmart Inc.

- GPC Medical Ltd.

Frequently Asked Questions

The global sharps container market is projected to reach US$398.5 million in 2026.

Rising healthcare procedures, increasing medical waste generation, stricter sharps disposal regulations, and growing emphasis on infection prevention and healthcare worker safety drive the sharps container market.

The sharps container market is expected to grow at a CAGR of 4.9% from 2026 to 2033.

Expanding home healthcare services, growing adoption of reusable sharps containers, and increasing investment in safe medical waste management programs present significant market opportunities.

Thermo Fisher Scientific Inc., BondTech Corporation (Atlas Copco AB), Cardinal Health, and Medline Industries, LP are the leading players.