- Semiconductor Materials & Components

- Semiconductor Diffusion Equipment Market

Semiconductor Diffusion Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Semiconductor Diffusion Equipment Market by Product Type (Vertical Diffusion Systems, Single Wafer Diffusion Systems, Others), Technology (Thermal Diffusion, Rapid Thermal Processing (RTP), Others), Wafer Size, End-user, and Regional Analysis for 2026 - 2033

Semiconductor Diffusion Equipment Market Size and Trends Analysis

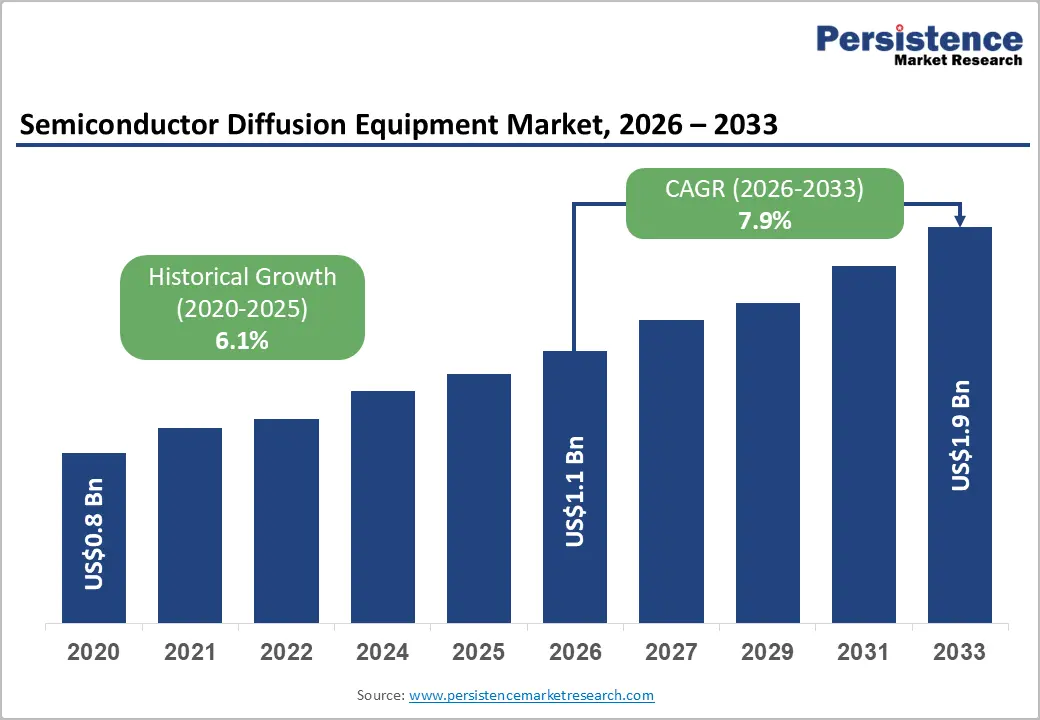

The global semiconductor diffusion equipment market size is likely to be valued at US$1.1 billion in 2026 and is expected to reach US$1.9 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by increasing emphasis on thermal processing capabilities for oxidation, annealing, and diffusion applications across both batch and single-wafer platforms.

Expanding semiconductor fabrication capacity, wider adoption of 300 mm wafers, and continued investments in both advanced-node and mature-node manufacturing facilities are driving equipment demand. In addition, government-led semiconductor localization initiatives across key economies are accelerating fab investments and semiconductor processing equipment procurement.

Key Industry Highlights:

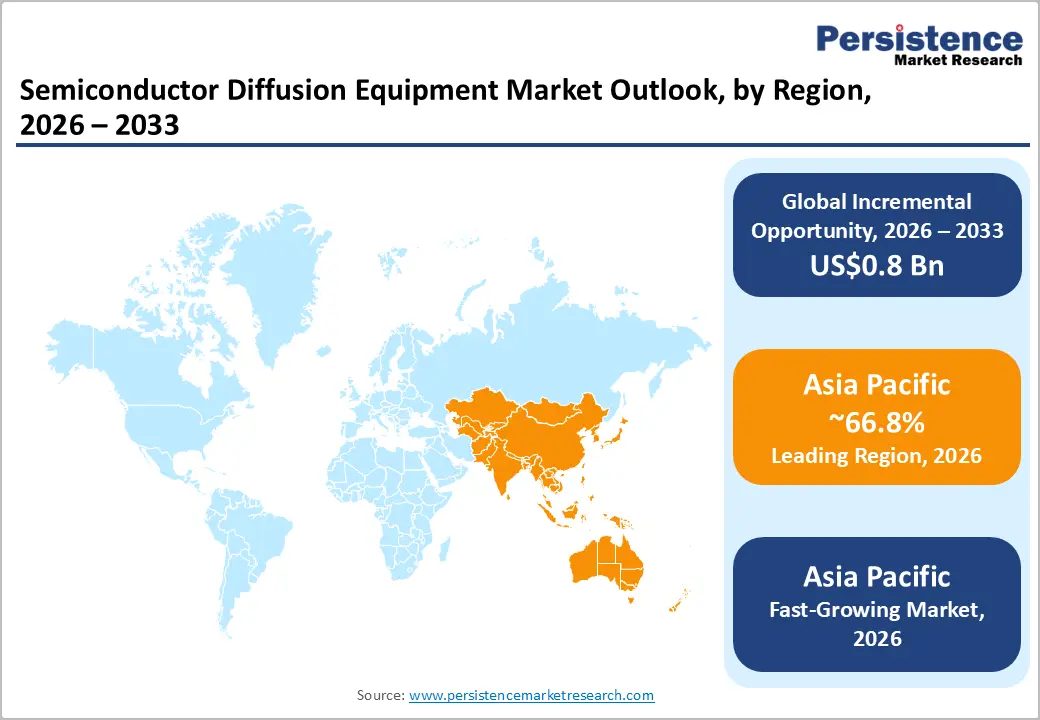

- Leading Region: Asia Pacific is projected to account for 66.8% of market share, driven by strong manufacturing concentration in China, Taiwan, South Korea, and Japan.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by continued fab investments and emerging semiconductor ecosystems in India and Southeast Asia.

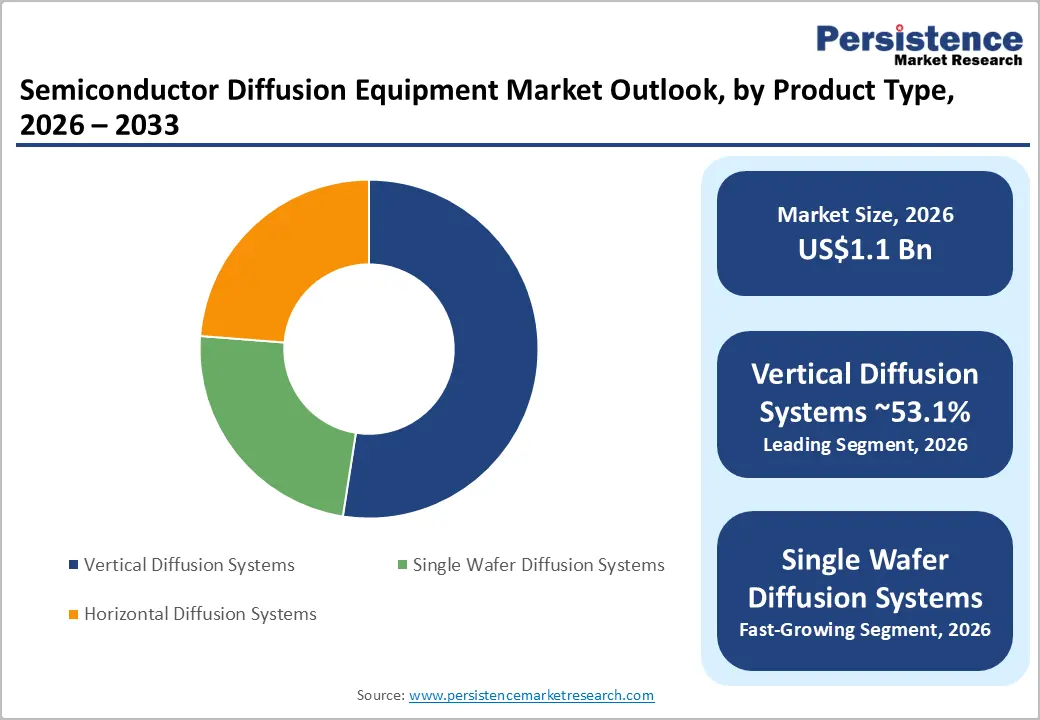

- Dominant Product Type: Vertical diffusion systems are anticipated to dominate, with 53.1% market share, due to their high throughput, process uniformity, and suitability for large-scale 300 mm wafer production.

- Leading Technology: Thermal diffusion is estimated to lead, accounting for 50.2% of the market share, supported by its widespread use in oxidation, annealing, and dopant activation processes across semiconductor manufacturing.

DRO Analysis

Driver - Fab Expansion in 300 mm and Advanced-Node Capacity is Driving Thermal Equipment Demand

Global semiconductor manufacturing capacity is undergoing a structural expansion driven by rising demand for advanced computing, artificial intelligence, automotive electronics, and high-performance memory. Large-scale fab construction programs and capacity upgrades are increasing the demand for front-end equipment, including diffusion systems used in oxidation, annealing, and dopant activation processes.

The transition toward smaller process nodes, including sub-5 nm and emerging 2 nm technologies, requires precise thermal control and consistent process uniformity, elevating the importance of advanced diffusion systems. At the same time, continued investment in mature nodes for automotive and industrial applications is sustaining demand for high-throughput batch diffusion tools. This dual demand structure, advanced-node precision and mature-node volume, creates a stable and recurring equipment demand cycle, strengthening long-term revenue visibility for suppliers.

Government-Led Semiconductor Localization Is Accelerating Regional Equipment Investments

Public-sector support for semiconductor manufacturing has become a defining growth driver. National programs in the United States, Europe, and Asia are incentivizing domestic fabrication through subsidies, tax benefits, and infrastructure investment. These initiatives aim to reduce supply chain dependencies and enhance technological sovereignty.

As a result, new fabs are being developed across multiple regions, increasing demand for localized equipment procurement and technical support. Diffusion equipment vendors benefit from this shift by establishing regional service hubs, application centers, and partnerships with emerging fabrication facilities. Localization also shortens qualification cycles, as proximity enables faster process validation and maintenance support. This structural shift is expanding the addressable market beyond traditional semiconductor hubs.

Restraint - High Capital Costs and Complex Qualification Processes Limit Rapid Adoption

Semiconductor diffusion equipment requires significant capital investment and involves complex integration into fabrication workflows. Equipment must undergo extensive qualification procedures, including process validation, contamination control, and compatibility testing with adjacent manufacturing steps such as lithography and deposition.

These requirements increase time-to-market and create high switching costs for semiconductor manufacturers. Equipment procurement decisions are therefore closely tied to long-term production strategies and capital expenditure cycles. Any delays in fab construction or node transitions can lead to postponed equipment orders, creating demand volatility. While the overall market remains on a growth trajectory, purchasing patterns are uneven and highly dependent on semiconductor industry investment cycles.

Opportunity - Emerging Semiconductor Manufacturing Hubs Offer Long-Term Growth Potential

The expansion of semiconductor manufacturing into emerging regions such as India and Southeast Asia is creating new growth avenues for diffusion equipment suppliers. Governments in these regions are actively promoting semiconductor ecosystem development through policy incentives, infrastructure investments, and strategic partnerships.

New fabrication facilities in these markets require complete equipment ecosystems, including diffusion systems for front-end processing. This creates opportunities not only for initial equipment sales but also for long-term service contracts, upgrades, and spare parts supply. Establishing an early presence in these regions allows suppliers to build customer relationships and secure recurring revenue streams as local ecosystems mature.

Advanced Thermal Processing Technologies are Gaining Importance in Next-Generation Devices

As semiconductor devices become more complex, the need for precise and efficient thermal processing is increasing. Advanced logic devices, high-bandwidth memory, and 3D architectures require tighter control over temperature profiles, dopant distribution, and defect levels.

Technologies such as rapid thermal processing and single-wafer diffusion systems are gaining traction because they enable shorter process cycles and improved precision. These systems help manufacturers optimize yield, reduce energy consumption, and manage increasingly stringent process requirements. Equipment suppliers that invest in innovation and develop energy-efficient, high-precision solutions are well-positioned to capture value in this evolving landscape.

Category-wise Analysis

Product Type Analysis

Vertical diffusion systems are anticipated to account for 53.1% of the market share over the forecast period, driven by their ability to deliver high wafer throughput, uniform thermal distribution, and efficient cleanroom space utilization. These systems are widely deployed in 300 mm fabrication facilities, particularly in high-volume logic and memory fabs where batch processing efficiency is critical.

For instance, leading semiconductor manufacturers such as Taiwan Semiconductor Manufacturing Company and Samsung Electronics utilize vertical furnace systems extensively in oxidation and annealing steps to maintain process consistency across large wafer volumes. Their strong installed base and proven reliability make them the preferred choice for high-volume manufacturing environments. Equipment suppliers such as Tokyo Electron and Kokusai Electric have developed advanced vertical furnace platforms that support multi-wafer batch processing with high uniformity and low defect rates.

Single wafer diffusion systems are the fastest-growing, supported by increasing demand for precision processing in advanced semiconductor nodes. These systems offer superior control over thermal cycles, enabling better dopant accuracy and reduced process variability, which is critical for sub-5 nm and emerging 2 nm technologies.

They are particularly suited for advanced logic, memory, and specialized semiconductor applications where process margins are narrow. For example, companies such as Intel Corporation and Micron Technology increasingly adopt single-wafer and rapid thermal systems to optimize junction formation and reduce thermal budgets in advanced nodes. Their ability to support rapid process iteration also makes them valuable in R&D environments.

Technology Insights

Thermal diffusion is anticipated to hold 50.2% of the market share in 2026, reflecting its widespread use in semiconductor manufacturing. It remains a fundamental process for dopant activation, oxidation, and annealing across both advanced and mature nodes. The technology benefits from well-established process knowledge, reliability, and compatibility with existing fabrication workflows. It is extensively used in high-volume fabs operated by companies such as SK Hynix and GlobalFoundries, where consistent thermal processing is essential for maintaining yield across large production runs. Its versatility ensures continued adoption across a wide range of semiconductor applications, supporting its leadership position in both logic and memory manufacturing.

Rapid thermal processing (RTP) is anticipated to grow, driven by the need for precise and short-duration thermal cycles. RTP enables faster heating and cooling, reducing thermal exposure and improving process control, which is critical for advanced semiconductor devices. This technology is increasingly adopted in cutting-edge fabs, including those operated by Taiwan Semiconductor Manufacturing Company and Intel Corporation, where minimizing thermal diffusion is essential to maintain transistor performance at smaller geometries. RTP is also widely used in advanced memory production, particularly for high-bandwidth memory (HBM) and 3D NAND, where precise thermal budgets directly impact device efficiency.

Regional Insights

North America Semiconductor Diffusion Equipment Market Trends

North America is experiencing steady growth, supported by strong government incentives and advanced semiconductor innovation. Public funding programs are encouraging domestic manufacturing, leading to increased fab construction and equipment demand. A notable example is the expansion of fabrication facilities by Intel Corporation in Arizona and Ohio, alongside investments by Taiwan Semiconductor Manufacturing Company in its Arizona fabs. These developments are increasing demand for front-end equipment, including diffusion systems, as new production lines require complete thermal processing infrastructure.

U.S. Semiconductor Diffusion Equipment Market Trends

The U.S. remains the regional anchor, driven by policy-backed manufacturing and strong R&D capabilities. Companies such as Micron Technology are investing in advanced memory fabs, while GlobalFoundries continues to expand capacity for specialty semiconductors. These investments are strengthening domestic supply chains and increasing the need for localized equipment servicing and process optimization.

The region’s strength lies in its innovation ecosystem, advanced research capabilities, and focus on high-performance semiconductor technologies. Demand for diffusion equipment is driven by advanced logic and memory production and by ecosystem development. Local presence and service capabilities are becoming increasingly important, as semiconductor manufacturers prioritize supply chain resilience and operational efficiency.

Europe Semiconductor Diffusion Equipment Market Trends

Europe’s semiconductor market is driven by policy initiatives aimed at achieving technological independence and strengthening regional capabilities. Investments in semiconductor manufacturing are increasing, supported by government incentives and strategic programs. For example, Intel Corporation has announced large-scale investments in Germany, while STMicroelectronics and Infineon Technologies are expanding production capacity for automotive and power semiconductors. These developments are driving demand for diffusion equipment tailored to both advanced and mature-node applications.

Germany Semiconductor Diffusion Equipment Market Trends

Germany leads the region due to its strong industrial base and semiconductor investments. Infineon’s expansion in power semiconductor manufacturing and Intel’s planned fab projects are strengthening the country’s position as a key hub for both advanced and specialty chip production. This is increasing demand for thermal processing systems used in power electronics and automotive chips.

The region offers opportunities for suppliers that align with regulatory frameworks and focus on specialized applications such as automotive and industrial semiconductors. The emphasis on energy-efficient manufacturing and supply chain resilience is also shaping equipment procurement decisions.

Asia Pacific Semiconductor Diffusion Equipment Market Trends

Asia Pacific is projected to dominate the market, accounting for 66.8% of market share in 2026 and growing at a CAGR of 8.4%. The region benefits from a high concentration of semiconductor manufacturing facilities and strong investment activity, making it the primary demand center for diffusion equipment.

China Semiconductor Diffusion Equipment Market Trends

China continues to expand its domestic semiconductor manufacturing capabilities through companies such as Semiconductor Manufacturing International Corporation and Yangtze Memory Technologies. These firms are increasing capacity in both logic and memory production, driving demand for diffusion and thermal processing equipment as part of broader efforts toward semiconductor self-sufficiency.

Taiwan Semiconductor Diffusion Equipment Market Trends

Taiwan remains a global leader in advanced semiconductor manufacturing, led by Taiwan Semiconductor Manufacturing Company. Its continuous investment in advanced-node fabs, including 3 nm and beyond, is creating sustained demand for high-precision thermal equipment such as RTP and single-wafer diffusion systems. These investments reinforce Taiwan’s central role in the global semiconductor supply chain.

South Korea Semiconductor Diffusion Equipment Market Trends

South Korea is a major hub for memory production, driven by Samsung Electronics and SK Hynix. Their expansion in DRAM and NAND manufacturing, particularly for high-bandwidth memory, is increasing the need for advanced thermal processing technologies that ensure precision and yield in complex device architectures.

Japan Semiconductor Diffusion Equipment Market Trends

Japan contributes through both semiconductor manufacturing and equipment innovation. Companies such as Tokyo Electron and Kokusai Electric are global leaders in diffusion and thermal processing equipment. Their technological advancements and strong export presence support regional and global market growth.

The region’s combination of scale, technological capability, and policy support ensures its continued leadership in the market.

Competitive Landscape

The global semiconductor diffusion equipment market is moderately concentrated, with a small number of established players dominating core thermal processing technologies. At the same time, the presence of specialized and regional suppliers contributes to overall market fragmentation.

Competition is driven by technological innovation, process expertise, and long-term customer relationships. Suppliers differentiate themselves through product performance, reliability, and service capabilities.

Key players are focusing on innovation, regional expansion, and lifecycle service offerings. Strategies include developing high-precision thermal systems, expanding local support infrastructure, and improving energy efficiency. Companies are also investing in advanced process technologies to address evolving semiconductor manufacturing requirements.

Key Industry Developments:

- In December 2025, ASM International announced the acquisition of Axus Technology, a U.S.-based provider of CMP equipment, to expand its capabilities in compound semiconductors and advanced packaging, strengthening its position in next-generation semiconductor processing.

Companies Covered in Semiconductor Diffusion Equipment Market

- Tokyo Electron Ltd.

- Kokusai Electric Corporation

- ASM International N.V.

- Applied Materials, Inc.

- SCREEN Holdings Co., Ltd.

- Thermco Systems

- Centrotherm International AG

- NAURA Technology Group Co., Ltd.

- ULVAC, Inc.

- CVD Equipment Corporation

- Expertech Inc.

- Tempress Systems, Inc.

- Bruce Technologies, Inc.

- SEMCO Technologies

- SVCS Process Innovation S.r.l.

- PVA TePla AG

- Lam Research

Frequently Asked Questions

The semiconductor diffusion equipment market is estimated to be valued at US$1.1 billion in 2026.

The semiconductor diffusion equipment market is projected to reach US$1.9 billion by 2033.

Key trends include increasing adoption of 300 mm wafer fabrication, rising demand for single-wafer and rapid thermal processing systems, and strong investments in regional semiconductor manufacturing driven by government initiatives.

Vertical diffusion systems are the leading product segment, accounting for 53.1% of the market share, due to their high throughput and suitability for large-scale semiconductor production.

The semiconductor diffusion equipment market is expected to grow at a CAGR of 7.9% between 2026 and 2033.

Major players include Tokyo Electron, Kokusai Electric, ASM International, Applied Materials, and Lam Research.