- Automation & Robotics

- Screening Equipment Market

Screening Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Screening Equipment Market By Product Type (Vibrating Screens, Mobile & Modular, Others), Technology (Conventional Mechanical Vibratory, High-Frequency/Ultrafine, Others), End-user, Service, and Regional Analysis for 2026 - 2033

Screening Equipment Market Size and Trends Analysis

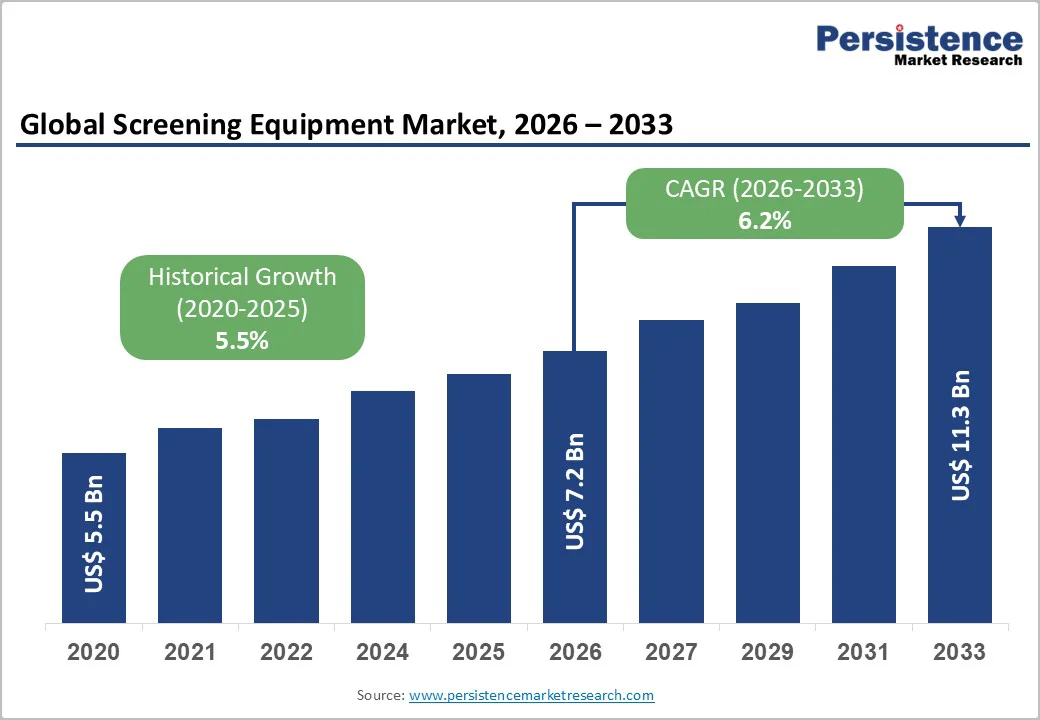

The global screening equipment market size is likely to be valued at US$7.2 Billion in 2026 and is expected to reach US$11.3 Billion by 2033, growing at a CAGR of 6.2% from 2026 to 2033, driven by steady demand across construction, mining, recycling, and industrial processing applications.

Growth is shaped by rising mineral exploration activity, expansion in infrastructure projects, and the increasing adoption of automated screening systems. Environmental compliance requirements and improvements in material handling efficiency further reinforce market momentum.

Key Industry Highlights

- Leading Region: Asia Pacific, accounting for around 41.8% of global screening equipment demand in 2026, driven by large-scale mineral processing, aggregate production, and extensive infrastructure expansion.

- Fastest-growing Region: Asia Pacific, due to accelerated recycling adoption, increasing capacity additions in mining, and rapid industrialization in China, India, and ASEAN.

- Investment Plans: Global OEMs are directing substantial capital toward regional manufacturing expansion and electrified mobile fleet development, with estimated investment growth of 6-8% annually in facility upgrades, digital capability building, and aftermarket infrastructure through 2030.

- Dominant Product Type: The vibrating screens category is expected to dominate the market, holding approximately 47.2% of the total revenue in 2026, supported by widespread use in mining, aggregates, and high-throughput industrial processing.

- Leading Technology: Mechanical vibratory screening systems are expected to lead with about 51.5% share in 2026, reflecting their proven durability, cost efficiency, and suitability across a broad range of feed materials.

| Key Insights | Details |

|---|---|

| Screening Equipment Market Size (2026E) | US$7.2 Bn |

| Market Value Forecast (2033F) | US$11.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Infrastructure and Construction Projects

Global construction output continues to grow, supported by public-sector investments in transportation corridors, energy facilities, and housing developments. According to government infrastructure expenditure reports across major economies, annual capital allocation in transportation and utilities has increased steadily, creating sustained demand for screening machinery used in cement plants, aggregates processing, and construction material preparation.

Higher volumes of raw materials, such as gravel, sand, and crushed stone, require efficient screening systems to meet project performance standards. As more countries prioritize urban development and industrial expansion, equipment replacement cycles shorten, driving recurring demand for advanced and energy-efficient screening units.

Rising Mining and Mineral Processing Activities

The mining sector remains a core consumer of screening systems, with increased exploration and extraction of base metals, precious metals, and industrial minerals contributing to market expansion. Government mineral output statistics indicate consistent growth in iron ore, copper, and bauxite extraction, which intensifies the need for robust screening technologies capable of handling high-capacity operations.

Adoption of advanced screens enhances mineral recovery rates, reduces waste, and supports compliance with operational safety standards. Automation, wear-resistant screening media, and high-frequency screens are gaining adoption as mines modernize to optimize efficiency. Production scale-ups in both surface and underground mines further reinforce long-term screening equipment demand.

Waste Recycling and Environmental Compliance Requirements

Municipal and industrial waste generation continues to rise, prompting governments to enact stricter material recovery and landfill reduction regulations. Screening equipment is essential in recycling plants for sorting plastics, metals, aggregates, and biomass. Regulatory directives targeting higher recycling rates and sustainable material management contribute to equipment adoption.

The shift toward circular economy models and increased investments in recycling infrastructure strengthen the market for screening systems engineered for resource recovery. High-precision screens ensure better separation quality, enabling recycling operators to meet purity benchmarks established by environmental agencies.

Barrier Analysis - High Capital Investment and Operating Costs

Screening machinery requires significant upfront investment, especially for large-capacity, automated, or technologically advanced models. Operators in small and mid-sized enterprises often face financial constraints that limit equipment upgrades.

Maintenance requirements, such as periodic replacement of screening media and mechanical components, add to total ownership costs, reducing adoption rates in cost-sensitive markets. Variability in raw material prices and energy costs also affects operational budgets, prompting delays in planned machinery purchases.

Supply Chain Volatility and Component Shortages

The screening equipment industry is vulnerable to disruptions involving steel, motors, hydraulics, and electronic control components. Fluctuations in global logistics capacity, port delays, and long lead times for critical parts create production bottlenecks.

Manufacturers may encounter delays in fulfilling orders, leading to project postponements and higher procurement costs for end users. Persistent supply chain uncertainty hampers scaling of advanced screening products and affects long-term industry growth consistency.

Opportunity Analysis - Integration of Automation and IoT-Enabled Monitoring

Automation adoption is accelerating in mineral processing, recycling, and industrial manufacturing. The integration of smart monitoring systems, digital sensors, and predictive maintenance technologies provides operational insights regarding vibrations, screen load, and wear patterns.

IoT-enabled screening systems offer real-time diagnostics, enhancing uptime and improving processing efficiency. The opportunity for vendors lies in developing modular digital solutions that complement existing equipment. As industries modernize, the digital screening segment represents a growing market opportunity valued at several billion dollars over the forecast horizon based on technology adoption rates.

Growing Demand in Emerging Markets

Industrial expansion across emerging economies in Asia, Africa, and Latin America fuels demand for construction aggregates, minerals, and processed materials. Large-scale infrastructure development and mining reforms in these regions create a significant growth opportunity for screening machinery suppliers.

Market penetration into emerging regions is associated with projected multi-year growth due to increasing mechanization and foundational industrial development. Companies offering cost-effective, durable, and adaptable screening solutions are well-positioned to capture untapped market potential.

Shift toward Energy-Efficient and Environment-Friendly Screens

Environmental regulatory agencies across major regions emphasize reduced emissions, noise limits, and resource efficiency in industrial equipment. Manufacturers developing low-energy screens, lightweight screening media, and noise-controlled systems can access a growing demand segment.

Energy-efficient machinery supports compliance while reducing operational costs, creating measurable financial benefits for users. This trend opens avenues for product development and innovation, with an estimated multi-year market expansion trajectory.

Category-wise Analysis

Product Type Insights

Vibrating screens, including linear, circular, and banana configurations, are anticipated to hold approximately 47.2% share of the market in 2026. These systems are widely used in mining, aggregate production, and the processing of construction materials as they support high throughput, reliable particle separation, and continuous operation under demanding conditions.

They are essential in high-capacity mineral-processing lines where consistent performance, serviceability, and operating efficiency guide equipment selection. Leading product examples include high-capacity banana screens, heavy-duty linear screens, and elliptical-motion designs deployed in major quarrying and mining operations worldwide.

Mobile and modular screening systems, including trommels, compact tracked screens, and portable plant configurations, are growing at the fastest pace due to strong adoption in recycling, contract mining, and infrastructure development. These systems enable rapid site setup, reduced civil works requirements, and lower transport and installation costs for short-term or multi-location projects.

Their uptake is particularly strong among mid-tier operators seeking flexible assets and among recyclers integrating screening into construction and demolition debris processing and municipal solid-waste lines. Electrified mobile trailers, hybrid powerpacks, and modular screening plants further accelerate adoption. As a result, mobile and modular systems record a higher compound annual growth rate than stationary units in most forward-looking projections.

Technology Insights

Conventional mechanical screens are expected to lead with about 51.5% share in 2026, based on vibratory motion and robust steel fabrication. These systems are preferred for heavy industrial applications such as mining, aggregates, and large-scale material-processing operations. Their appeal is rooted in proven reliability, high throughput, ease of maintenance, and long service lifecycles supported by extensive OEM and distributor networks.

Conventional technologies account for the majority of global revenue as they satisfy core classification needs, especially in plants that prioritize uptime and low cost per ton. Despite the emergence of digital and high-frequency alternatives, conventional screens remain the standard for primary and secondary screening tasks.

Sensor-enabled and high-frequency screening platforms are likely to expand at the fastest rate in 2026. These systems combine precision motion patterns, fine-mesh media, and real-time monitoring capabilities to achieve more accurate cut points and higher product-quality consistency. Embedded sensors monitor vibration levels, detect screen blinding, and support predictive maintenance, reducing downtime and improving yield.

Growth is driven by mineral-processing applications where fine classification directly affects recovery rates and by industries seeking more automated, data-driven operations. Digital-ready screen designs, remote diagnostics, and integrated control systems contribute to strong adoption momentum, making this technology segment the fastest-growing within the market.

Regional Insights

North America Screening Equipment Market Trends - High-Capacity Demand, Electrification, and Recycling Growth

North America remains one of the most significant regional markets for screening equipment, led primarily by the U.S. The region accounts for a sizable share of global revenue, supported by large aggregates operations, mining activity in the western states, and increasing investments in recycling infrastructure.

The U.S. market benefits from high replacement cycles and strong demand for premium, high-capacity equipment, resulting in above-average per-unit selling prices. Market growth generally aligns with mid-single-digit annual increases, reflecting steady infrastructure spending and upgrades to more energy-efficient and electrified systems.

The U.S. dominates regional revenue, driven by robust aggregates production, asphalt and concrete recycling, and mineral-processing activity. Canada contributes significantly through mining-centric provinces such as Ontario, Quebec, and Alberta, where mineral-processing plants maintain a consistent need for heavy-duty screening solutions.

Across North America, successful OEMs rely on extensive dealer networks, strong aftermarket presence, and rapid parts availability. The region’s rental market creates recurring opportunities for mobile and compact screening solutions, particularly for short-duration projects.

Europe Screening Equipment Market Trends - Energy-Efficient Systems and Circular-Economy Compliance

Europe represents a mature yet innovation-intensive market for screening equipment, supported by high regulatory standards and a strong emphasis on energy efficiency and circular-economy practices. Demand originates from mining, quarrying, urban infrastructure, and well-developed recycling markets.

Germany, the U.K., France, and Spain serve as the region’s primary contributors, reflecting strong aggregate consumption and steady investment in infrastructure modernization.

Germany’s established industrial ecosystem supports demand for engineered screening solutions across mineral-processing and specialty material applications. The U.K. and France exhibit strong adoption of mobile screening units used in quarrying and recycling operations. Spain’s demand is driven by infrastructure investments and aggregates production, supported by funding programs intended to improve climate resilience and sustainability.

Customers across Europe typically prioritize equipment efficiency, low emissions, and compliance with stringent environmental regulations. Key growth drivers include the region’s sustainability mandates, which encourage the expansion of recycling facilities and high-efficiency material-separation systems.

Replacement of older diesel-driven fleets with electric and hybrid models also supports market momentum. Technological integration, especially digital monitoring, automated process optimization, and advanced high-frequency screening systems, is increasingly embedded into plant operations across Europe.

Asia Pacific Screening Equipment Market Trends - Infrastructure-Driven Expansion and High-Volume Installations

Asia Pacific is the largest and fastest-expanding regional market for screening equipment, estimated to account for around 41.8% of the market share. Growth is driven by extensive infrastructure pipelines, large-scale mining activity, strong aggregates demand, and cost-competitive manufacturing bases. APAC accounts for the highest installation volumes globally and a growing share of high-capacity, high-spec equipment purchases.

China remains the single largest market in the region, supported by strong domestic manufacturing capacity and extensive use of screening equipment in mining, aggregates, and industrial processing. India shows rapidly accelerating demand driven by major road-building programs, urban-development initiatives, construction-and-demolition recycling, and expanded mineral-processing capacity.

Japan and ASEAN countries maintain a steady demand for high-availability screening solutions used in ports, industrial facilities, and bulk-handling infrastructure, with a preference for equipment offering reliability and strong service coverage.

Growth across APAC is supported by three main factors. Massive infrastructure investment, including highways, smart-city programs, and transportation corridors, continues to drive demand for both mobile and stationary screening systems.

Mining expansion in Australia, Indonesia, and several Southeast Asian countries further boosts the need for large-capacity screening equipment. In addition, the localization of manufacturing and assembly by major OEMs is reducing lead times and lowering costs, making equipment more accessible to regional buyers.

Competitive Landscape

The global screening equipment market is moderately concentrated at the top, with major OEMs dominating high-value installations through broad portfolios and global service networks. Lower tiers remain fragmented, served by regional and specialist manufacturers targeting cost-sensitive and niche applications. Competitive advantage hinges on aftermarket strength, reliability, energy efficiency, and service speed.

Barriers to entry are moderate, with technology and service capabilities reinforcing incumbents. Key strategies include electrification, digitalization, aftermarket expansion, localized manufacturing, lifecycle-value offerings, and bundled service and financing, while mid-tier players focus on price, delivery speed, and customization.

Key Industry Developments

- In March 2025, Sandvik introduced its new fully-electric tracked crushing and screening train, featuring an electric cone crusher paired with an electric screening unit designed to lower fuel consumption and improve onsite efficiency.

- In February 2025, Terex released its next-generation mobile scalping screen with hybrid electric-diesel capability, targeting recycling, construction, and quarry operations needing low-emission equipment.

Companies Covered in Screening Equipment Market

- Metso

- Sandvik

- Terex

- McCloskey

- Astec Industries

- Thyssenkrupp

- Haver & Boecker

- Kleemann

- Komatsu

- Rubble Master

- Eagle Crusher

- CDE Global

- Derrick Corporation

- SMICO Manufacturing

- NAWA Engineers

- IROCK Crushers

- Superior Industries

- MEKA

- SBM Mineral Processing

- Powerscreen

Frequently Asked Questions

The screening equipment market size in 2026 is estimated at US$7.2 Billion.

By 2033, the market value is expected to reach US$11.3 billion.

Major trends include rapid uptake of electrified and hybrid mobile screeners, growing use of high-frequency and sensor-enabled units, expansion of recycling and circular-economy processing lines, and rising aftermarket service contracts as operators emphasize uptime and predictive maintenance.

Vibrating screens (including linear, circular, and banana configurations) represent the leading segment, contributing around 47.2% of the total market revenue due to their high throughput and broad industrial applicability.

The screening equipment market is projected to grow at a CAGR of 6.2% from 2026 to 2033.

The key players include Metso, Sandvik, Terex, McCloskey, and Astec Industries.