- Pharmaceuticals

- Saudi Arabia Pharmaceuticals Market

Saudi Arabia Pharmaceuticals Market Size, Share, Growth, and Forecast, 2026 to 2033

Saudi Arabia Pharmaceuticals Market by Product Type (Prescription Products, Over The Counter (OTC) Products), Disease Area (Cardiovascular Diseases, Diabetes, Oncology / Cancer Treatments, Infectious Diseases, Respiratory Diseases, Others), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Others), Analysis from 2026 to 2033

Saudi Arabia Pharmaceuticals Market Share and Trends Analysis

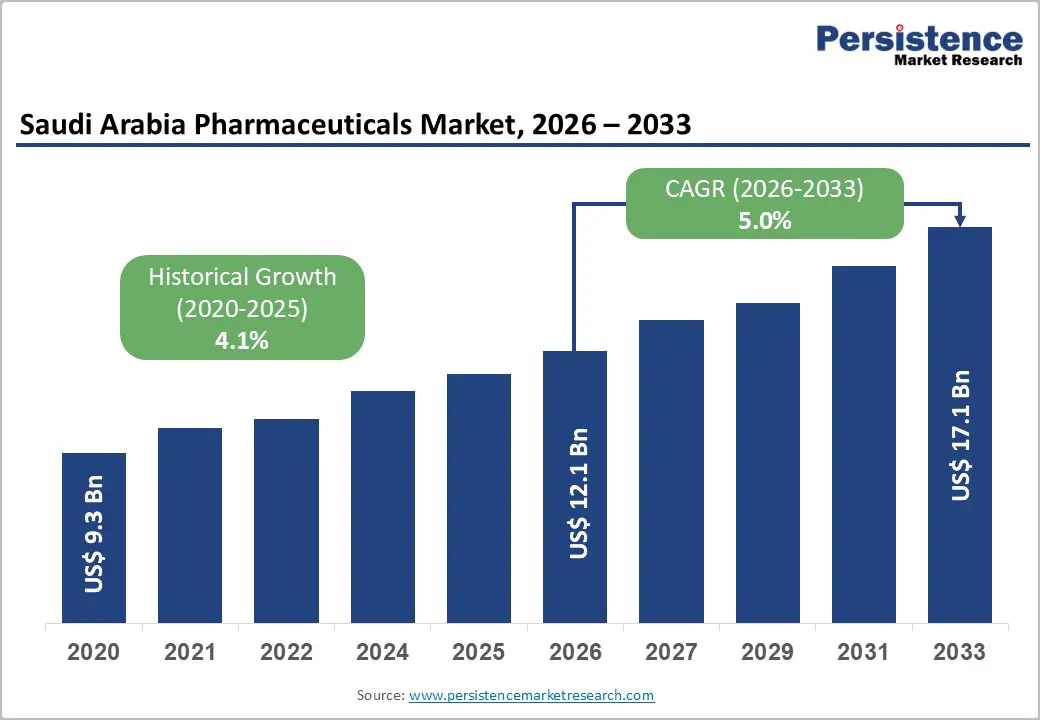

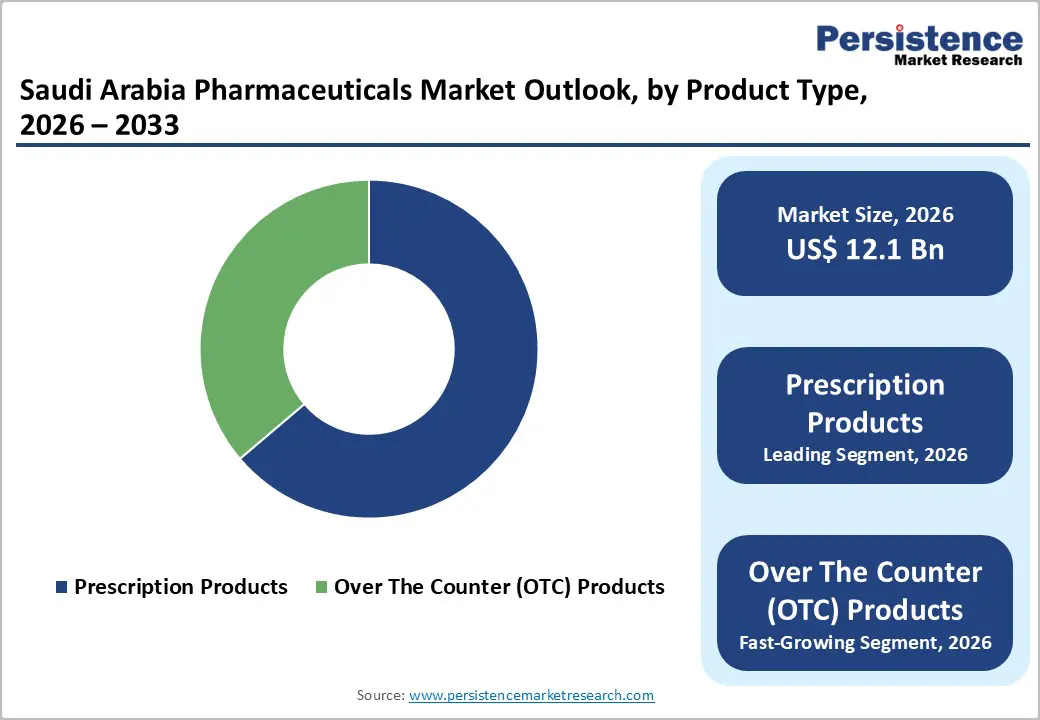

The Saudi Arabia pharmaceuticals market is estimated to grow from US$ 12.1 billion in 2026 to US$ 17.1 billion by 2033. The market is projected to record a CAGR of 5.0% during the forecast period from 2026 to 2033 driven by rising chronic disease prevalence, growing healthcare expenditure, and strong government support under Vision 2030.

Increasing demand for biologics, specialty drugs, and localized manufacturing boosts growth. Expanding hospital infrastructure and insurance coverage further accelerate market development across prescription and specialty therapeutic segments nationwide.

Key Industry Highlights

- Dominant Product Segment: Prescription drugs account for approximately 63.8% share of the Saudi Arabia pharmaceuticals market in 2025, driven by high prevalence of chronic diseases such as cardiovascular disorders and diabetes. Strong hospital demand, specialist therapies, and expanding insurance coverage support continued dominance over OTC products.

- Growth Indicators: Rising burden of chronic and lifestyle diseases, a growing geriatric population, increasing healthcare expenditure under Vision 2030, expanding health insurance coverage, localization of pharmaceutical manufacturing, and strong government regulatory support are key factors driving market growth.

- Market Opportunity: Opportunities include expansion of biologics and biosimilars manufacturing, investment in local API production, growth in specialty and oncology therapies, digital pharmacy platforms, public-private partnerships, and strategic collaborations between multinational pharmaceutical companies and domestic manufacturers to strengthen supply chain resilience.

| Key Insights | Details |

|---|---|

| Saudi Arabia Pharmaceuticals Market Size (2026E) | US$ 12.1 Bn |

| Market Value Forecast (2033F) | US$ 17.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver: Increasing Government Healthcare Expenditure under Vision 2030

The Saudi government’s Vision 2030 framework has made healthcare a strategic priority with substantial public expenditure to strengthen the sector. In 2023, Saudi Arabia allocated $50.4 billion (≈SAR 189.6 billion) to healthcare and social development, representing a significant portion of national spending and underscoring the emphasis on improving healthcare systems and access. Vision 2030 also aims to develop healthcare infrastructure, increase private participation, and improve service quality by investing over $65 billion in healthcare infrastructure, including new facilities and health clusters integrated across the Kingdom. This substantial funding supports increased consumption of pharmaceuticals, broader insurance coverage, expanded hospital capacity, and stronger drug procurement processes, all driving demand for medications.

The government's commitment to healthcare expenditure also aligns with broader public health goals. For example, the Ministry of Health plans to double the number of primary healthcare visits per capita, expand digital healthcare solutions, and advance preventive care programs. By bolstering infrastructure and insurance coverage, the government is deepening pharmaceutical demand across chronic disease segments, including diabetes, cardiovascular conditions, and oncology. The expanded budget also provides room for pharmaceutical policy reforms, technology adoption, and partnerships that further enhance market growth under Vision 2030.

Restraints: Strict Drug Pricing Controls and Regulatory Pressure

Saudi Arabia’s pharmaceutical market is subject to stringent pricing regulations enforced by the Saudi Food and Drug Authority (SFDA) and related government bodies. All pharmaceutical products entering the market undergo a defined pricing evaluation process, which includes technical review, pricing committee assessment, and final approval before reimbursement and procurement listing. This structured regulatory pathway aims to protect patient affordability and control national healthcare spending, but also creates margin compression for pharmaceutical manufacturers operating in the Kingdom. Because prices are tightly overseen, companies often face limitations on setting competitive prices that reflect global market levels, which can discourage investment in high-cost specialty therapies.

In addition, the reliance on imported APIs and high-value drugs exacerbates pricing pressure. Domestic manufacturers currently satisfy only about 20-30% of total pharmaceutical demand by volume, leaving the majority dependent on imported medicines, with regulated margins once approved. While this regulatory environment protects patients and keeps medicines affordable, it constrains growth for multinational and local manufacturers by capping revenue potential and prolonging approval timelines, as part of the pricing committee’s mandate. These pressures can limit the pace at which advanced therapies, such as complex biologics with higher production costs, penetrate the market relative to regions with more flexible pricing regimes.

Opportunity: Expansion of Domestic Biologics and Biosimilars Production

Saudi Arabia is actively supporting the local expansion of biologics and biosimilars production as part of its economic diversification under Vision 2030. Currently, domestic manufacturing meets only about 20-25 % of total pharmaceutical demand by value, indicating a significant opportunity to grow local production, particularly in high-value segments such as biologics and biosimilars. Government initiatives, including incentives for localization, regulatory alignment with global standards, and industrial support programs, are creating fertile ground for investment in biopharmaceutical manufacturing and technology transfer partnerships. The biopharma manufacturing market in Saudi Arabia is valued at approximately USD 1.6 billion and is expected to expand as demand and infrastructure improve.

Local biosimilar production represents a strategic opportunity to address both healthcare needs and economic goals. The Saudi Biotech Strategy aims to significantly increase biosimilar penetration, potentially exceeding 60%, which could reduce drug costs and expand access to advanced therapies across therapeutic areas such as oncology and immunology. By fostering partnerships with multinational companies and offering incentives such as tax relief and procurement preferences, Saudi Arabia is positioning itself not only to reduce import dependency but also to become a regional hub for biopharmaceutical manufacturing. This expansion can generate high-value jobs, enhance supply chain resilience, and support export growth for advanced therapeutic products originating from the Kingdom.

Category-wise Analysis

By Product Type Insights

Prescription pharmaceuticals lead the Saudi Arabian market because the healthcare system emphasizes regulated, clinician-supervised treatment for chronic and complex diseases, which require ongoing medical oversight and follow-up. According to market data, prescription drugs held about 63.8% of the market share in 2025, significantly higher than OTC products, as medicines such as cardiovascular, diabetes, and oncology therapies are dispensed only with physician authorization. The SFDA controls drug approval and distribution to ensure safety, meaning only trained providers can prescribe medications for serious conditions, thereby enlarging the prescription segment. Chronic diseases like diabetes (18.5% prevalence among adults) and hypertension are widespread in Saudi Arabia, necessitating long-term pharmacotherapy that cannot be self-administered. These systemic factors make prescription products the dominant segment.

By Disease Area Insights

Cardiovascular diseases (CVDs) dominate the disease-area share of the Saudi pharmaceuticals market due to their high burden and the need for long-term medication management. Market data indicate that the cardiovascular segment accounts for roughly 28.3% of pharmaceutical demand, more than other therapeutic areas. National health statistics show a significant prevalence of heart and vascular conditions: for adults aged ≥65, CVD prevalence reaches 11%, and overall adult CVD rates stand around 1.6%, with higher rates in older age groups. Moreover, comorbidities such as diabetes and hypertension prevalent in Saudi Arabia increase cardiovascular risk, further boosting demand for heart-related drugs. The combination of demographic risk factors and clinical necessity sustains cardiovascular drugs as the largest therapeutic segment.

Competitive Landscape

The Saudi Arabia pharmaceuticals market is highly competitive, led by domestic manufacturers such as SPIMACO, Tabuk Pharmaceuticals, and Jamjoom Pharma, alongside multinationals like Hikma and Pfizer. Competition centers on pricing strategies, portfolio diversification, biologics expansion, regulatory compliance with SFDA standards, localization initiatives, and strategic hospital and government procurement partnerships.

Key Developments

- In October 2025, Jamjoom Pharma unveiled a new corporate brand identity as part of its strategy to accelerate regional and global expansion. The rebranding reflected the company’s transformation from a regional pharmaceutical manufacturer into a broader healthcare solutions provider with growing international ambitions. The updated visual identity included a redesigned logo and refreshed corporate messaging to better represent innovation, quality, and patient-centric values.

- In September 2025, Bio-Thera Solutions and Jamjoom Pharma announced a strategic partnership to commercialize a secukinumab biosimilar across the Middle East and North Africa (MENA) region. Under the agreement, Bio-Thera granted Jamjoom Pharma exclusive rights to register, market, and distribute the biosimilar in selected MENA countries. Secukinumab is a monoclonal antibody used to treat autoimmune conditions such as psoriasis, psoriatic arthritis, and ankylosing spondylitis.

Companies Covered in Saudi Arabia Pharmaceuticals Market

- Jamjoom Pharma

- Tadawi

- Hikma Pharmaceuticals

- Ameco Pharmaceutical Company

- Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO)

- Modern Pharmaceutical Company (MPC)

- Julphar Saudi Arabia

- Tabuk Pharmaceuticals

- Others

Frequently Asked Questions

The Saudi Arabia pharmaceuticals market is projected to be valued at US$ 12.1 Bn in 2026.

Rising chronic diseases, healthcare spending growth, insurance expansion, and pharmaceutical localization initiatives.

The Saudi Arabia pharmaceuticals market is poised to witness a CAGR of 5.0% between 2026 and 2033.

Biologics expansion, local manufacturing growth, oncology demand, digital pharmacies, strategic partnerships.

Jamjoom Pharma, Tadawi, Hikma Pharmaceuticals, Ameco Pharmaceutical Company, Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO), Modern Pharmaceutical Company (MPC).