- Pharmaceuticals

- S1P Receptor Modulator Drugs Market

S1P Receptor Modulator Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

S1P Receptor Modulator Drugs Market by Drug Type (Fingolimod, Ozanimod, Siponimod, Others), Application (Multiple Sclerosis, Inflammatory Bowel Disease, Psoriasis, Cancer), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026-2033

S1P Receptor Modulator Drugs Market Share and Trends Analysis

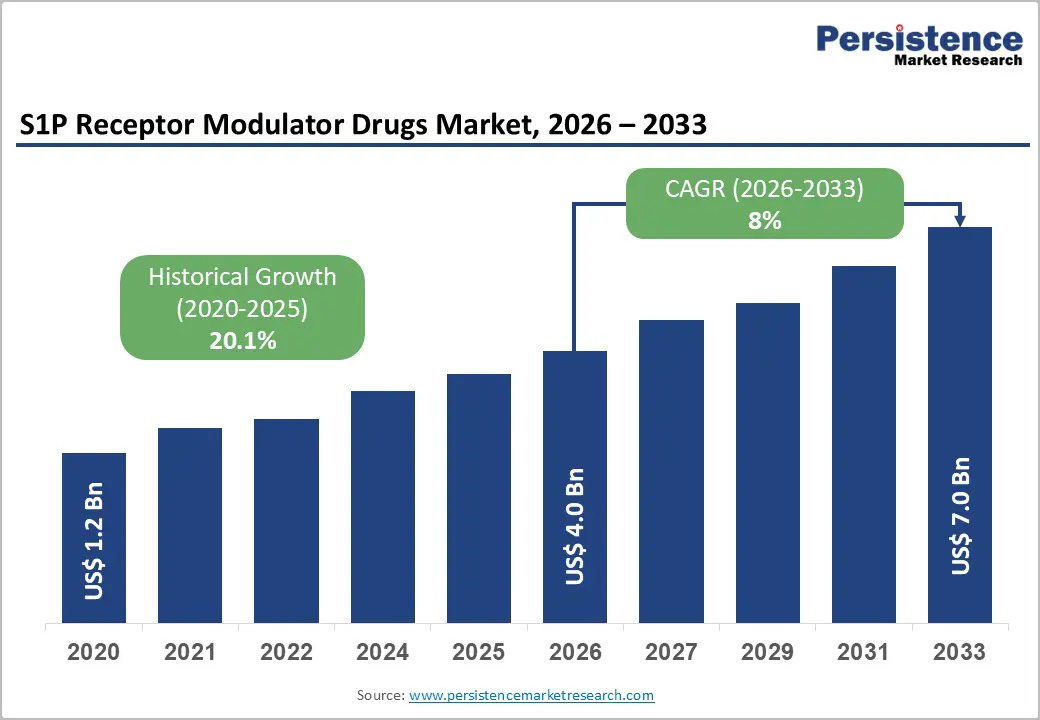

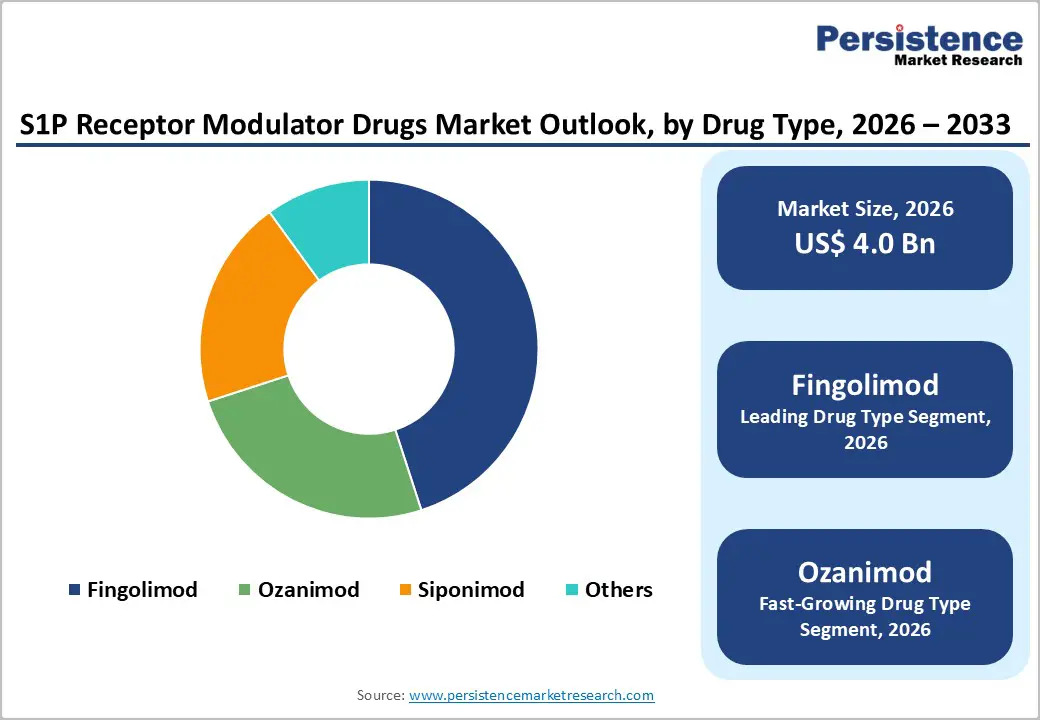

The global S1P receptor modulator drugs market size is likely to be valued at US$ 4.0 billion in 2026, and is projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 8% during the forecast period 2026−2033.

Market expansion is being driven primarily by the rising prevalence of autoimmune disorders, particularly multiple sclerosis (MS). The World Health Organization (WHO) estimates that more than 1.8 million people worldwide are living with MS, which is increasing demand for long-term disease-modifying therapies. Sphingosine (S1P) receptor modulators are gaining clinical preference because they regulate lymphocyte migration and reduce inflammatory activity through targeted immune modulation. As diagnosis rates improve and treatment guidelines continue evolving, demand for advanced oral immunotherapies is strengthening across major healthcare markets. The transition toward oral disease-modifying therapies is further supporting adoption, as patients and clinicians are favoring convenient administration over injectable regimens. Expanding research into additional indications such as inflammatory bowel disease (IBD) and systemic lupus erythematosus is broadening the therapeutic scope of S1P modulators. Regulatory agencies are granting approvals for next-generation molecules with improved safety profiles, which is reinforcing physician confidence and patient adherence. Healthcare expenditure is increasing in emerging economies, supported by expanded insurance coverage and government investment in chronic disease management programs.

Key Industry Highlights

- Drug Type Leadership: Fingolimod is slated to lead with approximately 45% of the revenue share in 2026, with ozanimod likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Application Dominance: MS is poised to be the dominant application with an estimated 75% revenue share in 2026, while IBD is expected to register the highest 2026-2033 CAGR.

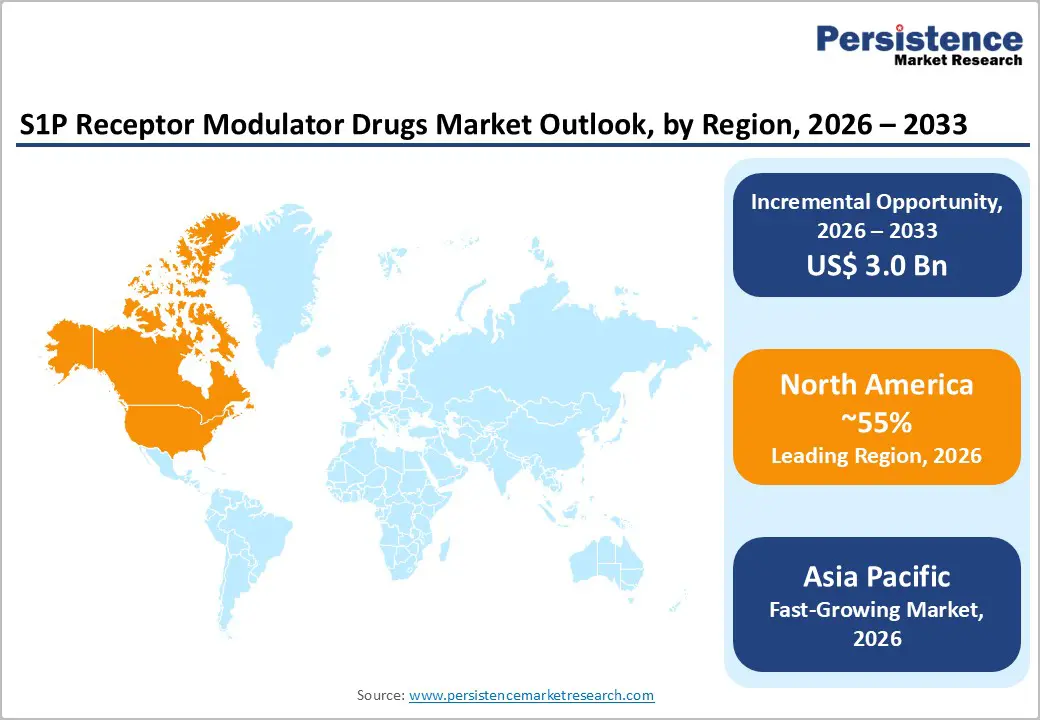

- Dominant Region: North America is expected to command about 55% of the market share in 2026, owing to advanced healthcare infrastructure and rapid regulatory pathways.

- Fastest-growing Market: The Asia Pacific market is poised to be the fastest-growing during the 2026-2033 forecast period, powered by the rapidly expanding healthcare infrastructure in China and India.

| Report Attribute | Details |

|---|---|

|

S1P Receptor Modulator Drugs Market Size (2026E) |

US$ 4.0 Bn |

|

Market Value Forecast (2033F) |

US$ 7.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

20.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Multiple Sclerosis and Autoimmune Disorders

The rising prevalence of multiple sclerosis serves as a key growth driver for the S1P receptor modulator drugs market. Healthcare providers increasingly recognize MS cases across broader patient demographics, including younger adults and diverse ethnic groups. This trend reflects improved diagnostic capabilities through advanced magnetic resonance imaging (MRI) techniques and greater physician awareness. Patients now seek more effective long-term management options beyond conventional treatments such as interferons or glatiramer acetate. S1P receptor modulators address this need by selectively targeting immune cell trafficking, which helps prevent inflammatory cell migration into the central nervous system. Pharmaceutical companies have opportunities to expand their treatment portfolios and capture larger market segments.

Clinicians often favor S1P receptor modulators for their convenient oral administration and demonstrated ability to modify disease progression in relapsing-remitting multiple sclerosis (RRMS). These agents fit well into existing treatment algorithms, particularly for patients who experience breakthrough disease activity on first-line therapies. Health systems can benefit from fewer hospitalizations and improved patient quality of life, which supports favorable reimbursement decisions. Organizations should prioritize strategic positioning in this therapeutic class, as autoimmune disease management continues to shift toward precision immunology approaches. This evolution can create more sustainable revenue streams for companies that invest in next-generation formulations and expanded indications beyond neurology.

Cardiovascular Safety Concerns and Monitoring Requirements

S1P modulators require structured cardiovascular monitoring protocols that are limiting broad clinical uptake. Regulatory authorities mandate observation for approximately six hours after the first dose to detect potential cardiac effects such as bradycardia and atrioventricular conduction delay. Physicians are conducting baseline cardiac evaluations, including electrocardiograms (ECGs), prior to treatment initiation. Patients with recent myocardial infarction, unstable angina, cerebrovascular events, or pre-existing conduction abnormalities are often excluded from therapy. These safety precautions are requiring coordination among neurologists, cardiologists, and primary care providers, which is increasing operational complexity within hospital and outpatient settings. As a result, workflow constraints are influencing prescribing decisions in high-volume clinical environments.

Ongoing monitoring requirements are extending beyond initial dosing. Clinicians are performing periodic ophthalmologic assessments to screen for complications such as macular edema and posterior reversible encephalopathy syndrome. Primary care practitioners are often demonstrating limited familiarity with this drug class, which is contributing to hesitancy in managing long-term MS therapy. Consequently, prescribing patterns are remaining concentrated among specialists, thereby restricting broader patient access in community care settings. Pharmaceutical companies are responding by developing physician education initiatives and simplified risk management frameworks. Strengthening prescriber training and streamlining monitoring pathways will be essential to expand utilization while maintaining safety compliance.

Combination Therapy Approaches and Personalized Medicine Integration

Emerging treatment strategies are increasingly emphasizing combination regimens and biomarker-guided patient selection, which are creating strategic opportunities for S1P modulators within personalized medicine frameworks. Clinical researchers are evaluating these agents alongside B-cell–depleting therapies such as anti-cluster of differentiation 20 (anti-CD20) monoclonal antibodies to improve disease stabilization in complex multiple sclerosis (MS) cases. Parallel pharmacogenomic studies are identifying genetic markers associated with therapeutic response and adverse event risk. These data-driven insights are enabling clinicians to stratify patients earlier and optimize treatment sequencing. Pharmaceutical companies that are developing companion diagnostics and precision dosing algorithms are aligning product strategies with increasingly individualized care pathways. As clinical guidelines continue evolving toward targeted intervention, integration of molecular profiling into prescribing decisions will be strengthening competitive differentiation.

Digital health ecosystems are further enhancing therapeutic value by supporting adherence tracking and remote symptom monitoring through mobile applications. Neurology specialists are adopting integrated care models because they improve longitudinal outcome measurement and streamline follow-up management. Real-world evidence platforms are capturing treatment durability and safety performance across diverse patient populations. Organizations that are investing in interoperable data systems are positioning themselves to demonstrate value in outcomes-based reimbursement frameworks. Strategic partnerships with digital health developers and genomics firms are enabling access to new patient cohorts and advanced analytics capabilities. This convergence of precision medicine and digital infrastructure is supporting sustainable growth while reinforcing clear clinical positioning in a competitive autoimmune treatment landscape.

Category-wise Analysis

Drug Type Insights

Fingolimod is anticipated to capture an estimated 45% of the S1P receptor modulator market revenue share in 2026. As one of the earliest agents in this class to receive regulatory approval, it has established a substantial clinical footprint in MS management. Its demonstrated ability to reduce relapse rates and delay disease progression has supported sustained adoption among neurologists and multidisciplinary care teams. Long-term safety and efficacy data have strengthened prescriber confidence when compared with recently introduced therapies. In addition, ongoing clinical investigations are evaluating its utility in additional autoimmune conditions, which may broaden its therapeutic scope. This combination of established evidence and potential label expansion is reinforcing its continued commercial relevance through the forecast period.

Ozanimod is expected to emerge as the fastest-growing drug segment between 2026 and 2033. As a newer S1P receptor modulator, it has gained regulatory approvals for both multiple sclerosis and inflammatory bowel disease, thereby expanding its clinical reach beyond neurology into gastroenterology. Healthcare providers are valuing its selective receptor targeting profile, which is offering effective immune modulation with improved tolerability relative to earlier-generation agents. This dual-indication positioning is enhancing prescribing flexibility across specialties. Regulatory clearances in multiple therapeutic areas are already supporting revenue expansion, while ongoing clinical trials are exploring further indications. As evidence continues to accumulate, ozanimod is likely to strengthen its competitive standing within the evolving autoimmune treatment landscape.

Application Insights

Multiple sclerosis is projected to account for approximately 75% of S1P receptor modulator market share in 2026. High global MS prevalence is generating sustained demand for long-term disease-modifying therapies. These agents are demonstrating strong clinical efficacy in reducing relapse rates and slowing disability progression, which is supporting their inclusion in neurologist-led treatment algorithms. Physicians are increasingly prescribing S1P modulators for patients who experience breakthrough disease activity despite first-line injectable therapies. Ongoing clinical research is refining dose optimization strategies and evaluating combination regimens tailored to specific MS phenotypes. This focused therapeutic alignment is reinforcing the segment’s dominant contribution to overall market revenue.

Inflammatory bowel disease is expected to be the fastest-growing application segment through 2033. Rising incidence rates are expanding the population of patients who require advanced therapeutic options beyond conventional immunosuppressants. S1P modulators are demonstrating targeted immune regulation that reduces intestinal inflammation and supports sustained remission. Gastroenterologists are increasingly considering these therapies for moderate-to-severe cases that show inadequate response to biologic agents or small-molecule treatments. Regulatory approvals in ulcerative colitis and related indications are validating their role within updated clinical guidelines. Pharmaceutical companies are advancing additional trials to expand indication breadth, positioning IBD as a strategic growth avenue that diversifies revenue beyond neurology-focused applications.

Distribution Channel Insights

Hospital pharmacies are predicted to lead with nearly 60% of the revenue share in 2026, reflecting high prescription volumes generated within specialized care settings. Hospitals function as primary treatment centers for patients with complex autoimmune disorders who require coordinated, multidisciplinary management. Neurologists, gastroenterologists, and rheumatologists are often initiating therapy in hospital environments where structured first-dose monitoring and cardiovascular assessments can be conducted under supervision. These facilities are integrating electronic health records (EHRs) with laboratory monitoring systems to ensure safety protocol adherence and streamline reimbursement documentation. Dedicated pharmacy teams are providing medication counseling, coordinating follow-up evaluations, and managing transitions between inpatient and outpatient care. This integrated infrastructure is supporting compliance with regulatory requirements while reinforcing hospital pharmacies’ dominant distribution role.

Retail pharmacies are expected to represent the fastest-growing distribution segment between 2026 and 2033. Community-based outlets are improving accessibility for patients managing chronic autoimmune conditions, particularly those who face geographic or scheduling constraints. Convenient locations and extended operating hours are supporting consistent prescription refills, which are essential for maintaining therapeutic continuity. Retail pharmacists are offering adherence guidance, side-effect counseling, and coordination with prescribing specialists when dose adjustments are required. As specialty medication distribution models evolve, retail pharmacy networks are expanding their capacity to manage complex therapies. This shift is broadening patient reach and contributing to sustained growth in outpatient dispensing channels.

Regional Insights

North America S1P Receptor Modulator Drugs Market Trends

North America is estimated to secure around 55% of the S1P receptor modulator drugs market value in 2026, on the back of an advanced healthcare infrastructure and efficient regulatory processes. The United States is leading regional performance due to broad insurance coverage for specialty pharmaceuticals under Medicare Part D and commercial health plans. This coverage structure is facilitating patient access to oral disease-modifying therapies. The U.S. Food and Drug Administration (FDA) has been granting approvals for key agents including fingolimod, siponimod, ozanimod, and ponesimod, which has accelerated therapeutic availability relative to other regions. Academic medical centers and community neurology practices are actively incorporating these treatments into clinical pathways. Physicians are favoring oral regimens for newly diagnosed multiple sclerosis patients who prefer alternatives to injectable therapies, which is reinforcing regional demand.

Healthcare providers in North America are leveraging robust real-world evidence systems and structured post-marketing surveillance programs to refine treatment guidelines and support reimbursement negotiations. The FDA Priority Review and Breakthrough Therapy designations are expediting development timelines for emerging candidates, thereby sustaining innovation momentum. Pharmaceutical companies are investing in research programs that explore expanded indications beyond neurology, including gastroenterology and rheumatology applications. Venture capital funding is strengthening clinical development pipelines and supporting biotechnology partnerships. Strategic collaboration with payers and specialty pharmacy networks is improving market penetration and adherence management. As treatment strategies increasingly incorporate combination regimens and biomarker-guided therapy selection, North America is expected to maintain leadership in clinical adoption and product innovation within the S1P receptor modulator market.

Europe S1P Receptor Modulator Drugs Market Trends

Europe is likely to represent the second-largest market for S1P receptor modulator drugs in 2026 and through 2033, supported by structured regulatory systems and comprehensive public healthcare coverage. The European Medicines Agency (EMA) manages centralized approval pathways, enabling coordinated market entry across multiple member states. Germany, the U.K., France, Italy, and Spain are generating the majority of regional demand through established neurology networks and broad reimbursement frameworks. Health technology assessment bodies are conducting detailed cost-effectiveness analyses that directly influence pricing and coverage decisions. These evaluations are shaping access conditions and creating reference benchmarks across national markets. As a result, manufacturers are aligning pricing strategies with value-based evidence requirements to secure sustainable reimbursement positioning.

European healthcare systems are benefiting from harmonized clinical guidelines and well-maintained patient registries that support real-world data collection. These registries are validating therapeutic effectiveness and informing updated treatment recommendations. National pricing negotiations and innovative reimbursement mechanisms, including outcomes-based agreements, are expanding access for patients with refractory autoimmune conditions. Demographic trends, including population aging, are increasing autoimmune disease incidence and reinforcing long-term demand. Organizations that are prioritizing collaboration with academic research consortia and digital health providers are accelerating development of next-generation compounds. Integration of remote monitoring tools within prescribing workflows is enhancing treatment adherence and strengthening value demonstration in payer negotiations.

Asia Pacific S1P Receptor Modulator Drugs Market Trends

Asia Pacific is projected to be the fastest-growing 2026-2033 market for S1P receptor modulator drugs, fueled by expanding healthcare infrastructure and rising treatment accessibility. China and India are increasing public and private healthcare expenditure, which is enabling broader adoption of specialty therapies. China is extending advanced diagnostic capabilities into tier-2 and tier-3 cities, thereby improving early detection of autoimmune disorders and expanding eligible patient pools. Japan is maintaining stable access through its National Health Insurance system, which provides structured reimbursement for approved therapies. India is demonstrating long-term potential as government initiatives such as Ayushman Bharat are gradually expanding coverage to include higher-cost specialty medications. ASEAN economies, led by Thailand, Indonesia, Malaysia, and the Philippines, are contributing through growth in private insurance, medical tourism, and increasing demand for advanced treatment options.

The region is also functioning as a critical pharmaceutical manufacturing base. Production facilities across Asia Pacific are supplying active pharmaceutical ingredients and finished dosage forms at competitive costs, reinforcing global supply chain integration. China’s National Medical Products Administration (NMPA) is accelerating review timelines through participation in the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) and alignment with global regulatory standards. Multinational pharmaceutical companies are forming partnerships with regional distributors and contract manufacturing organizations to optimize commercialization strategies. Investments in physician education programs and patient support initiatives are strengthening clinical familiarity and adherence. By tailoring engagement models to local healthcare systems, organizations are positioning themselves to capture sustained growth across this high-potential region.

Competitive Landscape

The global S1P receptor modulator drugs market structure is moderately concentrated. The market landscape is headlined by major pharmaceutical companies such as Novartis, Bristol Myers, Johnson & Johnson, Otsuka Pharmaceutical, and Biogen, which together control approximately 35–40% of total market share. These organizations are benefiting from established product portfolios, global commercialization capabilities, and strong regulatory expertise. Market structure is gradually shifting as exclusivity periods for first-generation therapies expire in several jurisdictions. Loss of patent protection is enabling generic manufacturers to enter key markets, which is increasing pricing pressure and expanding treatment accessibility. This transition is influencing procurement decisions, particularly in cost-sensitive healthcare systems.

Originator companies are advancing next-generation compounds that emphasize selective receptor targeting and improved safety profiles. Clinical pipelines are including combination regimens and novel formulations designed for patients with suboptimal response to existing therapies. This parallel evolution of lower-cost generics and differentiated premium agents is reshaping competitive positioning. Payers are increasingly favoring cost-effective alternatives where therapeutic equivalence is demonstrated, while specialists are adopting innovative molecules that address unmet clinical needs. The interaction between affordability and clinical differentiation is creating opportunities for market share redistribution.

Key Industry Developments

- In February 2026, Everest Medicines received approval from China’s NMPA for the treatment of adults with moderately to severely active ulcerative colitis, making it one of the first oral S1P receptor modulators authorized for this indication in the country. The approval is expected to broaden therapeutic options for IBD patients and support future commercial expansion in China’s specialty drugs market.

- In December 2025, according to a study published in The Lancet Gastroenterology & Hepatology, etrasimod significantly improves both induction and maintenance of remission in patients with ulcerative colitis, demonstrating clinical benefit as an oral S1P receptor modulator in IBD treatment. The findings support etrasimod’s potential as a valuable therapeutic option for achieving sustained disease control in moderate-to-severe cases.

- In September 2025, Zydus Lifesciences entered an exclusive licensing and supply agreement with Synthon BV for a generic version of Ozanimod capsules (Zeposia®), targeting the U.S. market for relapsing forms of multiple sclerosis. This partnership advances affordable access to the sphingosine 1 phosphate receptor modulator, also approved for ulcerative colitis (UC).

Companies Covered in S1P Receptor Modulator Drugs Market

- Novartis AG

- Bristol Myers Squibb Company

- Johnson & Johnson

- Otsuka Pharmaceutical Co., Ltd.

- Biogen Inc.

- Merck KGaA

- Arena Pharmaceuticals (Pfizer)

- Celgene Corporation (Bristol Myers Squibb)

- Idorsia Pharmaceuticals Ltd.

- Galapagos NV

- Aslan Pharmaceuticals

- Sanofi S.A.

Frequently Asked Questions

The global S1P receptor modulator drugs market is projected to reach US$ 4.0 billion in 2026.

Rising autoimmune disease prevalence, particularly multiple sclerosis, is fueling the demand for effective oral disease-modifying therapies with proven relapse reduction and driving the market.

The market is poised to witness a CAGR of 8% from 2026 to 2033.

Emerging indications such as atopic dermatitis and UC, plus healthcare infrastructure strengthening in India, China, and ASEAN, are resulting in substantial growth potential.

Novartis AG, Bristol Myers Squibb Company, Johnson & Johnson, Otsuka Pharmaceutical Co., Ltd. and Biogen Inc. are some of the key players in the market.