- Pharmaceuticals

- Regenerative Dentistry Market

Regenerative Dentistry Market Size, Share, and Growth Forecast 2026 - 2033

Regenerative Dentistry Market by Product Type (Biomaterials, Stem Cell-Based Products, Tissue Engineering Products, Growth Factors), Application (Periodontal Regeneration, Endodontic Regeneration, Bone Regeneration, Tooth Regeneration), End-user (Dental Clinics, Hospitals, Academic & Research Institutes), by Regional Analysis, 2026 - 2033

Regenerative Dentistry Market Share and Trends Analysis

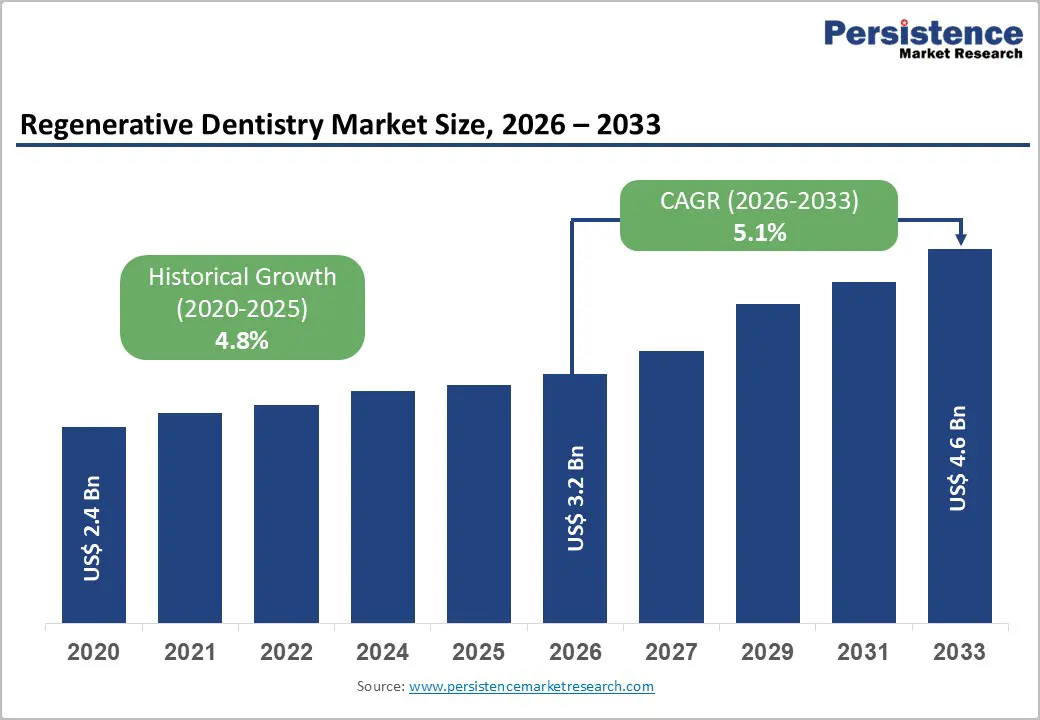

The global regenerative dentistry market size is expected to be valued at US$ 3.2 billion in 2026 and projected to reach US$ 4.6 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This steady expansion is primarily driven by the rising global prevalence of periodontal diseases, the increasing geriatric population requiring advanced dental care solutions, and continuous innovations in biomaterials and tissue engineering technologies. The market is benefiting from growing patient preference for minimally invasive regenerative procedures over traditional interventional treatments, coupled with expanding applications of stem cell therapies in dental restoration. According to the World Health Organization (WHO), oral diseases affect nearly 3.5 billion people globally, creating substantial demand for advanced regenerative solutions that offer better functional outcomes and improved quality of life for patients suffering from tooth loss and periodontal deterioration.

Key Industry Highlights:

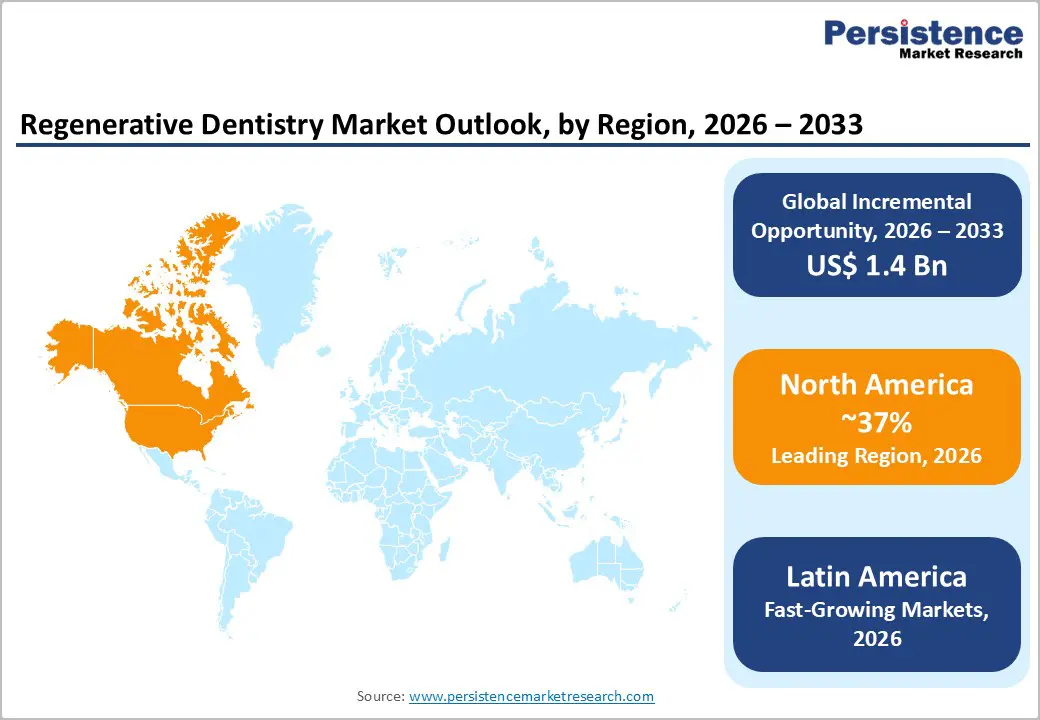

- Regional Leadership: North America is the leading region in the regenerative dentistry market, capturing about 37% share in 2025, supported by advanced dental infrastructure, high prevalence of periodontal and tooth-loss conditions, robust private insurance coverage for many restorative procedures, and the presence of major industry players and academic research hubs driving adoption of cutting-edge regenerative technologies.

- Fast-growing Region: Latin America is expected to be the fastest-growing regional market, driven by a rise in middle-income population, increasing demand for cosmetic and implant dentistry, and expanding dental tourism in countries such as Brazil, Mexico, and Costa Rica, where clinics are increasingly adopting biomaterials and regenerative protocols to deliver premium services at competitive prices.

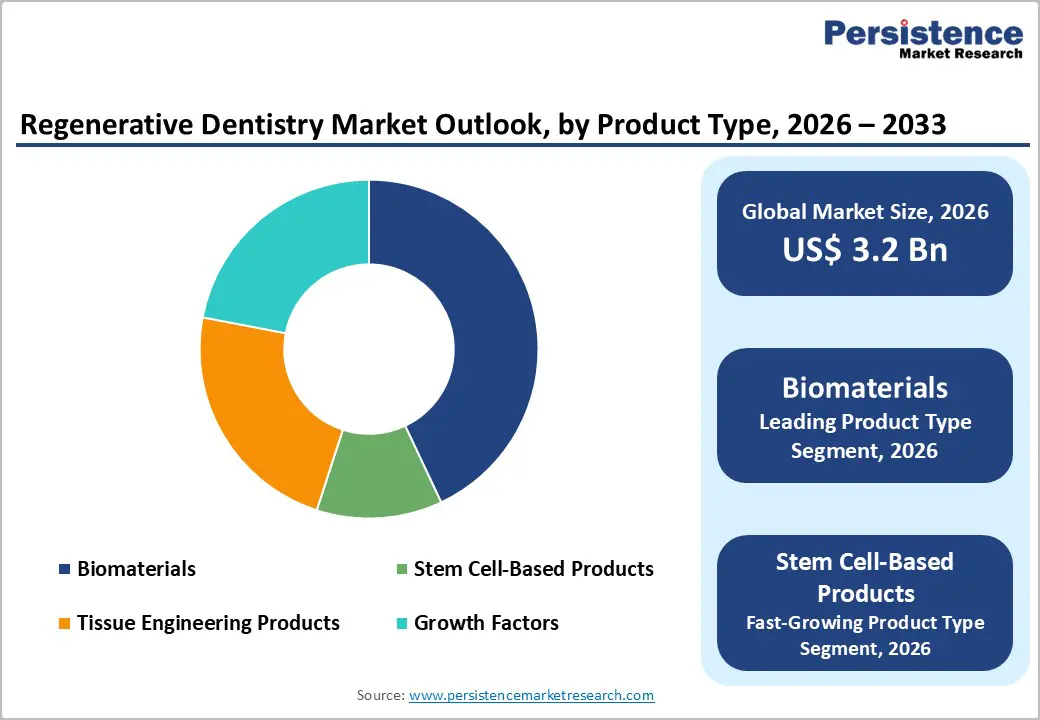

- Leading Product: In the product landscape, biomaterials remain the dominant category with an estimated 43% share in 2025, underpinned by their integral role in bone grafting, guided bone regeneration, and periodontal regeneration, with companies such as Geistlich Pharma AG, Dentsply Sirona, Zimmer Biomet, and Collagen Matrix pioneering evidence-based solutions with proven long-term clinical outcomes.

| Key Insights | Details |

|---|---|

| Regenerative Dentistry Market Size (2026E) | US$ 3.2 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Drivers - Rising Prevalence of Periodontal Diseases Fueling Demand for Regenerative Solutions

The increasing global burden of periodontal diseases represents a fundamental driver propelling the regenerative dentistry market forward. Severe periodontal diseases affect more than 1 billion cases worldwide according to published epidemiological research, with periodontitis ranking among the most common chronic conditions globally. The condition leads to progressive destruction of supporting dental tissues, including gingiva, periodontal ligament, and alveolar bone, ultimately resulting in tooth loss if left untreated. Regenerative dentistry offers advanced therapeutic approaches, including guided tissue regeneration, bone grafting procedures, and application of enamel matrix derivatives that stimulate natural tissue repair processes. Long-term clinical studies, including those from the University of Bern, School of Dental Medicine, have demonstrated clinical success rates exceeding 90% for periodontal regeneration procedures using advanced biomaterials over mean follow-up periods of around 10 years, reinforcing clinician confidence in regenerative protocols and driving higher adoption in specialist practices.

Restraints - High Treatment Costs and Limited Reimbursement Coverage Restricting Market Penetration

The substantial financial burden associated with regenerative dental procedures represents a major restraint limiting widespread adoption, especially in low- and middle-income populations. Advanced regenerative treatments involving bone graft substitutes, barrier membranes, growth factors, or stem cell therapies often cost in the range of US$ 2,000-5,000 per site or tooth, significantly higher than conventional restorative options such as basic fixed prostheses. Many public and private insurance schemes either do not reimburse regenerative procedures or offer only partial coverage, categorizing them as elective or aesthetic rather than essential medical interventions. In markets where out-of-pocket expenditure constitutes a high share of total health spending, patients may opt for lower-cost, non-regenerative alternatives such as extractions and removable dentures. The cost of specialized biomaterials, the need for advanced surgical skills, and multiple clinical visits further compound economic barriers and slow penetration of regenerative solutions in broader patient segments.

Regulatory Complexity and Lengthy Approval Processes Hindering Innovation

The stringent regulatory landscape governing regenerative dental products also constrains market growth, particularly for smaller innovators. Biomaterials, tissue-engineered constructs, and stem cell-based products must pass rigorous preclinical and clinical evaluation to demonstrate safety, biocompatibility, and long-term performance. In the European Union, the Medical Device Regulation (EU) 2017/745 (MDR) has tightened requirements for dental materials and devices, including comprehensive clinical evaluation, traceability, and post-market surveillance, increasing the cost and duration of obtaining CE marking. In the United States, the U.S. Food and Drug Administration (FDA) oversees regenerative products through medical device, biologic, or combination product pathways, often involving complex premarket approval or 510(k)/de novo procedures. These frameworks, while essential for patient safety, prolong time-to-market and require substantial investment in regulatory, quality, and clinical capabilities. The result can be slower commercialization of novel regenerative technologies and reduced ability of small and mid-sized companies to compete with large, well-capitalized players.

Opportunities - Advancements in Stem Cell Technologies Opening New Therapeutic Frontiers

Stem cell-based regenerative dentistry is emerging as one of the most promising opportunities, with the potential to transform treatment paradigms for a range of oral conditions. Dental stem cells derived from dental pulp, periodontal ligament, apical papilla, and exfoliated deciduous teeth exhibit mesenchymal properties and the capacity to differentiate into odontoblast-like, osteoblast-like, and other cell types relevant for tissue regeneration. Peer-reviewed studies, including those indexed on PubMed, have reported successful regeneration of pulp-like tissue and periodontal structures using dental-derived mesenchymal stem cells in preclinical and early clinical settings.

The American Academy of Pediatric Dentistry (AAPD) has issued a policy on using harvested dental stem cells, recognizing their potential but also emphasizing current limitations and the need for more evidence. Globally, tooth and dental stem cell banking services are expanding, allowing parents and patients to cryopreserve cells for potential future use. As regulatory frameworks around cell-based therapies evolve and more robust clinical data emerge, companies focusing on stem cell platforms, cell-scaffold constructs, and cell-derived products are well-positioned to leverage high-value, differentiated growth opportunities within regenerative dentistry.

Integration of Digital Technologies and 3D Bioprinting Revolutionizing Treatment Approaches

The integration of digital dentistry with regenerative medicine and 3D bioprinting offers substantial value creation opportunities for market participants. Advances in 3D bioprinting enable the fabrication of customized scaffolds that replicate the microarchitecture and mechanical properties of native bone or periodontal tissues, thereby improving cell attachment, vascularization, and tissue integration. Digital workflows using cone-beam computed tomography (CBCT) and CAD/CAM technologies allow clinicians to virtually plan regenerative procedures, design patient-specific grafts or membranes, and optimize implant positioning in relation to regenerated bone. The broader tissue engineering and 3D printing markets have already shown strong growth, with dental applications becoming an increasingly important segment due to high aesthetic and functional expectations. Emerging materials incorporating bioactive molecules, controlled-release growth factors, and antibacterial agents further enhance healing and reduce complications. Companies that invest in integrated digital-regenerative solutions, develop validated digital planning protocols, and collaborate with dental laboratories and clinics on customized scaffold production can differentiate their offerings and tap into premium, technology-driven subsegments of the regenerative dentistry market.

Category-wise Analysis

Product Type Insights

Biomaterials dominate the regenerative dentistry market with an estimated 43% share in 2025, reflecting their role as the backbone of most regenerative procedures. This segment includes bone graft materials (autografts, allografts, xenografts, and synthetic alloplasts), collagen membranes for guided bone and tissue regeneration, barrier films, and bioactive materials such as bioactive glass. Companies such as Geistlich Pharma AG have become global benchmarks in regenerative biomaterials, with products like collagen-based grafts and membranes supported by more than 100 scientific publications and millions of clinical applications worldwide.

Dentsply Sirona offers solutions such as the Symbios line of bone graft and membrane products, while Zimmer Biomet, BioHorizons, and Collagen Matrix also maintain robust biomaterial portfolios. The dominance of biomaterials is underpinned by several factors: broad clinical applicability across periodontal, implant, and oral surgery procedures; relatively clear regulatory pathways; strong evidence base for many established products; and continuous incremental improvements in handling characteristics and biological performance.

Application Insights

Periodontal regeneration is the leading application segment, accounting for an estimated 38% share of the regenerative dentistry market in 2025. Severe periodontitis is highly prevalent, affecting roughly 11% of the global adult population according to large-scale epidemiological assessments, which translates into hundreds of millions of affected individuals. Periodontal regenerative procedures aim to restore the lost periodontal attachment apparatus, including cementum, periodontal ligament, and alveolar bone. Clinically, this is achieved through combinations of bone grafts, enamel matrix derivatives, guided tissue regeneration membranes, and sometimes biologics like growth factors. The European Federation of Periodontology (EFP) and other professional bodies have published consensus reports and guidelines supporting regenerative techniques in well-selected defects, with long-term clinical data indicating stable gains in clinical attachment and radiographic bone fill. Products such as Straumann Emdogain (enamel matrix derivative) have been used in more than 1 million patients worldwide, with follow-up data extending to 10 years in some cohorts. Rising awareness of the systemic links between periodontitis and conditions like diabetes and cardiovascular disease is also encouraging more proactive management of periodontal health, thereby supporting continued growth in periodontal regeneration procedures.

End-user Insights

Dental clinics represent the dominant end-user group, with an estimated about 48% market share in 2025. These include private general practices, group practices, specialist periodontal and implantology clinics, and oral surgery centers. A significant proportion of bone grafting, soft tissue grafting, and periodontal regenerative procedures is performed in outpatient dental clinic environments. Markets such as North America and Europe have high dentist-to-population ratios and a well-established culture of private dental care, which accelerates adoption of advanced regenerative products in clinics. The North American dental services market, valued at well over US$ 200 billion in the mid-2020s, underscores the scale of the addressable customer base for regenerative materials and technologies. Dental clinics seek solutions that are easy to use chairside, compatible with minimally invasive techniques, and supported by training and education programs. Leading manufacturers frequently run continuing education courses, hands-on workshops, and digital learning platforms to help clinicians incorporate regenerative protocols into daily practice. Hospitals and academic & research institutes also contribute meaningfully, but clinics remain the primary deployment setting for commercial regenerative dentistry products.

Regional Insights

North America Regenerative Dentistry Market Trends and Insights

North America leads the regenerative dentistry market due to its advanced healthcare infrastructure, strong adoption of innovative dental technologies, and high awareness of oral health treatments. The region benefits from significant investments in regenerative medicine research, particularly in areas such as stem cell therapy, biomaterials, and tissue engineering for dental applications. Increasing prevalence of periodontal diseases, tooth loss, and aging populations is also driving demand for regenerative dental procedures. Dental clinics and hospitals across the United States and Canada are increasingly integrating regenerative techniques such as bone grafting, guided tissue regeneration, and growth factor-based therapies to restore dental tissues and improve treatment outcomes. Additionally, strong academic research networks and collaborations between dental institutions and biotechnology firms support the development of new regenerative solutions. Favorable reimbursement frameworks, high healthcare spending, and the presence of well-established dental product manufacturers further strengthen the region’s leadership. As patients increasingly seek minimally invasive and long-lasting dental restoration solutions, regenerative dentistry technologies are gaining wider clinical adoption across North America.

Asia Pacific Regenerative Dentistry Market Trends and Insights

Asia Pacific is emerging as a significant growth region in the regenerative dentistry market due to improving healthcare infrastructure, rising dental awareness, and increasing demand for advanced oral treatments. Rapid urbanization, growing disposable incomes, and expanding middle-class populations in countries such as China, India, Japan, and South Korea are encouraging patients to seek modern dental procedures, including regenerative therapies for periodontal disease, bone loss, and tooth restoration. The region is also witnessing a steady rise in dental disorders caused by changing lifestyles, high sugar consumption, and aging populations, which is further boosting demand for regenerative dental solutions. Governments and private healthcare providers are investing in dental research, clinical training, and advanced treatment facilities, supporting the adoption of biomaterials, tissue engineering techniques, and stem-cell-based dental therapies. Additionally, the rapid expansion of dental clinics, dental tourism, and academic research centers is strengthening the regional market. As access to specialized dental care continues to improve, regenerative dentistry technologies are expected to gain broader acceptance across the Asia Pacific region.

Competitive Landscape

The regenerative dentistry market is characterized by a competitive landscape with the presence of established dental product manufacturers, biomaterial developers, and emerging biotechnology firms focused on regenerative therapies. Companies compete primarily through innovation in biomaterials, stem-cell technologies, growth factors, and tissue engineering solutions designed to restore dental tissues and improve clinical outcomes. Continuous investments in research and development are driving the introduction of advanced regenerative materials, minimally invasive treatment techniques, and improved scaffold technologies for bone and periodontal regeneration. Strategic collaborations between dental technology firms, biotechnology companies, and academic research institutions are also accelerating product development and commercialization of new regenerative solutions.

Key Developments:

- In October 2025, TBS Dental launched the Master Restorative Kit, a comprehensive dental instrumentation system developed in collaboration with Neal Patel and introduced at DS World 2025 in Las Vegas. The kit was designed to streamline crown, bridge, and implant restorative procedures by providing a complete workflow solution in a single system.

- In April 2025, Convergent Dental launched Solea Perioguide, a next-generation minimally invasive periodontal treatment designed for use with the Solea All-Tissue Dental Laser. The new application enabled safe, effective, and efficient periodontal therapy without the need for sutures and with minimal post-operative discomfort.

- In March 2025, Solventum partnered with SprintRay to develop and commercialize high-quality, permanent same-day dental restorations using advanced chairside 3D printing technology. The collaboration combined Solventum’s expertise in dental material science with SprintRay’s 3D printing ecosystem to enable dentists to produce crowns, inlays, and onlays directly in the clinic during a single visit.

Companies Covered in Regenerative Dentistry Market

- Straumann Group

- Dentsply Sirona

- 3M

- Henry Schein

- Geistlich Pharma AG

- Zimmer Biomet Holdings

- Envista Holdings

- Ivoclar Vivadent AG

- BioHorizons

- Septodont Holding

- Integra LifeSciences

- Collagen Matrix

- Others

Frequently Asked Questions

The global regenerative dentistry market is expected to be valued at US$ 3.2 billion in 2026, reflecting steady growth supported by rising periodontal disease prevalence, increasing geriatric populations, and ongoing innovation in biomaterials, tissue engineering, and minimally invasive regenerative techniques.

Key demand drivers include the high global burden of periodontal disease affecting hundreds of millions of adults, growing awareness of oral-systemic health links, demographic aging with more than 2 billion people aged 60+ projected by mid-century, and technological advances in biomaterials, stem cells, and 3D bioprinting that improve clinical outcomes and expand the range of treatable indications.

North America is the leading regional market, accounting for about 37% of global regenerative dentistry revenues in 2025, supported by advanced clinical infrastructure, high per capita spending on dental care, strong presence of major manufacturers, and extensive research activity under institutions such as the National Institutes of Health (NIH) and leading dental schools.

One of the most significant opportunities lies in the integration of digital dentistry and 3D bioprinting with regenerative therapies, enabling customized scaffolds, digitally planned regenerative procedures, and more predictable clinical results, thereby allowing companies that master this convergence to capture premium, innovation-driven segments.

Prominent players include Straumann Group, Dentsply Sirona, 3M, Geistlich Pharma AG, Zimmer Biomet Holdings, Envista Holdings, Ivoclar Vivadent AG, BioHorizons, Henry Schein, Integra LifeSciences, and Collagen Matrix, all of which offer comprehensive portfolios of biomaterials, implant-related regenerative solutions, and supporting services globally.