- Specialty & Fine Chemicals

- Recycled Polyolefin Market

Recycled Polyolefin Market Size, Share, and Growth Forecast, 2026 - 2033

Recycled Polyolefin Market by Product Type (Polyethylene, LDPE, Others), Source (Plastic Bottles, Plastic Films, Others), Application, and Regional Analysis for 2026 - 2033

Recycled Polyolefin Market Size and Trends Analysis

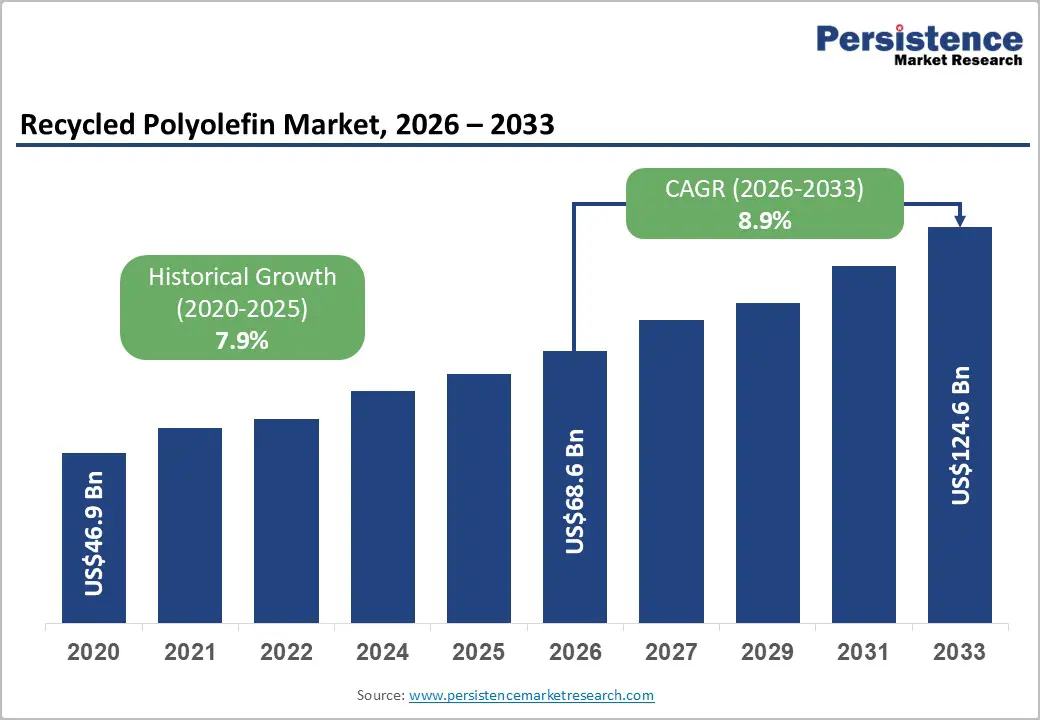

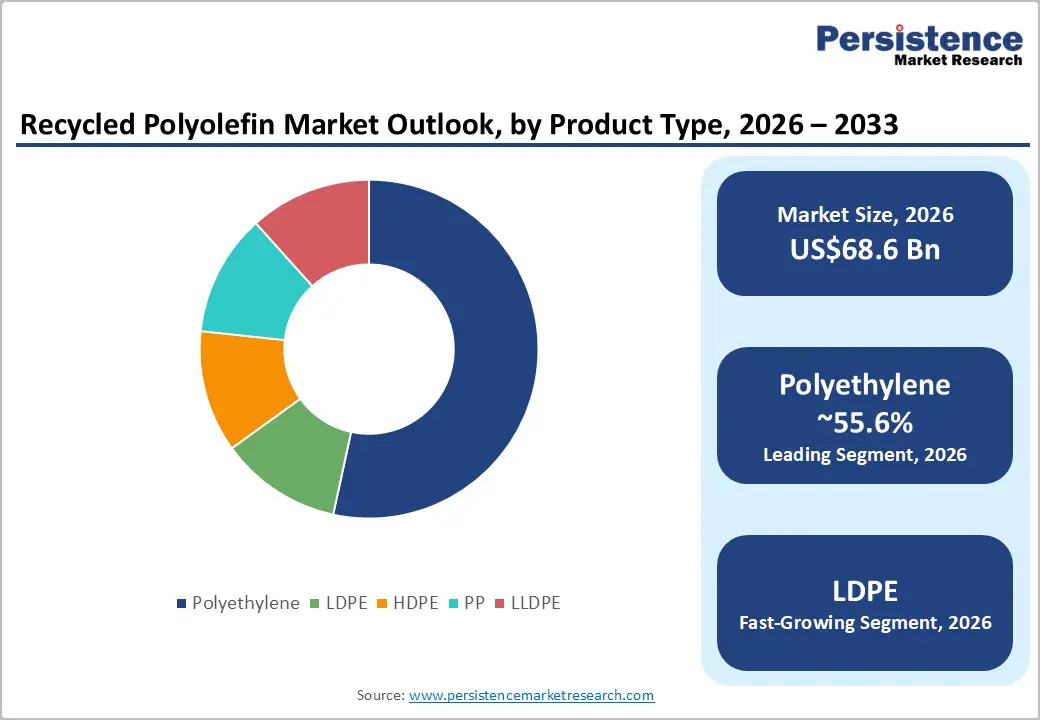

The global recycled polyolefin market size is likely to be valued at US$68.6 billion in 2026 and is expected to reach US$124.6 billion by 2033, growing at a CAGR of 8.9% during the forecast period from 2026 to 2033, driven by accelerating regulatory mandates for recycled content, increasing adoption of circular economy principles in manufacturing, and expanding demand from packaging, automotive, and construction sectors.

Improvements in recycling technologies and material processing capabilities have also enhanced the commercial viability of recycled polyolefins across multiple applications. Investments in waste collection infrastructure, sorting technologies, and recycling facilities are strengthening supply chains, enabling higher recovery rates and improved material quality. Feedstock availability, contamination risks, and price competition with virgin polyolefins remain key factors shaping market dynamics.

Key Industry Highlights:

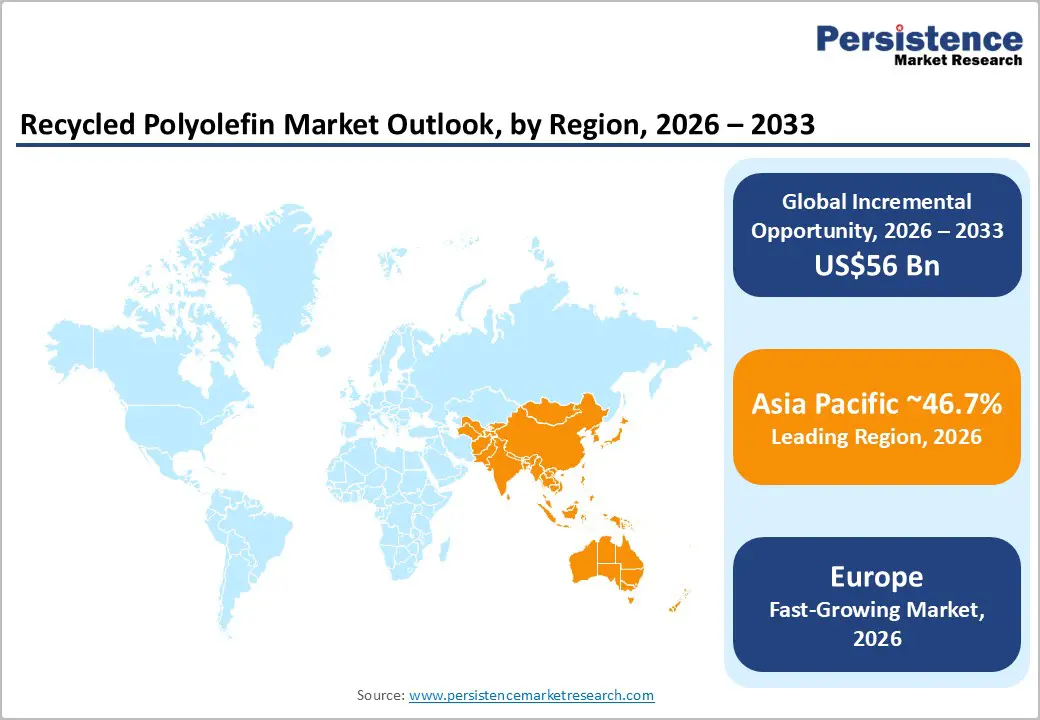

- Leading Region: Asia Pacific is projected to lead the market with approximately 46.7% share. Strong manufacturing activity in China, India, and Southeast Asia drives demand.

- Fastest-growing Region: Europe is the fastest-growing regional market due to strict recycling regulations and circular economy policies, which are accelerating the adoption of recycled polyolefins across the packaging and automotive sectors.

- Investment Plans: Companies are expanding mechanical and chemical recycling capacity. Investments are focused on advanced sorting, film recycling technology, and large-scale recycling plants to increase recycled resin supply.

- Dominant Product Type: Polyethylene is anticipated to lead with around 55.6% market share, supported by the high availability of HDPE and LDPE waste from packaging applications, which supports its dominance.

- Leading Source: Plastic bottles are estimated to dominate with approximately 42.1% share, supported by high collection rates and deposit-return systems, which ensure a stable supply of recyclable HDPE feedstock.

| Key Insights | Details |

|---|---|

| Recycled Polyolefin Market Size (2026E) | US$68.6 Bn |

| Market Value Forecast (2033F) | US$124.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Recycled-Content Mandates and Extended Producer Responsibility (EPR)

Governments across major economies are introducing stricter regulations on plastic waste management and mandating higher recycled content in packaging materials. Extended Producer Responsibility programs require manufacturers and packaging producers to finance the collection, recycling, and disposal of plastic waste, encouraging the adoption of recycled materials. Many national and regional regulations require packaging producers to incorporate recycled polymers into their products by the end of this decade. These policies create a structural demand for recycled polyolefins, particularly recycled polyethylene (rPE) and recycled polypropylene (rPP). Companies operating in packaging, consumer goods, and food industries increasingly source recycled materials to comply with regulatory requirements and reduce environmental impact. As a result, recyclers and polymer processors are expanding capacity and developing higher-grade recyclates capable of meeting industry specifications.

Corporate Sustainability Commitments and Brand Procurement Programs

Major consumer brands and retailers are implementing sustainability strategies focused on reducing plastic waste and increasing the use of recycled materials. Many multinational consumer goods companies have pledged to incorporate significant levels of post-consumer recycled plastic in their packaging portfolios. These commitments have translated into long-term procurement contracts with recyclers and polymer compounders. Brand-driven demand has accelerated innovation in recycled polyolefin processing, enabling the development of consistent, high-quality recyclates suitable for packaging applications. Packaging converters are increasingly transitioning toward mono-material designs that allow easier recycling and higher recycled content. This transformation has increased the value and market acceptance of recycled polyolefins, particularly in flexible and rigid packaging formats.

Advances in Recycling Technologies and Material Processing

Technological advancements in recycling infrastructure have significantly improved the efficiency and output quality of recycled polyolefins. Innovations such as automated optical sorting systems, advanced washing processes, and compatibilization technologies enable recyclers to process complex waste streams more effectively. Chemical recycling technologies are also emerging as complementary solutions to traditional mechanical recycling. These processes convert plastic waste into feedstock suitable for polymer production, enabling the recovery of polyolefins from materials that are difficult to recycle mechanically. As recycling technologies scale and operational efficiencies improve, production costs for recycled polyolefins are expected to decline, supporting wider adoption across multiple industrial sectors.

Barrier Analysis - Feedstock Quality Variability and Contamination Risks

One of the most significant structural challenges in the recycled polyolefin market is the variability in feedstock quality. Post-consumer plastic waste often contains mixed polymers, food residues, additives, and multilayer materials that complicate recycling processes. Contamination reduces processing efficiency and affects the mechanical properties of recycled materials. These challenges require recyclers to invest in advanced sorting and cleaning systems, which increases operational costs. In some cases, processing yield losses can reach 10-25% in mixed waste streams compared with homogeneous plastic inputs. This variability can create supply constraints for high-quality recyclates and limit their use in applications requiring consistent material properties.

Price Competition with Virgin Polyolefins

Recycled polyolefins must compete economically with virgin polymers produced from petrochemical feedstocks. Fluctuations in crude oil and natural gas prices can reduce the price of virgin polyethylene and polypropylene, making recycled materials less competitive. Furthermore, recycling facilities require substantial capital investments in sorting, washing, and processing equipment. Advanced recycling technologies require even greater capital expenditures. As a result, smaller recyclers may struggle to achieve economies of scale. Long-term supply agreements and policy incentives are often necessary to ensure financial viability for recycling projects.

Opportunity Analysis - Expansion of Food-Grade Recycled Polyolefins

Food packaging represents one of the largest potential growth opportunities for recycled polyolefins. Historically, strict safety regulations limited the use of recycled plastics in food-contact applications. However, advances in purification technologies and regulatory approvals are enabling the production of food-grade recycled polymers. Manufacturers that invest in advanced purification systems, quality assurance protocols, and traceability solutions can supply high-value recycled materials for food packaging. Even modest substitution of virgin polymers with recycled alternatives in food packaging could generate substantial incremental demand for recycled polyolefins in the coming decade.

Adoption in Automotive and Durable Goods Manufacturing

Automotive manufacturers are increasingly incorporating recycled materials into vehicle components to reduce weight and carbon emissions. Recycled polyolefins offer favorable properties such as durability, chemical resistance, and cost efficiency, making them suitable for interior trim panels, underbody shields, and various non-structural components. The transition toward electric vehicles further strengthens this trend, as manufacturers seek lightweight materials to improve vehicle efficiency. Partnerships between polymer recyclers and automotive manufacturers are expected to expand, enabling the development of specialized recycled compounds tailored to automotive performance requirements.

Growth in Emerging Markets and Circular Economy Infrastructure

Emerging economies in Asia, Latin America, and parts of Africa are investing in waste management and recycling infrastructure. Rapid urbanization and rising plastic consumption are generating large volumes of recoverable plastic waste. Governments and private investors are establishing modern sorting facilities, recycling plants, and circular economy programs to address these challenges. As recycling infrastructure improves in these regions, the supply of recyclable plastics is expected to increase significantly. This development creates opportunities for international recyclers, technology providers, and packaging companies to expand their operations in high-growth markets.

Category-wise Analysis

Product Type Insights

Polyethylene is anticipated to hold approximately 55.6% of the market share in 2026, making it the dominant product category during the forecast period. Its leadership is primarily driven by the extensive use of polyethylene in flexible packaging, plastic films, shopping bags, containers, bottles, and industrial packaging products. Among the various polyethylene grades, recycled high-density polyethylene (rHDPE) and recycled low-density polyethylene (rLDPE) account for a significant portion of recovered material because these polymers are widely used in consumer packaging and are frequently collected through municipal recycling programs.

Recycled polyethylene is widely used across the packaging, construction, and consumer goods industries. For instance, rHDPE is commonly utilized in manufacturing detergent bottles, milk containers, industrial drums, and piping systems, while rLDPE is widely applied in flexible packaging films, garbage bags, agricultural films, and stretch wrap. Companies in the packaging and consumer goods sectors are increasingly incorporating recycled polyethylene into their product portfolios to meet sustainability goals and regulatory requirements.

Continuous advancements in sorting technologies, such as automated optical sorting and improved washing systems, are enabling recyclers to produce higher-quality polyethylene recyclates suitable for demanding applications such as packaging films and rigid containers.

Low-density polyethylene is anticipated to represent the fastest-growing product segment within the market. The strong growth of this segment is attributed to the significant volume of plastic films and flexible packaging waste generated worldwide. Products such as grocery bags, food packaging films, pallet wraps, and agricultural mulch films contribute substantially to the availability of recyclable LDPE feedstock.

Flexible packaging manufacturers are increasingly transitioning toward mono-material polyethylene structures that improve recyclability and allow higher levels of recycled content. For example, several packaging companies have introduced recyclable polyethylene pouches and film packaging solutions designed specifically to incorporate recycled LDPE. As a result, recyclers are investing in advanced film recycling technologies that improve the recovery and processing of LDPE waste.

Technological improvements in washing, filtration, and pelletization are also enhancing the mechanical performance and purity of recycled LDPE, enabling its use in higher-value applications such as industrial liners, shipping envelopes, agricultural films, and packaging films for consumer products.

Source Insights

Plastic bottles are anticipated to account for approximately 42.1% of the market share in 2026, making them the leading source segment in the market. High-density polyethylene bottles are widely used for packaging household chemicals, personal care products, detergents, and industrial liquids. Owing to their standardized shapes and material compositions, plastic bottles are among the easiest plastic products to collect and recycle. Municipal curbside recycling programs and deposit-return systems play a crucial role in ensuring the consistent recovery of bottle-grade plastics.

For example, household detergent bottles, shampoo containers, and cleaning product packaging are commonly collected through recycling programs and processed into recycled HDPE pellets. These recyclates are subsequently used to produce new packaging containers, pipes, crates, and industrial components. The relatively high purity of bottle-derived plastics allows recyclers to manufacture high-quality recycled resins suitable for packaging and industrial applications, which strengthens the commercial attractiveness of this feedstock stream.

Plastic films are anticipated to emerge as the fastest-growing feedstock source in the recycled polyolefin market due to increasing improvements in film collection systems and recycling technologies. Plastic films include a wide range of materials such as packaging films, grocery bags, shrink wraps, pallet stretch films, agricultural films, and industrial protective coverings. Historically, recycling plastic films posed significant challenges because these materials are lightweight, easily contaminated, and difficult to process in conventional recycling facilities. However, advancements in film recycling technologies and expanded collection initiatives are improving recovery rates.

For instance, retail store take-back programs for shopping bags and flexible packaging waste have expanded in several regions, while agricultural film recovery initiatives are gaining momentum in farming communities. At the same time, improvements in optical sorting systems and film washing technologies allow recyclers to process larger volumes of film waste more efficiently. As these collection and processing systems continue to expand, plastic films are expected to become a more prominent feedstock for recycled polyolefin production.

Regional Insights

North America Recycled Polyolefin Market Trends - Corporate Circular Polymer Initiatives, Advanced Recycling Investments, and Recycled Packaging Demand

North America represents a mature but steadily expanding market for recycled polyolefins, supported by strong industrial demand, developed recycling infrastructure, and corporate sustainability commitments. The U.S. dominates regional consumption due to its large packaging sector and extensive network of recycling facilities. Major metropolitan recycling programs and municipal waste collection systems provide a continuous supply of post-consumer plastics, enabling recyclers to scale operations and improve material recovery. Several polymer producers and packaging companies have also increased their investments in recycling capacity, strengthening the regional supply chain for recycled polyethylene and polypropylene.

The presence of leading polymer producers, packaging manufacturers, and recycling companies plays an important role in advancing the regional circular economy. For instance, companies such as Dow Inc. and ExxonMobil have expanded their circular polymer initiatives by investing in recycled resin production and collaborating with waste management firms to improve plastic recovery. Similarly, LyondellBasell has developed circular polymer product lines using mechanically recycled feedstock, targeting packaging and consumer goods applications. These developments are helping to increase the availability of recycled polyolefins for manufacturers seeking sustainable material alternatives.

Government policies at the state level are also accelerating market development. Several states have introduced legislation encouraging the use of recycled content in packaging materials while promoting investments in recycling infrastructure. For example, Eastman Chemical Company and ExxonMobil have advanced chemical recycling projects in the U.S. that convert difficult-to-recycle plastic waste into raw materials for new polymers. These projects are designed to process complex plastic streams that cannot be easily recycled through traditional mechanical methods.

Corporate sustainability programs are also strengthening demand for recycled polyolefins. Consumer brands such as The Coca-Cola Company and PepsiCo have introduced packaging initiatives aimed at increasing recycled content in plastic bottles and flexible packaging. These commitments encourage packaging suppliers and polymer producers to expand their recycled resin portfolios. In addition, retailers, including Walmart, have introduced packaging sustainability programs that prioritize the use of recycled plastics in product packaging. Investment activity across the region is focused on expanding recycling capacity and improving waste collection systems.

Partnerships between waste management companies, polymer manufacturers, and packaging producers are helping to establish integrated circular economy ecosystems. As these collaborations expand, North America is expected to strengthen its position as a key market for high-quality recycled polyolefins used in packaging, automotive, and consumer goods industries.

Europe Recycled Polyolefin Market Trends - Strong Regulatory Recycling Targets and Advanced Circular Economy Infrastructure

Europe represents the fastest-growing regional market for recycled polyolefins, supported by strong regulatory frameworks, ambitious recycling targets, and well-developed waste management systems. European governments have implemented policies that encourage plastic recycling and require manufacturers to incorporate recycled content into packaging materials. These regulations are accelerating the transition toward circular material use across the packaging, automotive, and consumer goods industries.

Countries such as Germany, the U.K., France, and Spain are leading the regional market. Germany has one of the most advanced recycling infrastructures globally, supported by deposit-return schemes and strict waste segregation policies. Companies such as Borealis AG have expanded mechanical recycling operations across Europe to increase the production of recycled polyethylene and polypropylene.

Similarly, ALPLA Group has invested in recycling facilities in multiple European countries to produce recycled plastics for packaging applications. European regulatory policies require manufacturers to increase the recycled content used in plastic packaging while promoting circular economy initiatives across industries. This regulatory environment has significantly increased demand for recycled polyolefins. Packaging companies such as Amcor and Berry Global have introduced recyclable packaging formats that incorporate recycled polyethylene and polypropylene, supporting the transition toward sustainable packaging solutions.

The region has also become a hub for innovation in recycling technologies. Several companies are investing in advanced mechanical recycling systems as well as chemical recycling technologies that can process complex plastic waste streams. For example, SABIC has launched certified circular polymer products produced from recycled feedstock for use in packaging and consumer goods. These innovations allow manufacturers to integrate higher levels of recycled content into plastic products without compromising performance or quality.

Investment in recycling infrastructure continues to expand as governments and private companies collaborate to improve collection systems and recycling capacity. European packaging and polymer producers are also working closely with automotive manufacturers to incorporate recycled polyolefins into vehicle components. These initiatives are expected to strengthen the supply of recycled plastics and support sustained market growth throughout the region.

Asia Pacific Recycled Polyolefin Market Trends - Large Manufacturing Base, Expanding Recycling Capacity, and Rising Industrial Demand for Recycled Polymers

Asia Pacific is projected to represent the largest regional market, accounting for approximately 46.7% of the market share in 2026. Rapid industrialization, expanding consumer markets, and large-scale plastic consumption contribute to the region’s dominance. The region also benefits from a strong manufacturing base, which creates significant demand for recycled materials in packaging, construction, electronics, and automotive production.

China remains the largest market within the region due to its extensive manufacturing sector and growing recycling industry. The country has implemented policies designed to improve waste management and reduce plastic pollution while encouraging the use of recycled materials in manufacturing. Major petrochemical companies such as Sinopec and PetroChina have expanded recycling initiatives and circular polymer programs aimed at increasing the supply of recycled polyolefins for domestic industries. Japan is recognized for its advanced recycling technologies and highly efficient waste management systems.

Companies such as Mitsubishi Chemical Group are investing in innovative recycling processes that convert plastic waste into high-quality recycled polymers suitable for packaging and industrial applications. These technologies support Japan’s broader circular economy goals and promote sustainable material use across manufacturing sectors. India and Southeast Asian nations are also experiencing rapid growth in plastic consumption and waste generation. Governments in these countries are expanding recycling infrastructure and encouraging private investment in waste management projects.

For example, Reliance Industries Limited has launched initiatives to produce recycled polymers and promote plastic recycling across India’s manufacturing sector. In Southeast Asia, packaging companies and consumer brands are collaborating with recycling firms to increase the collection and processing of plastic waste. The region’s strong manufacturing ecosystem provides extensive opportunities for the use of recycled polyolefins in packaging, construction materials, consumer goods, and automotive components.

As investments in recycling infrastructure and collection systems continue to increase, Asia Pacific is expected to maintain its leadership position in the global recycled polyolefin market while supporting the transition toward a circular plastics economy.

Competitive Landscape

The global recycled polyolefin market is characterized by a moderately fragmented structure. Numerous regional recycling companies operate alongside large polymer producers and global packaging manufacturers. While smaller recyclers focus on localized waste processing, larger companies leverage advanced recycling technologies and integrated supply chains to produce high-quality recycled materials.

Major polymer producers are increasingly expanding their recycling capabilities to meet sustainability targets and customer demand for recycled materials. Strategic collaborations between recyclers, packaging companies, and consumer goods manufacturers are becoming more common as companies seek to secure stable supplies of recycled polymers. Leading companies focus on capacity expansion, technology development, and strategic partnerships to strengthen their positions in the recycled polyolefin market. Vertical integration across waste collection, recycling, and polymer production is emerging as a key strategy. Companies are also investing in advanced recycling technologies and product certification to access high-value applications such as food packaging and automotive components.

Key Industry Developments:

- In March 2025, Borealis AG introduced Borcycle™ M CWT120CL, a recycled linear low-density polyethylene (rLLDPE) grade containing 85% post-consumer recyclate for non-food flexible packaging applications. The new material improves performance for stretch films and industrial packaging while helping manufacturers increase recycled content in packaging products.

- In September 2025, Borealis AG commissioned a new compounding line in Beringen, Belgium, designed to produce high-quality recyclate-based polyolefins using Borcycle™ M mechanical recycling technology. The facility strengthens the supply of recycled polyethylene and polypropylene for demanding applications such as packaging and automotive components.

Companies Covered in Recycled Polyolefin Market

- Veolia

- SUEZ

- Biffa plc

- LyondellBasell

- Borealis AG

- SABIC

- Dow Inc.

- ExxonMobil

- MBA Polymers

- KW Plastics

- Republic Services

- Waste Management, Inc.

- Remondis SE & Co. KG

- Indorama Ventures

- Reliance Industries Limited

- Berry Global

Frequently Asked Questions

The global recycled polyolefin market is expected to be valued at US$68.6 billion in 2026.

The recycled polyolefin market is projected to reach US$124.6 billion by 2033.

Key trends include growing adoption of recycled content in packaging, expansion of advanced mechanical and chemical recycling technologies, increasing corporate sustainability commitments, and rising investments in plastic waste collection and recycling infrastructure.

Polyethylene is the leading product segment, accounting for around 55.6% of the market share. Its dominance is driven by its extensive use in packaging films, containers, plastic bags, and industrial packaging applications.

The recycled polyolefin market is expected to grow at a CAGR of 8.9% between 2026 and 2033.

Major companies include Borealis AG, LyondellBasell, Dow Inc., SABIC, and Veolia.