- Agrochemicals

- Pyrethroids Market

Pyrethroids Market Size, Share, and Growth Forecast, 2026 - 2033

Pyrethroids Market By Product Type (Bifenthrin, Deltamethrin, Permethrin, Cypermethrin, Cyfluthrin, Lambda-Cyhalothrin, Others), Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others), Application (Household, Agriculture, Others), and Regional Analysis for 2026 - 2033

Pyrethroids Market Share and Trends Analysis

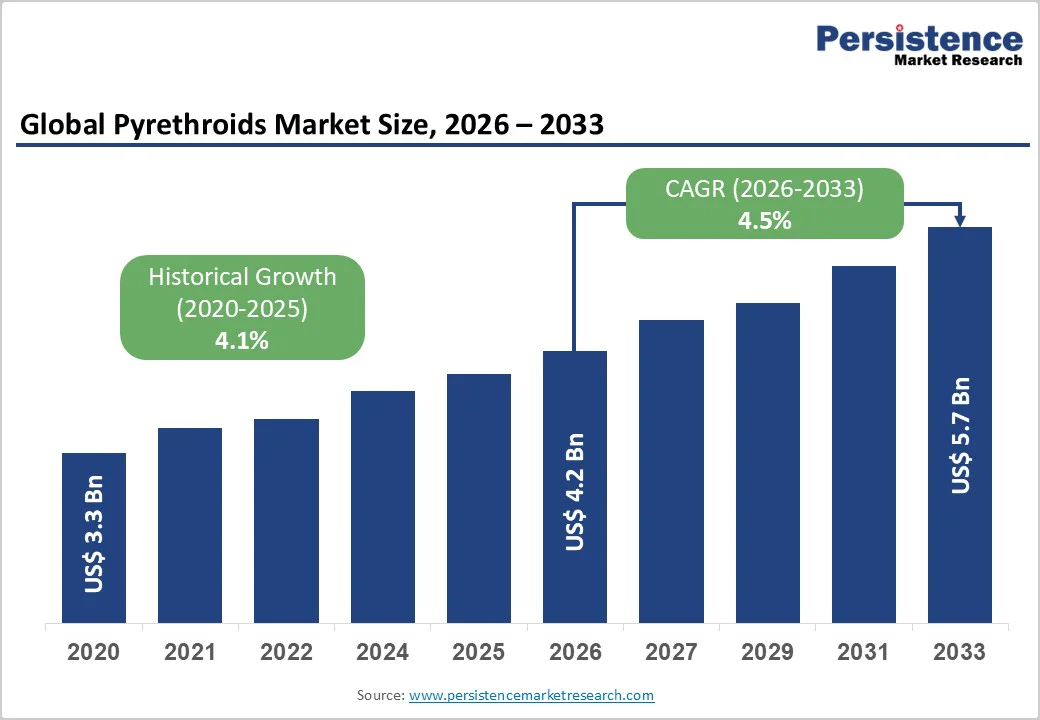

The global pyrethroids market size is likely to be valued at US$4.2 billion in 2026 and is estimated to reach US$5.7 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026 - 2033. The primary factors fueling market growth are closely linked to rising demand for food production driven by growing populations and changing consumption patterns.

This surge in food demand necessitates intensified agricultural activities, which in turn expands the reliance on effective crop protection solutions such as pyrethroids. These synthetic insecticides play a crucial role in safeguarding yields against diverse pest threats, helping to maintain crop quality and productivity.

Supportive government regulations that encourage the adoption of safe and efficient pest control measures, combined with continuous advancements in formulation technologies, further enhance the effectiveness and environmental compatibility of pyrethroids.

Key Industry Highlights

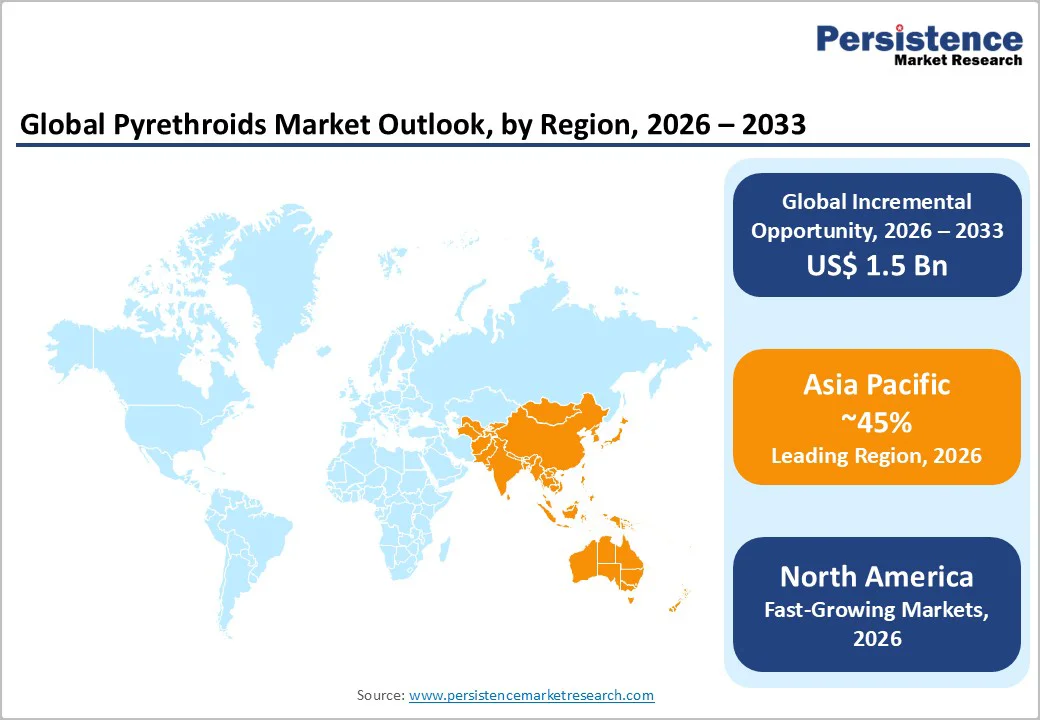

- Dominant Region: Asia Pacific is projected to account for over 45% of the pyrethroids market share in 2026, driven by heavy agricultural dependence and multiple pest cycles.

- Fastest-growing Market: North America is expected to be the fastest-growing market through 2033, driven by rising demand for high-performance, reliable insect control solutions.

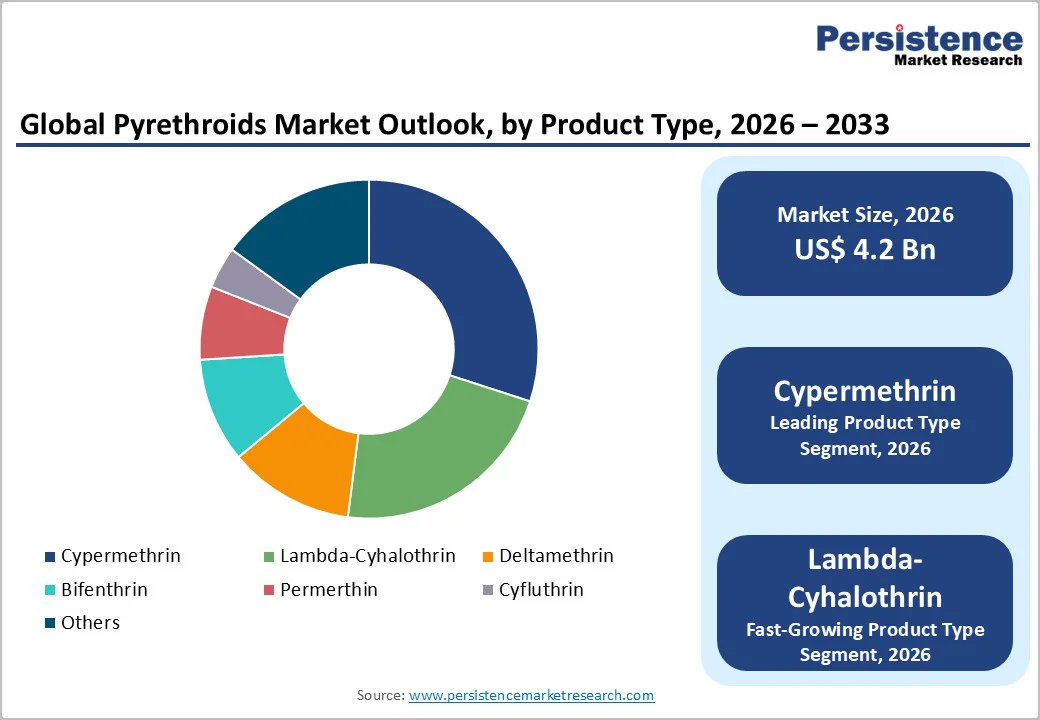

- Leading Product Type: Cypermethrin is projected to lead in 2026 with a 30% share, owing to its broad-spectrum efficacy, cost efficiency, and adaptability across crops.

- Fastest-growing Product Type: Lambda-Cyhalothrin is expected to be the fastest-growing pyrethroid from 2026 to 2032, driven by high-potency, low-dose formulations and strong regulatory support.

- September 2025: Research revealed that several fruits and vegetables in the U.S. carry pesticide residues, including insecticides linked to serious health risks.

| Key Insights | Details |

|---|---|

| Pyrethroids Market Size (2026E) | US$4.2 Bn |

| Market Value Forecast (2033F) | US$5.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Escalating Global Food Demand and Agricultural Expansion

Surging global food demand continues to exert consistent pressure on agricultural systems to preserve crop yields and overall productivity. Factors such as the expansion of cultivation areas, shorter planting cycles, and the use of high-value crop varieties have created conditions that favor rapid pest proliferation.

In response, growers increasingly rely on synthetic insecticides known for their rapid action and broad-spectrum efficacy to ensure dependable field performance within demanding production timelines. Sustained pest suppression is pivotal to stabilizing harvest volumes, strengthening supply chain continuity, and safeguarding growers’ profitability amid climatic fluctuations and uncertain weather patterns.

The expansion of agricultural frontiers, particularly in emerging economies, is also driving higher adoption of advanced crop-protection inputs that deliver consistent results across varied environments. Among these, pyrethroid-based formulations stand out due to their strong field stability, compatibility with high-volume spraying systems, and cost-effectiveness, making them suitable for both smallholder and large-scale farming operations.

As commercial agriculture evolves toward greater mechanization and adherence to international quality benchmarks, the need for efficient, integrated, and rapidly deployable insect control solutions becomes increasingly critical to maintaining both farm productivity and market competitiveness.

Regulatory Restrictions and Environmental Concerns

Regulatory oversight and environmental sustainability concerns are emerging as persistent constraints on the global insecticide market, as authorities intensify their scrutiny of chemical inputs with potential ecological risks. Pyrethroid compounds, while effective, pose acute toxicity hazards to aquatic species and beneficial pollinators, triggering stricter compliance requirements across numerous regions.

Rising enforcement of residue thresholds, discontinuation of high-risk formulations, and the need for frequent product reauthorizations have substantially increased operational complexity. These regulatory pressures drive up compliance costs, lengthen product registration timelines, and limit the range of approved active ingredients available to manufacturers, reducing agility in formulation design and slowing innovation pipelines within the crop-protection sector.

Environmental sensitivity is also reshaping industry dynamics, as ecosystems are increasingly vulnerable to chemical runoff, soil degradation, and bioaccumulation. Growing awareness of pest resistance development has led regulators to restrict permissible usage volumes and application frequency further, encouraging the adoption of integrated pest management practices.

Simultaneously, buyers and end-users are becoming more discerning, prioritizing low-impact pest-control solutions that align with corporate sustainability goals and consumer expectations.

The evolving pattern of preferences compels producers to reengineer formulations, invest in safer and more targeted delivery systems, and recalibrate product portfolios to meet both regulatory mandates and market demand for environmentally responsible crop-protection frameworks.

Growing Adoption of Integrated Pest Management Solutions

Integrated pest management (IPM) strategies present a significant growth avenue for pyrethroid manufacturers as global agriculture evolves toward data-informed and efficiency-oriented pest-control systems. Farmers, agribusinesses, and institutional stakeholders increasingly prioritize technologies that support precise application, reduced chemical dependency, and effective resistance management.

Within these frameworks, pyrethroid compounds occupy a strong position due to their rapid action, broad-spectrum efficacy, compatibility with biological control agents, and suitability for rotational use in resistance-prevention programs. Their relevance continues to deepen as growers seek solutions that uphold field performance, integrate with sustainable practices, and comply with modern agronomic standards focused on environmental and economic balance.

Rising adoption of precision agriculture techniques further accelerates demand for reliable and adaptable insecticides. Producers, cooperatives, and public health initiatives are investing in decision-support systems, digital surveillance platforms, and precision-spraying technologies that depend on crop-protection inputs capable of maintaining consistent results under monitored and regulated dosage conditions.

Pyrethroids align well with these technical parameters, offering predictable field performance within structured and sustainable usage models. As the industry transitions toward integrated, data-driven pest management ecosystems, pyrethroid formulations gain renewed commercial relevance, creating opportunities for product innovation, advanced delivery mechanisms, and differentiated value propositions aligned with long-term sustainability goals.

Category-wise Analysis

Product Type Insights

Cypermethrin is projected to retain a leading market position in 2026, accounting for an estimated 30% of the pyrethoid market revenue share, supported by its broad-spectrum efficacy, cost competitiveness, and strong compatibility with multiple agricultural systems. Its widespread deployment across staples such as cereals, cotton, vegetables, and plantation crops underscores both its versatility and sustained utility in large-scale production environments.

Continued consumption across Asia Pacific and North America further amplifies its commercial footprint, benefiting from mature distribution networks and established usage familiarity among growers. Reliable supply availability, consistent field performance, and proven economic value collectively reinforce Cypermethrin’s dominance within global insect-control markets.

Lambda-Cyhalothrin is poised to record the fastest growth among pyrethroid products during 2026 - 2033, reflecting a broader shift toward potent, low-dose insecticide technologies aligned with integrated pest-resistance management strategies.

Its quick-acting properties, coupled with ongoing advancements in formulation science, have enhanced both efficacy and safety profiles, driving adoption across professional farming operations and residential pest-control applications.

Strengthening regulatory preference for effective yet environmentally responsible chemistries adds momentum to this trend, positioning Lambda-Cyhalothrin as a key growth driver with expanding market penetration and strong adoption potential across diverse end-use segments.

Crop Type Insights

Oilseeds and pulses are expected to maintain their leading market position in 2026, accounting for approximately 34% of the total demand. Their dominance is anchored in extensive cultivation acreage and significant economic importance across key producing regions worldwide.

Persistent pest pressure from chewing and sucking insects continues to challenge yield stability, driving steady adoption of pyrethroid-based solutions for effective crop protection. Reliance on these chemistries, supported by well-established agronomic practices and proven efficacy, ensures consistent usage, reinforcing the segment’s sustained demand and leadership within the global crop protection landscape.

The fruits and vegetables segment is projected to represent the fastest-growing crop types through 2033, underpinned by rising consumer expectations for quality, appearance, and extended shelf life. These high-value crops require intensive pest-management regimes to prevent economic loss and maintain export viability, fostering greater reliance on targeted, low-residue pyrethroid treatments.

Growth in horticultural cultivation, expanding premium markets, and the pursuit of reliable protective mechanisms are accelerating adoption across both conventional and precision agriculture models. As a result, fruits and vegetables are positioned to capture strong short-term momentum and become a key driver of pyrethroid market expansion during the forecast period.

Application Insights

The agriculture sector is expected to command over 40% of the market revenue share in 2026. This dominance is driven by the indispensable role of pyrethroid-based insecticides in protecting key crops such as cereals, oilseeds, vegetables, and plantation commodities from persistent pest infestations.

Their broad-spectrum efficacy, cost-effectiveness, and operational compatibility with large-scale mechanized farming systems continue to support widespread adoption. In developing economies, increasing cultivation area and the growing imperative to secure stable yields under variable climatic conditions are further consolidating agriculture’s supremacy as the primary application domain for pyrethroid usage.

The household segment is anticipated to be the fastest-growing application area between 2026 and 2033, spurred by rapid urbanization and escalating public awareness of vector-borne disease threats. Consumers increasingly depend on pyrethroid-based aerosols, coils, mats, and home-care formulations to manage mosquitoes, flies, and other domestic pests effectively.

Expanding distribution of branded pest-control products, coupled with rising living standards and a heightened focus on health and hygiene, is accelerating uptake across both emerging and developed markets. This growing demand positions the household segment as a key growth frontier, combining strong volume potential with steady gains in consumer preference for safe, effective, and accessible pest-control solutions.

Regional Insights

North America Pyrethroids Market Trends

North America is projected to register the fastest growth from 2026 to 2033, propelled by increasing pest pressure stemming from climatic variability, escalating resistance challenges, and rising demand for high-performance insect control solutions across both agricultural and non-agricultural sectors.

Extensive cultivation of major crops such as corn, soybeans, cotton, and specialty produce continues to drive adoption of advanced pyrethroid formulations known for dependable efficacy and seamless integration with precision and large-scale farming systems.

The region’s sustained focus on food security, yield reliability, and crop quality improvement further reinforces the strategic role of pyrethroids within IPM frameworks, strengthening their relevance in modern, technology-enabled agriculture.

Complementing this agricultural demand, robust expansion is also observed within household and commercial pest-control markets, driven by urban population growth and increasing awareness of vector-borne health risks.

The region’s investment landscape is evolving rapidly, with strong capital inflows directed toward formulation innovation, precision-application equipment, and collaborative programs with professional pest management providers. Enhanced regulatory transparency, coupled with advanced research infrastructure and a clear trajectory toward lower-toxicity, efficiency-optimized insecticides, is accelerating commercialization across the value chain.

Europe Pyrethroids Market Trends

Europe is expected to sustain a strong and stable position in the pyrehroids market in 2026, supported by its technologically advanced agricultural infrastructure, rigorous crop-protection standards, and a well-defined regulatory framework favoring safer, lower-toxicity insecticides.

Large-scale cultivation of cereals, fruits, vegetables, and oilseeds continues to drive steady pyrethroid use as European growers focus on maintaining yield consistency and product quality within stringent residue and environmental compliance limits. The region’s temperate climate fosters moderate yet persistent pest pressure, encouraging structured and preventive pest-management regimes across multiple crop cycles, thereby underpinning continuous demand.

The strength of the Europe market extends beyond agriculture, shaped by well-developed public health initiatives, increasing emphasis on vector control, and robust household insect-management segments operating under tight environmental guidelines.

Regional producers are actively channeling investments into the development of compliance-ready pyrethroid formulations with improved safety and sustainability profiles, enabling alignment with evolving European Union (EU) regulatory mandates. Mature distribution networks, advanced farming technologies, and a strong integration of digital decision-support tools contribute to reliable market performance.

Asia Pacific Pyrethroids Market Trends

Asia Pacific is expected to account for more than 45% of the pyrethroids market share in 2026, fueled by the heavy dependence of farmers in the region on crop-protection products and expanding agricultural activity across fast-developing economies. The region’s warm, humid climate facilitates multiple pest breeding cycles annually, heightening the demand for rapid-action insecticides with reliable field efficacy.

Dominance in this market is further supported by extensive cultivation of oilseeds, pulses, fruits, and vegetables, where pyrethroids are vital for maintaining yield integrity and meeting international export standards. Strengthening of local manufacturing capabilities, supported by efficient supply networks and competitive pricing strategies, continues to boost adoption across both smallholder farms and large commercial operations.

Asia Pacific’s leadership is also bolstered by evolving regulatory frameworks that emphasize low-toxicity and residue-efficient pest-management solutions, positioning pyrethroids favorably within sustainable agriculture agendas.

Rising urban populations are increasing household demand for insect-control products, while frequent outbreaks of mosquito-borne diseases are driving large-scale public health initiatives reliant on pyrethroid formulations. Governments and private enterprises are simultaneously investing in IPM systems, where pyrethroids function as pivotal components balancing efficacy, safety, and cost.

Competitive Landscape

The global pyrethroids market exhibits a moderately consolidated competitive structure, with leading industry participants collectively commanding approximately 50% of the total market share. Prominent companies such as Bayer, BASF, Syngenta, and DuPont de-Nemours anchor this landscape through comprehensive product portfolios, efficient global distribution frameworks, and continuous investment in advanced formulation technologies.

Their scale and technical expertise enable effective navigation of evolving regulatory standards and ensure product reliability tailored to the needs of modern agricultural systems. These established players also leverage research synergies and strategic collaborations to enhance performance efficiency while maintaining high compliance and sustainability benchmarks.

The remaining market share is distributed among regional and domestic producers, contributing to a dynamic and competitive operating environment. These smaller participants differentiate through cost-effective manufacturing, localized distribution strategies, and tailored product offerings that address specific pest profiles and crop conditions.

The coexistence of large multinationals and agile regional manufacturers creates a balanced market ecosystem where innovation, affordability, and accessibility remain key growth enablers.

Key Industry Developments

- In August 2025, a new study reveals that a 2024 mass die-off of Monarch butterflies near California’s overwintering grounds was likely caused by pesticide exposure. Every butterfly tested carried multiple chemicals, including lethal doses of pyrethroids, providing rare direct evidence that residential and agricultural insecticide use can trigger large-scale insect mortality.

- In July 2025, a research team led by Prof. Jiang Changlong at the Hefei Institutes of Physical Science developed a rapid method to detect harmful pyrethroid pesticide residues in just 10 seconds. The new fluorescent probe changes color upon contact with pyrethroids, allowing results to be seen with the naked eye, offering a fast and practical solution for monitoring both household and agricultural products.

- In April 2025, BASF's Interceptor® G2, a WHO-approved dual-active ITN (alpha-cypermethrin pyrethroid + chlorfenapyr), combats pyrethroid-resistant malaria mosquitoes, reducing child malaria incidence by 43-55%, as compared to pyrethroid-only nets in Benin/Tanzania trials. Developed over 11 years with IVCC/London School of Hygiene, it offers surface-coated, wash-resistant protection against resistant vectors in sub-Saharan Africa, slowing resistance evolution.

Companies Covered in Pyrethroids Market

- Bayer AG

- BASF SE

- Syngenta AG

- Corteva Agriscience

- FMC Corporation

- DuPont de Nemours, Inc.

- Nanjing Red Sun Co. Ltd

- Meghmani Organics Ltd

- Bonide Products LLC

- Bharat Rasayan Ltd

- Sumitomo Chemical Co., Ltd

- UPL Limited

Frequently Asked Questions

The global pyrethroids market is projected to reach US$ 4.2 billion in 2026.

Key drivers of the market include increasing agricultural intensification, growing prevalence of vector-borne diseases, rising adoption of integrated pest management, demand for high-yield and high-quality crops, and expanding use of household insecticides.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

The development of integrated pest management solutions, rapid detection technologies, and expanding demand of advanced pest control formulations in emerging agricultural and urban markets are key market opportunities.

Some of the key market players include Bayer AG, BASF SE, Syngenta AG, and Corteva Agriscience.