- Executive Summary

- Global Polycarboxylate Ether Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Chemical Industry Overview

- Global Construction Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Polycarboxylate Ether Market Outlook: By Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by By Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- Market Attractiveness Analysis: By Product Type

- Global Polycarboxylate Ether Market Outlook: By Form

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by By Form, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- Market Attractiveness Analysis: By Form

- Global Polycarboxylate Ether Market Outlook: By End-Use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by By End-Use , 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- Market Attractiveness Analysis: By End-Use

- Global Polycarboxylate Ether Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- Europe Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- East Asia Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- South Asia & Oceania Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- Latin America Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- Middle East & Africa Polycarboxylate Ether Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by By Product Type, 2026-2033

- Standard Polycarboxylate Ether

- High-Range Water Reducers

- Superplasticizers

- Water-Reducing Agents

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by By Form, 2026-2033

- Liquid

- Powder

- Granular

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by By End-Use , 2026-2033

- Residential Construction

- Commercial Construction

- Infrastructure Development

- Industrial Construction

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Sika AG

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- BASF SE

- Abadgaran Group

- Arkema SA

- Mapei S.P.A.

- Sakshi Chem Sciences Private Ltd.

- Fosroc International Ltd.

- TriStar Technical Co.

- Henan Kingsun Chemical Co., Ltd

- Himadri Speciality Chemicals Ltd.

- KMT Polymers

- Chemocon Tecsys Pvt. Ltd

- Ruia Chemicals

- Kashyap Industries

- Others

- Sika AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Polycarboxylate Ether Market

Polycarboxylate Ether Market Size, Share, and Growth Forecast 2026 - 2033

Polycarboxylate Ether Market by Product Type (Standard Polycarboxylate Ether, High-Range Water Reducers, Superplasticizers, Water-Reducing Agents), Form (Liquid, Powder, Granular), End-user (Residential Construction, Commercial Construction, Infrastructure Development, Industrial Construction), and Regional Analysis, 2026 - 2033

Polycarboxylate Ether Market Size and Trend Analysis

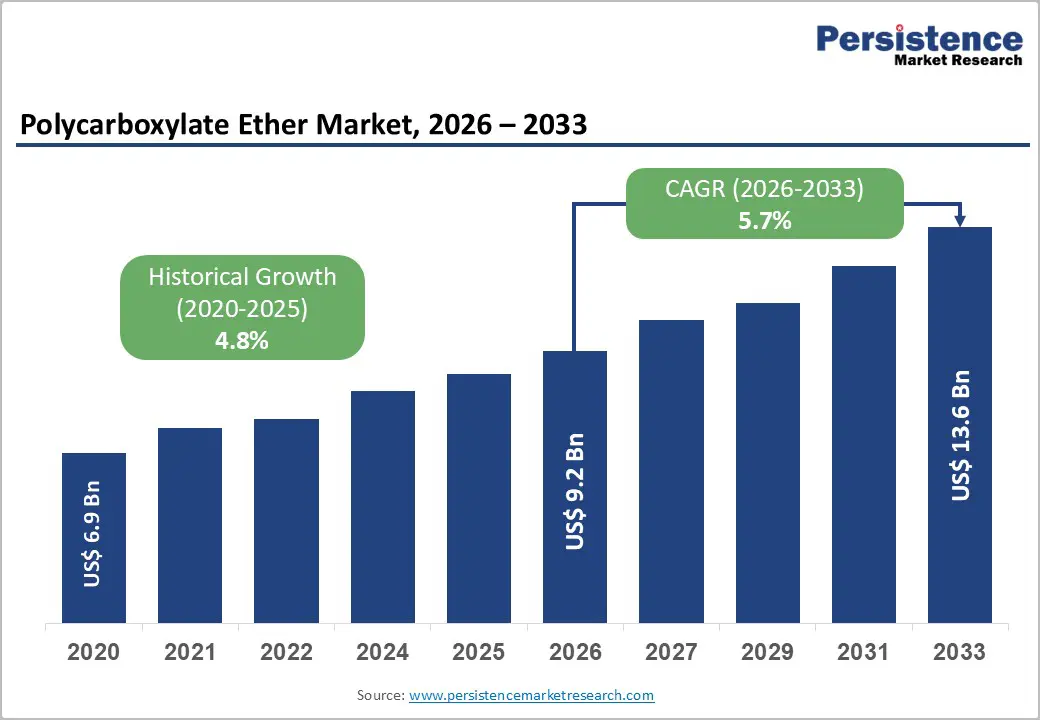

The global polycarboxylate ether market size is likely to be valued at US$ 9.2 Billion in 2026 and is expected to reach US$ 13.6 Billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The market's accelerating expansion is principally driven by the global construction industry's structural shift toward high-performance, low water-to-cement ratio concrete formulations, where Polycarboxylate Ether (PCE)-based superplasticizers deliver unmatched workability, durability, and sustainability benefits compared to older-generation admixtures.

Key Industry Highlights:

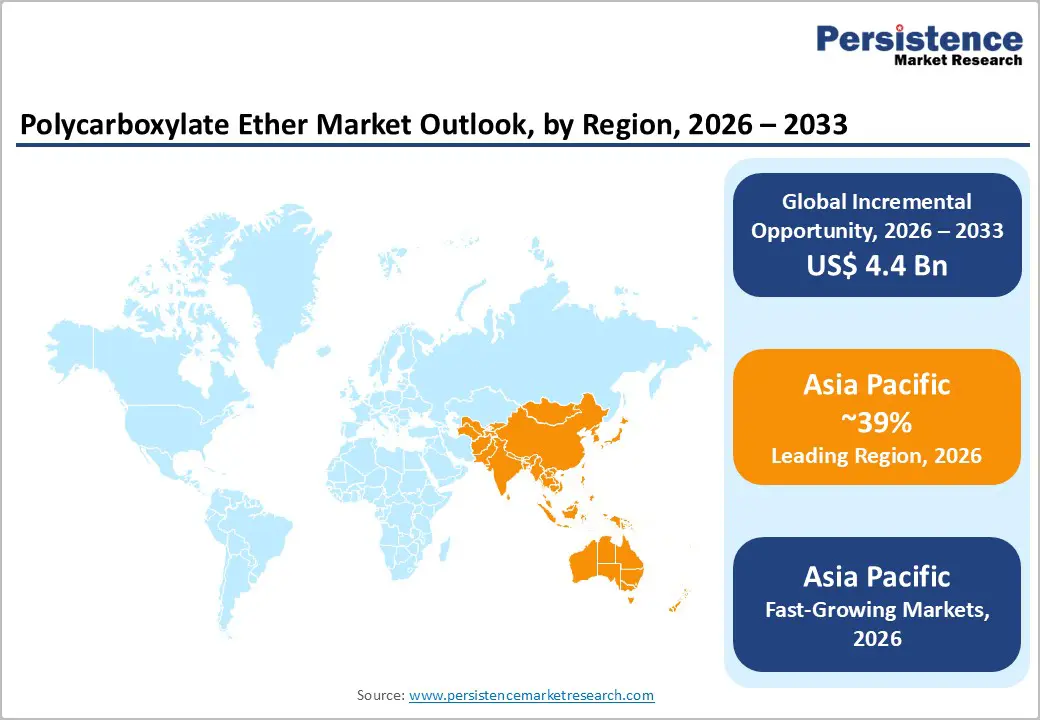

- Leading Region: Asia Pacific leads the global Polycarboxylate Ether market holding 39% share, driven by China's massive ready-mix concrete sector, with over 7,000 commercial plants nationally, and India's National Infrastructure Pipeline valued at approximately INR 111 trillion, making the region the world's highest-volume PCE demand hub.

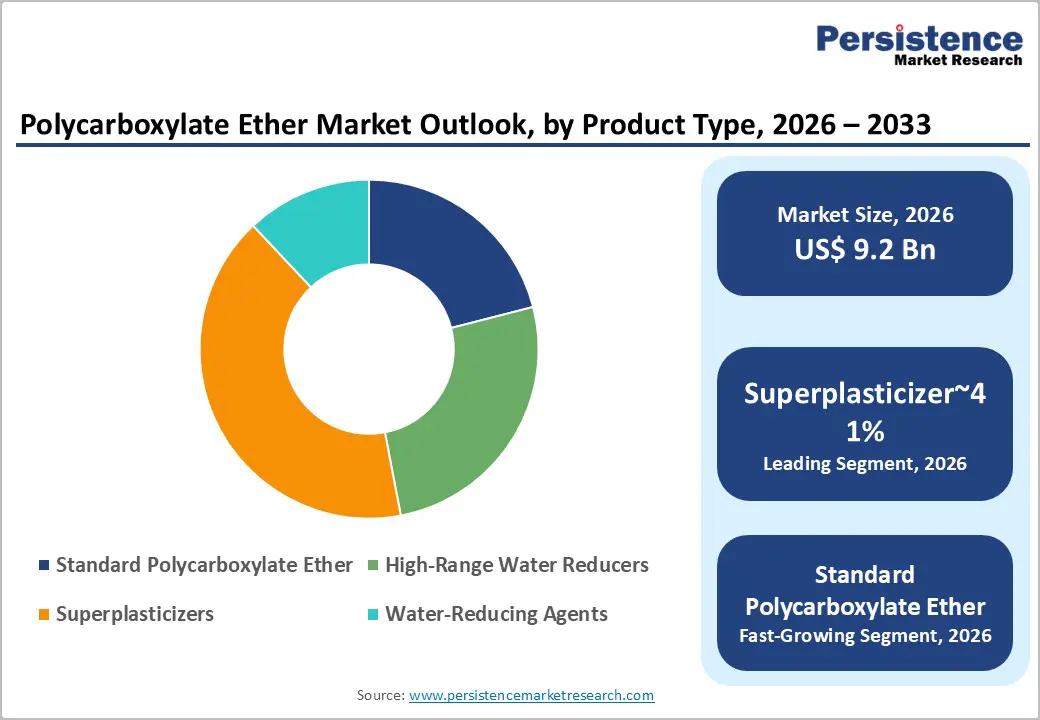

- Leading Product Segment: Superplasticizers dominate the Product Type segment with approximately 41% revenue share in 2026, anchored by their 40.8% share in the global concrete superplasticizer market and their mandated specification across ASTM C494, EN 934-2, and IS 9103 admixture standards in public infrastructure contracts.

- Fastest-Growing Form Segment: Liquid PCE formulations are the dominant and fastest-growing Form segment, commanding approximately 68% market share due to universal compatibility with automated batching plant systems across ERMCO-affiliated ready-mix plants in Europe and the thousands of concrete plants operating across Asia Pacific.

- Key Opportunity: Third-generation iPEG-based PCE chemistry and 3D concrete printing applications represent the key market opportunity, with BASF's Pluriol A 2400 I launch in 2025 and growing adoption of 3DCP across smart city and prefabrication programs offering manufacturers premium pricing, proprietary positioning, and long-term margin expansion.

| Key Insights | Details |

|---|---|

| Polycarboxylate Ether Market Size (2026E) | US$ 9.2 Billion |

| Market Value Forecast (2033F) | US$ 13.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Surging Global Infrastructure Investment Amplifying PCE-Based Concrete Admixture Demand

Large-scale national infrastructure investment programs across multiple regions are creating one of the strongest and most sustained demand drivers for Polycarboxylate Ether (PCE) products worldwide. In the United Kingdom, the Office for National Statistics (ONS) reported a 15.9% increase in total new construction orders, reaching £1.43 billion in Q1 2024 compared to Q4 2023. This growth reflects strong infrastructure development activity that directly translates into increased procurement of PCE-based admixtures.

In the United States, the Infrastructure Investment and Jobs Act of 2021 committed US$1.2 trillion toward roads, bridges, water systems, and public transit networks, maintaining high levels of concrete production demand. PCE admixtures are widely preferred due to their ability to reduce water-to-cement ratios by up to 40% and maintain slump retention for nearly 90 minutes, significantly outperforming older naphthalene-based systems. Similarly, India’s National Infrastructure Pipeline (NIP), valued at approximately INR 111 trillion, along with expanding urban transit projects across Southeast Asia, continues to strengthen long-term demand for PCE-based superplasticizers in infrastructure-grade concrete applications globally.

Accelerating Adoption of High-Performance and Self-Compacting Concrete in Commercial Construction

The global commercial construction sector is increasingly adopting advanced concrete technologies such as high-performance concrete (HPC), self-compacting concrete (SCC), and ultra-high-performance concrete (UHPC). This transition is creating strong technical demand for PCE-based superplasticizers, which are among the few admixture chemistries capable of meeting the strict workability, strength, and durability requirements of these modern concrete systems. Standards developed by the European Committee for Standardization (CEN) and ASTM International for SCC specifically recommend high-range water reducers, most of which are based on PCE chemistry.

These guidelines have made PCE admixtures the preferred solution in specification-driven commercial construction projects. Industry analysis indicates that the PCE-based segment accounted for around 40.8% of total revenue in the global concrete superplasticizer market in 2025, supported by its superior dispersing performance and long workability retention. Rapid construction of high-rise residential and mixed-use commercial towers in China, India, and ASEAN countries is further increasing the need for pumpable concrete mixtures that require sustained slump retention during long delivery times, strengthening demand for PCE admixtures worldwide.

Restraints - Volatility in Petrochemical and Ethylene Oxide Raw Material Prices

The production of Polycarboxylate Ether relies heavily on petrochemical feedstocks such as ethylene oxide (EO), acrylic acid, and methacrylic acid. The prices of these raw materials are closely linked to crude oil price fluctuations and global ethylene supply dynamics, making the cost structure of PCE production inherently volatile. Significant price increases in these upstream inputs can directly affect the profitability of PCE manufacturers. For example, during 2021-2022, global ethylene oxide prices increased by more than 30% due to pandemic-related supply chain disruptions and constrained petrochemical output.

Such fluctuations significantly reduced margins for many PCE producers, particularly mid-sized regional manufacturers that lack integrated feedstock supply capabilities. According to the International Energy Agency (IEA), petrochemical feedstock price volatility remains a persistent structural challenge for polymer-based specialty chemical producers. This instability makes it difficult for manufacturers to maintain stable product pricing in competitive construction chemical markets and can discourage long-term supply contracts from cost-sensitive buyers within the infrastructure and commercial construction sectors.

Environmental Regulations on Ethylene Oxide Usage Constraining Production Scalability

The synthesis of key PCE monomers involves the industrial use of ethylene oxide, particularly during the polyethylene glycol (PEG) ethoxylation process. Ethylene oxide has been classified as a Group 1 human carcinogen by the International Agency for Research on Cancer (IARC), leading to stricter regulations governing its handling, emissions, and occupational exposure levels. Across the European Union, regulatory authorities have introduced tighter standards under the Industrial Emissions Directive (IED), which impose stringent monitoring and compliance requirements on facilities using ethylene oxide.

The European Chemicals Agency (ECHA) has also implemented stricter occupational exposure limits and emission control measures. As a result, PCE manufacturers operating in Europe must invest significantly in advanced emission-control technologies, closed-loop reactor systems, and enhanced worker safety infrastructure. These investments increase capital expenditure requirements for new manufacturing plants and expansion projects. Consequently, the rising regulatory burden may slow down capacity expansion in highly regulated markets and create barriers for new regional manufacturers attempting to establish PCE production operations in Western Europe.

Opportunities - Third-Generation PCE Innovation and Bio-Based Feedstock Development Creating Premium Product Differentiation

Technological advancements in Polycarboxylate Ether chemistry are opening new opportunities for product innovation and differentiation in the global market. The development of third-generation PCE formulations based on advanced monomer structures such as isoprenol-PEG (iPEG) and allyl-PEG (APEG) is significantly improving concrete performance characteristics. These new molecular architectures provide enhanced flow properties, longer slump retention, and improved durability in demanding construction applications. In May 2025, BASF SE introduced Pluriol A 2400 I, a specialized iPEG monomer developed for third-generation PCE admixtures at its Ludwigshafen facility. This production site features a fully integrated polyethylene glycol to PCE supply chain, enabling reduced carbon emissions through localized feedstock sourcing.

At the same time, the construction chemicals industry is increasingly focusing on sustainability, driving research into bio-based polymer precursors and renewable raw materials for PCE production. Such innovations align with the European Green Deal and broader carbon-neutral construction initiatives. Manufacturers that develop certified environmentally friendly PCE products and achieve ISO 14001 environmental management certification are likely to gain premium pricing advantages and stronger positioning in sustainability-focused infrastructure and commercial construction projects.

3D Concrete Printing and Precast Expansion Generating High-Growth Niche Applications for Specialized PCE Formulations

Emerging construction technologies such as 3D concrete printing and the expanding global precast concrete industry are creating new high-growth application areas for specialized PCE formulations. These innovative construction methods require precise control over concrete rheology, including viscosity, flow behavior, and buildability characteristics that conventional admixtures cannot provide. PCE-based admixtures play a critical role in achieving the required balance between extrudability and structural stability in 3D printed concrete.

Organizations such as ASTM International and the International Federation for Structural Concrete (fib) are currently developing technical standards for 3D printable concrete, with PCE-based rheology modifiers identified as essential components in mix design. The global precast concrete market, valued at more than US$100 billion, heavily depends on high-range water-reducing PCE admixtures to ensure faster strength development, precise dimensional accuracy, and superior surface finishing in factory-produced concrete components. Leading companies, including Sika AG and Mapei S.P.A., are actively investing in construction technology collaborations and developing specialized precast admixture product lines to capture premium margins within these rapidly expanding application segments.

Category-wise Insights

By Product Type

Superplasticizers dominate the global Polycarboxylate Ether market by product type, accounting for approximately 41% of the total market revenue share in 2026. This leadership closely aligns with the PCE-based superplasticizer segment’s 40.8% share in the global concrete superplasticizer market in 2025, as supported by industry data. The strong position of PCE-based superplasticizers is driven by their exceptional technical performance, particularly their ability to achieve water reduction levels of 40% in concrete mixtures.

This capability enables higher strength and improved durability in modern construction projects. In addition, these admixtures provide extended workability retention of up to 90 minutes, making them highly suitable for large-scale infrastructure and ready-mix concrete applications. Their superior compatibility with blended cement systems containing fly ash, slag, and silica fume further supports their use in sustainable construction practices. Compliance with major global standards such as ASTM C494, EN 934-2, and IS 9103 has also strengthened their adoption in public infrastructure projects worldwide. High-Range Water Reducers (HRWR) represent the fastest-growing product sub-segment due to rising demand for ultra-high-performance concrete and precast construction applications.

By Form

The liquid form segment leads the global Polycarboxylate Ether market, capturing approximately 68% of the total form segment revenue in 2026. Liquid PCE formulations are widely preferred because they offer operational convenience, easy dosing, and efficient mixing during concrete production. These formulations integrate seamlessly with automated dosing systems used in modern batching plants, which allows precise measurement and consistent admixture performance. Their ability to disperse effectively when mixed directly with concrete mix water further enhances their reliability in large construction projects.

According to the European Ready-Mixed Concrete Organisation (ERMCO), automated admixture dispensing systems are installed in most modern concrete batching plants across Europe, reinforcing the dominance of liquid PCE formulations in large-scale concrete production. In the Asia Pacific region, particularly in China and India, where the number of ready-mix concrete plants is rapidly expanding, liquid PCE remains the most commonly procured format. Although powder and granular forms are witnessing growth in export-oriented and remote markets where transportation of liquids is challenging, their overall market share remains significantly smaller than that of liquid formulations.

By End-user

Infrastructure development represents the largest end-use segment in the global Polycarboxylate Ether market, accounting for approximately 38% of total end-use revenue in 2026. Large infrastructure projects, including highways, bridges, tunnels, airports, railways, dams, and water treatment facilities, require high-performance concrete that delivers superior durability, strength, and long-term resistance to environmental and chemical exposure. PCE-based superplasticizers play a critical role in achieving these performance requirements by enabling low water-to-cement ratios while maintaining excellent workability.

This technical advantage makes them a preferred admixture in many national infrastructure construction standards. Major regulatory frameworks, such as those issued by the Federal Highway Administration (FHWA) in the United States and the EN 1992 design standards in Europe, encourage the use of high-performance admixtures in critical civil engineering applications. These standards directly contribute to the strong demand for PCE products in infrastructure construction. Meanwhile, commercial construction is the fastest-growing end-use segment, driven by rapid urbanization and the increasing number of high-rise buildings and mixed-use developments across China, India, and the Middle East.

Regional Insights

North America Polycarboxylate Ether Trends

North America is one of the most mature and technologically advanced regional markets for Polycarboxylate Ether (PCE) products. Market growth is largely driven by the United States’ strong construction chemicals innovation ecosystem, strict concrete performance standards enforced by ASTM International, and sustained infrastructure spending under the Infrastructure Investment and Jobs Act of 2021, which allocates about US$1.2 trillion for public construction projects.

Technical guidelines from the American Concrete Institute (ACI) and bridge construction specifications from the American Association of State Highway and Transportation Officials (AASHTO) highlight high-range water reducer performance standards that strongly encourage the use of PCE-based admixtures in federally funded infrastructure. Leading suppliers such as BASF SE, Sika AG, and GCP Applied Technologies (now part of Saint-Gobain) maintain strong market presence through extensive distribution networks and technical support services. Additionally, the expanding precast and prefabricated construction sector in the U.S., driven by labor shortages and efficiency needs, is increasing demand for specialized PCE formulations that support early strength development and high surface quality in factory-controlled casting environments.

Europe Polycarboxylate Ether Market Trends

Europe is considered a technology-driven market for Polycarboxylate Ether chemistry, supported by advanced construction industries in Germany, France, the United Kingdom, and Italy. The region also benefits from strict environmental regulations and well-established chemical manufacturing capabilities. Germany hosts the headquarters of BASF SE and serves as a key European hub for PCE monomer research and development. In May 2025, BASF introduced Pluriol A 2400 I at its Ludwigshafen facility, highlighting integrated PEG-to-PCE production and a local sourcing model designed to reduce carbon emissions.

The European Standard EN 934-2 for concrete admixtures requires strict testing related to chloride content and performance, raising quality benchmarks across the EU construction sector. In addition, the EU Renovation Wave Strategy aims to renovate 35 million buildings by 2030 under the European Green Deal, creating strong demand for PCE-based repair mortars and plasticized concrete. Companies such as Sika AG and Mapei S.P.A. continue expanding their distribution and application technology centers to provide on-site support.

Asia Pacific Polycarboxylate Ether Market Trends

Asia Pacific is the largest and fastest-growing regional market for Polycarboxylate Ether globally. Growth is supported by China’s large construction industry, India’s increasing infrastructure investments, and rapidly developing urban sectors across ASEAN countries. China remains the world’s biggest consumer of PCE, supported by major infrastructure expansion under the China 14th Five-Year Plan and the country’s position as the largest producer of ready-mix concrete, with more than 7,000 commercial plants operating nationwide.

Domestic manufacturers such as Henan Kingsun Chemical Co., Ltd. and Hangzhou Lans Concrete Admixture Inc. have built strong cost-efficient production capacity to supply both domestic and export markets. India is the fastest-growing PCE market in the region, supported by the National Infrastructure Pipeline, Smart Cities Mission, and PM Gati Shakti National Master Plan. These programs are driving investment in roads, railways, airports, and ports, which significantly increases demand for high-performance concrete admixtures.

Competitive Landscape

The global Polycarboxylate Ether market is moderately fragmented and follows a two-tier competitive structure. The first tier includes large multinational chemical companies such as BASF SE, Sika AG, Arkema SA, and Mapei S.P.A. These companies differentiate themselves through vertically integrated ethoxylation facilities, advanced monomer technologies, strong research capabilities, and comprehensive technical service networks. They also maintain strict compliance with global construction chemical regulations, which strengthens their market position.

BASF’s iPEG investment in Ludwigshafen and Sika’s partnerships with engineering, procurement, and construction companies highlight the industry’s focus on innovation and collaboration. The second tier consists of regional manufacturers, particularly in China and India, that compete mainly through cost advantages and local distribution networks. Companies such as Himadri Speciality Chemicals Ltd. and Chemocon Tecsys Pvt. Ltd. are successfully expanding in mid-market and export segments by offering competitively priced products and flexible supply capabilities.

Key Developments:

- In May 2025: BASF SE introduced Pluriol® A 2400 I, an advanced isoprenol-PEG (iPEG) monomer used in third-generation polycarboxylate ether (PCE) superplasticizers. Produced at its Ludwigshafen site, the innovation improves concrete flow performance and durability while supporting reduced CO2 emissions through BASF’s backward-integrated manufacturing process.

- In January 2025: BASF SE and Sika AG collaborated to launch Baxxodur EC 151, a bio-based amine epoxy hardener designed for sustainable industrial flooring systems. The product enhances durability, chemical resistance, and environmental performance, reinforcing the companies’ joint focus on sustainable construction chemistry innovation.

- In April 2023: Sika AG announced the expansion of its superplasticizer production facility in India to meet growing demand for PCE-based concrete admixtures. The investment supports infrastructure development projects and strengthens Sika’s supply capacity and long-term growth strategy across the Asia Pacific construction chemicals market.

Companies Covered in Polycarboxylate Ether Market

- Sika AG

- BASF SE

- Abadgaran Group

- Arkema SA

- Mapei S.P.A.

- Sakshi Chem Sciences Private Ltd.

- Fosroc International Ltd.

- TriStar Technical Co.

- Henan Kingsun Chemical Co., Ltd.

- Himadri Speciality Chemicals Ltd.

- KMT Polymers

- Chemocon Tecsys Pvt. Ltd.

- Ruia Chemicals

- Kashyap Industries

- GCP Applied Technologies

- Coatex S.A.S.

- Hangzhou Lans Concrete Admixture Inc.

- Sure Chemical Co., Ltd.

Frequently Asked Questions

The global Polycarboxylate Ether market is estimated to be valued at US$ 9.2 Billion in 2026 and is projected to reach US$ 13.6 Billion by 2033, registering a forecast CAGR of 5.7% over the period 2026 to 2033. The market recorded a historical growth rate of 4.8% CAGR between 2020 and 2025.

The primary growth drivers are the global infrastructure investment wave, anchored by the U.S. Infrastructure Investment and Jobs Act's US$ 1.2 trillion commitment and India's National Infrastructure Pipeline of INR 111 trillion, and the global construction sector's transition toward high-performance and self-compacting concrete systems, where PCE-based superplasticizers deliver 40% water reduction and 90-minute slump retention that older-generation admixtures cannot match.

The Superplasticizers segment leads the Product Type category, representing approximately 41% of total market revenue share in 2026. This is corroborated by the PCE-based segment's 40.8% revenue leadership in the global concrete superplasticizer market in 2025, driven by superior dispersing ability, workability retention, and mandatory specification alignment with ASTM C494, EN 934-2, and IS 9103 international concrete admixture performance standards.

Asia Pacific leads the global Polycarboxylate Ether market, with China as the world's largest single PCE consumer, supported by over 7,000 commercial ready-mix concrete plants nationally, and India as the fastest-growing demand market within the region, driven by the PM Gati Shakti Master Plan and Smart Cities Mission generating unprecedented demand for high-performance PCE admixtures in specification-grade infrastructure concrete.

The most significant opportunity lies in third-generation iPEG-based PCE chemistry and 3D concrete printing applications. BASF's 2025 launch of Pluriol A 2400 I at its integrated Ludwigshafen facility demonstrates the commercial viability of sustainable next-generation PCE formulations. Growing adoption of 3DCP in smart city and prefabrication programs globally is creating premium niche demand for precisely engineered, application-specific PCE rheology systems commanding significantly above-average margin profiles.

The leading companies include BASF SE, Sika AG, Arkema SA, Mapei S.P.A., Fosroc International Ltd., GCP Applied Technologies, Himadri Speciality Chemicals Ltd., Henan Kingsun Chemical Co., Ltd., Abadgaran Group, Sakshi Chem Sciences Private Ltd., Chemocon Tecsys Pvt. Ltd., Ruia Chemicals, KMT Polymers, and Kashyap Industries, among other prominent participants operating across global, regional, and local PCE production and distribution segments.