- Specialty & Fine Chemicals

- Plaster Retarder Market

Plaster Retarder Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Plaster Retarder Market by Form (Liquid, Powder), Application (Gypsum Board Manufacturing, On-Site Plastering, Decorative Plaster & Moldings, Medical & Orthopedic Casting), End-Use (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Plaster Retarder Market Share and Trends Analysis

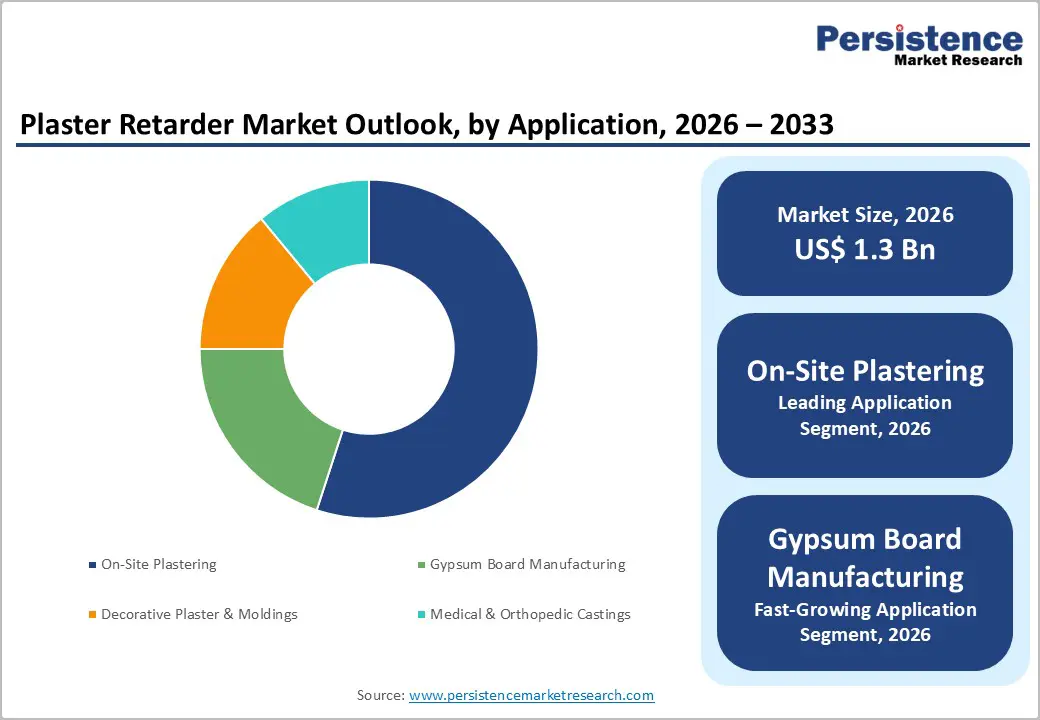

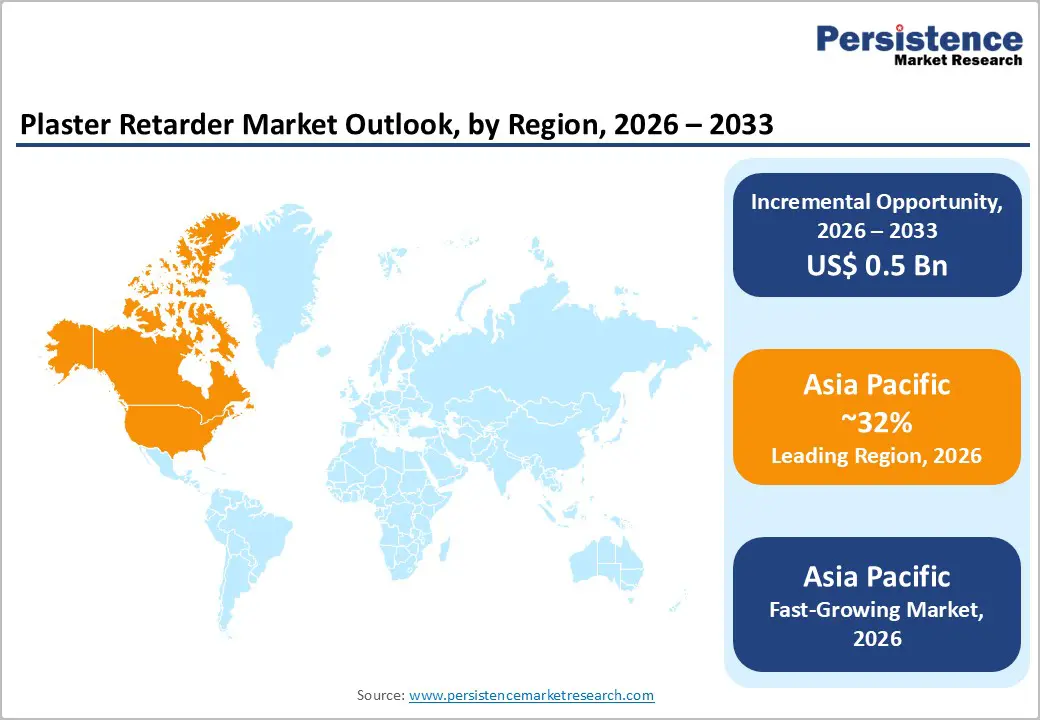

The global plaster retarder market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 1.8 billion by 2033, growing at a CAGR of 4.7% during the forecast period 2026−2033. Market growth is primarily driven by the construction sector's sustained expansion, particularly in Asia Pacific and the Middle East, where rapid urbanization is intensifying demand for plaster-based finishing systems. The global green building movement is simultaneously elevating the adoption of gypsum-based solutions, which require precisely formulated retarders to achieve optimal workability and setting times. Regulatory frameworks favoring low-VOC and eco-compatible construction chemistries are further supporting market value.

Key Industry Highlights

- Regional Leadership: Asia Pacific is likely to be both the leading and fastest-growing regional market from 2026 to 2033, accounting for approximately 32% market share in 2026, supported by rapid urban development and expanding construction activity.

- Leading End-Use: Residential is slated to lead by commanding approximately 42% market revenue share in 2026, owing to continuous housing development across both developed and emerging economies.

- Fastest-growing End-Use: Commercial is likely to be the fastest-growing segment during the 2026-2033 forecast period, driven by the expanding pipeline of hospital, educational facility, data center, and mixed-use development projects.

- Leading & Fastest-growing Application: On site plastering represent the dominant application segment, capturing approximately 55% revenue share in 2026, while gypsum board manufacturing is expected to be the fastest-growing segment over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

|

Key Insights |

Details |

|

Plaster Retarder Market Size (2026E) |

US$ 1.3 Bn |

|

Market Value Forecast (2033F) |

US$ 1.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

DRO Analysis

Accelerating Global Construction Activity and Urbanization

Urban expansion is reshaping construction demand across regions, and developers are continuously scaling up residential and commercial projects to accommodate growing city populations. Governments are introducing large housing programs, transport corridors, and smart city initiatives, which are steadily increasing the need for efficient building materials. This shift is pushing contractors to adopt gypsum-based plasters for faster application and improved surface quality. Within this process, plaster retarders are playing a critical role by controlling setting time and ensuring smooth workability during large-scale operations. As construction teams are handling wider surface areas and tighter project timelines, these additives are supporting consistent application and reducing material waste. Emerging economies such as India, Southeast Asia, and the Gulf Cooperation Council (GCC) region are driving this transformation through sustained infrastructure investments and urban housing expansion.

Construction activity is also evolving in terms of scale, complexity, and execution speed, which is strengthening the importance of performance-enhancing chemicals. Builders are prioritizing materials that are improving productivity without compromising finish quality, especially in high-rise and mass housing developments. Plaster retarders are enabling better control over curing cycles, which is helping workers maintain uniformity across extended application periods. This trend is encouraging manufacturers to refine formulations that are adapting to different climatic conditions and project requirements. Large infrastructure pipelines are progressing and urbanization is accelerating, demand for gypsum plasters and supporting additives such as retarders will have expanded significantly, reinforcing their role in modern construction practices.

Rising Demand for Gypsum-Based Building Materials and Prefabrication

Gypsum-based materials are gaining strong acceptance in modern construction as builders are focusing on safety, comfort, and environmental performance. Products such as drywall, plasterboards, and decorative plasters are offering fire resistance, sound insulation, and reduced environmental impact, which is encouraging their wider use across residential and commercial projects. Developers are selecting these materials to meet building codes and sustainability goals while maintaining cost efficiency. This growing preference is increasing the need for additives that can improve handling and application quality. Plaster retarders are becoming essential in this context as they are extending working time and ensuring smoother finishes during installation.

Industrial construction methods are also shaping demand patterns, especially as prefabrication is becoming more common across global markets. The prefabricated construction segment is driving the need for standardized materials that can perform reliably under controlled manufacturing conditions. In these environments, plaster retarders are supporting uniform setting behavior and enabling precise application during automated and mechanized processes. Manufacturers are developing advanced formulations that are adapting to varying climatic conditions and production requirements. Supply chains are becoming more organized and quality expectations are rising. The role of retarders will have strengthened significantly in ensuring consistent output and operational efficiency across large-scale construction systems.

Technical Complexity in Formulation and Application

Plaster retarders are requiring precise formulation to deliver consistent performance across changing environmental and application conditions. Temperature, humidity, substrate type, and water ratios are influencing how these additives behave during mixing and application. Manufacturers are developing advanced chemical compositions to ensure stable setting times under different site conditions. Even small errors in dosing or incompatibility with gypsum systems can lead to delayed curing, uneven surfaces, or reduced strength. These risks are increasing the need for careful material selection and controlled usage practices. Contractors are facing higher accountability since poor performance can affect structural reliability and finishing quality. This complexity is making plaster retarders less accessible for users who lack technical understanding or proper guidance.

Adoption challenges are becoming more visible in regions where construction practices are less standardized and heavily dependent on manual labor. Informal builders are often working without formal training, which is limiting their ability to handle specialized additives effectively. In areas such as Sub-Saharan Africa and parts of Southeast Asia, technical training infrastructure is still developing and not widely accessible. This gap is restricting the correct application of retarders and is slowing their penetration in cost sensitive markets. Industry participants are recognizing the need for skill development programs and on-site guidance to improve usage practices. Structured training systems and better awareness will have supported safer adoption and will have reduced performance related risks across diverse construction environments.

Competition from Alternative Setting Control Technologies

Construction material innovation is reshaping how plaster systems are being designed and used across modern projects. Manufacturers are offering ready mix plasters and pre blended compounds that already include performance enhancing additives such as retarders within controlled formulations. These integrated systems are ensuring uniform quality, reducing on site errors, and simplifying application processes for contractors. Smart release admixture technologies are further improving performance by regulating the timing of chemical reactions during application. This shift is reducing the need for separate retarder products, since functionality is already embedded within the material. Contractors are increasingly preferring these solutions because they are minimizing variability and improving workflow efficiency during large scale construction activities.

Adoption of these advanced systems is accelerating in developed regions where construction practices are highly standardized and efficiency remains a key priority. Markets in Western Europe and North America are emphasizing precision, repeatability, and reduced dependency on manual adjustments during application. Large contractors are choosing integrated gypsum systems to maintain consistency across projects and to meet strict quality benchmarks. This trend is gradually limiting the use of standalone retarder additives, especially in organized construction environments. Material suppliers are responding by focusing on innovation within complete system solutions rather than individual components.

Innovation in Bio-Based and Sustainable Retarder Chemistries

Sustainability requirements are increasingly shaping material innovation in the construction chemicals sector. Manufacturers are developing bio derived plaster retarders that are aligning with environmental standards while maintaining functional performance. Formulations based on protein hydrolysates, citric acid, and lignosulfonate derivatives are providing effective control over setting time while reducing environmental impact. These alternatives are gaining attention because they are supporting lower emissions and improved biodegradability compared to conventional synthetic options. Builders and project developers are actively seeking materials that are meeting green building criteria without compromising application efficiency. This shift is encouraging continuous research into renewable raw materials and cleaner production processes for plaster additives.

Market dynamics are also favoring companies that are prioritizing sustainable product portfolios and certification compliance. Eco labels such as Cradle to Cradle and Nordic Swan Ecolabel are becoming important decision factors in project specifications, especially in environmentally regulated regions. Manufacturers that are securing these certifications are strengthening their competitive position and are attracting premium customers focused on sustainable construction practices. Demand for bio-based retarders is expanding within green building projects, where material transparency and lifecycle impact are closely evaluated. Companies that are investing early in these technologies will have established strong market differentiation and will have gained access to high value projects that prioritize environmental responsibility and long-term performance.

Mechanized and Spray Plaster Application Growth

Mechanized plaster application is expanding across construction sites as contractors are focusing on faster execution and reduced dependence on manual labor. Spray based systems are enabling uniform coverage over large surfaces, which is improving productivity in both residential and commercial projects. This transition is increasing the demand for specialized plaster retarders that can perform reliably under machine driven conditions. These systems are requiring precise control over working time to ensure continuous flow and smooth finishing during application. Standard formulations are often struggling to maintain consistency in such environments, especially when pump pressure and material flow are varying during operation. This gap is pushing manufacturers to design advanced retarder chemistries that are aligning with the technical needs of mechanized equipment.

Performance expectations are also becoming more stringent as construction processes are becoming more automated and quality focused. Spray grade retarders are needing strong pump compatibility, stable viscosity, and predictable setting behavior to support uninterrupted operations. Manufacturers are investing in formulation improvements that are enhancing dispersion, reducing clogging risks, and ensuring uniform curing across surfaces. These innovations are helping suppliers differentiate their offerings in a competitive market. This focus on specialized products is also enabling premium pricing, as contractors are valuing efficiency, reliability, and reduced operational risk.

Category-wise Analysis

End-Use Insights

Residential end-uses are anticipated to dominate in 2026, commanding approximately 42% of the plaster retarder market revenue share, supported by continuous housing development across both developed and emerging economies. Government initiatives such as India’s Pradhan Mantri Awas Yojana and the United States Infrastructure Investment and Jobs Act (IIJA) are driving steady construction activity, which is increasing demand for gypsum finishing systems. High plaster usage across walls, ceilings, and decorative elements is strengthening retarder consumption. Market structure is remaining highly fragmented, with small contractors relying on distributor networks for procurement. This trend is encouraging supplier focus on distribution reach, technical training, and brand visibility among applicators.

Commercial is likely to be the fastest-growing segment during the 2026-2033 forecast period, driven by the pipeline of hospital, educational facility, data center, and mixed-use development projects. Commercial specifications increasingly mandate high-performance plaster systems with precise set-time control, particularly for fire-rated assemblies and acoustic plaster applications, driving premium retarder consumption. Large commercial contractors in this segment tend to operate with centralized procurement and approved product lists, creating durable, high-volume sales opportunities for retarder suppliers who achieve specification.

Application Insights

On-site plastering is set to hold an estimated 55% of the plaster retarder market share in 2026, due to its widespread use across residential and commercial construction. Large wall and ceiling areas are requiring controlled setting times to ensure smooth application and consistent finishes. Contractors are depending on retarders to extend workability during manual and mechanized plastering processes. Demand is increasing further with rising urban construction and renovation activities. The segment is also benefiting from strong distributor networks that are supplying materials directly to small and mid-sized contractors, making retarders easily accessible across diverse project types.

Gypsum board manufacturing is expected to be the fastest-growing segment over the 2026-2033 forecast period. Manufacturers are integrating retarders within production lines to control setting behavior and maintain product uniformity. Automated processes are requiring precise chemical performance to ensure consistency in board strength and surface quality. Demand is rising with the growing adoption of prefabricated building systems and drywall solutions. Production facilities are scaling operations to meet increasing construction needs, which is driving continuous innovation in retarder formulations tailored for high-speed manufacturing environments.

Regional Insights

Asia Pacific Plaster Retarder Market Trends

Asia Pacific is likely to be both the leading and fastest-growing for plaster retarders through 2033, claiming approximately 32% of the market share in 2026. Its leadership is powered by rapid urban development and expanding construction activity. China is leading regional demand due to its large-scale infrastructure projects, strong gypsum board manufacturing base, and continued focus on urban housing development. India is following closely, driven by government initiatives such as affordable housing programs and smart city development. The construction sector in India is becoming more organized, with builders increasingly adopting drywall and plasterboard systems. This transition is raising the need for reliable additives that can improve application efficiency and finish quality. Growing awareness of modern construction materials is also encouraging wider use of gypsum-based systems across urban and semi urban areas.

The region is also contributing to market expansion through steady economic growth and rising housing demand. Japan is maintaining a high value market through advanced construction practices and the use of gypsum assemblies in earthquake resistant structures. Nations within the ASEAN such as Vietnam, Indonesia, and the Philippines are attracting foreign direct investment (FDI), which is supporting infrastructure and residential development. Regional manufacturers are benefiting from cost advantages in production, especially in China and India, which is strengthening their competitive position. Global companies are focusing on product quality and brand strength to capture premium demand, which will have driven significant market expansion across Asia Pacific.

Top of Form

Bottom of Form

Europe Plaster Retarder Market Trends

Europe is holding a leading position in the plaster retarder market by value, supported by a mature construction ecosystem and strong focus on quality standards. Germany is driving regional demand due to its advanced building practices, high renovation activity, and widespread use of mechanized plaster application systems. France and the United Kingdom are also contributing significantly through steady residential and commercial development. Spain is emerging as a growing market, supported by infrastructure funding and rising hospitality construction linked to tourism expansion. Across the region, builders are emphasizing efficiency and surface finish quality, which is increasing reliance on high performance gypsum systems and supporting additives.

Regulatory frameworks are shaping market dynamics by enforcing consistent material standards and safety requirements. The European Union (EU) Construction Products Regulation (CPR) and European Chemicals Agency Registration, Evaluation, Authorization and Restriction of Chemicals (ECHA REACH) are ensuring uniform compliance across member states. These regulations are encouraging manufacturers to enhance product reliability and environmental performance. Sustainability initiatives such as the European Union Green Deal and the Renovation Wave program are promoting large scale building upgrades and energy efficient construction. European producers are leading innovation in bio-based retarders and certified sustainable solutions, which will have strengthened the region’s role as both a demand center and a global benchmark for advanced construction materials.

North America Plaster Retarder Market Trends

North America is maintaining a strong position in the market for plaster retarders. The United States is leading regional demand due to ongoing residential renovation, commercial space upgrades, and infrastructure development. Federal initiatives such as the IIJA are continuing to stimulate construction activity, which is increasing the consumption of gypsum systems and supporting additives. Builders are focusing on durability, efficiency, and finish quality, which is strengthening the role of retarders in both new construction and refurbishment projects. Market maturity is encouraging the adoption of advanced materials that can deliver reliable performance across diverse applications.

Regulatory oversight is shaping product development and market preferences across the region. Agencies such as the Environmental Protection Agency (EPA) and the Occupational Safety and Health Administration (OSHA), along with state level bodies, are enforcing strict standards on emissions and chemical safety. These requirements are driving the shift toward low emission and bio-based retarder formulations. The distribution landscape is highly organized, with building material wholesalers and specialty chemical distributors playing a central role in product availability. Growth in prefabricated and modular construction is creating new opportunities for tailored retarder solutions that can perform in controlled manufacturing environments, especially in multifamily housing and data infrastructure projects.

Competitive Landscape

The global plaster retarder market structure is moderately fragmented, dominated by leading players such as Sika AG, BASF SE, Nouryon, Mapei S.p.A., and Ardex Group. These players collectively capture 35-40% of the market share. The competitive landscape is featuring a mix of global specialty chemical companies, regional construction chemical providers, and numerous local manufacturers catering to domestic markets.

Competition is largely driven by product performance, technical support, and dependable supply chains. Companies are focusing on delivering consistent quality and application efficiency to strengthen their market position. Consolidation is progressing at a steady pace, with firms pursuing targeted acquisitions to expand regional reach and enhance product portfolios across diverse construction segments.

Key Industry Developments

- Novastar gypsum retarder is an amino-based chemical additive used in gypsum materials to control and delay setting time by slowing the hydration process, improving workability and application flexibility. It enhances flowability and extends working time for applications such as plaster, self-leveling compounds, and gypsum boards, without compromising strength or final material performance.

- KDR-18 is a protein-based gypsum retarder used in dry-mix gypsum systems to precisely control and extend setting time, improving workability and allowing flexible application durations. It delivers strong retarding efficiency at low dosage while minimizing strength loss, enhancing productivity and surface quality in applications such as plasters, joint compounds, and gypsum-based coatings.

Companies Covered in Plaster Retarder Market

- Sika AG

- BASF SE

- Nouryon

- Mapei S.p.A.

- Ardex Group

- Saint-Gobain S.A.

- Knauf Group

- USG Corporation

- GCP Applied Technologies

- Chryso Group

- Sobotec Ltd.

- Triveni Interchem Pvt. Ltd.

- COMEX Group

- Fosroc International

- Imerys S.A.

Frequently Asked Questions

The global plaster retarder market is projected to reach US$ 1.3 billion in 2026.

The market is driven by rapid urbanization and expanding construction activity, together with rising demand for eco‑friendly, high‑performance plaster systems.

The market is poised to witness a CAGR of 4.7% from 2026 to 2033.

Major opportunities lie in bio‑based and phosphate‑free retarders for green building standards, and in integrating specialized retarders into prefabricated.

Sika AG, BASF SE, Nouryon, Mapei S.p.A., and Ardex Group are some of the key players in the market.