- Beverages

- Pisco Market

Pisco Market Size, Share, and Growth Forecast, 2026 - 2033

Pisco Market by Origin (Chile, Peru), Product Type (Pisco Puro, Mosto Verde, Others), Sales Channel (Supermarket/Hypermarket, Specialty Stores, Online Stores, Others), and Regional Analysis for 2026 - 2033

Pisco Market Size and Trends Analysis

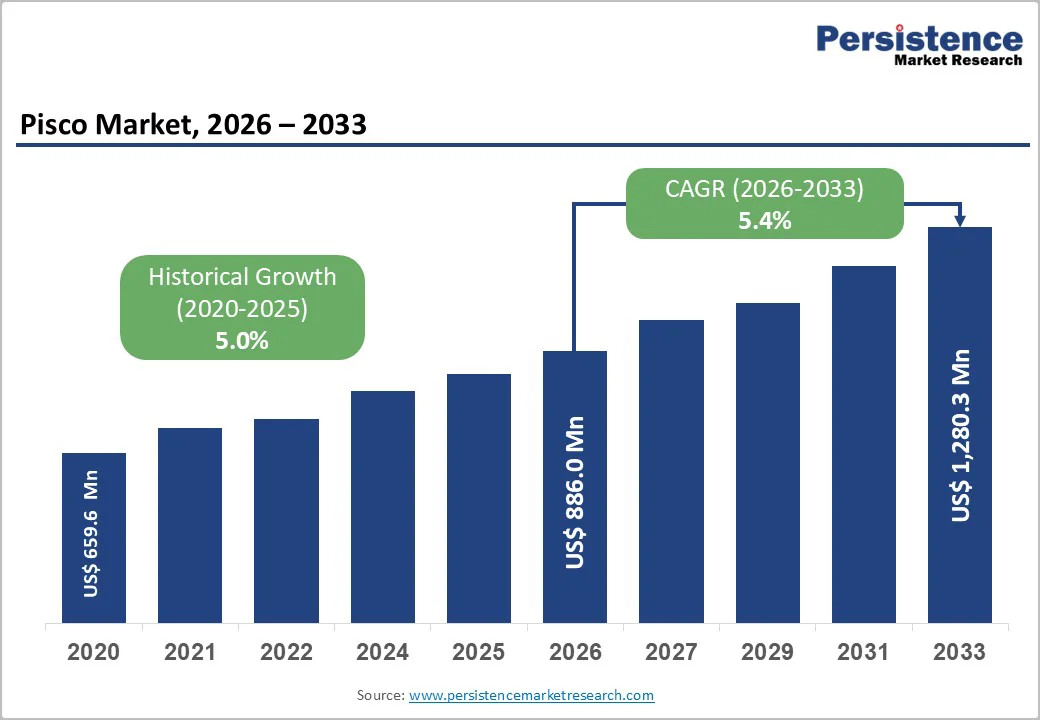

The global pisco market size is likely to be valued at US$886.0 million in 2026. It is expected to reach US$1,280.3 million by 2033, growing at a CAGR of 5.4% from 2026 to 2033, driven by the increasing prevalence of premium spirit consumption, rising demand for authentic grape-based brandies in cocktails, and advancements in artisanal distillation techniques.

Rising demand for versatile, aromatic pisco, particularly in pisco sours and premium cocktails, is driving broader adoption across consumer segments. Innovations in puro and mosto verde variants are enhancing uptake by delivering cleaner, more complex flavor profiles. Growing global recognition of pisco as a key Latin American heritage spirit continues to fuel market expansion.

Key Industry Highlights:

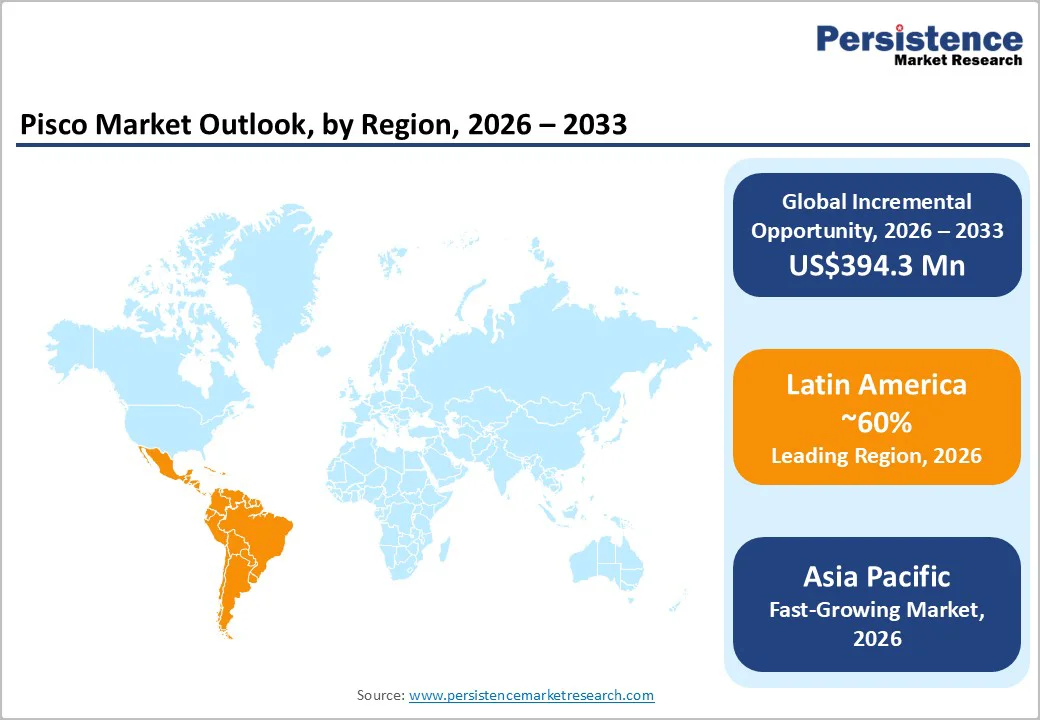

- Leading Region: Latin America is projected to dominate, with over 60% share in 2026, driven by tradition, premiumization, and evolving consumer preferences. Peru and Chile remain the core producers, focusing on high-quality, artisanal products that showcase unique grape varieties and terroirs.

- Fastest-growing Region: Asia Pacific, fueled by rising affluence, expanding nightlife, and growing investments in imported spirits in China and Japan.

- Dominant Origin: Peru, holding approximately 55% of the market share, as it provides traditional authenticity and regulatory protection for the pisco denomination.

- Leading Product Type: Pisco Puro to account for over 50% of the market revenue in 2026, due to single-varietal purity and versatility in classic cocktails.

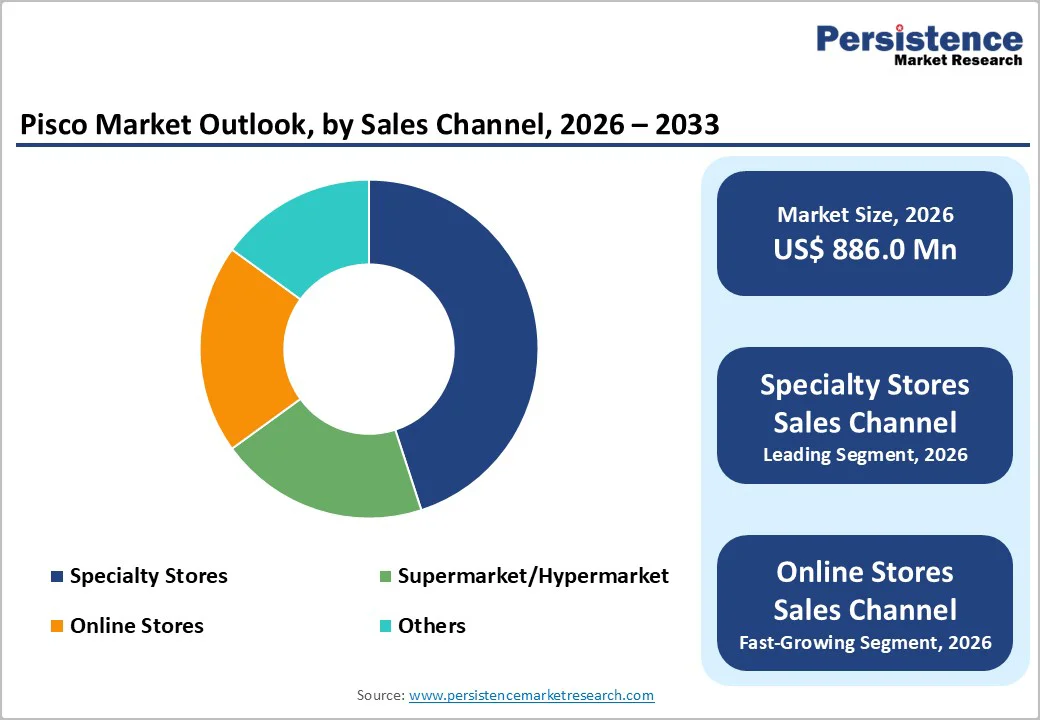

- Leading Sales Channel: Specialty stores, to contribute nearly 40% of the market revenue, due to expert curation and premium positioning.

| Key Insights | Details |

|---|---|

|

Pisco Market Size (2026E) |

US$886.0 Mn |

|

Market Value Forecast (2033F) |

US$1,280.3 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Interest in Authentic and Origin-Protected Spirits

There is a growing preference for authentic, origin-protected spirits that convey a distinct geographic identity and cultural heritage. This trend aligns with the broader movement toward experiential consumption, where consumers seek not just a beverage but a meaningful connection to a place, tradition, and story. In the spirits sector, geographic indications (GIs) and origin certifications signal that a product is produced using established methods in a recognized region, fostering trust and enhancing perceived value. Pisco, with its protected status in Peru and Chile, directly benefits from this trend.

Spirits with GI labels often command premium prices, as consumers associate them with authenticity and traceability to traditional production regions. A 2024 global beverage survey found that 58% of premium spirits buyers are willing to pay more for products verified as originating from a specific area or made using traditional methods. Peru’s legal requirements for pisco production, which restrict its creation to designated regions and specific grape varieties, reinforce its connection to terroir and artisanal craftsmanship. These protections help distinguish authentic Peruvian pisco in export markets, where demand for origin-verified products is rising.

Regulatory & Classification Challenges Across Markets

Regulatory and classification inconsistencies across international markets pose a significant challenge to the global growth of the pisco market. Varying rules and labeling requirements can delay market entry, increase costs, and create confusion for both producers and consumers. As a traditional grape brandy with protected origins in Peru and Chile, pisco exporters must navigate complex regulations that differ widely by country. In some markets, compliance with geographical indication (GI) laws, verifying origin and production methods, is strictly enforced, while in others, “pisco” may be treated as a generic spirit category, undermining its authenticity and marketing value.

Producers face higher legal and certification expenses and must adapt marketing strategies for each market, limiting the speed and scale of international expansion. This regulatory complexity slows broader consumer adoption and diminishes pisco’s competitive positioning compared with more standardized spirit categories.

Developments in Artisanal and Sustainable Delivery Platforms

Innovations in artisanal and sustainable pisco production are reshaping the global spirits market by addressing key challenges, including mass-production uniformity and environmental impact. Artisanal pisco focuses on small-batch craftsmanship, allowing terroir-driven flavor profiles for premium bars while reducing reliance on industrial blending. Techniques such as foot-treading, natural fermentation, single-distillation, and clay-pot aging enhance complexity, deepen flavor, and minimize homogenization, thereby lowering commoditization risks for brands and heritage-focused campaigns.

Sustainable production practices, including organic vineyards, water-neutral stills, recycled glass packaging, and carbon-offset shipping, promote eco-conscious branding by reducing environmental footprints, serving as a first line of defense against greenwashing. These approaches eliminate chemical inputs, preserve authenticity, and enable direct-to-consumer distribution without intermediaries, making them ideal for large-scale export strategies. Emerging technologies such as blockchain traceability, biodynamic farming, and VLP-based labeling further strengthen provenance verification and consumer trust.

Category-wise Analysis

Origin Insights

Peru is expected to lead the pisco market, capturing around 55% of the revenue share in 2026. Its leadership is supported by stringent denomination regulations, aromatic grape varieties, and heritage recognition, making it the preferred source for authentic pisco. Peruvian production standards ensure purity, quality, and global recognition, supporting large-scale export initiatives. For instance, companies such as Pisquera Tulahuen SpA supply Peruvian pisco to international bars, combining tradition with scalable cocktail programs.

Chile is projected to be the fastest-growing segment, driven by its diverse styles and increasing use of acholado blends. Its versatile flavor profiles make it well-suited for mixology, expanding its appeal in global markets. Ongoing innovations in Chilean distillation are enhancing accessibility and adoption across North America and Europe, where demand for approachable, value-oriented pisco is rising. To support this growth, the Chilean government launched the “Chilean Pisco: First Spirit” export campaign, promoting diverse production styles, including acholado and blended varietals, and positioning Chilean pisco as an ideal choice for international cocktails and mixology programs.

Product Type Insights

Pisco Puro is expected to dominate, accounting for around 50% of revenue share in 2026, driven by its single-grape purity, established traditional programs, and strong international demand for classic Pisco Sours. Its prominence continues as bars and mixologists increasingly emphasize authentic, heritage-driven recipes. The growing interest in Mosto Verde and other premium offerings underscores the rising focus on tiered product segments. Pisco Puro, produced entirely from a single grape variety, most commonly Quebranta, is regarded as the benchmark expression of Peruvian pisco. Its unblended character makes it a cornerstone for Peru’s iconic Pisco Sour, which has become a global bar staple and a key driver of consumer interest in heritage spirits.

Mosto Verde is likely to be the fastest-growing segment, fueled by rising demand for premium sipping experiences and the expansion of partially fermented luxury variants in high-end bars. The shift toward richer, more complex flavor profiles, along with enhanced aging techniques, is accelerating adoption. Limited releases and barrel-finished expressions entering collector and connoisseur markets further support growth. Brands such as Pisco Portón, Mosto Verde, and Barsol Supremo Mosto Verde Italia are marketed internationally as premium spirits, ideal for both classic cocktails such as the Pisco Sour and innovative mixology creations, while also appealing to enthusiasts who enjoy them neat. These expressions often command premium pricing and feature prominently on curated spirits menus at boutique bars and specialty retailers.

Sales Channel Insights

Specialty stores are projected to lead the market, accounting for nearly 40% of revenue in 2026, as they remain key destinations for curated selections, premium offerings, and expertly managed spirit aisles that require knowledgeable staff. Their strengths in product expertise, tasting events, and handling of rare or high-margin bottles drive higher sales. Specialty retailers are spearheading Pisco Puro launches and facilitating emerging Mosto Verde trials. For example, ABC Fine Wine & Spirits in the U.S. offers extensive premium selections, educational support, and events highlighting artisanal and region-specific products, boosting visibility and sales across premium categories.

Online stores are expected to be the fastest-growing channel, supported by a strong digital presence and expanding subscription-based models. They provide convenient, quick, and contact-free deliveries, appealing to consumers who prefer home-based purchasing. Enhanced outreach, user reviews, and wider availability of both standard and limited releases are accelerating e-commerce adoption across urban and semi-urban regions. Dedicated spirit e-commerce platforms offer “virtual aisles” for aged reserves and rare bottles, increasing accessibility for global consumers while easing the demand on physical retail spaces.

Regional Insights

Latin America Pisco Market Trends

Latin America is projected to dominate the market with over 60% share in 2026, driven by a blend of tradition, premiumization, and evolving consumer preferences. Peru and Chile remain the primary producers, with centuries-old distillation techniques underpinning both domestic consumption and exports. The market is increasingly leaning toward premium and craft offerings, as consumers seek artisanal, high-quality products that showcase distinct grape varieties and regional terroirs.

Urban consumers are fueling demand for ready-to-drink pisco cocktails and innovative flavored variants, reflecting a preference for convenience without compromising authenticity. Brands such as Pisco Portón, which emphasize small-batch, Quebranta grape-based production, cater to heritage-focused consumers, aligning with the broader Latin American trend toward craft and premium spirits.

E-commerce and online sales channels are experiencing rapid growth, particularly among younger demographics who favor low-contact, home-delivery options. This expansion is supported by digital marketing, social media campaigns, and subscription models, enabling brands to reach consumers beyond traditional urban centers and into semi-urban areas.

North America Pisco Market Trends

North America is expected to see strong growth, driven by the region’s sophisticated cocktail culture, robust R&D capabilities, and high consumer awareness of Latin spirits. Bars and mixology programs across the U.S. and Canada ensure broad accessibility of puro, mosto verde, and blended pisco. Rising demand for premium, convenient, and easy-to-mix formats is accelerating adoption, as these formats enhance versatility and reduce barriers to lesser-known spirits. Innovations in pisco production, such as stable aging, improved bottling, and cocktail-focused enhancements, are attracting substantial investment from both public and private sectors.

Government initiatives and bar-led campaigns are supporting pisco’s use as an alternative to tequila, addressing margarita fatigue, and promoting Latin fusion trends, sustaining market demand. The increasing emphasis on Chilean blends and specialty applications, particularly in bars and high-end venues, is further expanding the market’s target applications.

Europe Pisco Market Trends

Europe is being driven by rising awareness of heritage spirits, robust bar networks, and government-led wellness and promotional initiatives. Countries such as Germany, France, and the U.K. have well-established beverage frameworks that support regular mixology and encourage the adoption of innovative spirit formats, including pisco. These aromatic offerings appeal particularly to cocktail enthusiasts, flavor-conscious consumers, and export markets, enhancing engagement and market penetration.

Technological advancements in pisco production, such as precision distillation, origin-focused delivery, and refined blended variants, are further expanding market potential. European authorities are increasingly backing research and trials for both routine and specialty spirit applications, boosting market confidence. Growing demand for convenient, ready-to-drink formats aligns with the region’s focus on premium, accessible consumption and reducing reliance on vodka. Public awareness campaigns and promotional initiatives are extending reach across urban and rural areas, while producers are investing in grape quality and innovative aging methods to enhance product effectiveness.

Asia Pacific Pisco Market Trends

Asia Pacific is expected to be the fastest-growing market, driven by rising disposable incomes, growing consumer awareness, supportive government initiatives, and expanding application programs. Countries including India, China, Japan, and Southeast Asian nations are actively promoting spirit campaigns to cater to nightlife expansion and emerging fusion cocktail trends. Pisco’s exotic profile, mixability, and adaptability make it particularly appealing for large-scale bar programs in both urban and semi-urban markets.

Technological advancements are enabling the production and import of stable, high-quality pisco capable of withstanding complex logistics and minimizing flavor degradation. These innovations are vital for reaching remote venues and ensuring a consistent sensory experience. Increasing demand for food pairings, cocktail experimentation, and niche applications, such as cosmetics, is further driving growth. Public-private partnerships, rising beverage spending, and investments in import infrastructure and distribution networks are accelerating adoption. The combination of convenient delivery, enhanced aroma, and novelty appeal positions pisco as a preferred choice in the region.

Competitive Landscape

The global pisco market is characterized by competition between established heritage producers and emerging premium brands. In North America and Europe, Barsol Pisco GmbH and Catan Pisco lead the market through strong R&D, extensive distribution networks, and robust relationships with bars, supported by innovative product grades and cocktail programs. In the Asia Pacific region, Macchu Pisco LLC is gaining traction with localized offerings that enhance accessibility. Aromatic and high-quality delivery strengthens mixology applications, reduces dilution risks, and facilitates broader integration across markets. Strategic partnerships, collaborations, and acquisitions combine expertise, expand vineyard capacity, and accelerate commercialization. Premium formulations address authenticity concerns, supporting market penetration in upscale and discerning segments.

Key Industry Developments

- In September 2025, SUYO, a premium Single Origin Peruvian Pisco brand, became the first pisco to achieve B Corporation certification. Awarded by B Lab, a nonprofit promoting ethical business practices, this recognition underscores SUYO’s commitment to social and environmental responsibility alongside profitability, establishing a new sustainability benchmark within the spirits industry.

- In May 2025, Capel Pisco (Cooperativa Agrícola Pisquera Elqui Limitada), Chile’s leading and most iconic Pisco brand since 1938, made its official debut in China’s spirits market. Teaming up with Gotham East (Shanghai) Ltd, a leader in premium spirits distribution, Capel introduced its award-winning portfolio to Chinese consumers.

Companies Covered in Pisco Market

- Barsol Pisco GmbH

- Bauza

- Caravedo Piscos

- Catan Pisco

- Compañía de las Cervecerías Unidas S.A.

- Macchu Pisco LLC

- Malpaso

- Perola GmbH

- Pisquera Tulahuen SpA

Frequently Asked Questions

The global pisco market is projected to reach US$886.0 million in 2026.

The rising prevalence of premium spirit consumption and demand for authentic grape-based brandies are key drivers.

The pisco market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Advancements in artisanal and sustainable delivery platforms are the key opportunities.

Barsol Pisco GmbH, Caravedo Piscos, Macchu Pisco LLC, Pisquera Tulahuen SpA, and The Pisco People are the key players.