- Automation & Robotics

- Pin Inspection System Market

Pin Inspection System Market Size, Share, and Growth Forecast 2026 - 2033

Pin Inspection System Market by Product Type (2D Pin Inspection System, 3D Pin Inspection System), by Mode (Semi-Automatic, Automatic), by End Use Industry (Automotive Industry, Electronics Industry, Solar Industry, Others), by Regional Analysis, 2026-2033

Pin Inspection System Market Size and Trend Analysis

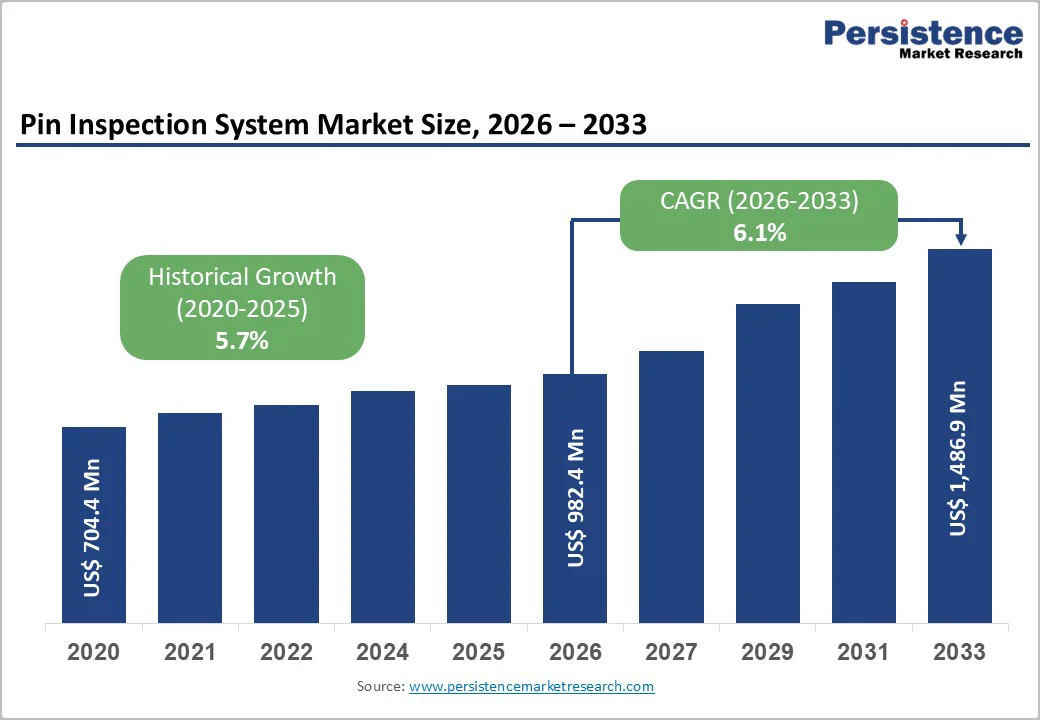

The global Pin Inspection System market size is expected to be valued at US$ 982.4 million in 2026 and projected to reach US$ 1,486.9 million by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The pin inspection system market is experiencing steady growth driven by escalating demand for precision quality control, heightened automotive industry digitalization, and the rapid adoption of automation technologies across global manufacturing facilities. Organizations increasingly recognize that manual visual inspection creates bottlenecks in production lines and introduces unacceptable human error rates ranging from 20% to 30%, prompting massive investment in automated optical inspection solutions and three-dimensional vision systems to ensure product quality and regulatory compliance. The convergence of Industry 4.0 technologies, including IoT, machine learning, and real-time analytics, has transformed pin inspection systems from standalone quality control tools into integrated components of intelligent manufacturing ecosystems, dramatically expanding market opportunities across diverse industrial sectors.

Key Market Highlights

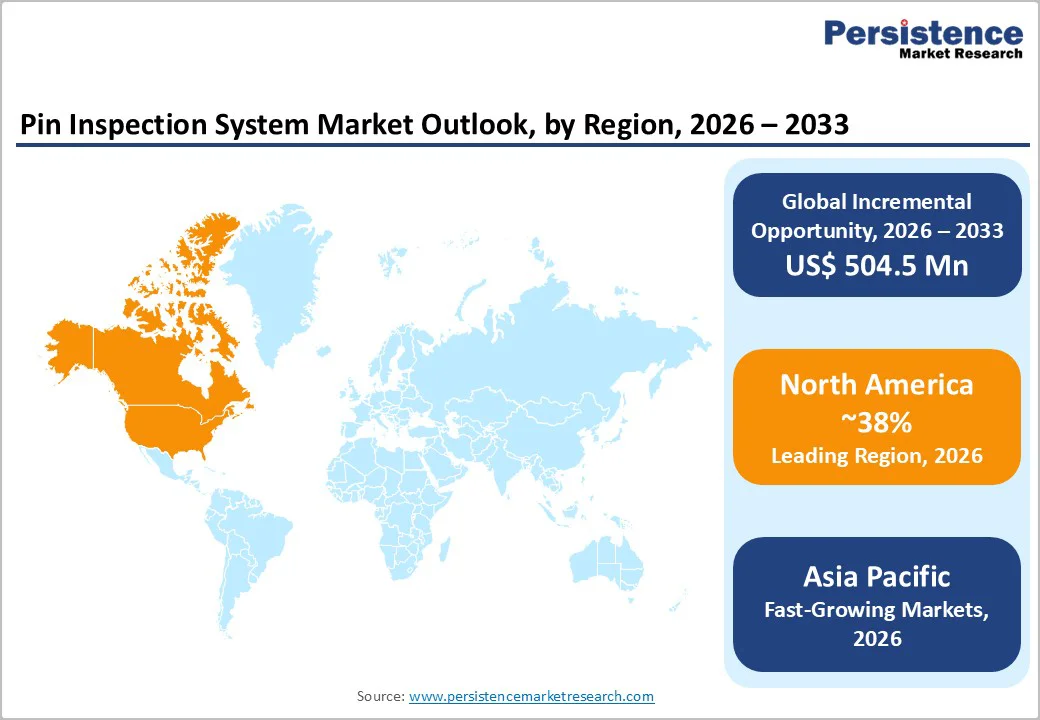

- Leading Region: North America leads the pin inspection system market with around 38% share, supported by advanced manufacturing infrastructure, strict quality regulations, and high automation adoption across automotive, electronics, and medical device industries.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, expanding at a 7.8% CAGR during 2026–2033, driven by rapid electronics manufacturing growth, automotive expansion, and increasing Industry 4.0 implementation.

- Dominant Segment: Automatic pin inspection systems dominate the market with approximately 68% share, as manufacturers prioritize high-throughput, consistent, and cost-efficient automated inspection processes.

- Fastest-Growing Segment: 3D pin inspection systems are the fastest-growing segment at an 8.4% CAGR, supported by rising demand for advanced defect detection beyond the capabilities of 2D inspection technologies.

- Key Market Opportunity: AI-enabled defect detection and automated optimization represent the strongest opportunity, enabling higher inspection accuracy, reduced false positives, and lower manual quality control workloads.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 982.4 Million |

| Market Value Forecast (2033F) | US$ 1,486.9 Million |

| Projected Growth CAGR (2026-2033) | 6.1% |

| Historical Market Growth (2020-2025) | 5.7% |

Market Dynamics

Market Growth Drivers

Rising Quality Assurance Requirements in High-Precision Manufacturing

Automotive, electronics, and semiconductor industries face mounting pressure to deliver defect-free components meeting increasingly stringent international quality standards including ISO/TS 16949, IEC 61508, and AEC-Q100 certifications. Modern vehicle platforms incorporating advanced driver assistance systems (ADAS), autonomous driving capabilities, and complex sensor networks require connector pins with micron-level precision to ensure safety and functionality, making traditional manual inspection methodologically inadequate and economically inefficient. The automotive industry reported that implementing 3D pin inspection systems reduced defect rates by 30% and improved first-pass yields by 25%, directly translating to substantial cost savings and improved customer satisfaction metrics. Miniaturization trends in consumer electronics and semiconductor packaging have made traditional 2D inspection systems insufficient for detecting volumetric defects, lifted leads, and coplanarity issues invisible to conventional optical imaging, thereby driving rapid adoption of advanced 3D vision-based inspection solutions capable of detecting defects with up to 99% accuracy. Regulatory frameworks including GDPR in Europe and California Consumer Privacy Act (CCPA) in the United States increasingly mandate comprehensive quality documentation and traceability throughout production, incentivizing manufacturers to implement automated inspection systems that provide real-time defect detection and complete audit trails for regulatory compliance verification.

Industry 4.0 Adoption and Smart Manufacturing Integration

Industry 4.0 and smart manufacturing initiatives are fundamentally transforming production line architectures globally, with 41% of manufacturers prioritizing factory automation hardware investments and 28% focusing specifically on vision system deployment according to the 2025 Deloitte Smart Manufacturing Survey. Integrated IoT sensors combined with cloud-based analytics platforms enable real-time monitoring of pin inspection system performance, allowing manufacturers to generate predictive maintenance alerts, optimize production workflows, and identify process improvement opportunities with unprecedented precision and speed. The integration of pin inspection systems with manufacturing execution systems (MES) and enterprise resource planning (ERP) platforms enables seamless data flow between quality control operations and supply chain management, facilitating automated defect tracking, root cause analysis, and implementation of corrective actions within minutes rather than days. Manufacturers implementing AI-powered visual inspection capabilities report production defect detection improvements of 50% and yield enhancements of 20% according to the IBM Institute for Business Values, creating compelling economic justifications for substantial capital investments in advanced inspection infrastructure. The rise of predictive analytics and machine learning algorithms enables pin inspection systems to continuously learn from production data, automatically adapting inspection parameters to changing material properties, component variations, and process conditions, thereby dramatically improving system flexibility and reducing false positives that plague traditional rule-based inspection approaches.

Market Restraints

High Capital Investment and Implementation Complexity

Pin inspection systems, particularly advanced 3D vision solutions with laser triangulation or structured light projection technology, require substantial capital investments ranging from $200,000 to $500,000 per installation for enterprise-grade systems with accompanying software integration and customization services. Small and medium-sized enterprises (SMEs), representing a significant portion of manufacturing capacity globally, often lack access to capital and technical expertise required to evaluate, select, and implement sophisticated inspection systems, thereby constraining market expansion within this critical customer segment. The integration of pin inspection systems into existing production lines demands extensive engineering effort, specialized programming knowledge, and manufacturing line downtime that disrupts production schedules and introduces implementation risks that deter capital-constrained organizations from pursuing automation initiatives. Legacy manufacturing facilities operating with aging production infrastructure face substantial retrofit costs and compatibility challenges when attempting to integrate modern vision-based inspection systems, frequently necessitating complete production line reconfiguration that exceeds available budgets and management risk tolerance thresholds. Technical expertise required to operate, maintain, and continuously optimize advanced inspection systems remains scarce globally, creating bottlenecks in system adoption and forcing manufacturers to invest heavily in employee training programs, technical support services, and consulting engagements to maximize return on technology investments.

Labor Skill Gaps and Cybersecurity Vulnerabilities

The manufacturing sector faces critical shortages of skilled technicians qualified to troubleshoot machine vision systems, configure advanced algorithms, and optimize vision-based inspection processes, constraining deployment velocity and creating dependency on high-cost consulting services and equipment vendors. Connected inspection systems generate massive volumes of production data including component specifications, defect patterns, and proprietary manufacturing processes that create attractive targets for industrial espionage and cyberattacks, necessitating comprehensive data security measures and cybersecurity protocols that increase implementation costs and operational complexity. Manufacturing executives express concerns regarding data privacy, intellectual property protection, and cybersecurity resilience when deploying cloud-connected vision systems that transmit sensitive manufacturing data external to facility boundaries, creating hesitancy to adopt fully integrated Industry 4.0 solutions despite acknowledged operational benefits and cost savings potential.

Market Opportunities

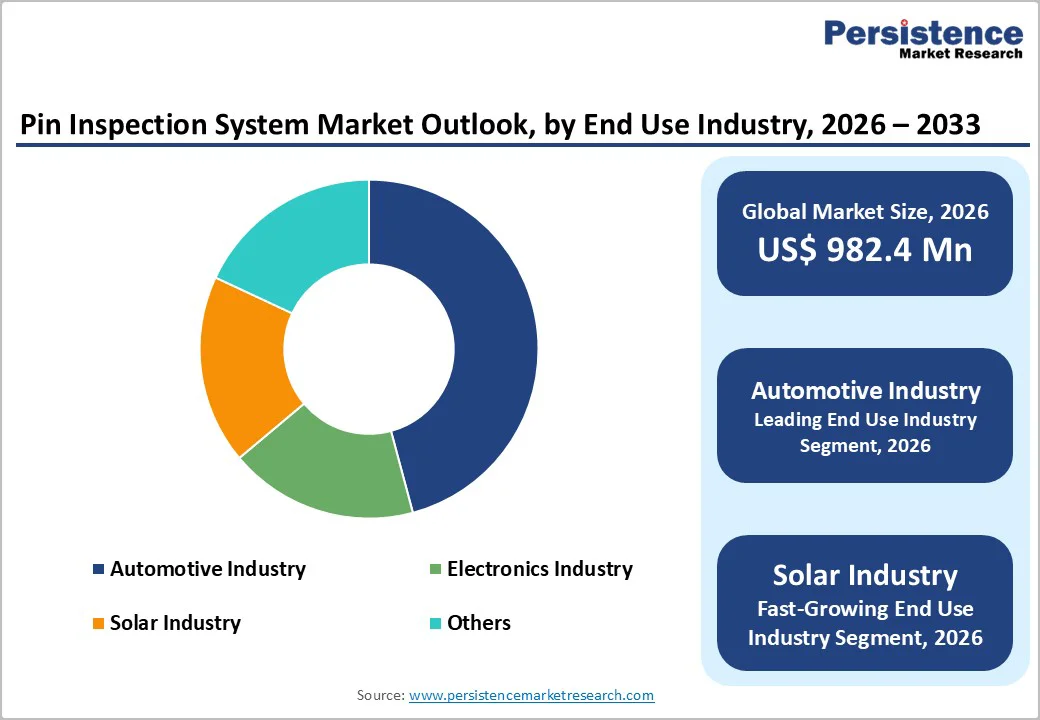

Expansion into Solar and Renewable Energy Manufacturing

The global solar photovoltaic (PV) industry is experiencing unprecedented growth with installations exceeding 1,000 gigawatts cumulatively and annual deployment increasing at 15%+ year-over-year rates driven by renewable energy mandates and declining equipment costs. Solar panel manufacturing involves complex connector pin assembly operations requiring precision alignment, proper solder joint formation, and reliable electrical connectivity critical for system performance and longevity, creating substantial opportunities for pin inspection system providers to capture share in this rapidly expanding industrial segment. Solar inverters and mounting systems incorporate hundreds of connector pins and critical electrical connections where defects compromise system efficiency, create fire hazards, and trigger warranty claims and insurance liabilities, thereby incentivizing manufacturers to adopt comprehensive quality inspection systems as differentiation strategies and risk mitigation measures. Battery energy storage systems (BESS) used to stabilize renewable energy grid integration involve complex connector architectures and high-current pin connections where inspection failures result in catastrophic equipment damage and grid stability threats, creating urgent demand for reliable inspection systems that validate connector integrity before grid interconnection. Photovoltaic module manufacturers report that implementing advanced pin inspection systems reduced defect rates in connector assemblies by 40%, prevented costly warranty failures, and improved customer satisfaction metrics, providing compelling business cases justifying rapid technology adoption throughout the solar industry.

Emergence of AI-Powered Defect Detection and Automated Optimization

Deep learning models and convolutional neural network (CNN) architectures are revolutionizing pin inspection capabilities by enabling systems to detect complex volumetric defects, subtle surface irregularities, and anomalous patterns that exceed detection capabilities of traditional rule-based vision algorithms. Generative AI techniques for synthetic data creation address critical bottlenecks in machine learning model training by enabling creation of realistic training datasets encompassing diverse defect types and manufacturing variations without requiring expensive manual annotation of thousands of production images. AI-powered pin inspection systems reduce false positive and false negative rates by 40% compared to traditional systems, decreasing scrap and rework costs while improving customer-facing product quality metrics and brand reputation protection. Manufacturers implementing AI-driven quality control report decreased manual verification workloads by 50-60%, enabling redirection of quality control personnel toward higher-value activities including root cause analysis, process optimization, and continuous improvement initiatives rather than routine visual screening. The integration of predictive maintenance algorithms enables pin inspection systems to forecast component failures, schedule preventive maintenance activities, and optimize system uptime, reducing unplanned downtime and associated production losses by up to 38%, thereby accelerating return on capital investments and justifying premium pricing for advanced technology platforms.

Category-wise Insights

Product Type Analysis: 3D Pin Inspection System

3D pin inspection systems are emerging as the fastest-growing product segment, driven by 3D pin inspection systems represent the fastest-growing product segment, projected to expand at a CAGR of 8.4% during 2026–2033 and capture approximately 42% market share by 2033, as manufacturers increasingly prioritize advanced defect detection capabilities. Three-dimensional imaging enables precise measurement of pin height, coplanarity, solder volume, and alignment, allowing detection of defects that are not visible using conventional 2D inspection. This capability is particularly critical for miniaturized and high-density electronic assemblies. Manufacturers adopting 3D pin inspection systems report improved first-pass yields and meaningful reductions in rework and scrap costs, supporting higher operational efficiency. Declining sensor costs, improved software platforms, and easier system integration are expanding adoption beyond large enterprises, positioning 3D inspection as a mainstream quality assurance tool.

Mode Analysis: Automatic Pin Inspection System

Automatic pin inspection systems dominate the market, accounting for approximately 68% market share in 2025, reflecting industry-wide reliance on fully automated quality control for high-volume manufacturing. These systems deliver consistent, objective inspection performance at high speeds, eliminating variability associated with manual inspection. By enabling continuous, around-the-clock operation, automatic systems support higher throughput and stable quality outcomes. Integration with robotic handling, automated sorting, and closed-loop feedback further enhances manufacturing efficiency and reduces defect propagation. Manufacturers deploying automatic pin inspection commonly achieve substantial reductions in labor costs, scrap, and rework, reinforcing the segment’s leadership. As manufacturers continue transitioning toward fully automated and unmanned production environments, automatic pin inspection systems remain central to scalable quality assurance strategies.

End Use Industry Analysis: Automotive Industry

The automotive industry is the leading end-use segment, holding approximately 45% market share in 2025, driven by the rapid increase in electronic content and strict safety and reliability standards. Modern vehicles rely on numerous connectors across powertrain, ADAS, infotainment, and electrification systems, where pin defects can lead to functional failures and safety risks. Regulatory and quality standards compel automotive manufacturers and suppliers to adopt advanced inspection technologies that ensure traceable and repeatable quality control. Pin inspection systems help prevent defects early in the production process, reducing recall risks and warranty costs while protecting brand integrity. Continued growth in vehicle electrification and advanced driver systems is expected to sustain strong demand from the automotive sector.

Regional Insights

North America Pin Inspection System Market Trends and Insights

North America continues to hold a leading position in the pin inspection system market, accounting for approximately 38% of global demand, supported by a well-established manufacturing base and high adoption of advanced automation technologies. The region benefits from stringent regulatory oversight across automotive, medical devices, electronics, and defense manufacturing, which reinforces the need for robust quality assurance and traceability systems. Automotive manufacturing clusters in the U.S. have been early adopters of automated inspection to meet increasingly complex electronic integration and safety standards.

Similarly, electronics and semiconductor supply chains emphasize connector reliability to minimize field failures and warranty risks. Medical device manufacturing further strengthens demand, as connector integrity is critical for patient safety and regulatory compliance. The region’s accelerating adoption of Industry 4.0 infrastructure, including IIoT connectivity, cloud-based quality monitoring, and data-driven manufacturing, supports seamless integration of pin inspection systems into enterprise quality platforms, reinforcing North America’s position as a technologically advanced and regulation-driven market.

Europe Pin Inspection System Market Trends and Insights

Europe represents a mature and quality-centric market for pin inspection systems, shaped by comprehensive regulatory frameworks governing product safety, machinery performance, and manufacturing reliability. Compliance with CE marking requirements, machinery directives, and harmonized quality standards drives consistent demand for precision inspection technologies across industrial sectors. The region’s strong automotive and industrial equipment manufacturing base emphasizes zero-defect production, supporting widespread adoption of automated inspection solutions within both OEM and supplier networks.

Sustainability and waste-reduction objectives further strengthen the business case for advanced inspection systems, as manufacturers seek to lower defect rates, reduce scrap, and improve process efficiency. European manufacturing culture places a strong emphasis on precision engineering and standardized quality management systems, where inspection technologies are embedded within documented quality workflows. Ongoing investments in smart manufacturing and factory digitization continue to modernize inspection infrastructure, positioning Europe as a stable, regulation-led market with sustained long-term demand.

Asia Pacific Pin Inspection System Market Trends and Insights

Asia Pacific is the fastest-growing regional market for pin inspection systems, projected to expand at a CAGR of 7.8% during 2026–2033, driven by rapid industrialization and large-scale electronics and automotive manufacturing growth. The region serves as the global manufacturing hub for electronic components and connectors, where quality assurance has become increasingly critical to meet international export standards. Rising regulatory emphasis on product reliability and safety, combined with growing customer expectations, is accelerating adoption of automated inspection technologies.

Government-led manufacturing initiatives and incentives across major economies are encouraging capital investment in advanced production equipment, including inspection systems. Supply chain diversification and manufacturing relocation trends are also driving new facility development across emerging economies, where inspection capabilities are being integrated from the outset. Supported by expanding Industry 4.0 adoption, cost-competitive manufacturing ecosystems, and strong export orientation, Asia Pacific is expected to steadily increase its share of the global pin inspection system market.

Competitive Landscape

Market Structure Analysis

The pin inspection system market is characterized by moderate fragmentation, with roughly a dozen established and emerging suppliers competing across 2D, 3D, and application-specific inspection solutions. The market structure reflects a mix of large automation technology providers offering broad inspection platforms and smaller specialists focusing on niche or high-precision use cases. Competition is primarily driven by technological differentiation rather than pricing, as customers prioritize inspection accuracy, throughput, and system reliability.

Business strategies increasingly emphasize portfolio expansion and platform integration, with suppliers embedding pin inspection capabilities into end-to-end manufacturing automation ecosystems through partnerships and acquisitions. Software capabilities are becoming a key differentiator, including AI-enabled defect detection, adaptive algorithms, and predictive maintenance features that enhance long-term value. Vendors are also shifting toward recurring-revenue models, such as SaaS-based analytics, cloud-enabled quality monitoring, and subscription-based upgrades, to improve customer retention. Smaller players compete effectively by offering cost-efficient, easy-to-deploy systems tailored to specific applications, reducing complexity and ownership costs for mid-scale manufacturers.

Key Market Developments

- June 2025, Cognex Corporation announced OneVision, a revolutionary cloud platform for AI-powered machine vision that streamlines application development from months to minutes, eliminates infrastructure costs, integrates tools seamlessly, and delivers consistent performance across manufacturing sites, starting with select In-Sight systems.

Companies Covered in Pin Inspection System Market

- Cognex Corporation

- G2 Technologies

- Sick Sensor Intelligence

- Mectron Inspection Engineering

- Abto Software

- D-Test Optical Measurement System

- Viscom AG

- JUKI CORPORATION

- Hamamatsu Photonics K.K.

- Saki Corporation

- Miroku Electronics

- Siemens Industrial Automation

- Keyence Corporation

- Basler AG

- National Instruments

Frequently Asked Questions

The global Pin Inspection System Market is expected to reach approximately US$ 982.4 million in 2026.

Key drivers include increasing automation, stricter quality assurance standards, automotive electronics complexity, and Industry 4.0 adoption.

North America is expected to lead the market with around 38% share during the forecast period.

AI-powered defect detection and automated inspection optimization represent the most significant growth opportunity.

Major players include Cognex Corporation, Viscom AG, JUKI Corporation, Hamamatsu Photonics, Keyence Corporation, and Basler AG.