- Medical Devices

- Oxygen Therapy Market

Oxygen Therapy Market Size, Share, and Growth Forecast, 2026 - 2033

Oxygen Therapy Market by Product Type (Compressed Oxygen, Concentrated Oxygen, Liquid Oxygen), Disease (Respiratory Disorder, Cardiovascular Disease, Sleep Apnea, Pneumonia), End-User (Hospitals, Home Healthcare, Clinics), and Regional Analysis for 2026-2033

Oxygen Therapy Market Share and Trends Analysis

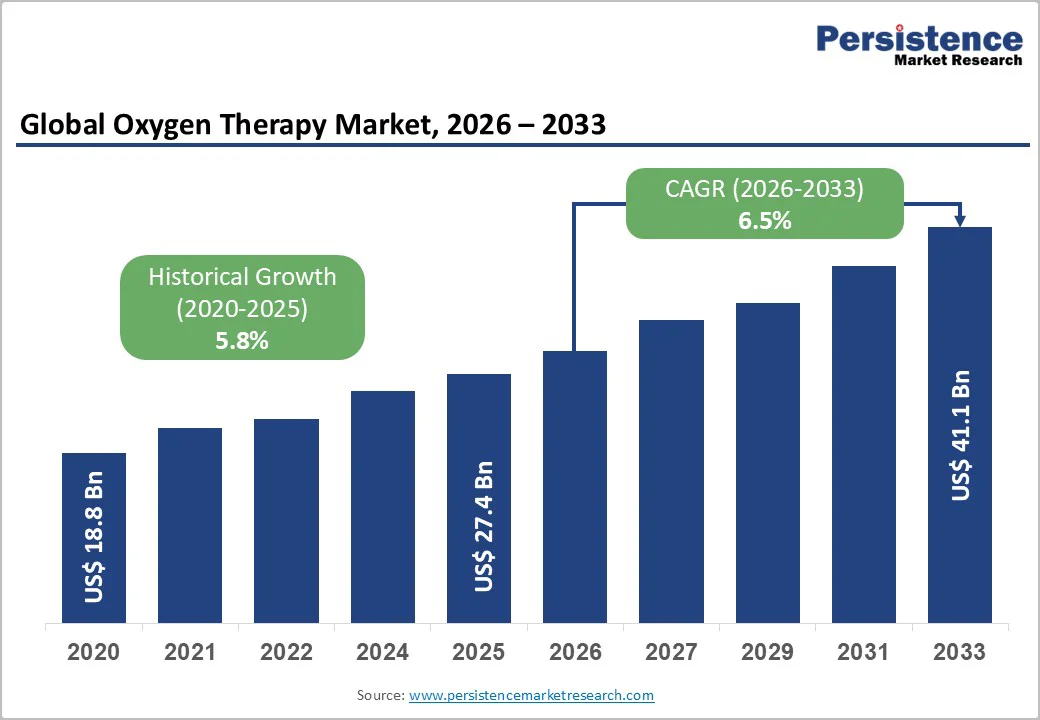

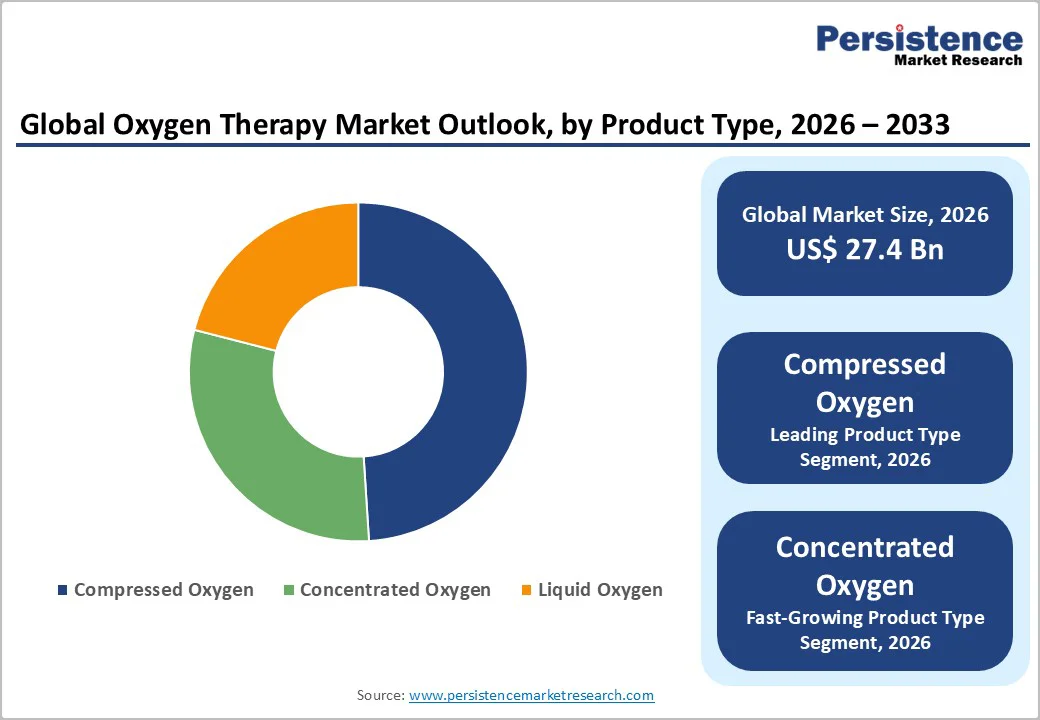

The global oxygen therapy market size is likely to be valued at US$ 27.4 billion in 2026, and is estimated to reach US$ 41.1 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026−2033. The rising prevalence of chronic respiratory diseases such as chronic obstructive pulmonary disease (COPD) and asthma, an aging population requiring long-term oxygen therapy, and increasing adoption of portable and home-based oxygen delivery systems are primarily driving the market. Advancements in high flow oxygen devices, portable concentrators, and smart monitoring solutions further support market expansion across both acute care and home healthcare settings.

Key Industry Highlights

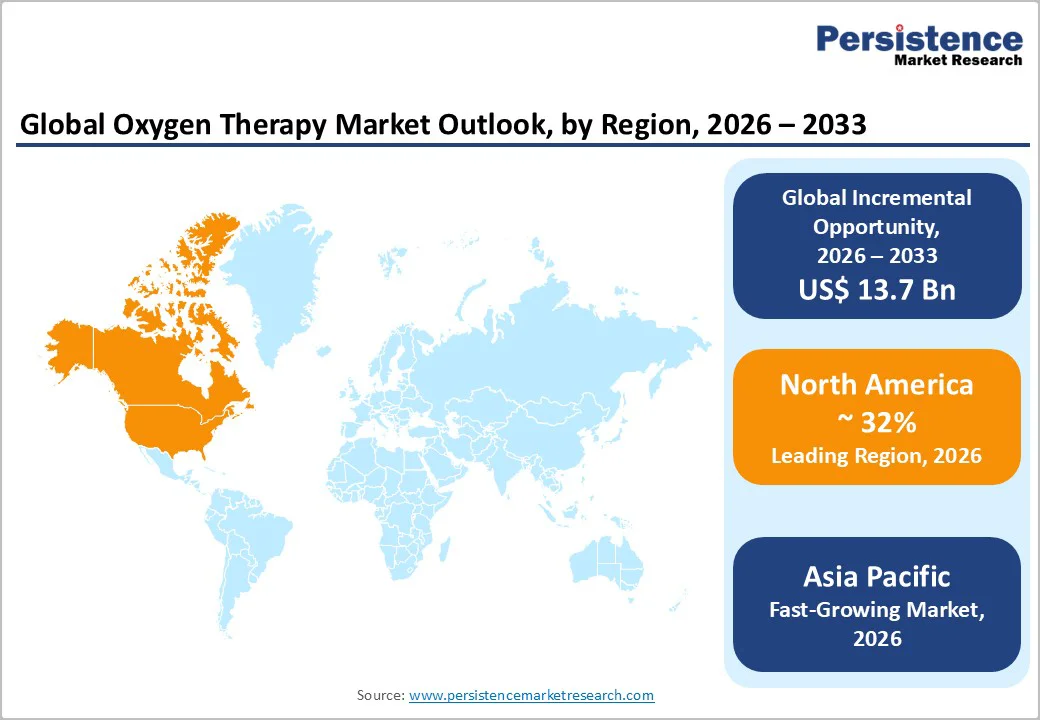

- Dominant Region: North America is expected to command about 32% market share in 2026, driven by well developed healthcare infrastructure and favorable reimbursement frameworks.

- Fastest-growing Market: Asia Pacific is anticipated to emerge as the fastest-growing market through 2033, fueled by growing populations, increasing healthcare expenditure, and improving healthcare infrastructure.

- Leading & Fastest-growing Product Type: Compressed oxygen is slated to dominate the market, with an estimated 2026 share around 49%, while oxygen concentrators are likely to be the fastest-growing from 2026 to 2033.

- Leading & Fastest-growing End-User: Hospitals are poised to lead with about 60% revenue share in 2026, as they are the primary point of care for patients.

- Fastest-growing End-User: Home health care is likely to be the fastest-growing end-user through 2033, on account of the expanding availability of advanced and portable oxygen concentrators.

| Key Insights | Details |

|---|---|

| Oxygen Therapy Market Size (2026E) | US$ 27.4 Bn |

| Market Value Forecast (2033F) | US$ 41.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2019 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Incidence of Chronic Respiratory Diseases and Aging Population

The global prevalence of COPD, asthma, and related respiratory conditions continues to accelerate, with particular concentration among aging populations. This demographic shift creates substantial medical need for extended oxygen supplementation across both institutional and home-care settings. As the world's population structure tilts toward older age groups, the clinical population managing advanced pulmonary and cardiovascular pathologies characterized by hypoxemia expands correspondingly, thereby establishing sustained demand for oxygen delivery infrastructure including concentrators, pressurized cylinders, and cryogenic liquid oxygen systems distributed across hospital networks and residential environments.

Oxygen therapy functions as a cornerstone intervention by delivering controlled volumetric flows of refined oxygen through patient interface devices such as oronasal masks or nasal cannulae, thereby elevating the inspired oxygen concentration beyond ambient levels. This therapeutic approach delivers multifaceted clinical benefits: it mitigates dyspnea and associated respiratory distress, restores adequate organ oxygenation for improved physiological function, and meaningfully enhances functional capacity for routine activities including personal hygiene, self-care, and low-intensity physical activity.

Regulatory Complexity and Product Safety Requirements

Oxygen therapy equipment operates within comprehensive regulatory frameworks mandated by international health authorities, with stringent protocols designed to safeguard patient safety and device reliability. These governance structures address critical failure modes including oxygen purity degradation, electrical system malfunctions, and structural integrity compromises that could precipitate adverse clinical outcomes or introduce novel patient harm. Manufacturers must demonstrate device performance across heterogeneous real-world deployment scenarios encompassing residential settings and clinical environments, where operational variables such as ambient humidity, mechanical vibration, and electrical supply instability present significant performance challenges requiring substantive engineering solutions.

Regulatory compliance mechanisms frequently necessitate enhanced quality assurance protocols, iterative design modifications, and extended validation timelines, collectively functioning as material impediments to accelerated product development cycles and expedited market entry. These interventions establish formidable barriers for emerging competitors while constraining supply-side expansion and imposing structural limitations on sector growth trajectories. The regulatory apparatus, though foundational to user protection and long-term market credibility, introduces substantial compliance costs and temporal friction that fundamentally reshape organizational innovation and competitive positioning.

Development and Adoption of Portable Oxygen Therapy Devices

Portable oxygen concentrators (POCs) address a fundamental limitation affecting patients on long-term oxygen therapy: restricted mobility and diminished independence. Traditional oxygen delivery systems, such as pressurized cylinders and stationary concentrators, impose significant practical burdens through their weight, noise generation, and cumbersome transport requirements. These constraints effectively confine patients to their homes and actively discourage participation in physical activities and social engagement. Portable oxygen concentrators offer a transformative alternative through their compact design and battery-powered operation, allowing patients to carry or wheel their equipment while maintaining continuous therapeutic oxygen delivery. This mobility enhancement fundamentally changes the therapeutic landscape, enabling patients to sustain active lifestyles, travel confidently, and participate in light exercise without compromising their oxygen supplementation.

The integration of smart technology into oxygen delivery equipment has converted traditional hardware into comprehensive care platforms with real-time data connectivity and remote clinical oversight. Connected concentrators transmit essential operational metrics including usage frequency, prescribed flow parameters, and relevant physiological data to secure cloud-based platforms accessible to healthcare providers and home-care coordinators. This connectivity enables clinicians to assess therapy adherence continuously, detect early warning signs of clinical deterioration, and implement timely interventions when usage patterns indicate suboptimal compliance or emerging complications. For manufacturers, this technological advancement creates meaningful competitive differentiation opportunities. Organizations that successfully combine connectivity infrastructure with regulatory compliance establish sustainable advantages through measurably improved patient outcomes, enhanced care coordination across distributed settings, and more robust clinical decision-making processes.

Category-wise Analysis

Product Type Insights

Compressed oxygen systems are positioned to maintain market leadership through 2026, with a projected revenue share around 50%. Cylinders and compressed gas delivery infrastructure remain foundational to clinical operations across hospitals, emergency departments, and primary care facilities globally. This sustained dominance is attributable to the demonstrated versatility of these systems across diverse clinical environments including operating rooms, intensive care units (ICUs), patient wards, and ambulance services. Mature global supply chains, established distribution networks, and seamless integration with existing regulatory equipment, flow measurement devices, and hospital gas management systems have perpetuated their market entrenchment.

Oxygen concentrators are likely to be the most rapidly expanding segment through 2033, driven by aging populations and rising chronic disease prevalence, which have generated a huge demand for long-term oxygen therapy solutions. Healthcare systems are systematically shifting toward home-based care delivery models, substantially elevating the clinical and economic appeal of concentrator technologies. This market transition has prompted manufacturers to accelerate development of next-generation POCs and high-flow delivery systems specifically engineered for home settings and extended-care residential facilities. These innovations position concentrators to chart a promising growth trajectory within patient populations prioritizing independence and quality of life outcomes.

Disease Insights

Respiratory disorders are expected to command approximately 35% of the oxygen therapy market revenue share in 2026. This leadership position reflects the convergence of two critical market dynamics: the substantial patient population affected by chronic pulmonary conditions and the intensive, prolonged oxygen utilization requirements these patients demand. COPD, asthma, interstitial lung disease (ILD), and related chronic pulmonary pathologies constitute the primary patient cohort requiring continuous oxygen supplementation. The scale of this population base, combined with sustained high-volume oxygen consumption throughout extended treatment periods, can establish durable revenue streams from recurrent oxygen replenishment and equipment maintenance requirements.

Sleep-disordered breathing is set to be the fastest-growing clinical application from 2026 to 2033, reflecting evolving therapeutic practices and expanding patient identification. Positive airway pressure devices, including continuous positive airway pressure (CPAP) and bilevel positive airway pressure (BiPAP) systems, remain the foundational therapy for obstructive sleep apnea (OSA). However, oxygen supplementation is increasingly deployed as an adjunctive treatment modality within carefully selected patient populations experiencing overlapping pathologies. Clinicians now employ oxygen therapy in patients with concurrent COPD and sleep apnea, obesity hypoventilation syndrome (OHS), and central sleep apnea (CSA), reflecting recognition of oxygen's role in addressing nocturnal hypoxemia within these complex patient subsets.

End-User Insights

Hospitals dominate the end-user landscape, holding around 60% of market share in 2026. This market leadership reflects hospitals' role as primary treatment centers for patients with the highest clinical acuity and the broadest spectrum of oxygen-dependent pathologies. Hospital systems maintain comprehensive oxygen therapy infrastructure to support emergency interventions, surgical procedures, intensive care management, and acute exacerbations of chronic respiratory conditions. This operational requirement generates consistently elevated device utilization rates and substantial recurring procurement volumes that sustain revenue predictability. Hospitals also function as early adopters of advanced oxygen delivery technologies, including high-flow oxygen systems, integrated patient monitoring platforms, and specialized delivery interfaces, which are essential for managing critically ill patients safely.

Home healthcare is expected to grow the fastest during 2026-2033, propelled by strong clinical evidence supporting the efficacy of home-based oxygen therapy. Technological advances in portable oxygen concentrators and cryogenic liquid oxygen (LOX) systems designed for residential use has substantially increased patient and provider adoption. Escalating healthcare expenditures and intensifying pressure to reduce treatment costs are systematically driving demand for cost-effective care delivery models. Home-based oxygen therapy delivers meaningful economic advantages by shifting care from expensive institutional settings to lower-cost residential environments while maintaining clinical effectiveness.

Regional Insights

North America Oxygen Therapy Market Trends

North America is positioned to command approximately 32% of the oxygen therapy market share in 2026. This supremacy is owing to the convergence of substantial disease burden with robust infrastructure and systemic enablers supporting widespread device adoption. The region is experiencing a growing prevalence of COPD, asthma, and OSA, generating a substantial clinical demand for oxygen therapy across both acute-care hospital settings and extended home-based treatment environments. This large patient population creates sustained demand for oxygen delivery equipment and establishes North America as a critical revenue center for global manufacturers.

Regional market growth is also being reinforced by well-established healthcare infrastructure and favorable reimbursement mechanisms that systematically expand patient access to advanced oxygen therapy solutions. Payers throughout the United States and Canada provide comprehensive reimbursement coverage for long-term oxygen therapy and home-based oxygen devices, eliminating cost barriers that might otherwise restrict device adoption. The region's elevated healthcare expenditure levels facilitate rapid market penetration of innovative technologies, including portable oxygen concentrators, high-flow oxygen delivery systems, and digitally integrated home oxygen solutions.

Europe Oxygen Therapy Market Trends

Europe holds a significant market position, driven by demographic shifts and evolving clinical practice patterns. The region's aging population structure generates escalating prevalence of chronic respiratory conditions requiring sustained oxygen supplementation. Clinical awareness and patient acceptance of modern, patient-centered oxygen solutions are systematically expanding among healthcare providers and treatment populations. Key markets including Germany, the United Kingdom, and France function as regional demand drivers through their combination of large patient populations and well-established hospital and home-care infrastructure supporting comprehensive respiratory disease management across institutional and residential settings.

Regulatory transformation under the European Union (EU) Medical Device Regulation (EU MDR) is fundamentally reshaping market access dynamics throughout the region. The regulatory framework elevates manufacturer compliance requirements and increases implementation costs, yet simultaneously strengthens device quality standards and post-market surveillance mechanisms. These enhanced oversight requirements particularly impact POCs and related oxygen delivery systems, creating competitive advantages for manufacturers with robust quality management systems and regulatory expertise. Western European nations, especially, demonstrate high penetration of home-based oxygen therapy, with strong integration of oxygen services within community healthcare networks and remote patient monitoring programs.

Asia Pacific Oxygen Therapy Market Trends

Asia Pacific is anticipated to be the fastest-growing market for oxygen therapy throughout the 2026-2033 period, propelled by demographic expansion, rising healthcare investment, and systematic improvements in clinical infrastructure. China, Japan, and India function as principal growth catalysts, each benefiting from escalating healthcare expenditures, broadening insurance coverage mechanisms, and government-mandated initiatives strengthening medical oxygen production capacity, distribution networks, and emergency preparedness infrastructure. These policy frameworks, bolstered by pandemic-driven recognition of oxygen supply criticality, create systematic incentives for manufacturers to expand regional presence and establish localized supply chains supporting market growth and healthcare system resilience.

The expanding utilization of oxygen therapy technologies correlates with rising incidence of chronic and acute respiratory pathologies, compelling healthcare systems and clinical providers to adopt more dependable and patient-centered oxygen delivery solutions. As clinician awareness and patient education regarding advanced oxygen technologies progressively expand, treatment populations increasingly recognize the therapeutic and quality-of-life benefits of portable oxygen concentrators, high-flow oxygen delivery systems, and integrated home-care platforms. This evolving clinical perspective systematically shifts regional practice patterns away from episodic, acute-care-focused oxygen utilization toward structured, sustained long-term oxygen management frameworks. Healthcare providers and patients in the region are increasingly adopting comprehensive respiratory care pathways that prioritize therapeutic continuity, functional independence, and proactive disease management.

Competitive Landscape

The global oxygen therapy market structure exhibits moderate consolidation, with dominant industry players commanding considerable market influence. Koninklijke Philips, Inogen Inc., Fisher & Paykel Healthcare, and ResMed Inc. collectively control approximately 55% of the total market share. This concentration is indicative of unmatched competitive advantages derived from established distribution networks, comprehensive product portfolios, strong brand recognition, and substantial research and development (R&D) capabilities. The leading manufacturers leverage these capabilities to maintain market position while creating meaningful barriers to competitive entry for smaller and emerging organizations.

The competitive environment is also characterized by dynamic, multi-faceted competitive strategies encompassing continuous product innovation, strategic partnerships and alliances, and active merger and acquisition (M&A) activity. Major market participants are systematically investing in R&D initiatives targeting next-generation oxygen therapy devices designed to enhance user experience, improve clinical outcomes, and address unmet patient needs. This environment incentivizes sustained product development, strategic differentiation through advanced features and connectivity capabilities, and targeted market expansion, particularly within rapidly growing segments including home healthcare and portable oxygen solutions.

Key Industry Developments

- In October 2025, CAIRE's FreeStyle Comfort POC became available in the U.S., featuring automatic breath-rate adjustment that delivers consistent oxygen volume during activity or rest. The lightweight 5-pound device delivers up to 1,050 milliliters of oxygen per minute across five flow settings, combines ergonomic curved design with smart oxygen delivery technologies including UltraSense breath detection and autoDOSE failsafe delivery.

- In July 2025, MedAccess, Unitaid, and the Clinton Health Access Initiative (CHAI) announced a volume guarantee agreement with Synergy Gases Ltd to expand affordable medical oxygen access across sub-Saharan Africa through a regional production and distribution network. The initiative includes construction of a state-of-the-art air separation unit (ASU) facility in Kenya, which will produce medical-grade liquid oxygen distributed via hub-and-spoke model across Kenya, Tanzania, and Uganda, with the East Africa Program on Oxygen Access (EAPOA).

- In June 2025, Inogen launched the Voxi 5 stationary oxygen concentrator (SOC) in partnership with Yuwell Medical, delivering 1-5 L/min of quiet, medical-grade oxygen through an 8-layer filtration system and featuring lockable casters for home mobility. The Voxi 5 includes advanced features such as compact design, 3-year sieve bed warranty, and quiet operation at 45 decibels (dB), enabling Inogen to expand market penetration among price-sensitive customers and multi-room home oxygen therapy users.

Frequently Asked Questions

The global oxygen therapy market is projected to reach US$ 27.4 billion in 2026.

The market is primarily driven by the growing global burden of chronic and acute respiratory diseases, aging populations, and higher clinical reliance on long‑term oxygen therapy across hospital and home‑care settings.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Major opportunities lie in expanding home‑based and long‑term oxygen therapy in emerging markets, where healthcare access and insurance coverage are improving and respiratory disease prevalence is rising.

Koninklijke Philips N.V., Inogen Inc., Fisher & Paykel Healthcare, ResMed Inc. are some of the key players in the market.