- Healthcare

- Oral Hydrogel Wound Dressing Market

Oral Hydrogel Wound Dressing Market Size, Share, and Growth Forecast 2026 – 2033

Oral Hydrogel Wound Dressing Market by Product Type (Amorphous hydrogel, Sheet hydrogel, Impregnated hydrogel), by Application (Chronic wounds, Acute wounds, Surgical wounds, Burns), by Distribution Channel (Hospital pharmacies, Retail pharmacies, Online pharmacies), by Regional Analysis, 2026-2033

Oral Hydrogel Wound Dressing Market Size and Trend Analysis

The global Oral Hydrogel Wound Dressing market size is expected to be valued at US$ 832.3 million in 2026 and projected to reach US$ 1,459.4 million by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

This growth is propelled by the superior wound healing properties of hydrogels, which maintain a moist environment, promote autolytic debridement, and reduce infection risk in the oral cavity's dynamic microenvironment. Rising prevalence of oral surgical procedures, chronic oral conditions like diabetic ulcers, and advancements in bioactive hydrogel formulations that incorporate antimicrobials, growth factors, and stimuli-responsive elements are expanding clinical adoption.

Key Market Highlights

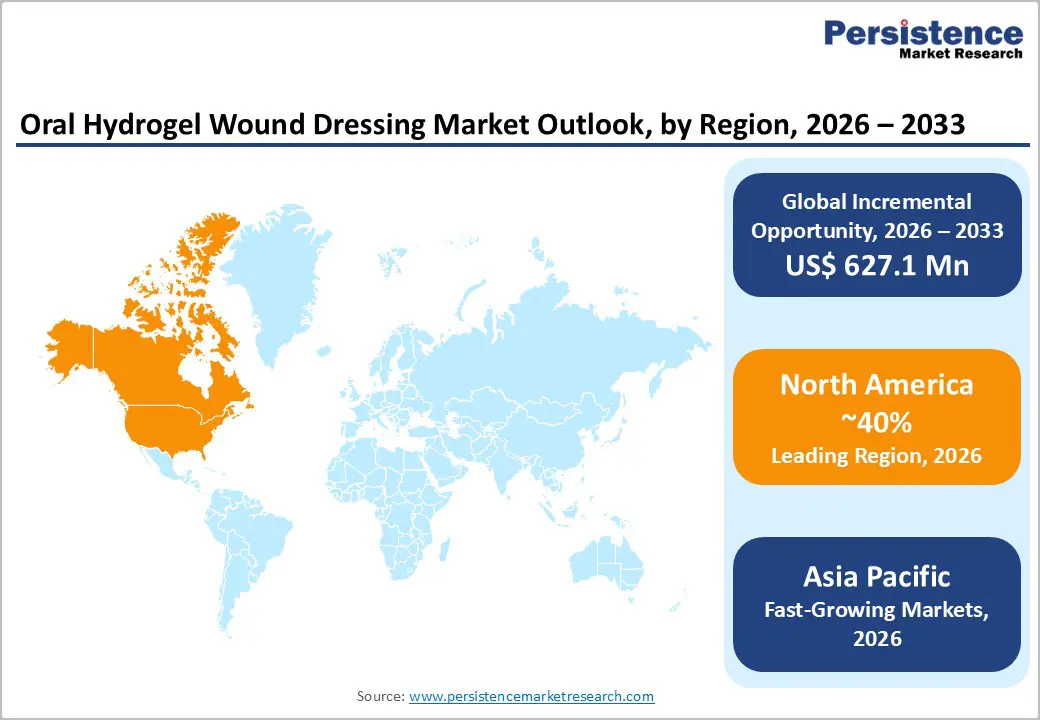

- North America dominates the Oral Hydrogel Wound Dressing market with 40% share in 2025, driven by FDA approvals, high diabetes rates, and innovation from leading medtech firms.

- Asia Pacific is the fastest growing region, fueled by diabetes epidemics, local manufacturing, and epharmacy expansion in China, India, and ASEAN.

- Amorphous hydrogel leads product types at 53% share in 2025, excelling in irregular oral wounds with superior moisture and debridement properties.

- Sheet hydrogel is the fastest growing segment, leveraging bioactive and responsive innovations for precise surgical and chronic oral applications.

- Key opportunity in stimuli responsive bioactive hydrogels for chronic diabetic oral wounds, integrating antimicrobials and growth factors for accelerated healing.

| Global Market Attributes | Key Insights |

|---|---|

| Oral Hydrogel Wound Dressing Market Size (2026E) | US$ 832.3 million |

| Market Value Forecast (2033F) | US$ 1,459.4 million |

| Projected Growth CAGR (2026-2033) | 8.4% |

| Historical Market Growth (2020-2025) | 6.9% |

Market Dynamics

Market Growth Drivers

Moist wound healing efficacy and biocompatibility in oral cavity

Hydrogel dressings drive market growth by creating an optimal moist environment that accelerates oral wound healing while minimizing infection and scarring risks. Clinical reviews confirm hydrogels promote autolytic debridement, re epithelialization, and angiogenesis through hydration and oxygen permeation, with amorphous types providing 15.2% superior moistening over alternatives. In oral/maxillofacial applications, biocompatibility resists salivary enzymes and mechanical stress, delivering agents like EGF or antimicrobials for enhanced regeneration. WHO moist healing guidelines and dental protocols reinforce adoption, reducing hospital stays and costs in post surgical and mucositis cases. This proven performance sustains demand across acute and chronic oral wounds.

Increasing oral surgeries and chronic oral conditions

Rising surgical procedures and chronic wounds propel the Oral Hydrogel Wound Dressing market. Dental implants, periodontal surgeries, extractions, and maxillofacial reconstructions generate high wound volumes, while diabetes (537 million cases globally) and chemotherapy mucositis exacerbate chronic lesions. Hydrogels mitigate delays by scavenging ROS and modulating inflammation, achieving faster closure in diabetic models via M2 macrophage shift. Aging populations and implant growth millions annually amplify needs, with guidelines favoring advanced dressings for complex sites. This expands hydrogel use in hospitals and outpatient care.

Market Restraints

Elevated costs and inconsistent reimbursement

Premium pricing of bioactive hydrogels, 2–3 times higher than traditional dressings due to advanced polymers and actives, restricts broad adoption, especially in cost sensitive markets. Reimbursement challenges persist; while U.S. Medicare covers select 510(k) cleared products, many payers demand randomized evidence of cost savings, delaying approvals for oral applications. In Europe and Asia, national formularies often prioritize generics, limiting hospital procurement. Out of pocket burdens deter retail/online sales for prophylactic use, confining hydrogels to severe cases and slowing volume growth despite superior outcomes.

Adhesion and retention challenges in oral dynamics

Hydrogels face significant hurdles retaining integrity in the saliva rich, mechanically stressed oral cavity, leading to migration or early degradation. Amorphous formulations may disperse unevenly in irregular beds; sheets struggle with contouring, requiring adhesives that risk irritation (<5% incidence). Frequent reapplication increases clinician burden and infection risk if not managed. Variability across patient factors like xerostomia or mucositis compounds performance inconsistencies, eroding confidence despite moist healing benefits and hindering routine protocol integration.

Market Opportunities

Advanced bioactive stimuli responsive sheet hydrogels

Sheet hydrogels hold substantial growth potential with stimuli responsive bioactives optimized for oral wounds, offering controlled release via pH, ROS, or temperature triggers. Light crosslinked variants achieve 24+ hour adhesion and targeted EGF/antimicrobial delivery, accelerating diabetic oral healing per in vivo data. Rising implant surgeries (millions yearly) and mucositis cases create demand; 3M Company, Smith & Nephew plc can collaborate on FDA trials and dental guidelines for surgical/chronic segments. Digital monitoring integration enhances differentiation, promising recurring revenue in outpatient care.

Digital distribution and emerging market penetration

Online pharmacies present a dynamic opportunity amid telemedicine expansion, ideal for hydrogel home use in chronic/post op oral care. Asia Pacific's diabetes boom (Asia hosts 60% global cases) and manufacturing hubs enable affordable scaling. ConvaTec Group plc, Coloplast A/S can launch subscription kits with tutorials, targeting India/China via e platforms. Policy support for advanced dressings amplifies reach, converting retail growth into sustained volumes for impregnated/chronic applications.

Category wise Insights

Product Type Analysis

Amorphous hydrogel dominates the product type segment, holding approximately 53% market share in 2025, due to its versatility in filling irregular oral wound beds and superior moisture donation. Clinical trials confirm amorphous hydrogels like EHO 85 achieve significantly higher wound healing rates (p < 0.01) versus hydrocolloids, with 15.2% greater moistening capacity and faster closure in hard to heal ulcers. Their syringe applicable form suits dynamic oral sites, facilitating autolytic debridement and exudate management while minimizing trauma on removal. Preferred in hospital pharmacies for acute surgical and chronic applications, amorphous hydrogels' biocompatibility and ease outweigh sheet limitations in complex geometries.

Application Analysis

Among applications, Chronic wounds lead the market in 2025, estimated at over 40% share, driven by persistent oral conditions like diabetic ulcers, mucositis, and periodontitis. Hydrogels excel in chronic settings by rehydrating necrotic tissue, scavenging ROS, and promoting M2 macrophage polarization, with studies showing complete epidermal regeneration in diabetic models. National Institute for Health and Care Excellence (NICE) guidelines endorse moist dressings for non healing wounds, amplifying use in long term care. While acute and surgical wounds contribute, chronic prevalence—linked to diabetes affecting 10.5% of adults globally—cements this segment's dominance.

Distribution Channel Analysis

Hospital pharmacies command the leading position among distribution channels, likely exceeding 50% share in 2025, as oral hydrogel dressings are primarily prescribed in clinical settings for post surgical and specialized wound care. Hospitals integrate hydrogels into protocols for maxillofacial procedures and oncology mucositis, where direct clinician oversight ensures proper application. With 24 polysaccharide based hydrogels FDA registered, procurement volumes favor institutional channels. Retail and online lag due to prescription norms but grow for home care.

Regional Insights

North America Oral Hydrogel Wound Dressing Market Trends and Insights

North America leads with around 40% market share in 2025, anchored by the U.S.'s advanced wound care ecosystem and high oral surgery rates. FDA clearances, including 24 polysaccharide hydrogels, and NIH funding for antimicrobial trials bolster innovation, with products like 3M's impregnated dressings gaining traction. High diabetes prevalence (14.7 million diagnosed) drives chronic wound demand, supported by Medicare reimbursements.

Robust R&D from firms like Smith & Nephew plc and Integra LifeSciences Corporation focuses on bioactive oral hydrogels, with dental associations promoting moist healing standards. Telehealth integration expands outpatient use via hospital pharmacies.

Europe Oral Hydrogel Wound Dressing Market Trends and Insights

Europe, including Germany, U.K., France, and Spain, shows steady adoption through harmonized CE Mark regulations and NICE endorsements for moist dressings. Clinical evidence from multicenter trials favors hydrogels like EHO 85 for superior healing (p < 0.01) in chronic ulcers. Aging populations and rising implant surgeries fuel demand.

National health systems reimburse advanced dressings, with U.K. and German guidelines prioritizing hydrogels for surgical wounds. Cross border collaborations accelerate bioactive innovations.

Asia Pacific Oral Hydrogel Wound Dressing Market Trends and Insights

The Asia Pacific oral hydrogel wound dressing market is one of the fastest growing regions globally, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing awareness of advanced wound care solutions. A growing prevalence of chronic diseases such as diabetes, combined with a large and aging population, is significantly increasing demand for effective wound management products across countries like China, India, and Japan. Improvements in healthcare access, particularly in urban and semi urban areas, are enabling wider adoption of hydrogel dressings in both hospitals and home care settings. Additionally, rising patient awareness about the benefits of hydrogel dressings for pain reduction and moisture balanced healing is supporting growth. Technological advancements and product launches tailored to regional needs are enhancing market competitiveness. Furthermore, economic growth and a stronger middle class with higher disposable income are making advanced wound care products more affordable and acceptable, further accelerating regional market expansion.

Competitive Landscape

Market Structure Analysis

The Oral Hydrogel Wound Dressing market is moderately consolidated, led by global medtech giants with strong R&D and distribution networks. Leaders like 3M Company, Smith & Nephew plc, ConvaTec Group plc, and Coloplast A/S differentiate via bioactive formulations, antimicrobial impregnation, and clinical evidence from trials showing faster healing. Strategies emphasize acquisitions, partnerships for stimuli responsive tech, and expansion into online channels. Emerging trends include subscription models and AI optimized dressings. Niche players focus on regional customization.

Key Market Developments

- In November 2025, Young Innovations, a leading dental industry innovator, and Umayana, a biotechnology company, announced a partnership to launch Murnia® Mouth Spray in the United States. This collaboration introduced a new approach to oral care and comfort, providing natural moisture through a patented formula for persistent oral dryness, which affected over 25 million Americans. The prevalence was expected to increase significantly due to aging populations, medication use, and lifestyle factors.

Companies Covered in Oral Hydrogel Wound Dressing Market

- 3M Company

- Smith & Nephew plc

- ConvaTec Group plc

- Coloplast A/S

- Mölnlycke Health Care AB

- Integra LifeSciences Corporation

- Medline Industries, Inc.

- Cardinal Health, Inc.

- Paul Hartmann AG

- B. Braun Melsungen AG

- Derma Sciences, Inc.

- Hollister Incorporated

Frequently Asked Questions

The global Oral Hydrogel Wound Dressing market is projected to reach US$ 832.3 million in 2026, driven by moist healing benefits and rising oral surgeries.

Demand stems from hydrogels' moist environment provision, infection reduction, and efficacy in chronic diabetic oral wounds, supported by clinical evidence of faster healing.

North America leads with 40% share in 2025, bolstered by FDA approvals, diabetes prevalence, and innovations from key medtech players.

Stimuli‑responsive bioactive sheet hydrogels for chronic and surgical oral wounds offer growth, with adhesion and cargo release innovations accelerating adoption.

Key players include 3M Company, Smith & Nephew plc, ConvaTec Group plc, Coloplast A/S, Mölnlycke Health Care AB, Integra LifeSciences, and Medline Industries.