- Medical Devices

- Neurovascular Thrombectomy Devices Market

Neurovascular Thrombectomy Devices Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Neurovascular Thrombectomy Devices Market by Product Type (Stent Retriever, Aspiration Catheter, Others), by Application (Acute ischemic stroke, Cerebral aneurysm, Arteriovenous malformation (AVM), Others), by End User, and Regional Analysis from 2026 - 2033

Neurovascular Thrombectomy Devices Market Share and Trends Analysis

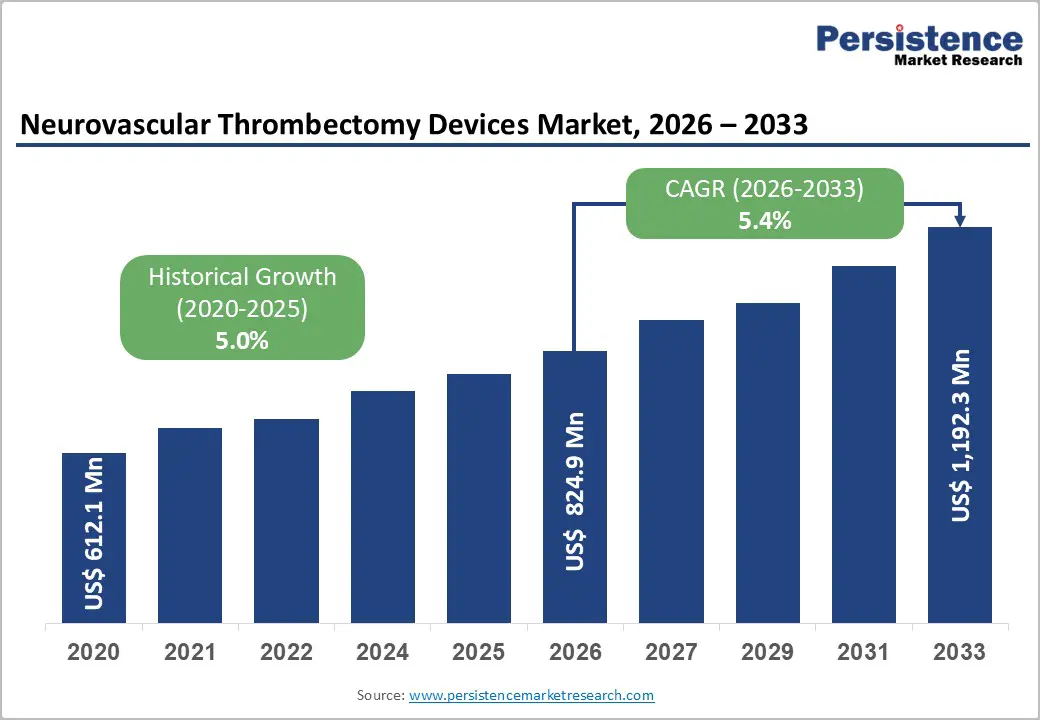

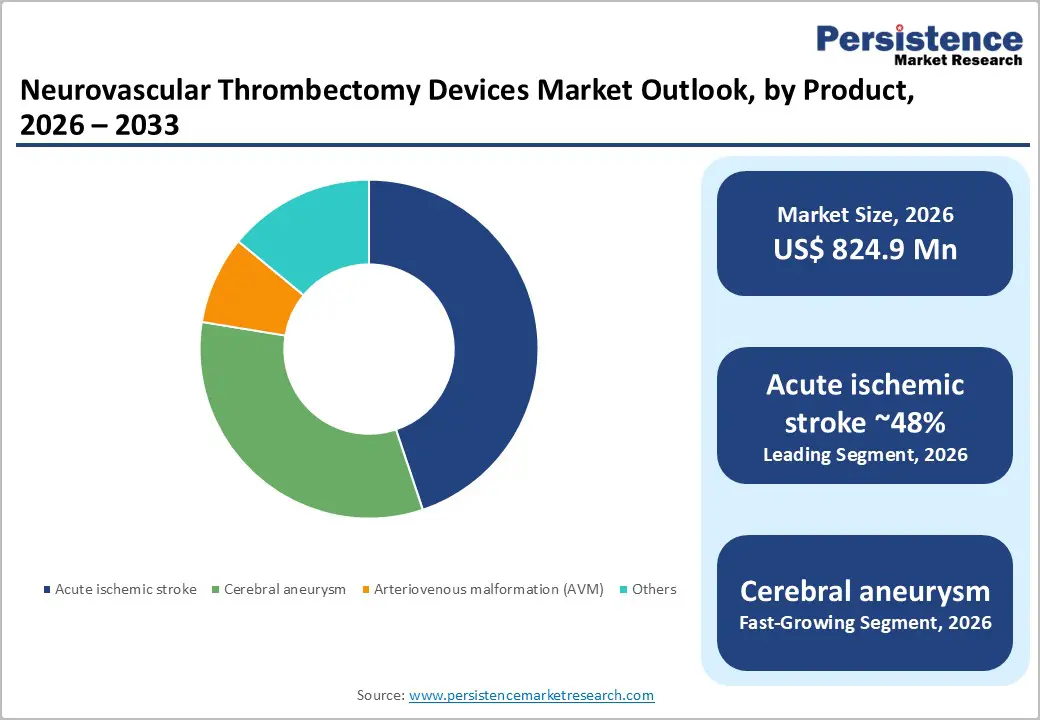

The global neurovascular thrombectomy devices market is likely to be valued at US$ 824.9 million in 2026 and US$1,192.3 million by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033. The global market is steadily expanding due to the rising global burden of acute ischemic stroke and growing adoption of minimally invasive neurointerventional procedures.

Advances in stent retrievers and aspiration technologies have significantly improved recanalization rates and clinical outcomes, driving physician preference for mechanical thrombectomy as a standard of care. Increasing awareness of early stroke intervention, expansion of comprehensive stroke centers, and supportive clinical guidelines further support market growth. Additionally, technological innovations, faster procedural times, and improved healthcare infrastructure in emerging economies are accelerating adoption, positioning neurovascular thrombectomy devices as a critical component of modern stroke management.

Key Industry Highlights:

- Increasing incidence of acute ischemic stroke globally is the primary driver, significantly boosting demand for mechanical thrombectomy procedures and advanced neurovascular clot-removal devices.

- Hospitals represent the largest end-user segment, supported by advanced neurointerventional infrastructure, availability of skilled specialists, and a growing number of certified stroke centers.

- Aspiration-based thrombectomy devices are witnessing rapid growth, driven by simpler procedures, reduced procedure time, and increasing physician preference for first-pass success.

- Innovations in stent retrievers, aspiration catheters, and hybrid techniques are improving procedural success rates, reducing complications, and enhancing clinical outcomes for stroke patients.

| Key Insights | Details |

|---|---|

|

Neurovascular Thrombectomy Devices Market Size (2026E) |

US$824.9 Mn |

|

Market Value Forecast (2033F) |

US$1,192.3 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Dynamics

Driver - Extended Treatment Window Validation

Extended treatment window validation has emerged as a transformative driver for the neurovascular thrombectomy devices market, fundamentally reshaping acute ischemic stroke management. Traditionally, mechanical thrombectomy was restricted to a narrow 6-hour window following stroke onset, significantly limiting patient eligibility. However, robust clinical evidence from landmark trials such as DAWN and DEFUSE 3 has demonstrated that selected patients can safely and effectively benefit from thrombectomy up to 24 hours after symptom onset when guided by advanced imaging. This paradigm shift has substantially expanded the treatable patient population, including those with delayed hospital arrival or wake-up strokes, which were previously excluded from intervention.

The broader treatment window has translated directly into higher procedural volumes across comprehensive stroke centers, driving increased demand for thrombectomy devices. Hospitals are now more likely to invest in advanced stent retrievers, aspiration catheters, and supporting technologies to manage the growing caseload. Additionally, extended eligibility has encouraged wider adoption of sophisticated imaging protocols, such as CT perfusion and MRI-based tissue viability assessments, further integrating thrombectomy into standardized stroke care pathways. From a market perspective, this shift has increased the economic value of each stroke program, as more patients progress to interventional treatment rather than relying solely on medical management. As awareness of extended-window benefits continues to grow among emergency physicians and neurologists, sustained increases in device utilization are expected, reinforcing long-term market growth and innovation.

Restraints - Shortage of Skilled Neurointerventionalists

The shortage of skilled neurointerventionalists remains a critical structural barrier to the expansion of the neurovascular thrombectomy devices market. Mechanical thrombectomy is a highly complex, operator-dependent procedure that requires years of advanced training in neurology, neurosurgery, or interventional radiology, followed by dedicated neurointerventional fellowship experience. This long and resource-intensive training pathway has resulted in a limited global pool of qualified specialists, creating a significant imbalance between rising stroke incidence and procedural capacity. In emerging markets, the challenge is further compounded by inadequate access to accredited training programs, limited exposure to high procedural volumes, and migration of trained specialists toward metropolitan or international healthcare systems offering better compensation and infrastructure.

Rural and semi-urban regions are disproportionately affected, often lacking 24/7 neurointerventional coverage, which restricts timely thrombectomy access for eligible stroke patients. The shortage of skilled personnel also discourages hospitals from investing in advanced thrombectomy devices and catheterization labs, as the risk of underutilization remains high. Additionally, physician burnout and demanding on-call schedules contribute to workforce attrition, further tightening supply. Even in developed regions, uneven distribution of expertise results in procedural bottlenecks at comprehensive stroke centers, limiting patient throughput. Collectively, these workforce constraints significantly restrict market penetration, slow device adoption, and hinder equitable access to life-saving thrombectomy interventions across global healthcare systems.

Opportunity - Increasing Focus on First-Pass Success Rates

The increasing focus on achieving first-pass success in neurovascular thrombectomy procedures represents a significant and evolving market opportunity for device manufacturers. Clinicians and stroke centers are placing greater emphasis on complete and rapid vessel recanalization in a single device pass, as higher first-pass success rates are strongly associated with improved neurological outcomes, shorter procedure times, and lower complication rates. Each additional pass increases the likelihood of endothelial injury, distal embolization, intracranial hemorrhage, and prolonged ischemia, reinforcing the clinical value of devices that can effectively remove the clot on the first attempt.

This clinical shift is driving demand for innovative thrombectomy device designs that offer superior clot engagement, stable retrieval, and enhanced navigability through tortuous cerebral anatomy. Manufacturers are increasingly focusing on optimized stent retriever architectures, larger-bore and more flexible aspiration catheters, and hybrid systems that combine aspiration with mechanical capture to maximize clot integration. Material advancements, such as improved radial force control, surface coatings for better thrombus adherence, and atraumatic designs, are further supporting this trend.

From a hospital and payer perspective, first-pass success aligns closely with efficiency and cost-containment goals. Faster procedures reduce anesthesia time, imaging utilization, and intensive care stays, making high-performance devices attractive in value-based care environments. As clinical benchmarks increasingly incorporate first-pass recanalization as a quality metric, manufacturers that deliver consistently high first-pass success rates are well-positioned to gain competitive differentiation, premium pricing potential, and long-term adoption across advanced stroke care centers.

Category-wise Analysis

By Product Type, the Stent Retriever Segment is leading in the Market

Stent retrievers account for the largest share of the neurovascular thrombectomy devices market, primarily due to their strong clinical validation, consistent performance, and long-standing adoption as a standard treatment for large vessel occlusion strokes. Multiple large-scale randomized clinical trials have demonstrated their ability to achieve high recanalization rates and favorable neurological outcomes, reinforcing physician confidence and driving widespread guideline recommendations. As a result, stent retrievers are often the first-choice device in complex stroke cases, particularly in comprehensive stroke centers.

Their design allows effective clot integration and secure retrieval across varying clot compositions and vessel anatomies, making them suitable for a broad patient population. In addition, continuous product innovations such as improved radial force control, enhanced flexibility, and optimized mesh structures have further strengthened their clinical reliability. From a hospital perspective, familiarity with stent retriever techniques, established training pathways, and predictable procedural outcomes support sustained usage volumes.

While aspiration catheters are gaining momentum due to faster procedures and lower costs, they are frequently used in combination with stent retrievers rather than as replacements. This complementary use further preserves stent retrievers' dominant revenue share, positioning them as the backbone of modern mechanical thrombectomy procedures.

By Application, Acute ischemic stroke Segment Leads the Market

Acute ischemic stroke dominates the neurovascular thrombectomy devices market, accounting for the highest application share due to its prevalence, clinical urgency, and strong guideline support. Acute ischemic stroke, particularly resulting from large vessel occlusion, is the most common neurovascular condition requiring immediate intervention to restore cerebral blood flow. Delays in treatment can lead to irreversible neuronal damage, severe disability, or death, which has driven the widespread adoption of mechanical thrombectomy as a frontline therapy in modern stroke care. Clinical evidence from multiple large-scale trials has consistently demonstrated that timely thrombectomy significantly improves functional outcomes, reduces long-term rehabilitation needs, and lowers overall healthcare costs, further reinforcing its use in acute ischemic stroke management.

In contrast, applications such as cerebral aneurysms and arteriovenous malformations (AVMs) involve smaller patient populations and often require highly specialized or adjunctive devices. These conditions are less frequent and typically managed with a combination of surgical, endovascular, or hybrid approaches, limiting routine thrombectomy use. Additionally, regulatory approvals and clinical protocols for these indications are more restrictive, which constrains device adoption.

The high incidence of acute ischemic stroke globally, coupled with a strong evidence base, dedicated stroke center infrastructure, and growing awareness of the benefits of early intervention, ensures that this application remains the primary driver of the neurovascular thrombectomy market. Consequently, device manufacturers prioritize acute ischemic stroke in product development, marketing, and clinical training initiatives, reinforcing its dominance in overall market share.

Regional Insights

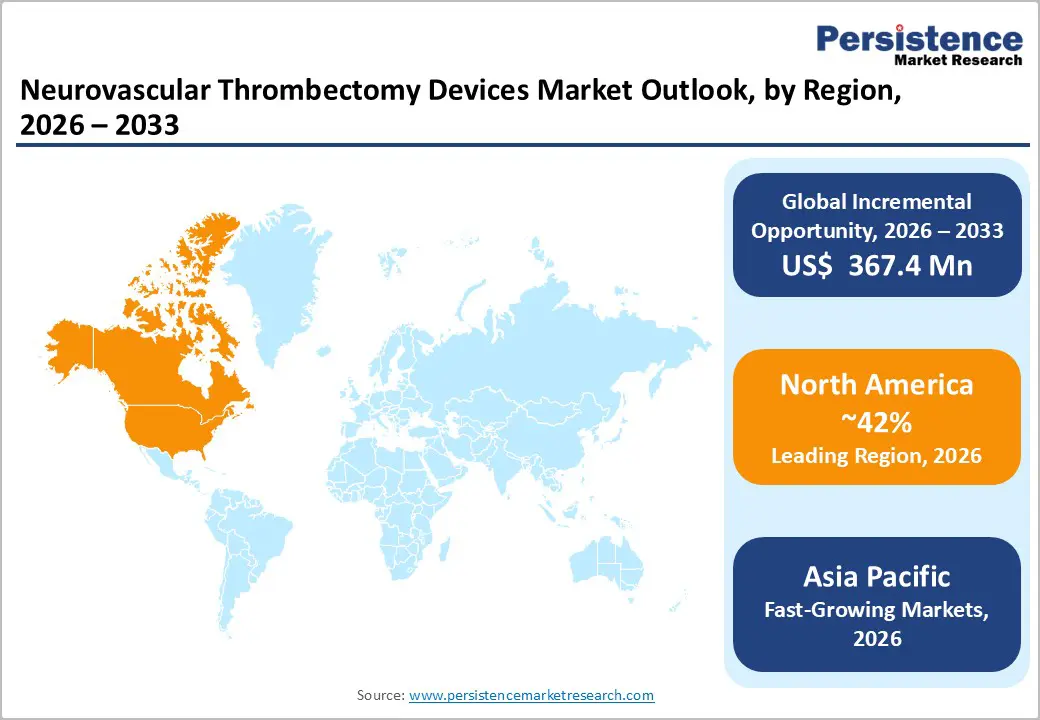

North America Neurovascular Thrombectomy Devices Trends

North America leads the neurovascular thrombectomy devices market due to high healthcare spending, advanced infrastructure, and early adoption of innovative neurointerventional technologies. The region benefits from a well-established network of comprehensive stroke centers, skilled neurointerventionalists, and strong awareness of acute ischemic stroke management among clinicians and patients. Evidence-based guidelines from organizations such as the American Heart Association (AHA) and American Stroke Association (ASA) strongly recommend mechanical thrombectomy for large vessel occlusion strokes, driving procedural volumes and consistent device demand.

The United States, as the largest contributor within North America, plays a pivotal role in market leadership. The growing incidence of stroke, increased public awareness campaigns, and reimbursement policies supporting thrombectomy procedures have accelerated device adoption. Additionally, the presence of leading global thrombectomy device manufacturers, continuous product innovation, and extensive clinical trial activity in the U.S. further strengthens market dominance.

Emerging trends in the region include the adoption of aspiration-first techniques, AI-assisted imaging for faster diagnosis, and hybrid stent-aspiration systems to improve first-pass recanalization rates. These advancements, combined with strong regulatory support and robust hospital infrastructure, ensure North America retains its leading position in the global neurovascular thrombectomy devices market.

Asia Pacific Neurovascular Thrombectomy Devices Market Trends

Asia Pacific is emerging as a high-growth region in the neurovascular thrombectomy devices market, driven by rising stroke prevalence, improved healthcare infrastructure, and increasing awareness of advanced neurointerventional procedures. Countries such as China, Japan, and India are witnessing a growing number of acute ischemic stroke cases, driving demand for mechanical thrombectomy devices. The expansion of comprehensive stroke centers, government initiatives to improve stroke care, and increased investments in healthcare facilities are facilitating wider adoption of these devices.

Emerging trends in the region include the gradual adoption of aspiration-first and hybrid thrombectomy techniques, as well as integration with advanced imaging technologies to enable faster diagnosis and improved procedural outcomes. Although adoption is still lower than in North America and Europe, rising physician awareness, ongoing training programs, and partnerships with global device manufacturers are accelerating market growth. Cost-optimized solutions for price-sensitive markets and expanding health insurance coverage further enhance accessibility, positioning Asia Pacific as the fastest-growing market for neurovascular thrombectomy devices.

Competitive Landscape

The competitive landscape of the neurovascular thrombectomy devices market is highly dynamic and innovation-driven, with companies focusing on product differentiation, clinical efficacy, and procedural efficiency. Key strategies include continuous technological advancements in stent retrievers and aspiration systems, development of hybrid devices, and integration with advanced imaging platforms. Manufacturers are also investing in clinical trials, physician training programs, and strategic partnerships to expand market reach.

Key Industry Developments:

- In April 2025, Anaconda Biomed, S.L., a medical technology company developing next-generation neurothrombectomy devices, enrolled and treated the first U.S. patient in its ATHENA clinical trial. The procedure was performed by Shahram Majidi, MD, Associate Professor of Neurosurgery, Neurology, and Radiology at the Icahn School of Medicine at Mount Sinai, New York

- In February 2025, Johnson & Johnson MedTech launched the CEREGLIDE 92 Catheter System, a next-generation 0.092" catheter with the INNERGLIDE 9 delivery aid, which was indicated for facilitating the insertion and guidance of interventional devices in the neurovascular system.

Companies Covered in Neurovascular Thrombectomy Devices Market

- Medtronic Plc

- Stryker Corporation

- Teleflex Incorporated

- Terumo Corporation

- Johnson & Johnson Services, Inc.

- Penumbra Inc.

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Acandis GmbH

- Argon Medical Inc

- Others

Frequently Asked Questions

The global neurovascular thrombectomy devices market is projected to be valued at US$824.9 Mn in 2026.

The increasing prevalence of ischemic strokes worldwide boosts demand for rapid and effective thrombectomy interventions.

The global neurovascular thrombectomy devices market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Rapid growth of healthcare infrastructure in Asia-Pacific, Latin America, and the Middle East presents untapped demand for neurovascular devices.

Medtronic Plc, Stryker Corporation, Teleflex Incorporated, Terumo Corporation, Johnson & Johnson MedTech, and others.