- Plastics, Polymers & Resins

- mLLDPE Market

mLLDPE Market Size, Share and Growth Forecast, 2026-2033

mLLDPE Market by Product Type (C6, C8), Process (Blow Molding, Cast, Extrusion, Others), End-Use (Agriculture, Food, Others), and Regional Forecast for 2026-2033

mLLDPE Market Share and Trends Analysis

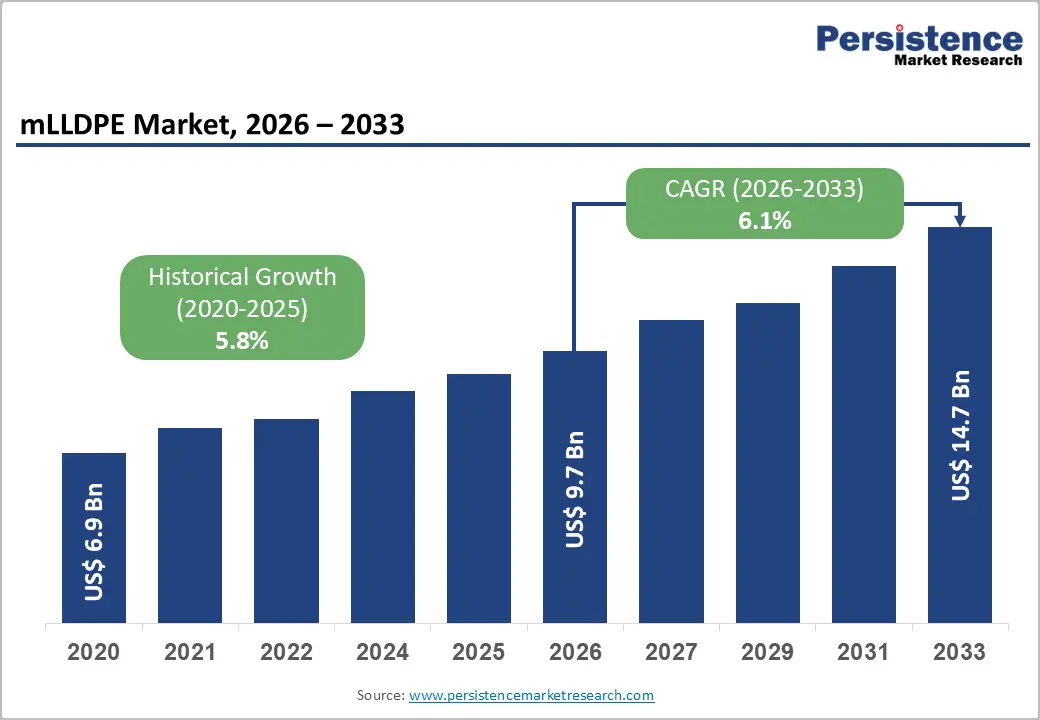

The global mLLDPE market size is likely to be valued at US$ 9.7 billion in 2026, and is projected to reach US$14.7 billion by 2033, growing at a CAGR of 6.1% during the forecast period 2026 - 2033.

This market is expanding steadily, as converters and brand owners increasingly adopt high-performance polymer solutions for flexible packaging, agricultural films, and industrial applications, seeking greater material efficiency and product protection. The material has provided enhanced clarity, toughness, and reliable sealing performance compared with conventional linear low-density polyethylene (LLDPE), enabling processors to downgauge films while maintaining or improving functionality and appearance.

Manufacturers and end-users are currently focusing on applications such as e-commerce mailers, food pouches, and advanced farm films, where durability, seal integrity, and shelf appeal are critical differentiators. At the same time, sustainability expectations have been reshaping specifications, and mLLDPE has been featuring in strategies that combine source reduction, recyclability, and improved product preservation.

Key Industry Highlights

- Dominant Product Types: C6 mLLDPE is projected to lead with an estimated 61% revenue share in 2026, while C8 mLLDPE is expected to register the fastest growth at a 6.5% CAGR through 2033, driven by a strong demand for high-clarity and impact-resistant films.

- Leading Process Types: Cast process is expected to dominate at about 35% in 2026, while blow molding is likely to grow the fastest at nearly 7% CAGR through 2033, supported by mLLDPE adoption in automotive components.

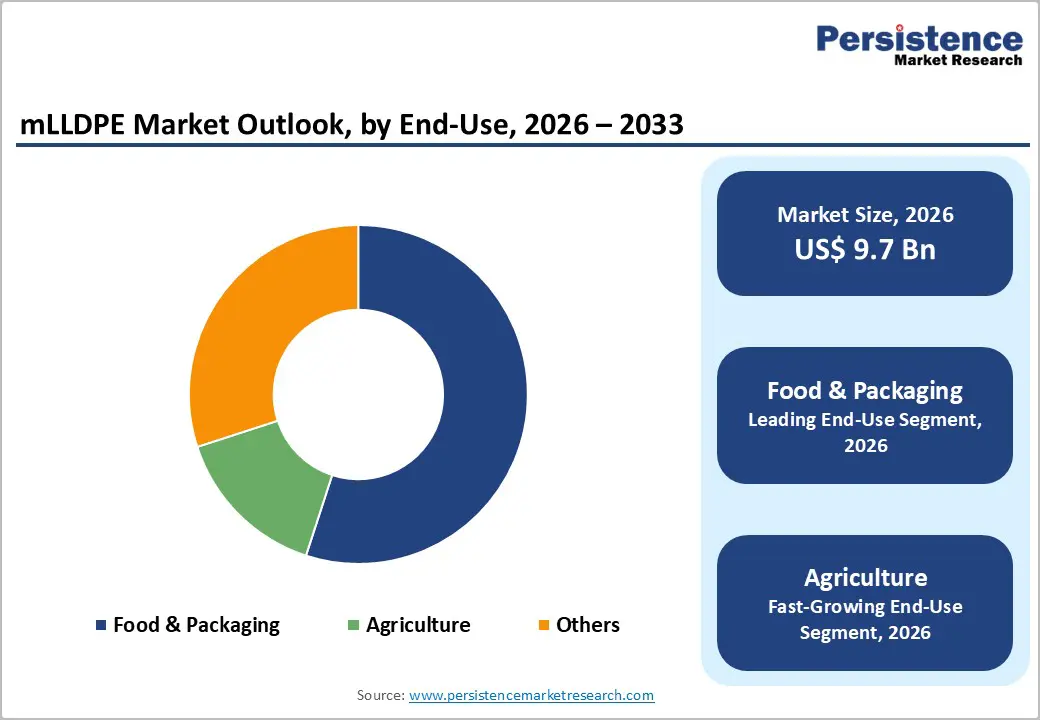

- Leading End-Uses: Food & packaging is anticipated to hold roughly 55% share in 2026, whereas agriculture is set to grow the fastest at a 7.2% CAGR from 2026 to 2033, driven by mulch films, greenhouse covers, and irrigation liners.

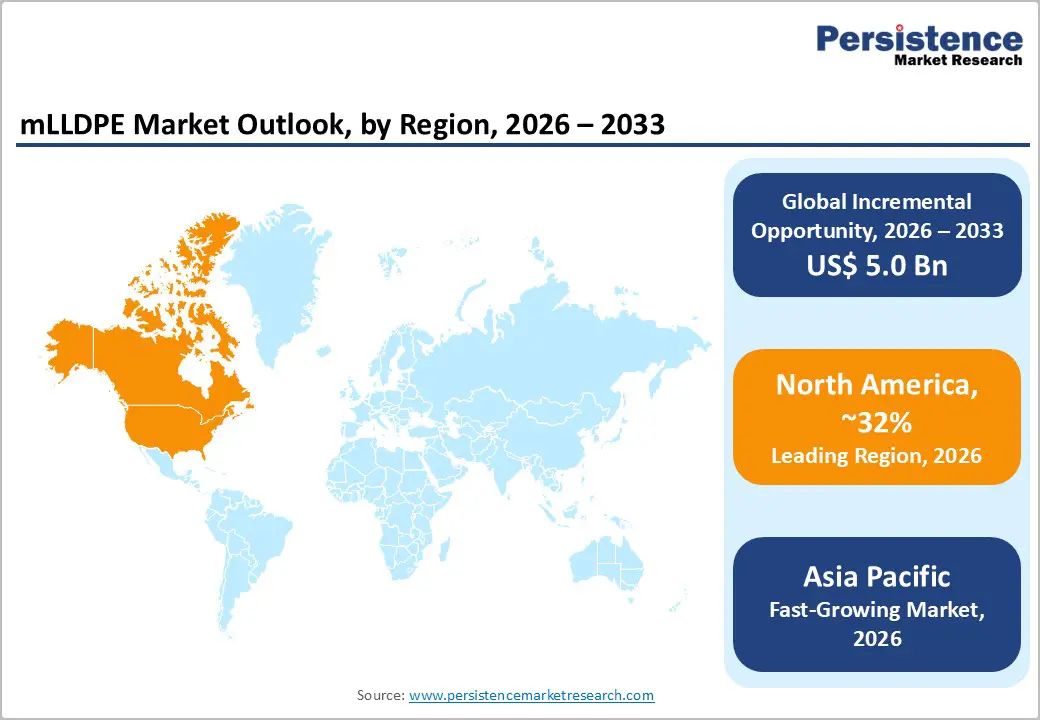

- Regional Leadership: North America is expected to command a share of around 32% in 2026, while Asia Pacific is poised to be the fastest-growing market with a projected 7.8% CAGR, fueled by rapid industrialization and massive packaging demand.

- Competitive Environment: Key industry players are driving market momentum through capacity expansions, new product launches, and strategic regional investments, emphasizing innovation and sustainability.

- Sustainability & Innovation: The adoption of mLLDPE continues to be supported by downgauging initiatives and recyclable polymer solutions, aligning with global sustainability mandates and increasing material efficiency across end-use sectors.

| Key Insights | Details |

|---|---|

| mLLDPE Market Size (2026E) | US$ 9.7 Bn |

| Market Value Forecast (2033F) | US$ 14.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Industry-wide Demand for High Performance mLLDPE

The demand for mLLDPE is being driven by its expanding use in flexible packaging, industrial films, and agricultural materials, as well as by the need for polymers with high tensile strength, clarity, sealability, and durability. In packaging, metallocene linear low-density polyethylene enables thinner, high-strength films that support cost-efficiency and sustainability objectives while meeting performance requirements across the food, beverage, and consumer goods segments.

Growth in e-commerce and logistics further amplifies demand for lightweight, durable packaging materials. Its superior mechanical properties allow manufacturers to downgauge materials, enhancing material efficiency and reducing waste while supporting environmental compliance. These trends reinforce the ongoing shift toward high-performance polymers across major downstream sectors.

Supporting this dynamic, SIBUR introduced a new high-performance mLLDPE grade, tailored for FMCG and flexible packaging producers, delivering improved strength, puncture resistance, and optical properties that enable downgauging and enhanced film performance, directly addressing market demand for sustainable, high-performance film solutions.

Emerging economies in Asia Pacific and Latin America are also contributing significantly as industrialization, infrastructure build-out, and agricultural modernization expand polymer consumption in irrigation films, geomembranes, and industrial liners. With increasing regulatory emphasis on recyclable and lightweight materials, what is the role of metallocene linear low-density polyethylene as a material-efficient, high-performance polymer is critical for addressing both performance and sustainability priorities across global end uses.

Feedstock Price Volatility and Processing Barriers Constraining mLLDPE Expansion

The mLLDPE market's growth continues to face significant headwinds from feedstock price volatility, particularly fluctuations in ethylene and crude oil costs, which directly affect producer margins and downstream pricing strategies. These unpredictable cost swings make procurement planning and capital investment decisions more challenging, often delaying capacity expansion or new project commitments.

Cyclicality in petrochemical feedstocks can suppress profitability, especially during periods of supply disruptions or geopolitical instability, contributing to conservative investment behavior among producers. As a result, short-term market confidence can waver, impacting order books and long-range strategic planning. This constraint is amplified in markets where feedstock expenses constitute a large portion of total production costs.

Compounding these economic pressures are processing compatibility issues for smaller converters, who often rely on legacy extrusion and film equipment optimised for conventional LLDPE. Adopting metallocene linear low-density polyethylene grades frequently requires capital investment in updated systems and process reformulations, creating a barrier to entry and slowing penetration in price-sensitive developing markets.

LG Chem and Lotte Chemical announced restructuring initiatives to reduce naphtha-cracking capacity and improve efficiency, in response to thin margins and oversupply challenges across Asia’s petrochemical sector, highlighting industry efforts to adapt to cost pressures and supply constraints. Addressing these barriers through technology partnerships, converter training, and flexible processing solutions is essential to unlock broader metallocene linear low-density polyethylene adoption.

Expanding Applications and Sustainability Initiatives Driving mLLDPE Market Expansion

The market is benefiting from expansion into emerging specialty applications such as medical packaging, pharmaceutical films, and advanced industrial liners, which require high clarity, chemical resistance, and sterilizability. These applications enable mLLDPE to displace conventional materials and unlock premium revenue streams. Growth in flexible packaging is further supported by the polymer’s strength, puncture resistance, and downgauging potential, aligning with sustainability objectives.

Additionally, agricultural films such as mulch covers, greenhouse films, and irrigation liners rely on metallocene linear low-density polyethylene’s durability and mechanical resilience, providing long-term adoption opportunities across high-growth markets. These combined applications broaden the market’s addressable scope and reinforce long-term demand.

A notable example in this context is the commissioning of a new 730,000 t/yr LLDPE unit in Huizhou, China, by ExxonMobil in February 2025, with plans to supply part of its output as high-performance mLLDPE. This strategic expansion targets growing demand for advanced polyethylene grades in flexible packaging and industrial films across Asia. The development underscores industry efforts to enhance supply and support innovation in high-performance polymers.

Rising global food demand and modernization of agriculture further bolster the adoption of mLLDPE in irrigation liners, mulch films, and greenhouse covers, making this combination of technical innovation and sustainability-driven applications a critical long-term growth opportunity for the market.

Category-wise Analysis

Product Type Insights

The C6 variant is likely to lead, commanding an estimated 61% of the mLLDPE market revenue share in 2026 due to its balanced strength, flexibility, and suitability for a wide range of film and liner applications. C6 grades are widely adopted in flexible packaging, stretch films, and industrial liners, where mechanical performance and processability are essential. Their dominance is reinforced by broad converter familiarity and compatibility with existing film lines, which supports stable volume demand across major regions, including North America and the Asia Pacific. As majors expand production networks and supply chain integration, the C6 product type remains a workhorse for standard and heavy-duty applications.

Is the C8 type expected to be the fastest-growing product segment, projected to display a 2026-2033 CAGR of 6.5% on the strength of its exceptional impact resistance and optical clarity. These attributes make C8 grades especially attractive in premium packaging, medical films, and high-performance industrial applications where enhanced mechanical properties justify material selection. Supporting this trend, Repsol’s planned 300,000-tpa mLLDPE plant in Sines, Portugal, adds targeted capacity for advanced polymer grades, reflecting strategic investment in higher-value product variants that align with evolving converter and brand requirements.

Process Type Insights

The cast platform is anticipated to dominate the production landscape with a 35% market share of overall output due to its versatility and ability to produce a wide variety of film formats. Cast processes are preferred for high-clarity, flat films with excellent optical properties. Its dominance is reinforced by strong installed base infrastructure in markets such as North America, Europe, and Asia Pacific as converters seek consistent film quality and operational flexibility.

Blow molding is projected to be the fastest-growing process segment, with an estimated 7% CAGR through 2033, driven by the increasing demand for lightweight automotive components, durable containers, and specialized industrial parts where metallocene linear low-density polyethylene’s toughness and elongation are advantageous. Its growth is supported by investments in downstream equipment and material technologies that improve cycle times and product performance.

A key 2025 development supporting this shift is Dow’s start-up of a new 600,000t/y HDPE/LLDPE swing unit in Freeport, Texas, capable of producing high-performance octene co-monomer variants relevant to advanced blown film and molded products. This capacity expansion enhances the supply of tailored resin grades that converters need for blow molding applications.

End-Use Insights

The food & packaging segment is expected to lead the end use demand for mLLDPE, capturing an estimated 55% share in 2026 as flexible packaging formats such as films, pouches, wraps, and courier bags remain the largest consumption drivers. Metallocene linear low-density polyethylene’s high tensile strength, puncture resistance, and sealing performance meet stringent food safety and shelf-life requirements, while its ability to support downgauging aligns with cost and sustainability goals. A broad spectrum of industries, from food and beverages to consumer goods, depends on reliable, high-performance films, making packaging the foundational demand pillar for mLLDPE resin producers worldwide.

The agriculture segment is projected to be the fastest-growing end use, exhibiting an approximate CAGR of 7.2% and demand rising rapidly as advanced materials replace conventional polymers in mulch films, greenhouse covers, silage wraps, and irrigation liners. The growth in this segment is propelled by the modernization of farming practices, especially in the Asia Pacific and Latin America, where improved crop yields and resource efficiency are priorities.

Reinforcing this expansion, Borealis launched a new high-performance recycled PE grade designed for flexible packaging applications, signaling broader industry focus on recyclable polymers that also serve robust end-use sectors such as agricultural films. This trend supports the adoption of high-performance and sustainable mLLDPE solutions across the agricultural landscape.

Regional Insights

North America mLLDPE Market Trends

North America is expected to stand as the leading regional market, securing an estimated 32% of the mLLDPE market share in 2026, supported by strong demand from flexible packaging, industrial films, and agricultural applications. The region benefits from advanced polymer processing infrastructure, abundant feedstock availability, and early adoption of high-performance film technologies. Packaging applications dominate consumption, particularly in food, healthcare, and e-commerce logistics.

The United States continues to anchor regional demand, with consistent uptake of downgauged and recyclable film structures. Overall market growth is steady, driven by performance-oriented material selection rather than volume expansion. Innovation and material compliance remain central to regional competitiveness.

The U.S. Department of Agriculture (USDA) expanded sustainability-linked funding programs aimed at improving packaging efficiency for food and export supply chains, indirectly supporting the adoption of downgauged polyethylene films. This initiative reinforced demand for high-performance polymers that enable material reduction while maintaining safety and durability. Regulatory emphasis on food-contact compliance and recyclability continues to influence resin selection. Competitive intensity remains high among major petrochemical producers, driving incremental product innovation. These factors collectively sustain North America’s leadership position while ensuring long-term market stability.

Europe mLLDPE Market Trends

Europe represents a mature and regulation-driven mLLDPE market, shaped by stringent sustainability, recyclability, and material efficiency mandates. Packaging and industrial applications remain the primary demand centers, supported by well-established converting industries across Germany, France, the UK, and Southern Europe. Adoption of metallocene linear low-density polyethylene is closely tied to its ability to support mono-material structures and downgauging. Regulatory alignment across the European Union (EU) continues to guide polymer selection toward recyclable polyethylene solutions. Growth remains moderate, reflecting market maturity rather than structural demand weakness.

One prominent example is the inauguration of a new mechanical recycling facility in Porto Marghera, Italy, by Versalis (Eni) aimed at supplying recycled polymers for packaging and industrial applications. This development strengthened Europe’s circular economy infrastructure and increased focus on compatibility between virgin and recycled polyethylene (PE) grades. The move encouraged converters to prioritize materials that integrate efficiently into recycling streams. Ongoing policy reinforcement under EU packaging regulations continues to favor high-performance, recyclable polymers. As a result, metallocene linear low-density polyethylene maintains strategic relevance in Europe’s evolving polymer landscape.

Asia Pacific mLLDPE Market Trends

Asia Pacific is projected to be the fastest-growing regional market for mLLDPE, with a CAGR of about 7.2% during the 2026-2033 forecast period, driven by the expansion of the industrial, packaging, and agricultural sectors. Countries such as China, India, Japan, and the economies of ASEAN lead this growth due to rising consumer goods production, rapid urbanization, expanding e-commerce markets, and modernized agricultural practices.

The region’s growth rate significantly outpaces other geographies, as manufacturers increase capacity investments to meet both domestic and export demand. Metallocene linear low-density polyethylene adoption in flexible films, irrigation liners, and consumer packaging underpins broad usage. Rapid infrastructure development and enhancements in polymer processing further reinforce regional demand momentum.

ExxonMobil’s petrochemical complex in Huizhou, China entered test operations, including LLDPE facilities capable of supplying high performance polymer feedstock that can be shifted toward metallocene linear low density polyethylene variants to address flexible packaging and industrial requirements across Asia Pacific. Southeast Asian nations are also advancing sustainability policies such as mandatory recyclability targets and PFAS restrictions, further catalyzing the demand for monomaterial PE packaging and circular solutions in the region. These developments, combined with favorable demographics and manufacturing growth, position Asia Pacific as a central driver of metallocene linear low-density polyethylene market expansion through the next decade.

Competitive Landscape

The global mLLDPE market structure is characterized by moderate consolidation, with leading petrochemical producers such as ExxonMobil, Dow, LyondellBasell, SABIC, and Borealis controlling a major portion of worldwide production capacity. These companies have been leveraging integrated feedstock supply, proprietary metallocene catalyst technologies, and extensive manufacturing networks to ensure a steady output of high-performance mLLDPE grades for packaging, agricultural, and industrial applications. Their ability to invest continuously in resin innovations focused on downgauging has allowed them to maintain a competitive edge and respond effectively to evolving customer requirements.

Regional producers in the Asia Pacific and the Middle East have been supporting global supply by providing cost-effective mLLDPE grades that are tailored to local market demands. However, high capital requirements, stringent catalyst intellectual property rights, and rigorous food-contact compliance standards have been creating significant entry barriers for new competitors. Market differentiation is increasingly being driven by application-specific formulations and alignment with sustainability goals, with more producers collaborating closely with converters and brand owners. Going forward, competition will likely be shaped by capacity expansions and strategic technology partnerships, rather than large-scale consolidation, as companies seek to balance innovation, compliance, and market responsiveness.

Key Industry Developments

- In October 2025, Cargill introduced Incroflo™ P50, a next-generation bio-based polymer processing aid (PPA) for LLDPE film extrusion. Designed to replace fluoropolymer PPAs amid rising PFAS regulatory pressure, the product improves melt flow, eliminates surface defects such as sharkskin, and enhances film clarity. With approximately 86% bio-based content, Incroflo™ P50 supports sustainability goals while improving throughput and processing efficiency.

- In August 2025, SIBUR developed mLL20183 FE, a new mLLDPE grade for flexible FMCG packaging such as barrier films, lamination, dairy packs, and stretch wraps. It matches foreign equivalents in strength, tear resistance, sealing, and processability, enabling efficient blown film production and cost savings.

- In May 2025, Univation Technologies announced a new world-scale UNIPOL™ PE Process design with a single-line capacity of 800,000 tons per year. The platform enables flexible production of HDPE, LLDPE, and metallocene PE resins, leveraging advanced catalyst systems such as XCAT™ metallocene catalysts. This development improves economies of scale, lowers capital cost per tonne, and enhances production adaptability.

Companies Covered in mLLDPE Market

- ExxonMobil Corporation

- Dow Inc.

- Chevron Phillips Chemical Company LLC

- LyondellBasell Industries N.V.

- SABIC

- INEOS Group Limited

- TotalEnergies SE

- LG Chem Ltd.

- Prime Polymer Co., Ltd.

- Mitsui Chemicals

- Borealis AG

- Formosa Plastics Group

Frequently Asked Questions

The global mLLDPE market is projected to reach US$ 9.7 billion in 2026.

Rising demand for high-performance flexible packaging, increasing focus on downgauging and material efficiency, and growing adoption of advanced polymer films in agriculture and industrial applications are driving the market.

The market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Prime opportunities include sustainable mono-material packaging, expansion into specialty and medical films, and rising demand for high-durability agricultural films in emerging economies.

ExxonMobil Corporation, Dow Inc., LyondellBasell Industries, SABIC, and Borealis are some of the key players in the market.