- Executive Summary

- Global Mine Backfill Services Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Mining Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Mine Backfill Services Market Outlook: By Backfill Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by By Backfill Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- Market Attractiveness Analysis: By Backfill Type

- Global Mine Backfill Services Market Outlook: By Service Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by By Service Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- Market Attractiveness Analysis: By Service Type

- Global Mine Backfill Services Market Outlook: By Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by By Application, 2020-2025

- Current Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- Market Attractiveness Analysis: By Application

- Global Mine Backfill Services Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- North America Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- North America Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- Europe Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- Europe Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- Europe Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- East Asia Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- East Asia Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- East Asia Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- South Asia & Oceania Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- South Asia & Oceania Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- South Asia & Oceania Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- Latin America Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- Latin America Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- Latin America Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- Middle East & Africa Mine Backfill Services Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by By Backfill Type, 2026-2033

- Paste Fill

- Hydraulic Fill

- Cemented Rock Fill (CRF)

- Middle East & Africa Market Size (US$ Bn) Forecast, by By Service Type, 2026-2033

- Consulting Services

- Material Delivery

- On-site Backfill System Implementation

- Middle East & Africa Market Size (US$ Bn) Forecast, by By Application, 2026-2033

- Metal Mining

- Coal Mining

- Industrial Mineral Mining

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- BASF Construction Chemicals

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Normet Group

- SRK Consulting

- Golder Associates

- FLSmidth

- Paterson and Cooke

- Metso Outotec

- Sika AG

- Barrick Gold Corporation

- Victaulic

- CEC Mining Systems

- Hatch Ltd.

- Others

- BASF Construction Chemicals

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Metals & Minerals

- Mine Backfill Services Market

Mine Backfill Services Market Size, Share, and Growth Forecast 2026 - 2033

Mine Backfill Services Market by Backfill Type (Paste Fill, Hydraulic Fill, Cemented Rock Fill), by Service Type (Consulting Services, Material Delivery, On-site Backfill System Implementation), by Application (Metal Mining, Coal Mining, Industrial Mineral Mining), and Regional Analysis, 2026 - 2033

Mine Backfill Services Market Size and Trend Analysis

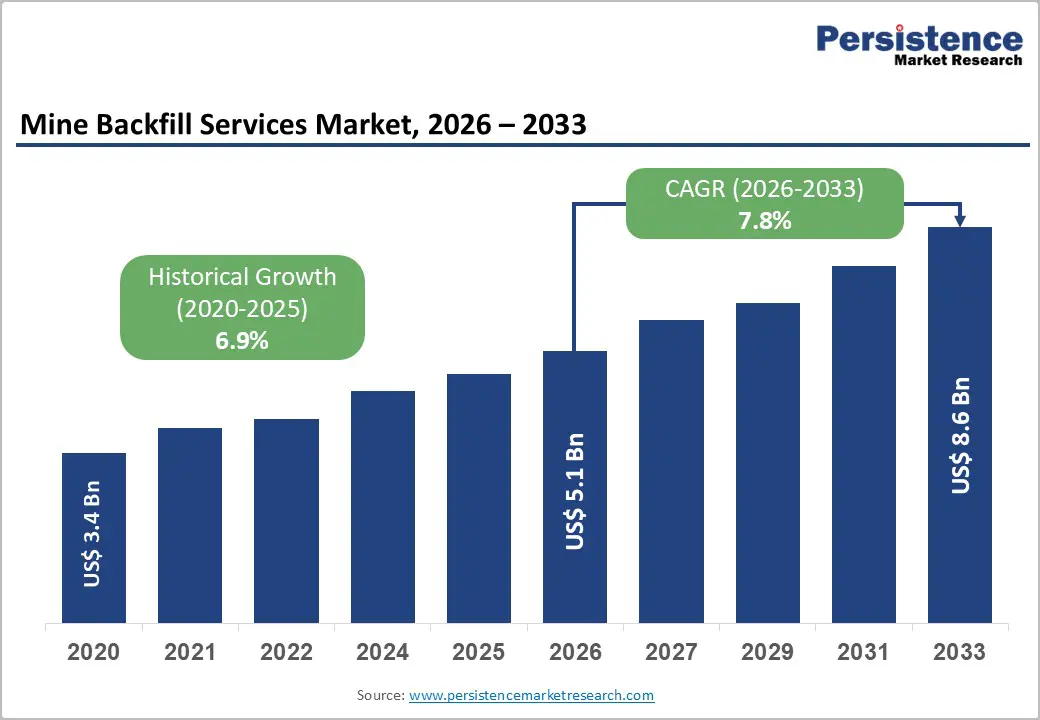

The global Mine Backfill Services market size is likely to be valued at US$ 5.1 billion in 2026 and is expected to reach US$ 8.6 billion by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033.

The market's sustained and accelerating growth is fundamentally driven by the global mining industry's expanding adoption of underground mining methods, particularly cut-and-fill and sublevel stoping techniques, which mandate engineered backfill systems for ground stability, mine void management, and regulatory compliance with occupational safety standards.

Key Industry Highlights:

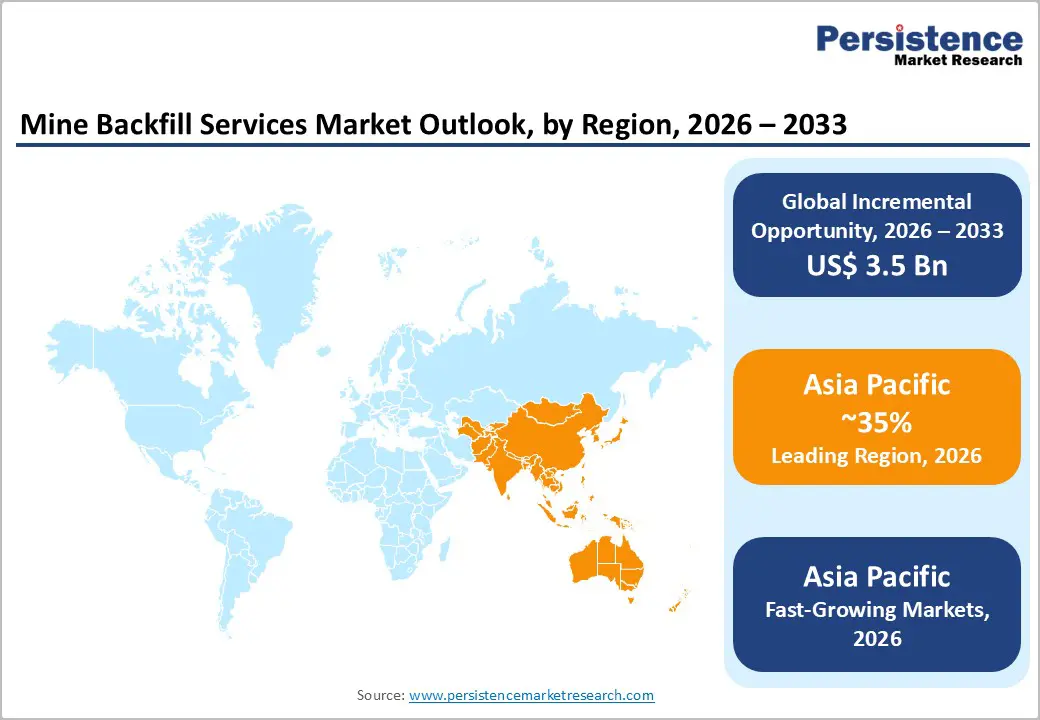

- Leading Region: Asia Pacific leads the Mine Backfill Services market with 35% share, supported by China’s large underground mine base, Australia’s paste fill innovation ecosystem, and strong critical mineral mining developments across China, Australia, and India.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 8.7%, due to stricter mining safety regulations in China and India, along with expanding deep underground mining programs in Australia requiring advanced paste and cemented backfill systems.

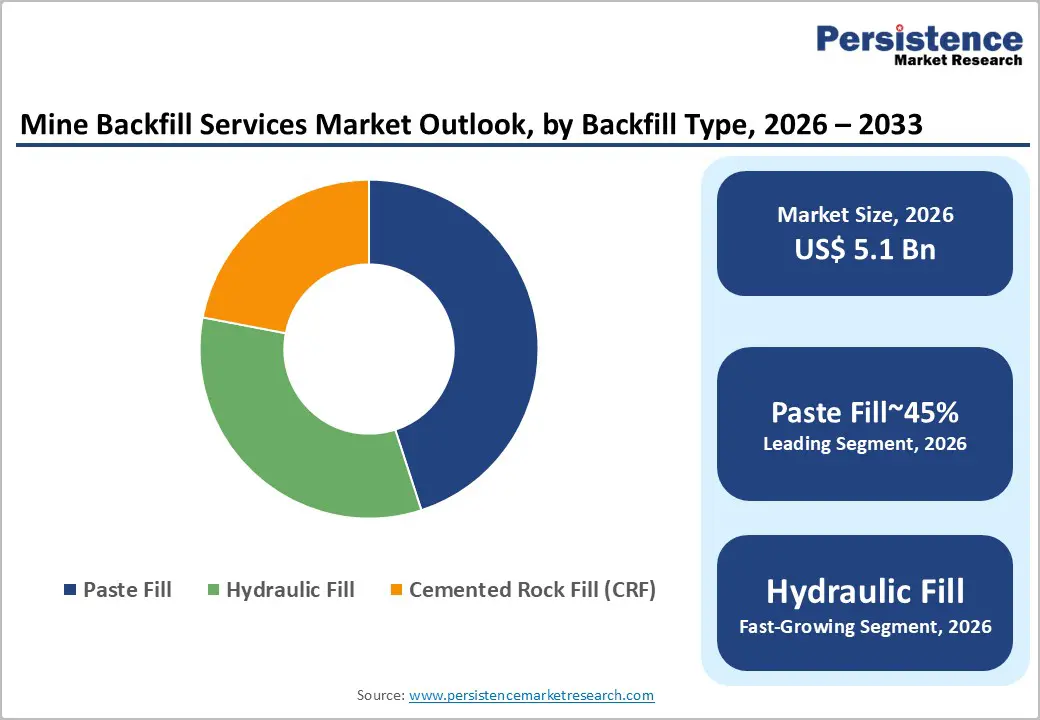

- Leading Segment: Paste Fill leads the Backfill Type segment with around 45% share, supported by global tailings risk regulations, strong technical validation, and growing adoption by major mining companies for improved underground stability and safety.

- Fastest-Growing Segment: On-site Backfill System Implementation is the fastest-growing service segment, accounting for about 9.2% CAGR, driven by rising underground mine construction projects and the complex engineering requirements of paste fill plant installation.

- Key Opportunity: Rapid expansion of underground mining for critical minerals and stricter global tailings management standards create major growth opportunities for engineering firms and backfill service providers supporting new mine development projects.

| Key Insights | Details |

|---|---|

|

Mine Backfill Services Market Size (2026E) |

US$ 5.1 Billion |

|

Market Value Forecast (2033F) |

US$ 8.6 Billion |

|

Projected Growth CAGR (2026–2033) |

7.8% |

|

Historical Market Growth (2020–2025) |

6.9% |

Market Dynamics

Drivers - Critical Minerals Demand and Deep Underground Mining Expansion Mandating Advanced Backfill System Adoption

The rapid global shift toward clean energy is significantly increasing the demand for critical minerals such as copper, nickel, cobalt, lithium, gold, and silver, which are essential for electric vehicle batteries, renewable energy infrastructure, and modern power grids. As mining companies attempt to meet this demand, they are increasingly developing deeper underground ore bodies where advanced backfill systems are no longer optional but essential for safe and efficient mining operations. The International Energy Agency’s Critical Minerals Market Review 2023 highlights that demand for minerals used in clean energy technologies could grow more than 3.5 times by 2030 and over six times by 2040 compared to 2020 levels.

This rapid expansion is driving investment in deeper underground mines where paste fill and cemented rock fill systems are necessary to maintain stability in mined-out spaces. Major mining operations such as BHP Group’s Olympic Dam in Australia, Newmont Corporation’s underground mines in Nevada and Ghana, and Glencore’s polymetallic mines in Canada and the Democratic Republic of Congo demonstrate the scale of backfill demand. Leading mining equipment companies such as Metso Outotec and FLSmidth have also increased investment in paste backfill technologies, recognizing the long-term growth potential of this services segment.

Global Tailings Storage Facility Risk Reduction Policies Accelerating Transition to Underground Paste Fill Utilization

The global mining industry is undergoing a major shift in tailings management strategies following several catastrophic dam failures, most notably the Brumadinho disaster in Brazil in January 2019 that resulted in 270 deaths and financial losses exceeding US$7 billion for Vale S.A. Earlier failures such as the Fundão dam incident in 2015 also highlighted the environmental and social risks associated with traditional tailings storage facilities. As a result, mining companies are increasingly redirecting tailings materials into underground mine voids through paste fill systems rather than storing them on the surface.

The Global Industry Standard on Tailings Management (GISTM), introduced in August 2020 by the International Council on Mining and Metals, the United Nations Environment Programme, and the Principles for Responsible Investment, has created strict guidelines for tailings risk management. These regulations encourage mining operators to adopt underground paste fill wherever technically feasible. Engineering consultancies such as Paterson and Cooke and SRK Consulting have reported a surge in requests for paste fill feasibility studies and plant design services. Additionally, Brazil’s National Mining Agency has mandated the closure of upstream tailings dams by 2025 and banned new upstream constructions, further accelerating paste fill adoption across mining operations.

Restraints - High Capital Investment Requirements for Paste Fill Plant Infrastructure Creating Adoption Barriers at Smaller Mines

Despite its technical advantages, the adoption of paste fill systems is often limited by the high capital investment required to build the necessary infrastructure. Establishing a complete underground paste backfill system requires several specialized components, including high-density thickener tanks, paste mixing equipment, agitation systems, high-pressure pump units, underground distribution pipelines, and advanced monitoring systems to control slurry behaviour. The total capital investment for such systems typically ranges between US$15 million and US$50 million depending on the plant capacity, mining depth, and pipeline complexity.

This level of investment can be difficult for smaller mining companies or operations with limited financial resources to justify. Mines with marginal ore economics may struggle to secure financing for large infrastructure projects, particularly during early production phases. According to the World Gold Council, junior and mid-tier gold mining companies operating smaller underground mines are more likely to rely on lower-cost alternatives such as hydraulic fill or dry rock fill. As a result, high infrastructure costs continue to limit the broader adoption of paste fill systems across smaller mining operations.

Technical Complexity of Paste Fill Rheology Management Creating Operational Risk and Requiring Specialized Expertise

Operating an underground paste backfill system requires careful management of slurry rheology, which includes controlling paste density, yield stress, and flow behavior throughout the entire pipeline network from the surface plant to underground filling points. Improper management of these parameters can result in serious operational issues such as pipeline blockages, pump failures, or interruptions in the backfill delivery system. These problems can halt mining operations and lead to costly repairs and production losses.

The Canadian Institute of Mining, Metallurgy and Petroleum has identified pipeline blockages as one of the most disruptive operational failures in paste fill systems. Clearing blocked pipelines can take several days and may require replacement of pipeline sections, resulting in significant downtime. Because of this technical complexity, mining companies require highly skilled engineers and trained operators to manage paste plant operations effectively. In emerging mining regions such as West Africa, Central Asia, and Southeast Asia, the availability of trained backfill specialists is limited. This shortage of technical expertise often discourages mining companies from adopting advanced paste fill systems.

Opportunity - Critical Mineral Mining Boom and Battery Metal Underground Mine Development Generating Greenfield Backfill Demand

The global surge in demand for critical minerals required for clean energy technologies is creating a major opportunity for mine backfill service providers. According to projections from the International Energy Agency, demand for minerals used in renewable energy systems, electric vehicles, and battery technologies could increase more than six times by 2040. This surge in demand is encouraging mining companies to develop new underground mines for copper, nickel, cobalt, and lithium across several regions. S&P Global Market Intelligence has reported that more than 200 copper mining projects were under development globally as of 2023, many of which involve deep underground ore bodies.

Countries such as Chile, Peru, the Democratic Republic of Congo, and Australia are witnessing significant investment in underground mining infrastructure. Large projects like Codelco’s Chuquicamata Underground conversion in Chile and the West Musgrave copper-nickel project in Western Australia demonstrate the scale of upcoming mining developments that require advanced backfill systems. Engineering firms such as Normet Group and Hatch Ltd. are positioning themselves to support these projects by providing integrated backfill system design, construction, and operational support services.

Digital Transformation and Smart Backfill System Monitoring Creating Premium Technology Service Opportunities

The mining industry’s broader digital transformation is creating new opportunities for technology-driven backfill services. Modern mining operations increasingly rely on advanced monitoring systems, automation technologies, predictive maintenance tools, and centralized remote operations centers to improve productivity and safety. Backfill service providers are now integrating digital monitoring platforms that allow mining operators to track paste rheology, pipeline pressure, pump performance, and system flow conditions in real time. These systems help prevent pipeline blockages, optimize plant performance, and improve overall operational efficiency.

Research programs led by Mining3 and Australia’s CSIRO Deep Earth Resources initiative are developing advanced sensor technologies and machine learning algorithms capable of predicting pipeline flow behavior and adjusting operating parameters automatically. Leading equipment manufacturers such as FLSmidth and Metso Outotec are integrating advanced process control systems into paste fill plants to improve operational reliability. At the same time, chemical companies such as BASF Construction Chemicals are offering specialized admixtures that improve paste strength and performance, creating additional value-added services for technologically advanced mining operations.

Category-wise Analysis

By Backfill Type Insights

Paste Fill leads the global Mine Backfill Services market by backfill type, accounting for approximately 45% of total segment revenue in 2026. This strong position is supported by paste fill’s superior technical performance, its alignment with global tailings management risk-reduction policies under the Global Industry Standard on Tailings Management (GISTM), and its increasing inclusion as a mandatory component in modern underground mine designs targeting deep, high-value ore bodies that require engineered ground control systems. Paste fill is characterized by a thick slurry containing 20% more solids than conventional hydraulic fill, with a non-segregating and non-draining consistency that enhances operational efficiency.

It improves stope filling effectiveness, reduces drainage water management needs, and provides higher in-situ strength when combined with cement additives. The technology also allows mining companies to reuse entire tailings streams that would otherwise require disposal in regulated tailings storage facilities (TSFs). The Australian Centre for Geomechanics (ACG) at the University of Western Australia has reported steady global growth in paste fill adoption as the preferred method for new underground mine developments. Cemented Rock Fill (CRF) represents around 30% of segment revenue due to its high compressive strength and suitability for pillar replacement in metal mines, while Hydraulic Fill holds the remaining share, mainly used in older underground mining operations.

By Service Type Insights

On-site Backfill System Implementation leads the global Mine Backfill Services market, accounting for approximately 52% of total revenue in 2026. This dominance is due to the significant capital investment and engineering complexity required for constructing paste fill and cemented rock fill plants, which represent the largest expenditure in the backfill services value chain. Services typically include construction, installation of thickeners and pumps, underground pipeline installation, system commissioning, mix design development, operator training, and performance testing.

Key providers include Normet Group, Metso Outotec, and FLSmidth, which excel in integrated engineering design and proprietary technology. Consulting Services represent about 28% of revenue, covering feasibility studies, plant design, regulatory compliance, and backfill strategy, with major firms like SRK Consulting, Golder Associates, Paterson and Cooke, and Hatch Ltd. active in this segment.

By Application Insights

Metal Mining leads the global Mine Backfill Services market by application, contributing approximately 62% of total segment revenue in 2026. This dominance reflects the high concentration of deep, technically complex, and high-value underground mining operations in the global metals sector, including gold, copper, nickel, zinc, lead, silver, and polymetallic deposits, where engineered backfill systems are essential for safe ore extraction and optimal recovery rates.

According to the World Gold Council, around 60% of global gold production comes from underground mines, including extremely deep operations in South Africa, Canada, Australia, and West Africa that rely heavily on paste fill and cemented fill systems to maintain ground stability and ensure safe production. Barrick Gold Corporation operates multiple underground gold mines across Nevada, Tanzania, the Dominican Republic, and Zambia and is among the world’s largest institutional users of engineered backfill services. The strategic use of backfill systems allows mining companies to maximize ore recovery while maintaining structural stability in deep underground environments. Coal Mining represents approximately 22% of the market, driven primarily by underground longwall coal operations in China, Australia, and the United States that use hydraulic and paste fill technologies for goaf void management and surface subsidence control.

Regional Insights

North America Mine Backfill Services Market Trends

North America is a leading regional market for Mine Backfill Services, supported by strong mining activity in Canada and the United States. Canada is considered one of the most mining-intensive economies in the world by capital investment per capita, with Natural Resources Canada reporting that the mining industry invests over CAD 14 billion annually in mineral exploration and deposit appraisal. The United States is also strengthening its mining sector through initiatives such as the Inflation Reduction Act (IRA) and the U.S. Department of Energy’s Critical Materials Strategy, which encourage domestic critical minerals production.

Canada’s underground mining sector, especially in the Ontario and Quebec gold and base metals belts, British Columbia copper operations, and the Sudbury Basin nickel complex, shows one of the highest per-mine investments in paste fill technology globally. Strict backfill regulations under Ontario’s Mining Act further drive adoption. In the U.S., Mine Safety and Health Administration (MSHA) standards require roof and void stabilization, encouraging certified backfill systems. Major mining companies Barrick Gold and Newmont operate several underground mines using advanced paste fill programs.

Europe Mine Backfill Services Market Trends

Europe has a technically advanced and commercially focused Mine Backfill Services market, driven largely by the strong underground mining industry in Scandinavia. Sweden plays a major role in this market through LKAB, which operates the Kiruna mine, recognized as the world’s largest and most technologically advanced underground iron ore mine at depths exceeding 1,365 meters. The company’s continuous underground expansion and mine deepening program has required extensive backfill systems to maintain ground stability during ore extraction.

Finland also contributes significantly through its copper, nickel, and gold mining activities in the Central Lapland Greenstone Belt. Normet Group, headquartered in Finland, is one of the leading providers of mine backfill equipment and related services across Europe. Germany’s potash and rock salt mining industry, led by K+S AG, relies on hydraulic and paste fill systems to prevent subsidence in densely populated regions. Additionally, the European Union’s Critical Raw Materials Act (CRMA) adopted in 2024 is encouraging new mining projects across Sweden, Finland, Portugal, and Spain, further increasing demand for backfill technologies.

Asia Pacific Mine Backfill Services Market Trends

Asia Pacific represents the largest and fastest-growing regional market for Mine Backfill Services worldwide, supported by strong underground mining activity in China, Australia, and emerging markets such as India. China remains the world’s largest underground mining economy, operating thousands of gold, copper, zinc, and lead mines mainly across Yunnan, Inner Mongolia, Xinjiang, and Sichuan provinces. The China Mining Association reports increasing investments in paste fill technologies as companies aim to improve ground control and meet stricter safety requirements under the country’s evolving Work Safety Law and Mine Safety Regulations.

Domestic engineering firms and companies such as CEC Mining Systems provide equipment and backfill implementation services across the Chinese mining sector. Australia also maintains advanced backfill practices in underground gold, copper, nickel, and iron ore mines, supported by strong safety regulations from state authorities. Institutions such as the Australian Centre for Geomechanics lead global research on paste fill technologies. Meanwhile, India’s underground coal and metal mining sector is gradually adopting hydraulic and paste fill systems to improve mine stability and safety.

Competitive Landscape

The global mine backfill services market is moderately consolidated, with a structured competitive landscape consisting of large engineering consultancies and specialized system implementation providers. Global consulting firms such as SRK Consulting, WSP, and Hatch Ltd. dominate high-value design and consulting services related to mine backfill feasibility, plant design, and operational strategy. Meanwhile, specialized equipment and system implementation companies including Normet Group, Metso Outotec, and FLSmidth lead the market in on-site plant construction, commissioning, and integrated engineering solutions.

Key competitive differentiators include extensive paste fill plant commissioning experience, proprietary high-pressure pumping and thickening technologies, ISO 9001-certified engineering processes, and the ability to provide fully integrated design-supply-commissioning service packages that reduce technical coordination challenges for mining clients. The market is also witnessing emerging business model innovations such as digital paste plant performance monitoring systems, integrated tailings-to-paste processing services, and sustainability-linked advisory services aligned with Global Industry Standard on Tailings Management (GISTM) compliance. BASF Construction Chemicals and Sika AG compete within the specialty chemical admixtures segment by supplying advanced additives that optimize the strength and durability of cemented paste fill systems used in underground mining operations.

Key Developments:

- In January 2025: Metso Outotec announced a strategic collaboration with Paterson & Cooke to provide integrated paste backfill plant design and equipment supply solutions. The partnership combines advanced paste rheology engineering with thickener and pumping technologies to support underground critical-minerals mining projects in Latin America and Africa.

- In September 2024: Normet Group introduced its SmartDrive® next-generation underground paste backfill distribution technology featuring automated pump control and real-time pipeline pressure monitoring. The system uses digital optimization tools to improve paste transport reliability and reduce pipeline blockage risks in deep underground mining operations.

- In March 2024: SRK Consulting expanded its paste fill and tailings management advisory services in Western Australia, adding specialized compliance consulting aligned with the Global Industry Standard on Tailings Management (GISTM). The expansion responds to rising mining industry demand for safer tailings management and engineered underground backfill solutions.

Companies Covered in Mine Backfill Services Market

- BASF Construction Chemicals

- Normet Group

- SRK Consulting

- Golder Associates

- FLSmidth

- Paterson and Cooke

- Metso Outotec

- Sika AG

- Barrick Gold Corporation

- Victaulic

- CEC Mining Systems

- Hatch Ltd.

Frequently Asked Questions

The global Mine Backfill Services market is valued at about US$ 5.1 billion in 2026 and is projected to reach US$ 8.6 billion by 2033, growing at a 7.8% CAGR, driven by underground mining expansion.

Key drivers include rising demand for critical minerals requiring deep underground mining and stricter global tailings management regulations, encouraging mining companies to adopt engineered backfill systems for improved safety and environmental compliance.

Paste Fill leads the backfill type segment with about 45% revenue share, supported by its strong ground stability performance, effective tailings reuse capability, and increasing adoption in modern underground mining operations worldwide.

Asia Pacific leads due to extensive underground mining activities in China, advanced mining technologies in Australia, and growing underground coal and metal mining developments across India and other emerging economies.

The biggest opportunity lies in expanding underground mining projects for critical minerals, along with increasing regulatory pressure for safer tailings management, encouraging greater adoption of paste fill systems and backfill engineering services.

Major players include Normet Group, Metso Outotec, FLSmidth, SRK Consulting, WSP (Golder Associates), Hatch Ltd., Paterson and Cooke, BASF Construction Chemicals, Sika AG, and CEC Mining Systems, among other mining engineering and service providers.