- Metalworking & Fabrication

- Metalworking Machine Market

Metalworking Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Metalworking Machine Market by Machine Type (Lathe, Milling, Grinding, Boring, Drilling), End-User (Automotive, Aerospace, Construction, Others), Control Type (Computer Numerical Control (CNC), Advanced Control, Conventional), and Regional Analysis for 2026-2033

Metalworking Machine Market Share and Trends Analysis

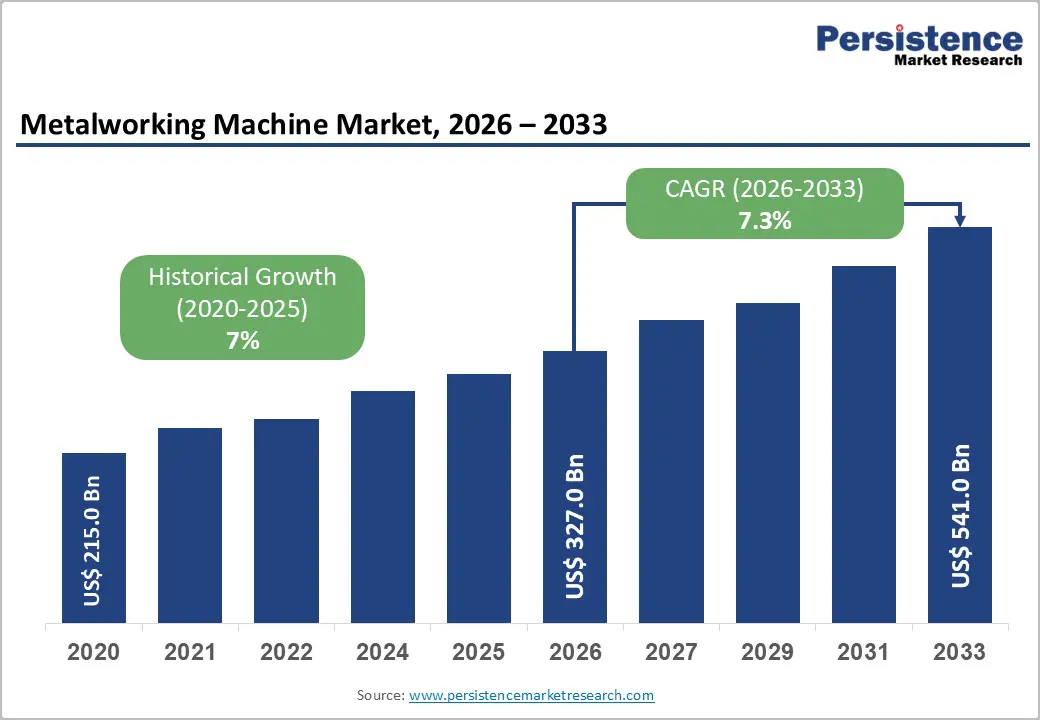

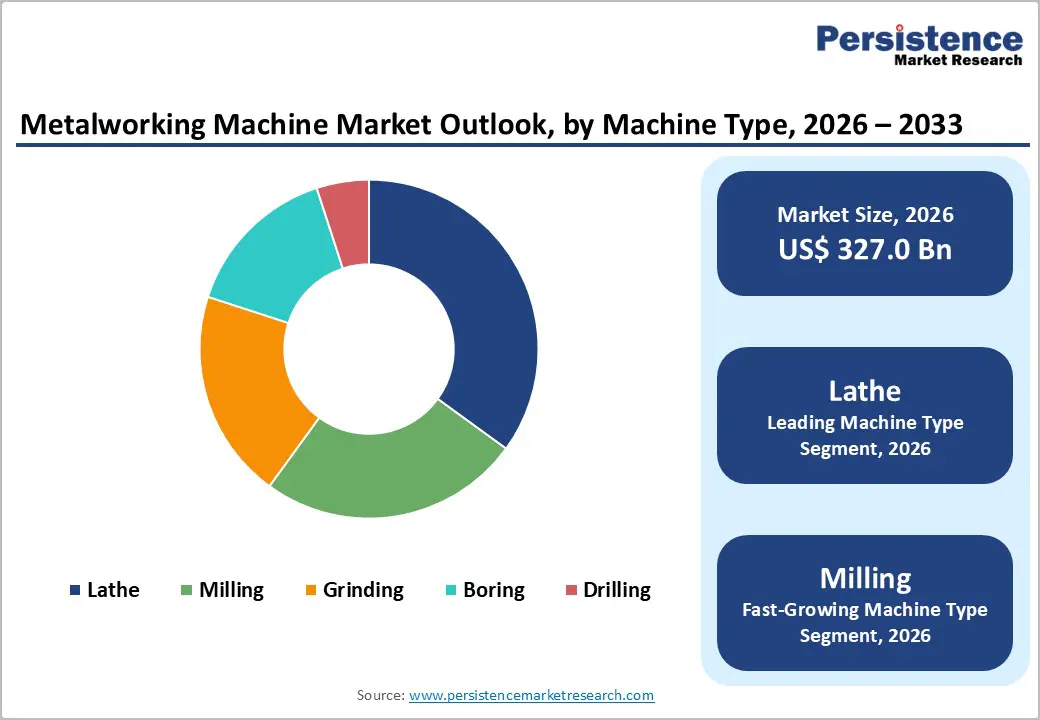

The global metalworking machine market size is likely to be valued at US$ 327.0 billion in 2026, and is projected to reach US$ 541.0 billion by 2033, growing at a CAGR of 7.3% during the forecast period 2026−2033. This growth is anchored in the essential role that metalworking equipment plays across automotive, aerospace, energy, heavy machinery, and industrial manufacturing sectors. Manufacturers are continuing to upgrade production lines to improve throughput, accuracy, and cost efficiency. Capacity expansion in electric vehicle production, aircraft component manufacturing, and industrial equipment fabrication is increasing demand for advanced machining centers, cutting tools, forming systems, and computer numerical control (CNC) platforms. Emerging economies are investing in industrial infrastructure to strengthen domestic manufacturing capabilities, which is supporting equipment replacement cycles and new installations.

Technological convergence is reshaping competitive dynamics within the sector. Traditional machining processes are integrating with Industry 4.0 frameworks, including real-time monitoring, predictive maintenance, digital twins, and automated quality inspection. These capabilities are enabling manufacturers to reduce downtime, optimize material utilization, and improve precision consistency. Smart factory initiatives are accelerating adoption of interconnected machinery that supports centralized data management and production analytics. As labor costs rise and skilled workforce availability tightens in several regions, automation is becoming a strategic necessity rather than an optional upgrade

Key geographies evaluated in this report are:

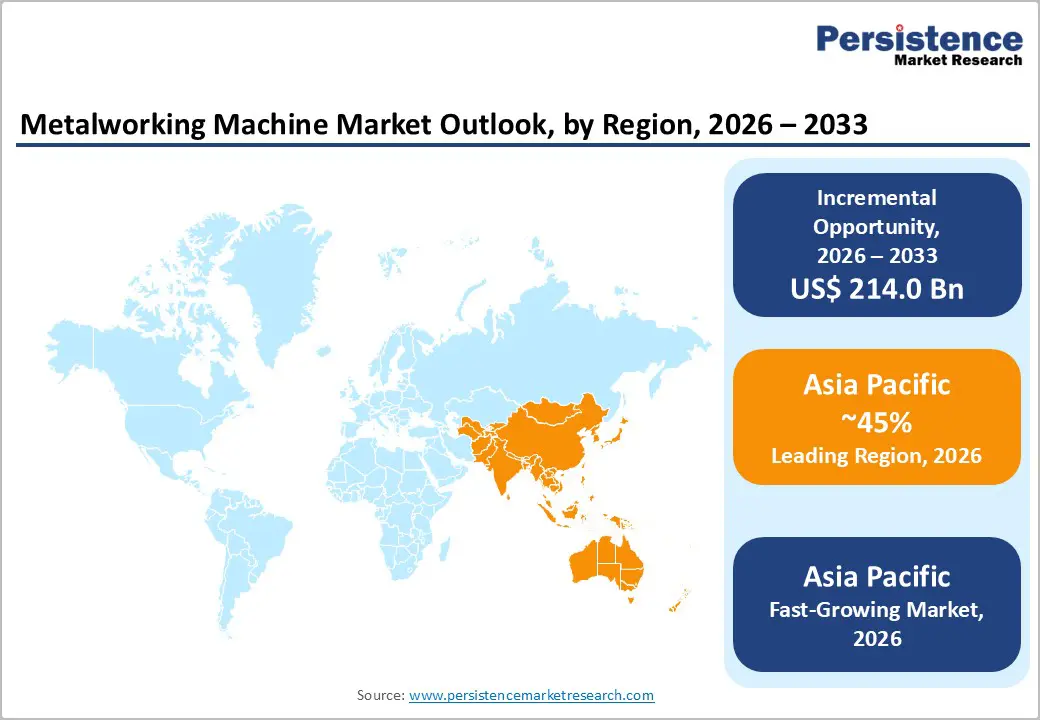

- Regional Dominance: Asia Pacific is likely to be the leading and the fastest-growing through 2033, accounting for approximately 45% of the market share in 2026, aided by massive manufacturing capacity across key sectors.

- Leading & Fastest-growing Machine Types: Lathe machines are poised to lead with around 35% revenue share in 2026, while milling machines are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Dominant End-Users: Automotive manufacturing is slated to command nearly 42% of the revenue share in 2026, with aerospace expected post the highest 2026-2033 CAGR.

- January 2026: Blaser Swisslube and Nidec Machine Tool America partnered to deliver integrated metalworking solutions that combine Blaser's high-performance "Liquid Tool" metalworking fluids with Nidec's advanced gear manufacturing and precision machining technologies.

| Key Insights | Details |

|---|---|

| Metalworking Machine Market Size (2026E) | US$ 327.0 Bn |

| Market Value Forecast (2033F) | US$ 541.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation and Smart Manufacturing Integration

Manufacturers are actively integrating Industry 4.0 technologies, which are serving as a central driver of sustained expansion in the global metalworking machine market. Production facilities are incorporating CNC systems, Internet of Things (IoT) sensors, and artificial intelligence (AI) applications focused on predictive maintenance and process optimization. These technologies are improving dimensional accuracy, repeatability, and surface finish consistency across machining cycles. Real-time monitoring is enabling operators to detect tool wear, vibration anomalies, and thermal deviations before defects occur. As a result, scrap rates are declining and equipment uptime is improving. Organizations that are prioritizing digital transformation are strengthening operational resilience and differentiating themselves through higher productivity and tighter quality control. This transition is becoming a strategic imperative as global customers demand shorter lead times and higher precision standards.

Cloud computing infrastructure and advanced data analytics are further enhancing production performance by linking machinery to enterprise resource planning and global supply chain systems. Real-time data flows are supporting dynamic scheduling, automated inspection routines, and continuous calibration of machining parameters. Integrated platforms are also supporting synchronized inventory management and reducing raw material waste. Engineers are accessing detailed performance metrics that inform process refinement and equipment upgrades. By leveraging connected manufacturing ecosystems, companies are building adaptive production networks that can withstand supply chain disruptions and market volatility while maintaining cost discipline and delivery reliability.

High Capital Investment and Operating Costs

Manufacturers are confronting significant capital requirements when investing in advanced metalworking machinery, particularly high-precision systems such as five-axis CNC machining centers. These assets require substantial upfront expenditure, which is placing financial pressure on small and medium-sized enterprises (SMEs) operating with constrained budgets. Leadership teams are carefully evaluating expected returns on investment, especially in environments where demand cycles fluctuate. Access to financing remains uneven across regions, which further limits adoption among smaller firms. Procurement managers are increasingly considering structured financing solutions such as equipment leasing, installment-based purchasing agreements, and vendor-supported credit programs to preserve liquidity. Spreading capital outlays over defined periods is helping firms stabilize cash flow while upgrading production capabilities.

Operating expenses are adding another layer of complexity. Companies must allocate resources for skilled workforce training, acquisition of precision tooling, preventive maintenance programs, and recurring software licensing fees tied to digital manufacturing platforms. Energy consumption is also becoming a critical variable as electricity costs rise and sustainability targets tighten. Retrofitting existing machinery with automation modules or digital sensors is offering a lower-risk pathway for incremental modernization. Strategic capital planning that integrates vendor support services and staged upgrades is enabling manufacturers to enhance productivity while managing long payback periods and uncertain market conditions.

Sustainable Manufacturing and Energy-Efficient Equipment

Stricter environmental standards and rising corporate sustainability commitments are reshaping capital allocation decisions in the metalworking machine market. Regulatory frameworks such as the European Union’s Carbon Border Adjustment Mechanism (CBAM) are increasing scrutiny on carbon intensity across manufacturing supply chains. As a result, producers are prioritizing equipment that consumes less energy, reduces coolant usage, and minimizes raw material waste. Machines equipped with regenerative braking systems, high-efficiency spindle motors, and intelligent power management controls are improving energy performance across production lines. Manufacturers that align early with evolving environmental benchmarks are strengthening their competitiveness in export-oriented and compliance-sensitive markets.

Process innovation is reinforcing this transition. Dry machining methods and minimum quantity lubrication techniques are lowering reliance on cutting fluids, which reduces disposal costs and environmental liabilities. Equipment designed with circular economy principles is gaining traction, including modular components, extended maintenance intervals, and remanufacturing compatibility. These features are extending asset life and lowering total cost of ownership. Companies are conducting supply chain audits to assess carbon exposure and regulatory readiness, particularly in high-volume production segments. Pilot programs that test energy-efficient technologies in core facilities are delivering measurable savings while enhancing compliance confidence. Integrating sustainability certifications and environmental performance standards into supplier evaluation frameworks is helping organizations build resilient operations that meet regulatory demands and appeal to environmentally conscious global clients.

Category-wise Analysis

Machine Type Insights

Lathe machines are expected to dominate among product types, commanding approximately 35% of the metalworking machine market revenue share in 2026, due to their exceptional versatility in processing cylindrical components such as shafts, automotive crankshafts, and aerospace structural fittings. These machines master turning operations that shape materials through rotational symmetry, forming the essential foundation of precision manufacturing workflows across diverse sectors, including automotive production lines and aircraft assembly. Their adaptability to both high-volume runs and custom prototypes ensures broad applicability, while compatibility with advanced tooling broadens their utility further. This consistent performance across applications secures lathe machines the largest revenue share among specified types, making them indispensable for manufacturers pursuing operational efficiency and part quality.

Milling machines are likely to be the fastest-growing segment during the 2026-2033 forecast period, propelled by escalating requirements for intricate geometries essential to electric vehicle (EV) components such as battery housings and transmission gears, alongside expanding multi-axis applications in modern fabrication. Their inherent flexibility shines through seamless integration with sophisticated Computer Numerical Control (CNC) systems, enabling precise contouring and sculpting of challenging materials that traditional setups struggle to achieve. This adaptability perfectly matches surging customization demands from sectors such as renewable energy and medical devices, where bespoke designs dominate production pipelines.

End-User Insights

Automotive manufacturing is poised to represent the leading application area, capturing around 42% of the metalworking machine market share in 2026. This sector's substantial equipment requirements span engine component manufacturing, transmission systems, body-in-white production, and electric vehicle powertrain components. The industry's ongoing transition to electric mobility drives replacement cycles as manufacturers retool facilities, invest in aluminum and advanced high-strength steel processing capabilities, and establish battery pack production lines requiring specialized metalworking equipment for enclosure manufacturing and thermal management components.

Aerospace is expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by commercial aircraft production recovery following pandemic disruptions, defense modernization programs, and space exploration initiatives. This sector demands ultra-precision metalworking capabilities for turbine engine components, structural airframe elements, and landing gear systems manufactured from difficult-to-machine materials, including titanium alloys and nickel-based super alloys. The stringent quality requirements, complex geometries, and high material costs in aerospace applications justify premium metalworking equipment investments. The emerging commercial space sector is creating new demand avenues for specialized machining capabilities to produce rocket engine components, satellite structures, and precision mechanisms operating in extreme environments.

Control Type Insights

The CNC segment is anticipated to command an approximate 55% revenue share in 2026, owing to its unmatched precision and robust automation features. These capabilities perfectly address the rigorous requirements of automotive production lines and aerospace component fabrication, where tight tolerances prove essential. Manufacturers favor CNC machines for their ability to execute complex operations with minimal human intervention, ensuring consistent output quality across diverse applications. Seamless integration with Industry 4.0 technologies, such as real-time monitoring and adaptive controls, amplifies their dominance by enabling smarter workflows and faster cycle times.

Advanced control is projected to be the fastest-growing segment during the 2026-2033 forecast period, powered by artificial intelligence (AI) enhancements and sophisticated multi-axis configurations. Manufacturers actively upgrade to these solutions to enable predictive maintenance features and real-time process optimization, which transform traditional operations into intelligent, responsive ecosystems. Production teams gain proactive insights that anticipate equipment issues before they disrupt workflows, ensuring smoother continuity across high-volume runs. Engineers value the precision these systems deliver in complex part geometries, particularly for sectors demanding flawless execution, such as aerospace assemblies and electric vehicle powertrains.

Regional Insights

Asia Pacific Metalworking Machine Market Trends

Asia Pacific market is likely to be both the leading and fastest-growing regional market for metalworking machines in 2026, accounting for approximately 45% of the metalworking machine market value, with China setting the pace through its vast manufacturing base that spans automotive assembly, electronics production, and industrial equipment fabrication. Japan contributes significantly with its focus on high-value precision tools tailored for robotics, vehicles, and consumer devices, while India accelerates growth via government-backed programs such as Production-Linked Incentive (PLI) schemes that boost local automotive output and defense capabilities. South Korea thrives in electronics and shipbuilding, and ASEAN countries such as Vietnam, Thailand, and Indonesia attract investments through diversified production shifts and foreign capital inflows.

Manufacturers in the Asia Pacific capitalize on key drivers such as ongoing industrialization, infrastructure projects, expanding electronics ecosystems, and rising electric vehicle production, all supported by policies that promote cutting-edge capabilities. Regulatory frameworks tighten safety and environmental standards in mature economies while offering flexibility in emerging ones, creating balanced pathways for compliance. Local players such as Dalian Machine Tool Group and Qinchuan Machine Tool challenge global giants, including Mazak, Okuma, and DMG Mori, especially in premium categories. Consultants advise prioritizing automation upgrades to counter labor cost pressures, forging joint ventures for technology transfers, and targeting opportunities in electric vehicle supply chains, miniaturized electronics gear, and import substitution efforts. Strategic investments here position firms to harness sustained expansion while navigating competitive dynamics effectively.

Europe Metalworking Machine Market Trends

Europe secures a prominent position in the global market for metalworking machines, with Germany leading through its renowned machine tool sector, robust automotive production featuring premium brands, and sophisticated industrial equipment manufacturing. The United Kingdom excels in aerospace fabrication and precision engineering projects, while France advances via demands from aerospace assembly, vehicle components, and nuclear power installations. Spain gains traction with automotive parts production and renewable energy gear, such as wind turbine assemblies. Manufacturers leverage these strengths to serve high-specification clients across the region, benefitting from established engineering talent and innovation hubs that drive consistent output.

Industry 4.0 adoption propels growth alongside strict emissions rules that spur powertrain advancements and renewable infrastructure needs for precisely crafted turbine and hydroelectric parts. Unified regulations through European Union (EU) machinery directives, CE marking protocols, and energy efficiency mandates shape equipment designs, while environmental standards such as Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) influence fluid choices. Domestic leaders, including DMG Mori, Trumpf, and GF Machining Solutions, compete effectively against Japanese entrants in key segments. Consultants recommend investments in green technologies, digital integration, and EV tooling to capture expansion in Central and Eastern Europe, aerospace networks, and medical device hubs.

North America Metalworking Machine Market Trends

North America claims a vital share of the market for metalworking machines globally, led by the United States with its powerhouse aerospace fabrication hubs, refreshed automotive assembly lines, and forward-leaning advanced manufacturing programs. Canada complements this strength through energy sector equipment needs and precision tooling for transportation projects. Manufacturers draw on deep engineering expertise and supply chain maturity to meet demanding specifications across these areas. Leaders who engage this region tap into a stable base for high-value production that supports broader North American economic priorities.

Reshoring efforts gain momentum from policies such as the Creating Helpful Incentives to Produce Semiconductors (CHIPS) Act and the Infrastructure Investment and Jobs Act, which spur domestic capacity alongside automation drives that offset skilled worker gaps and defense upgrades requiring exacting metal components. Regulators enforce Occupational Safety and Health Administration (OSHA) safety protocols and Environmental Protection Agency (EPA) rules on fluids and emissions, pushing designs toward sealed units with built-in filtration and reuse systems. Global contenders, including DMG Mori, Haas Automation, and Mazak, vie with niche suppliers for aerospace and medical markets.

Competitive Landscape

The global metalworking machine market structure remains moderately fragmented, with leading manufacturers collectively accounting for approximately 38% of total revenue. Competitive positioning is shaped by technological capability rather than sheer scale alone. Major producers differentiate through advanced engineering features such as artificial intelligence driven control systems, multi-axis machining platforms, and high-speed precision tooling solutions. These capabilities attract clients in aerospace, electric vehicle manufacturing, medical device fabrication, and high-performance automotive components. Application-specific expertise is also influencing purchasing decisions. Suppliers that demonstrate deep process knowledge in areas such as powertrain machining or orthopedic implant production are strengthening customer relationships by delivering tailored production solutions rather than standardized equipment.

After-sales infrastructure is serving as a critical competitive lever. Strong global service networks are providing rapid technical support, operator training, and preventive maintenance programs that reduce downtime and safeguard productivity. Customers are valuing uptime guarantees and remote diagnostics, particularly in high-volume manufacturing environments where production interruptions carry significant financial impact. Pricing strategies are balancing premium performance with accessible financing structures, enabling small and medium-sized enterprises to invest in advanced systems without excessive capital strain. Structured leasing, staged payment plans, and long-term service agreements are reinforcing durable partnerships.

Key Industry Developments

- In November 2025, NestWorks launched a consumer-grade desktop CNC machine on Kickstarter, positioning it as the first compact system designed for serious metal machining outside traditional industrial environments and targeting makers, small shops, and prototyping applications

- In October 2025, METALEX 2025 highlighted next-generation metalworking technologies that are enabling ASEAN manufacturers to transition toward smart manufacturing, emphasizing automation, digital integration, and advanced machining solutions for regional industrial growth.

- In August 2025, DN Solutions completed its acquisition of German precision engineering specialist HELLER, creating a powerhouse with DN Solutions' global scale and digital platforms with HELLER's expertise in high-end machining centers.

Companies Covered in Metalworking Machine Market

- DMG Mori Seiki Co., Ltd.

- Trumpf GmbH Co. KG

- Yamazaki Mazak Corporation

- Okuma Corporation

- Haas Automation, Inc.

- GF Machining Solutions

- Makino Milling Machine Co., Ltd.

- Doosan Machine Tools Co., Ltd.

- Dalian Machine Tool Group Corporation

- JTEKT Corporation

- INDEX-Werke GmbH & Co. KG

- Hurco Companies, Inc.

- Komatsu NTC Ltd.

- Hyundai WIA Corp.

- Shenyang Machine Tool Co., Ltd.

Frequently Asked Questions

The global metalworking machine market is projected to reach US$ 327.0 billion in 2026.

Rising Industry 4.0 adoption, automotive/aerospace demand, and infrastructure expansion are driving the market.

The market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Major opportunities are emerging in developing Asia Pacific markets, sustainability-focused technologies, and reshoring initiatives.

DMG Mori Seiki Co., Ltd., Yamazaki Mazak Corporation, Okuma Corporation, Haas Automation, Inc., and GF Machining Solutions are some of the key players in the market.