- Industrial Goods & Service

- Lubricants Oil Drum Market

Lubricants Oil Drum Market Size, Share, and Growth Forecast, 2026 - 2033

Lubricants Oil Drum Market by Product Type (Steel Drums, Plastic Drums, Other), Capacity (100-250 liters, Below 100 liters, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Lubricants Oil Drum Market Size and Trends Analysis

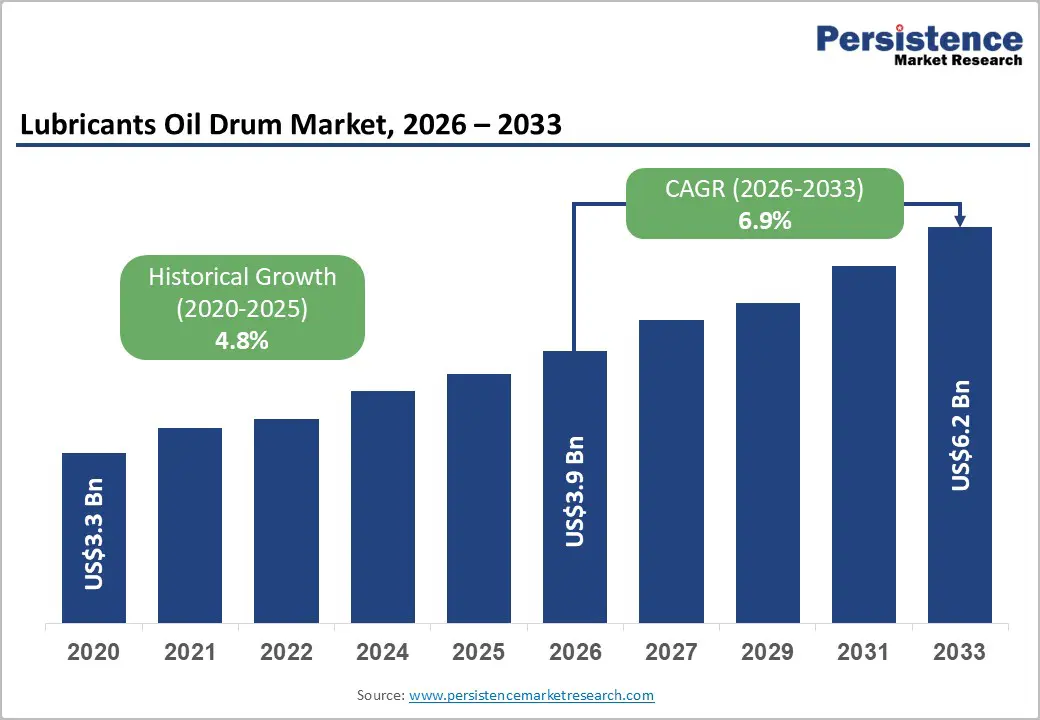

The global lubricants oil drum market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$6.2 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by recurring lubricant consumption across automotive and industrial sectors, increasing demand for recyclable industrial packaging, and the rising adoption of reconditioning and closed-loop drum systems. Steel drums continue to dominate due to durability and recyclability, while plastic drums are gaining traction as sustainability regulations encourage the use of recycled materials.

Key Industry Highlights:

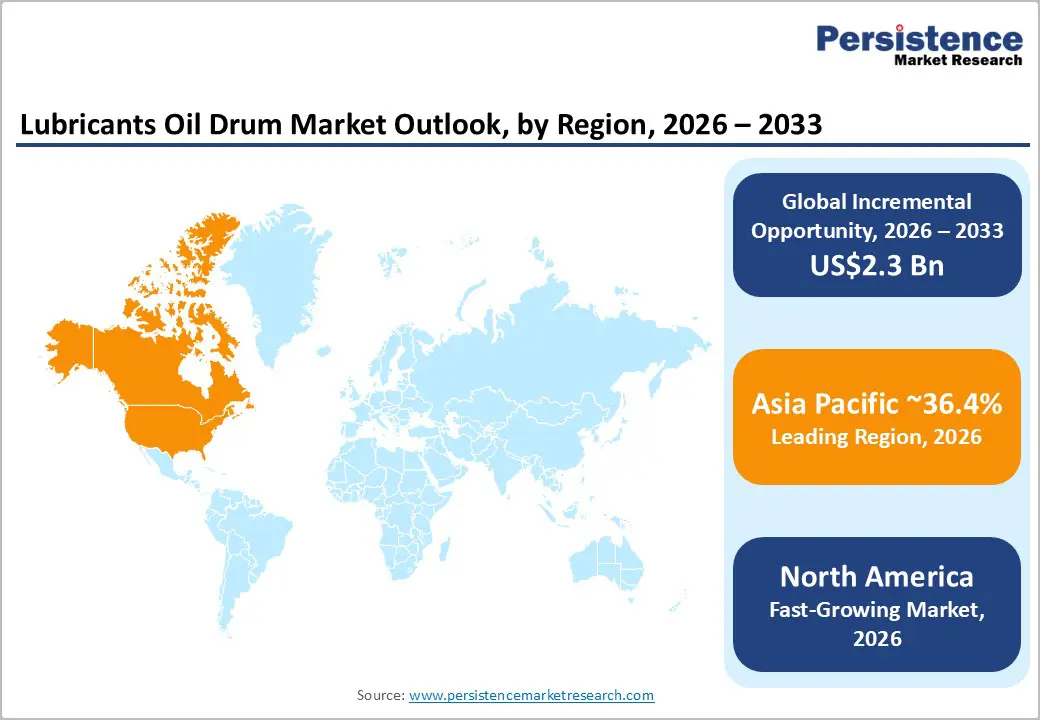

- Leading Region: Asia Pacific is projected to account for 36.4% of the market share, supported by strong manufacturing activity, expanding automotive production, and high lubricant consumption across China, India, Japan, and ASEAN economies.

- Fastest-growing Region: North America is the fastest-growing region, driven by advanced reconditioning infrastructure, industrial reshoring, and increasing adoption of sustainable packaging solutions, particularly in the automotive and chemical industries.

- Investment Plans: Industry investments are increasingly focused on low-carbon steel drums, PCR-based plastic drums, and expansion of reconditioning and recycling facilities, with companies strengthening closed-loop systems and regional production capabilities to improve lifecycle efficiency.

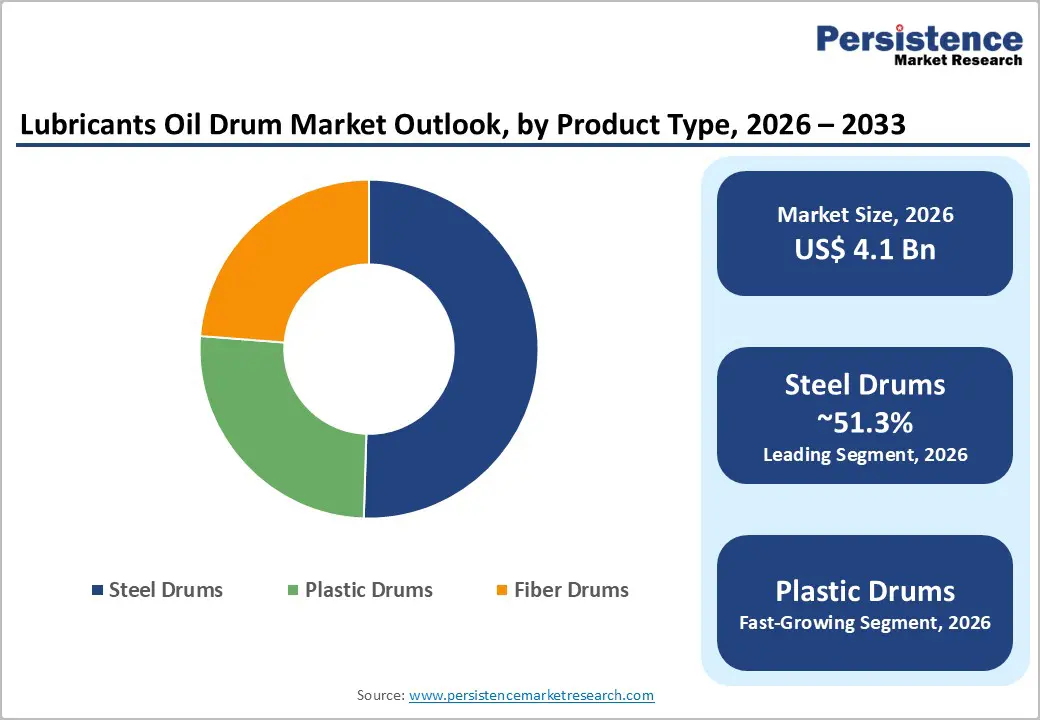

- Dominant Product Type: Steel drums are anticipated to dominate, holding approximately 51.3% market share, due to their durability, reusability, and compliance with industrial safety and transport standards.

- Leading Capacity: The 100-250 liters is anticipated to lead with around 40.8% share, as it aligns with standard industrial requirements for lubricant storage, transportation, and handling efficiency.

| Key Insights | Details |

|---|---|

| Lubricants Oil Drum Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$6.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

DRO Analysis

Driver Analysis - Recurring Demand from Automotive, Industrial, and Maintenance Ecosystems

Lubricants function as consumables, which ensures that packaging demand remains cyclical and replenishment-driven. Growth in global vehicle production, fleet expansion, and industrial output continues to sustain lubricant usage across multiple sectors. Automotive servicing, heavy machinery maintenance, and manufacturing operations require a consistent lubricant supply, leading to stable drum demand. The aerospace sector further contributes through maintenance-intensive operations that rely on high-performance lubricants. This recurring consumption pattern creates a predictable demand cycle for oil drums, reducing volatility and supporting long-term market stability.

Circular Economy Regulations Driving Reusable and Recyclable Drum Adoption

Regulatory frameworks focused on reducing packaging waste are significantly influencing procurement strategies. Policies aimed at improving recyclability, reuse, and material efficiency are encouraging end users to adopt steel drums and recycled plastic alternatives. Companies are increasingly prioritizing closed-loop systems, reconditioning, and recycled content in packaging procurement. This shift is moving purchasing decisions away from upfront cost considerations toward total lifecycle performance, including reuse potential and environmental impact. As a result, manufacturers offering circular solutions are gaining a competitive advantage in long-term contracts.

Expansion of Industrial Packaging Reconditioning and Lifecycle Services

Reconditioning services are transforming the economics of industrial packaging. Steel and plastic drums can be cleaned, tested, and reused multiple times, reducing disposal costs and extending product life cycles. This is particularly beneficial in lubricant distribution, where packaging reuse aligns with operational efficiency and sustainability goals. Service-based models, including drum collection, refurbishment, and redistribution, are becoming increasingly common. This evolution is shifting the market from a product-centric approach to a service-driven ecosystem, enhancing customer retention and reducing overall packaging costs for end users.

Restraint Analysis - Raw Material Price Volatility Impacting Cost Structures

The market remains highly sensitive to fluctuations in steel and polymer prices, which directly influence production costs. Steel drums depend on sheet metal pricing, while plastic drums rely on resin availability and recycled material supply. Price instability can compress margins and delay the adoption of sustainable materials when cost differentials widen. For price-sensitive customers, this may lead to a preference for lower-cost alternatives, limiting premium product penetration. Manufacturers must balance cost efficiency with innovation to remain competitive under fluctuating input conditions.

Regulatory Compliance and Reverse Logistics Complexity

Lubricant drums are subject to stringent regulations related to hazardous material handling, transportation safety, and environmental compliance. Requirements such as UN certifications, leak-proof designs, and proper cleaning protocols increase operational complexity. Reverse logistics, including collection and reconditioning, adds further challenges, especially in regions with underdeveloped infrastructure. These factors raise operational costs and create barriers for smaller market participants, potentially slowing adoption in less mature markets.

Opportunity Analysis - Premiumization through Low-Carbon and Recycled-Content Packaging

Sustainable packaging solutions present a significant opportunity for differentiation and margin expansion. Manufacturers are increasingly introducing low-carbon steel drums and PCR-based plastic drums to meet evolving environmental targets set by large industrial buyers. Many multinational lubricant companies are aligning procurement with Scope 3 emission reduction goals, making packaging a measurable component of sustainability reporting. This shift is enabling suppliers to position advanced drum solutions as value-added products rather than commodity packaging. Innovation is extending beyond materials to include lightweighting, improved coatings, and enhanced recyclability, which further improve lifecycle performance. Companies that can demonstrate verified carbon reduction and circularity benefits are more likely to secure long-term supply agreements and premium pricing, especially with global automotive and chemical manufacturers.

Regional Manufacturing Expansion and Supply Chain Localization

Asia Pacific’s dominance, with a 36.4% market share, underscores the importance of localized production and regional supply chain integration. Rapid industrialization, expanding automotive fleets, and strong manufacturing activity continue to drive lubricant demand, creating parallel growth in drum consumption. Local manufacturers benefit from reduced transportation costs, shorter delivery timelines, and better alignment with regional regulatory requirements. Supply chain disruptions in recent years have accelerated the shift toward nearshoring and regional manufacturing hubs, particularly in emerging economies such as India and Southeast Asia. This trend is encouraging both global and regional players to expand production capacity closer to end users. As a result, companies with multi-location manufacturing networks and strong regional distribution capabilities are better positioned to capture market share and respond to demand fluctuations efficiently.

Integration of Digital Tracking and Service-Based Business Models

Digitalization is creating new opportunities to transform traditional drum supply into integrated packaging management solutions. Technologies such as RFID tagging, barcode tracking, and IoT-enabled monitoring systems are improving visibility across the drum lifecycle, from filling and transport to collection and reconditioning. This enhanced traceability is particularly valuable for lubricant manufacturers handling large volumes across multiple distribution points. When combined with service offerings such as collection, cleaning, refurbishment, and redeployment, digital tracking enables a shift toward end-to-end service-based models. These solutions help customers reduce operational inefficiencies, improve inventory control, and ensure regulatory compliance. For suppliers, this approach creates recurring revenue streams, stronger customer relationships, and higher switching costs, positioning them as strategic partners rather than commodity vendors.

Category-wise Analysis

Product Type Insights

Steel drums are anticipated to dominate the market, accounting for approximately 51.3% of market share in 2026, driven by their high structural strength, durability, and reusability across multiple industrial cycles. These drums are extensively used in lubricant storage and transportation, particularly in automotive, petrochemical, and heavy manufacturing sectors, where resistance to leakage, impact, and extreme environmental conditions is critical. For instance, large lubricant distributors and oil companies commonly use 200-liter steel drums for bulk engine oil and industrial lubricants due to their compatibility with long-distance transport and stacking efficiency. Steel drums are also highly suitable for reconditioning and reuse programs, making them integral to circular packaging systems. Their compliance with UN safety standards and hazardous material regulations further strengthens their leadership in industrial applications.

Plastic drums are projected to be the fastest-growing segment, supported by rising demand for lightweight, corrosion-resistant, and environmentally sustainable packaging solutions. The increasing adoption of recycled high-density polyethylene (rHDPE) and post-consumer resin (PCR) is aligning plastic drums with global sustainability goals. These drums are widely used in specialty lubricant segments, such as synthetic oils and high-performance fluids, where contamination resistance and chemical stability are essential. For example, lubricant suppliers catering to precision machinery and export markets prefer plastic drums due to their lower weight and reduced transportation costs. Their ease of handling also makes them suitable for decentralized distribution networks. Fiber drums continue to serve niche applications, particularly in dry or semi-solid lubricants, but remain limited in heavy-duty liquid lubricant transport due to lower durability and moisture resistance.

Capacity Insights

The 100-250 liters segment is anticipated to lead the market with a 40.8% share in 2026, as it aligns closely with standard industrial packaging and logistics requirements. This capacity range is widely adopted across automotive workshops, industrial plants, and chemical processing units, where bulk lubricant handling is routine. The 200-210 liter drum format has become an industry benchmark, allowing compatibility with drum pumps, palletization systems, and global transport standards. For example, automotive service chains and fleet maintenance operators rely heavily on this size for efficient storage and dispensing of engine oils and greases. Its balance between volume efficiency and manageable handling makes it the most commercially viable and widely accepted segment.

The below 100 liters segment is expected to be the fastest-growing, driven by increasing demand from small and medium enterprises (SMEs), service centers, and specialized lubricant applications. These smaller drums are easier to transport, store, and handle manually, making them ideal for workshops with limited space or lower consumption volumes. For instance, regional distributors and maintenance service providers often use 50-liter or 80-liter drums for diversified lubricant portfolios and faster inventory turnover. This segment is also gaining traction in export markets where flexibility and reduced packaging weight are critical. The 251-500 liters segment caters to mid-scale industrial operations, including manufacturing units and large maintenance facilities that require higher-volume storage without transitioning to bulk tanks. Meanwhile, drums with a capacity of above 500 liters are used in specialized bulk applications such as large-scale industrial lubrication systems and oil storage, though adoption remains comparatively limited due to handling complexity and infrastructure requirements.

Regional Insights

North America Lubricants Oil Drum Market Trends - Service-Driven, Low-Carbon Drum Ecosystem Expansion

North America is emerging as the fastest-growing region, supported by industrial reshoring, strong maintenance demand, and a mature reconditioning ecosystem. The region benefits from a highly developed network of drum manufacturers and service providers such as Greif, Inc., Mauser Packaging Solutions, and North Coast Container, which collectively offer integrated services including new drum supply, collection, cleaning, and refurbishment. This service-based ecosystem improves operational efficiency for lubricant distributors and industrial users by reducing packaging waste and lowering lifecycle costs.

Recent developments highlight the region’s shift toward sustainability and value-added services. For instance, Greif, Inc. introduced low-carbon steel drums in 2025, leveraging reduced-emission steel inputs to align with customer sustainability targets. Similarly, Mauser Packaging Solutions expanded its reconditioning and recycling infrastructure, strengthening closed-loop packaging systems across North America. These initiatives directly support industries such as automotive, chemicals, and industrial manufacturing, where compliance and sustainability reporting are becoming critical procurement criteria. Regulatory frameworks in the U.S. and Canada emphasize environmental compliance, hazardous material handling, and waste reduction, encouraging wider adoption of reusable and recyclable drums. The presence of specialized reconditioning firms such as Orlando Drum & Container further strengthens reverse logistics capabilities. As a result, North America is transitioning toward a service-driven packaging model, where innovation in materials is complemented by lifecycle management, supporting its accelerated growth trajectory.

Europe Lubricants Oil Drum Market Trends - Regulation-Led Circular Packaging & Traceability Shift

Europe’s lubricants oil drum market is strongly influenced by stringent regulatory frameworks and circular economy mandates, which are reshaping packaging design and procurement strategies. Policies focused on reducing packaging waste and improving recyclability are accelerating the adoption of reusable steel drums and recycled plastic alternatives. Countries such as Germany, the U.K., France, and Spain play a central role due to their strong industrial bases, automotive sectors, and regulatory enforcement.

Leading companies such as SCHÜTZ GmbH & Co. KGaA and Mauser Packaging Solutions are actively investing in closed-loop packaging systems and recycling infrastructure across the region. A notable development includes Mauser’s 2025 expansion of its reconditioning and recycling facility in Spain, which enhances its ability to collect, clean, and reuse industrial drums within regional supply chains. Similarly, SCHÜTZ has expanded its Ticket Service model, enabling efficient return and reconditioning of drums across multiple European markets. These developments are driving a shift toward lifecycle-based procurement, where buyers evaluate not only product performance but also traceability, recyclability, and carbon footprint. The regulatory push is also encouraging innovation in low-carbon steel drums and PCR-based plastics, positioning Europe as a global leader in sustainable industrial packaging. As a result, the competitive landscape is increasingly defined by companies that can deliver compliant, traceable, and circular packaging solutions.

Asia Pacific Lubricants Oil Drum Market Trends - High-Volume Manufacturing & Cost-Efficient Supply Dominance

Asia Pacific is expected to lead the lubricants oil drum market with a 36.4% market share in 2026, driven by rapid industrialization, expanding automotive production, and large-scale manufacturing activity. Key contributors include China, India, Japan, and ASEAN economies, where strong demand for lubricants across automotive, chemicals, and heavy industries sustains high drum consumption.

The region’s competitive advantage lies in its cost-efficient manufacturing base, extensive production capacity, and proximity to end-use industries. Companies such as Time Technoplast Ltd. and Balmer Lawrie & Co. Ltd. have established strong regional footprints, offering a wide range of steel and plastic drums tailored to lubricant and chemical applications. For example, Balmer Lawrie continues to maintain a leading position in India’s steel drum segment, supplying large volumes to oil marketing companies and industrial lubricant distributors. Recent developments further highlight regional growth momentum. Time Technoplast Ltd. has expanded its industrial packaging capacity across Southeast Asia and the Middle East, strengthening supply chain reach for multinational lubricant companies. Meanwhile, Indian manufacturers such as Sicagen India Ltd. continue to scale production of 210-liter MS drums, which are widely used for lubricant oil transport and storage.

Demand is also supported by infrastructure development, power generation projects, and increasing chemical production across the region. Investment is increasingly directed toward recycled plastic drums, coated steel drums, and localized reconditioning facilities, which improve sustainability performance and reduce logistics costs. As regulatory frameworks gradually tighten, particularly in India and China, the market is expected to transition toward higher-quality, compliant, and environmentally sustainable packaging solutions, reinforcing Asia Pacific’s leadership position.

Competitive Landscape

The global lubricants oil drum market is fragmented at a global level but regionally concentrated. Leading multinational players compete alongside strong regional manufacturers. Global companies focus on innovation, sustainability, and service integration, while regional players leverage localized production and cost advantages. Competitive differentiation is increasingly based on lifecycle services, regulatory compliance, and material innovation rather than price alone.

Key players are focusing on circular economy integration, product innovation, and service-based models. Strategies include expanding reconditioning networks, developing sustainable materials, and strengthening regional production. Companies that combine cost efficiency with lifecycle value and regulatory compliance are best positioned to capture long-term market share.

Key Industry Developments:

- In 2025, Greif, Inc. announced strategic portfolio optimization actions, including restructuring operations and reallocating capital to higher-growth packaging segments such as industrial containers and drums, aiming to improve profitability and expand in resilient end-use markets.

Companies Covered in Lubricants Oil Drum Market

- Greif, Inc.

- Mauser Packaging Solutions

- SCHÜTZ GmbH & Co. KGaA

- Balmer Lawrie & Co. Ltd.

- Time Technoplast Ltd.

- Sicagen India Ltd.

- North Coast Container

- Myers Container LLC

- Orlando Drum & Container

- Chambers Drum Company

- CL Smith Company

- The Cary Company

- Schütz VASITEX

- Balmer Lawrie (UAE) LLC

- Great Western Containers Inc.

- Jakacki Bag & Barrel, Inc.

Frequently Asked Questions

The lubricants oil drum market is estimated to be valued at US$ 3.9 billion in 2026.

The lubricants oil drum market is projected to reach US$ 6.2 billion by 2033.

Key trends include the increasing adoption of recyclable and reusable drums, growing use of PCR-based plastic materials, expansion of reconditioning and closed-loop systems, and rising demand for low-carbon industrial packaging solutions.

The steel drums segment is the leading product type, accounting for approximately 51.3% of the market share, due to its durability, safety compliance, and reusability.

The lubricants oil drum market is expected to grow at a CAGR of 6.9% between 2026 and 2033.

Some of the major players include Greif, Inc., Mauser Packaging Solutions, SCHÜTZ GmbH & Co. KGaA, Balmer Lawrie & Co. Ltd., and Time Technoplast Ltd.