- Pharmaceuticals

- Liposarcoma Treatment Market

Liposarcoma Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Liposarcoma Treatment Market by Treatment Type (Chemotherapy, Radiation Therapy, Surgical Therapy), Drug Type (Soft Tissue Sarcoma Drugs, Chemo Drugs, Others), End-user (Multispecialty Clinics, Others), and Regional Analysis 2026 - 2033

Liposarcoma Treatment Market Size and Trends Analysis

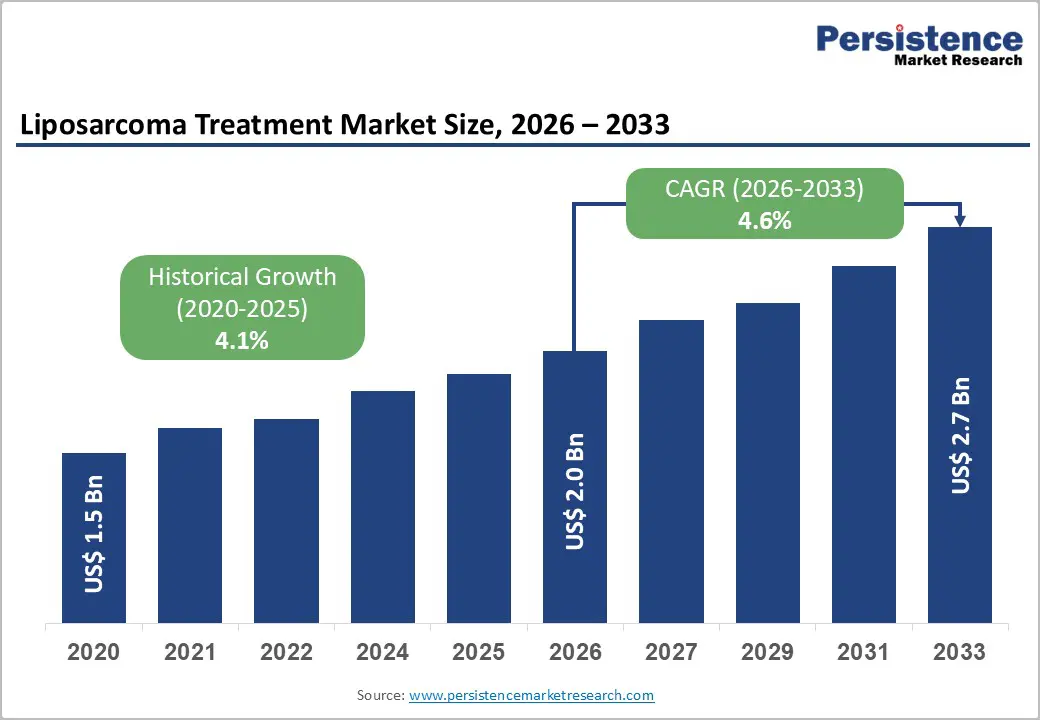

The global liposarcoma treatment market size is likely to be valued at US$2.0 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by the rising incidence of soft tissue sarcomas, which drives the procurement of advanced therapeutic options across oncology networks.

Precision medicine integration accelerates the adoption of targeted interventions that minimize side effects. Healthcare providers prioritize targeted agents to improve clinical outcomes for diverse patient populations. This clinical shift reinforces consistent procurement of advanced pharmacologic and surgical solutions. Ongoing research initiatives further strengthen the market trajectory toward precision oncology models.

Key Industry Highlights:

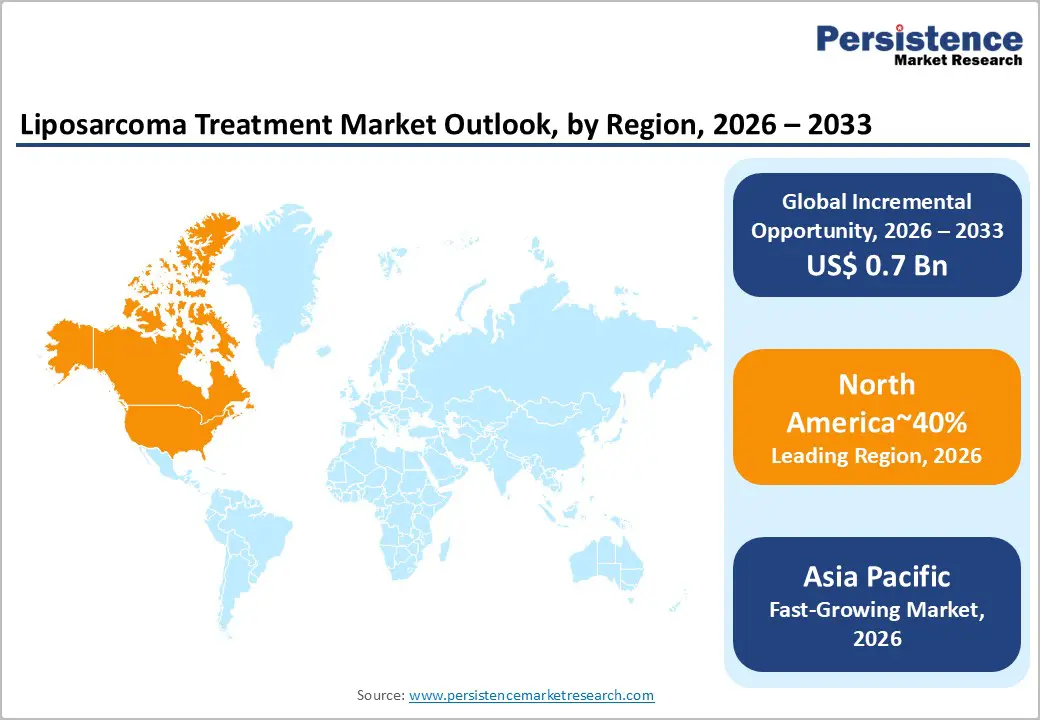

- Leading Region: North America is projected to lead, accounting for approximately 40% share in 2026, supported by high healthcare spending, established research infrastructure, and early adoption of novel targeted therapies.

- Fastest Growing Region: Asia Pacific is anticipated to grow fastest, driven by expanding hospital networks, rising medical awareness, and increased investment in oncology care infrastructure.

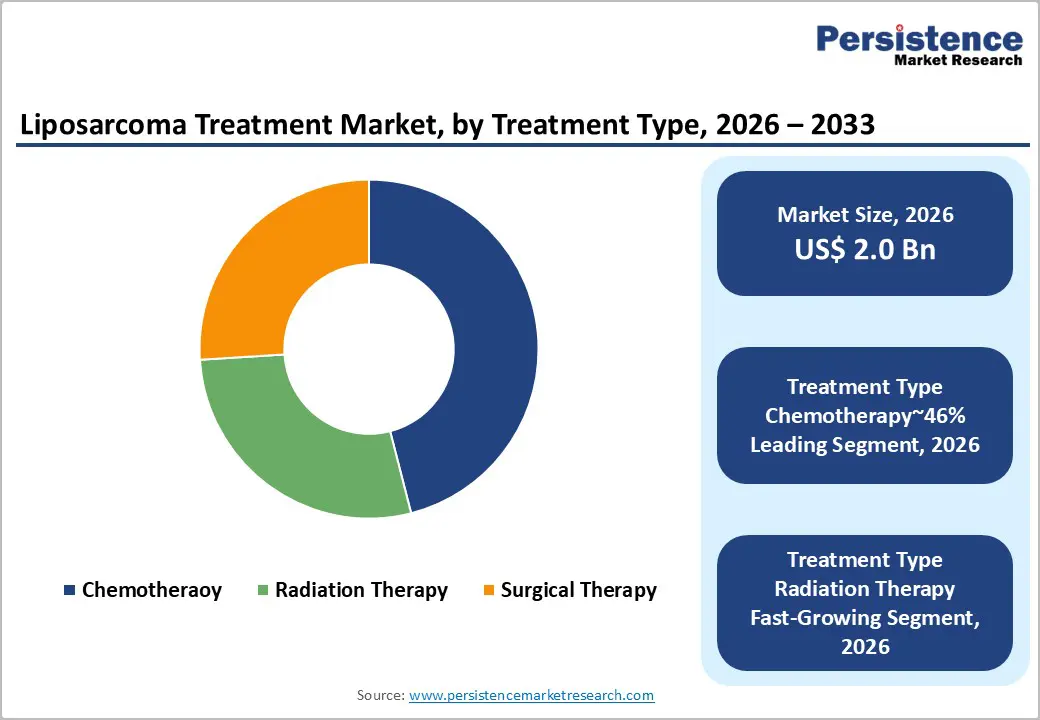

- Leading Treatment Type: Chemotherapy is expected to lead, accounting for approximately 46% share in 2026, anchored by its status as a primary systemic intervention for metastatic cases and high procedural volume.

- Leading Drug Type: Targeted Therapy Drugs are anticipated to dominate, accounting for approximately 46% share in 2026, anchored by superior molecular precision and reduced systemic toxicity profiles.

| Key Insights | Details |

|---|---|

|

Liposarcoma Treatment Market Size (2026E) |

US$2.0 Bn |

|

Market Value Forecast (2033F) |

US$2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

DRO Analysis

Driver Analysis – Orphan Drug Incentives in Rare Oncology Development

Regulatory frameworks provide substantial financial and operational advantages for developers targeting rare oncology indications globally. Extended market exclusivity periods offset high research and development expenditures associated with limited patient populations. These incentives encourage investment into niche segments addressing significant unmet clinical needs within liposarcoma treatment. Streamlined approval pathways accelerate progression from clinical validation to commercial availability across regulated markets. Government agencies align policy structures to support innovation within complex and low-prevalence disease categories. Cost dynamics shift favorably through reduced regulatory fees and enhanced funding accessibility mechanisms. These factors collectively sustain innovation momentum across specialized oncology therapeutic pipelines.

Ipsen with Tazverik benefits from orphan designations targeting specific epigenetic drivers within sarcoma treatment frameworks. Availability of specialized grants enables expansion of early-stage candidates into advanced clinical trial phases. Tax credits and regulatory fee waivers lower entry barriers for biotechnology firms pursuing rare disease innovations. Market participants leverage these incentives to establish competitive positioning within fragmented therapeutic categories. Pipeline diversification strengthens as firms explore targeted interventions across genetically defined patient subsets. These regulatory enablers reinforce consistent development of therapies addressing refractory and underserved oncology populations.

Molecular Targeting Precision in Dedifferentiated Liposarcoma

Advancements in genomic sequencing are transforming therapeutic strategies for dedifferentiated liposarcoma variants across oncology settings. Clinicians increasingly deploy molecular profiling to detect specific genetic amplifications within malignant tumor cells. This diagnostic precision enables the selection of personalized regimens aligned with tumor-specific biological pathways. Improved accuracy strengthens the adoption of advanced pharmaceutical interventions across specialized oncology treatment centers. Regulatory frameworks support targeted therapies demonstrating clear biomarker-linked efficacy and controlled safety profiles. Cost structures shift toward high-value precision drugs and integrated diagnostic infrastructure within hospital systems. These dynamics sustain demand for molecularly targeted oncology products addressing complex and rare tumor types.

Boehringer Ingelheim, with Brigimadlin, advances MDM2 inhibition as a mechanism restoring disrupted tumor suppression pathways. These agents demonstrate efficacy in controlling malignant proliferation while preserving surrounding healthy tissue integrity. Targeted action reduces reliance on conventional cytotoxic therapies associated with systemic toxicity burdens. Clinical trial progression strengthens validation of molecular therapies within first-line treatment protocols. Oncology providers increasingly integrate biomarker-driven treatments into standardized clinical pathways for rare cancers. This transition reinforces the expansion of niche therapeutic segments within precision oncology markets.

Restraint Analysis – Clinical Trial Recruitment Constraints in Liposarcoma Research

The low prevalence of liposarcoma subtypes constrains the assembly of statistically robust clinical trial cohorts globally. Identifying eligible patients meeting strict molecular criteria requires extensive, resource-intensive screening protocols. Geographically dispersed patient pools increase logistical complexity across multi-center and cross-border study designs. These recruitment barriers extend development timelines, delaying regulatory submissions and subsequent commercial market entry. Limited patient availability restricts trial scalability, reducing statistical power and complicating endpoint validation processes. Regulatory expectations for biomarker-driven enrollment further intensify screening burdens within specialized oncology trials. These structural constraints collectively hinder the efficient advancement of emerging therapeutic candidates within rare cancer pipelines.

Rain Oncology with Milademetan experienced clinical setbacks, underscoring the inherent risks associated with niche oncology drug development. High attrition rates during late-stage testing discourage sustained investment from smaller biotechnology participants. Unanticipated safety signals or efficacy limitations frequently result in discontinuation of otherwise promising programs. Pipeline volatility introduces uncertainty across development portfolios targeting genetically defined cancer subpopulations. Capital allocation strategies increasingly reflect heightened risk exposure within rare disease clinical research environments. Consistent and high-quality data generation remains critical to mitigate these barriers and sustain therapeutic progress.

Supply Chain Vulnerabilities in Liposarcoma Chemotherapy Access

Active pharmaceutical ingredient shortages disrupt the availability of chemotherapy regimens used in liposarcoma treatment protocols. Global sourcing dependencies expose supply chains to geopolitical tensions, elevating procurement costs during production cycles. Manufacturers increasingly ration allocations, prioritizing high-volume oncology indications over rare cancer requirements. These constraints limit consistent access to essential drugs within specialized oncology treatment centers. Healthcare providers face uncertainty in maintaining continuity of care due to intermittent supply disruptions. Cost volatility further pressures hospital procurement budgets and complicates inventory planning across distribution networks. Such vulnerabilities collectively weaken the reliability of chemotherapy access within rare oncology treatment ecosystems.

Teva Pharmaceutical Industries, with Doxorubicin, navigates recurring disruptions that extend lead times and complicate distribution scheduling frameworks. Providers respond by seeking therapeutic alternatives, often compromising established treatment pathway consistency. End-users adopt cautious stockpiling strategies, which further distort demand forecasting across supply networks. Allocation imbalances create uneven drug availability across regions, affecting treatment equity within oncology systems. Logistics inefficiencies intensify under constrained supply conditions, increasing operational burdens for distributors and healthcare facilities. These interlinked challenges constrain stable utilization of core chemotherapy agents across liposarcoma care pathways.

Opportunity Analysis – Digital Health Integration in Oncology Care Delivery

Adoption of digital platforms for remote patient monitoring enhances management of treatment-related toxicities across oncology settings. Healthcare providers deploy specialized applications to capture real-time physiological data and dynamically adjust therapeutic dosages. This digital intervention reduces dependency on frequent hospital visits while lowering operational and patient-incurred costs. Continuous data streams from wearable devices strengthen clinical datasets and improve research accuracy within oncology trials. Regulatory frameworks increasingly recognize digital endpoints as valid components within therapeutic evaluation processes. Cost structures shift toward interoperable platforms, cloud infrastructure, and secure patient data management systems. These developments collectively enable more efficient and patient-centric oncology service delivery models.

Merck & Co., with Keytruda integrates digital monitoring tools within research programs to track patient response patterns more effectively. Telehealth capabilities expand access for rural patients requiring consultation with specialized sarcoma treatment experts. Integrated electronic health records improve coordination across multidisciplinary oncology care teams and treatment pathways. Digital convergence enhances continuity of care by linking diagnostics, treatment monitoring, and clinical decision frameworks. Data-driven insights support optimized therapeutic adjustments and improved patient outcome tracking. These technological integrations expand the reach and scalability of advanced oncology treatments across diverse healthcare environments.

Biomarker-Driven Stratification in Liposarcoma Therapeutics

Emerging companion diagnostics enable refined stratification across liposarcoma subtypes, supporting personalized therapy selection frameworks. Clinicians increasingly rely on genomic panels to identify predictive markers linked with therapeutic response patterns. Policy shifts toward value-based care reinforce the adoption of treatments aligned with biomarker-validated efficacy outcomes. Rising genomic testing volumes strengthen the integration of diagnostics within routine oncology decision-making pathways. Regulatory systems support co-development of drugs and diagnostics, accelerating synchronized approvals across targeted treatment categories. Cost structures evolve toward bundled diagnostics and therapy models within precision oncology ecosystems. These dynamics collectively expand addressable cohorts for biomarker-driven liposarcoma interventions.

Foundation Medicine’s FoundationOne CDx advances stratification capabilities through comprehensive genomic profiling platforms used in oncology settings. Providers leverage such diagnostic panels to guide treatment decisions with improved clinical confidence. Targeted uptake of therapies increases as molecular classification refines patient eligibility across subtypes. Strategic expansions in diagnostic infrastructure position vendors to capture growing volumes of genomically profiled patients. Integration of testing within clinical workflows enhances efficiency across multidisciplinary oncology teams. These developments reinforce the sustained growth of precision-driven treatment pathways within liposarcoma care frameworks.

Category-wise Analysis

Treatment Type Insights

Chemotherapy is expected to lead the liposarcoma treatment market, accounting for approximately 46% share, underpinned by its role as the primary systemic intervention for advanced stages. Systemic cytotoxic agents remain the standard care for patients with unresectable or metastatic disease. High procedural volume within public and private hospitals supports consistent procurement of these medications. Adoption remains anchored in established clinical guidelines and long-term efficacy data across diverse populations. Healthcare systems prioritize chemotherapy due to its broad accessibility and familiar administrative protocols. This structural reliance on chemical interventions reinforces the segment’s leadership within the therapeutic landscape.

Radiation Therapy is forecast to be the fastest-growing segment in the Liposarcoma Treatment Market, driven by the rising adoption of neoadjuvant protocols to improve surgical success. Clinicians increasingly utilize targeted radiation to shrink tumors before performing complex limb-sparing resections. This strategic shift toward preoperative intervention is anticipated to enhance long-term local control rates. Advanced delivery systems like Varian Medical Systems with Halcyon allow for precise dose distribution with minimal tissue damage. Ongoing improvements in imaging guidance further strengthen the utility of radiation in multimodal care. This convergence of technological precision and expanding clinical applications sustains the segment's rapid acceleration. Manufacturers continue to innovate in dose optimization to reduce secondary toxicities for oncology patients.

Drug Type Insights

Targeted therapy drugs are anticipated to lead the liposarcoma treatment market, accounting for approximately 46% share in 2026, reinforced by superior molecular specificity and patient tolerability. These agents interact with specific proteins that drive malignant cell growth and survival. Clinicians prefer targeted options to minimize the systemic side effects typically associated with conventional treatments. This preference is set to expand as molecular diagnostics become more integrated into routine care. Research investments focus on inhibiting key pathways like MDM2 and CDK4 in sarcoma cells. This molecular focus continues to anchor the segment's dominant position in the pharmaceutical category.

Targeted therapy drugs are also projected to be the fastest-growing segment, driven by the emergence of next-generation inhibitors that address previously refractory cases. Breakthroughs in synthetic lethality and protein degradation offer new mechanisms for arresting tumor progression. Pharmaceutical vendors prioritize the development of oral agents to improve patient compliance and convenience. Increasing regulatory support for orphan drugs accelerates the transition of these candidates to the market. This constant innovation in drug design ensures a robust pipeline of high-value therapeutic options. Ongoing clinical trials are likely to expand the addressable patient pool for these advanced medications.

Regional Insights

North America Liposarcoma Treatment Market Trends

North America is expected to remain the leading regional market, accounting for approximately 40% share in 2026, supported by high healthcare expenditures and advanced research infrastructure. The region's dominance is anchored in the early adoption of novel targeted therapies and sophisticated molecular diagnostic tools. Well-established clinical trial networks facilitate the rapid validation and commercialization of emerging pharmaceutical candidates. High awareness among healthcare professionals regarding rare sarcoma subtypes ensures early and accurate patient diagnosis. Public and private insurance frameworks provide robust coverage for high-cost oncology treatments and surgical procedures. Consistent investment in biotechnology innovation further reinforces the region's central role in the global oncology landscape.

The U.S. is expected to anchor regional momentum through sustained federal funding for rare disease research and specialized cancer centers. Regulatory incentives such as Breakthrough Therapy designations are anticipated to accelerate the market entry of advanced medications. High demand for robotic-assisted surgery continues to drive procurement of advanced systems across major metropolitan hospitals. Strategic partnerships between academic institutions and private firms are forecast to yield diverse therapeutic breakthroughs. Continuous updates to oncology guidelines further ensure the integration of the latest clinical evidence into practice.

Europe Liposarcoma Treatment Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in replacement cycles and compliance upgrades. Regional market dynamics are influenced by centralized healthcare systems that prioritize cost-effectiveness and long-term clinical value. Strong regulatory oversight by the European Medicines Agency ensures high safety standards for all marketed oncology products. Academic research clusters in major economies drive the development of innovative surgical and radiation protocols. Increasing emphasis on personalized medicine is set to expand the utilization of molecularly targeted agents. Unified clinical guidelines across the region support consistent treatment standards for rare soft tissue cancers.

Germany is forecast to remain the primary driver of regional market growth through its extensive network of specialized oncology clinics and research institutes. The national healthcare system provides comprehensive access to the latest pharmaceutical and surgical interventions for sarcoma patients. High investments in medical imaging technology support early detection and more accurate tumor staging across the country. Collaborative research projects under the Horizon Europe framework are expected to foster cross-border clinical innovation. Rising adoption of digital health solutions is likely to improve patient monitoring and data collection.

Asia Pacific Liposarcoma Treatment Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as infrastructure buildout and manufacturing scale accelerate market expansion across the region. Rising investments in public healthcare systems are expanding access to specialized oncology care in developing economies. Urbanization and an aging population are contributing to a higher incidence of complex cancer cases requiring intervention. Increasing medical tourism is forecast to drive demand for world-class surgical and radiation facilities in regional hubs. Manufacturers are anticipated to localize production and distribution strategies to enhance the affordability of essential treatments. Strategic shifts toward universal health coverage are expected to improve procurement volumes for oncology drugs.

China is expected to lead regional acceleration through massive investments in domestic pharmaceutical research and hospital infrastructure modernization. Government initiatives to streamline drug approvals are anticipated to bring novel targeted therapies to the market more quickly. Expansion of private hospital chains is projected to increase the availability of advanced robotic surgery and radiation. Rising disposable incomes among the middle class are driving demand for premium healthcare services and personalized treatments. Collaborative ventures with global vendors are forecast to enhance local clinical expertise and service delivery.

Competitive Landscape

The Liposarcoma Treatment market is consolidated, with leadership concentrated among pharmaceutical firms such as Eisai and Janssen Pharmaceutical. These companies exert influence through robust oncology pipelines, clinical trial leadership, and integration with global treatment networks. Their therapies establish benchmarks for efficacy, safety, and regulatory acceptance across advanced-stage disease management. Strong relationships with oncology centers and established reimbursement pathways reinforce consistent adoption. Their operational scale and patient access programs support widespread treatment availability across key regions. This concentration creates high entry barriers, particularly within specialized oncology drug development and approval frameworks.

Competitive positioning reflects vertical differentiation through targeted molecular therapies and integration across diagnostic and treatment pathways. Premium participants emphasize precision oncology approaches addressing specific genetic drivers of tumor progression. Companies such as Boehringer Ingelheim and Ipsen advance specialized agents aligned with biomarker-driven treatment strategies. Industry dynamics include strategic acquisitions of early-stage assets to strengthen innovation pipelines. Platform evolution increasingly incorporates combination therapies and diagnostic integration, enhancing clinical decision-making. Forward-looking strategies prioritize navigation of reimbursement complexities and expansion of precision-based treatment models across oncology care ecosystems.

Key Industry Developments:

- In March 2026, the FDA granted tentative approval to a radioequivalent of Lutathera, signaling an expansion of the radioligand therapy market. While primarily for neuroendocrine tumors, this regulatory openness paves the way for radioligand development in other rare solid tumors such as liposarcoma.

- In January 2026, Intensity Therapeutics confirmed that it secured the necessary resources to reinitiate site activations for its Phase 3 liposarcoma study in Q1 2026. Resuming this trial is critical for the competitive space as it tests a localized "intratumoral" delivery method that could reduce the systemic toxicity typical of standard chemotherapy.

- In April 2025, Mabwell initiated a strategic collaboration with DP Technology to use AI-driven molecular simulations for the development of its B7-H3-targeting ADC. This partnership aims to reduce drug discovery timelines and improve the therapeutic window of ADCs used in refractory solid tumors like liposarcoma.

Companies Covered in Liposarcoma Treatment Market

- Johnson & Johnson

- Novartis AG

- Pfizer Inc.

- Merck & Co.

- Eli Lilly

- Bayer

- Eisai Co., Ltd.

- Bristol Myers Squibb

- Ipsen

- Boehringer Ingelheim

- Exelixis

- Adaptimmune Therapeutics

- Rain Oncology

- Intensity Therapeutics

- Sotio Biotech

- Intuitive Surgical

Frequently Asked Questions

The global liposarcoma treatment market is projected to be valued at US$2.0 billion in 2026 and is expected to reach US$2.7 billion by 2033, driven by the increasing incidence of rare soft tissue sarcomas and the expanding adoption of precision oncology therapies.

Orphan drug frameworks significantly drive market growth by offering extended exclusivity, tax credits, and reduced regulatory fees, which offset high R&D costs and encourage companies like Ipsen and Boehringer Ingelheim to invest in niche oncology pipelines targeting rare sarcoma subtypes.

The liposarcoma treatment market is forecast to grow at a CAGR of 4.6% from 2026 to 2033, reflecting steady demand for targeted therapies, advancements in molecular diagnostics, and increasing integration of biomarker-driven treatment approaches.

North America is the leading regional market, accounting for approximately 40% share, supported by advanced healthcare infrastructure, strong clinical research ecosystems, and early adoption of innovative therapies from companies such as Merck & Co. and Johnson & Johnson.

The liposarcoma treatment market is relatively consolidated, with key players including Novartis AG, Pfizer Inc., Eli Lilly, Bristol Myers Squibb, and Eisai Co., Ltd., competing through targeted therapy innovation, clinical trial expansion, and integration of precision medicine platforms.