- Automotive Components & Materials

- Automotive Cockpit Electronics Market

Automotive Cockpit Electronics Market Size, Share, and Growth Forecast for 2025 - 2032

Automotive Cockpit Electronics Market By Product Type (Infotainment & Navigation, Instrument Clusters, Others), Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Automotive Cockpit Electronics Market Size and Trends Analysis

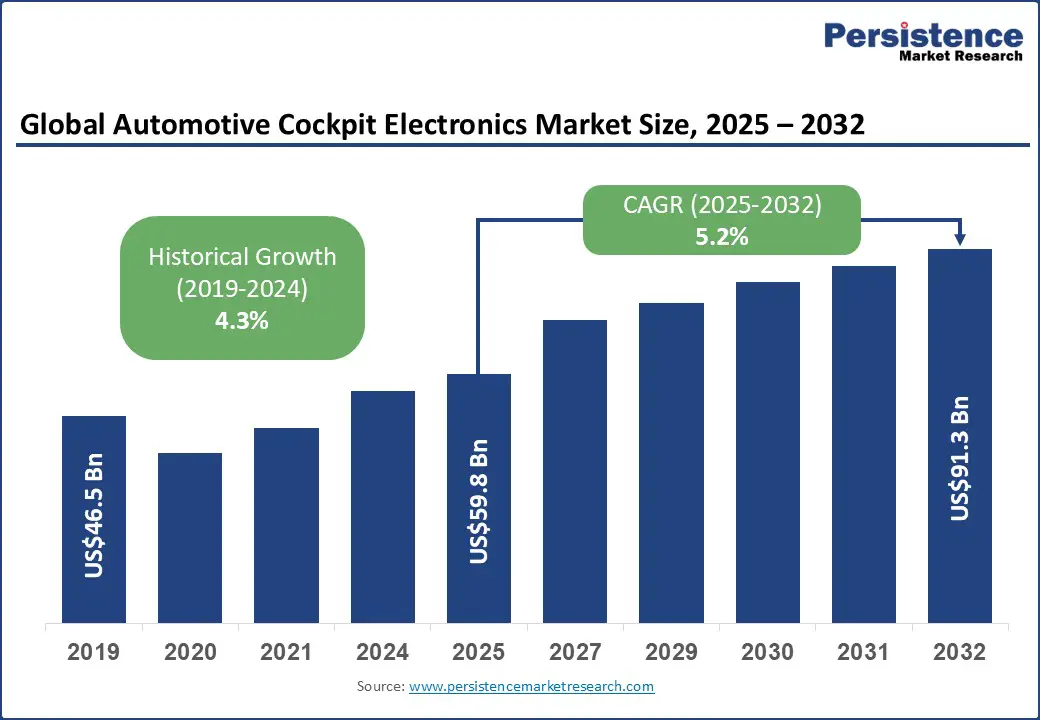

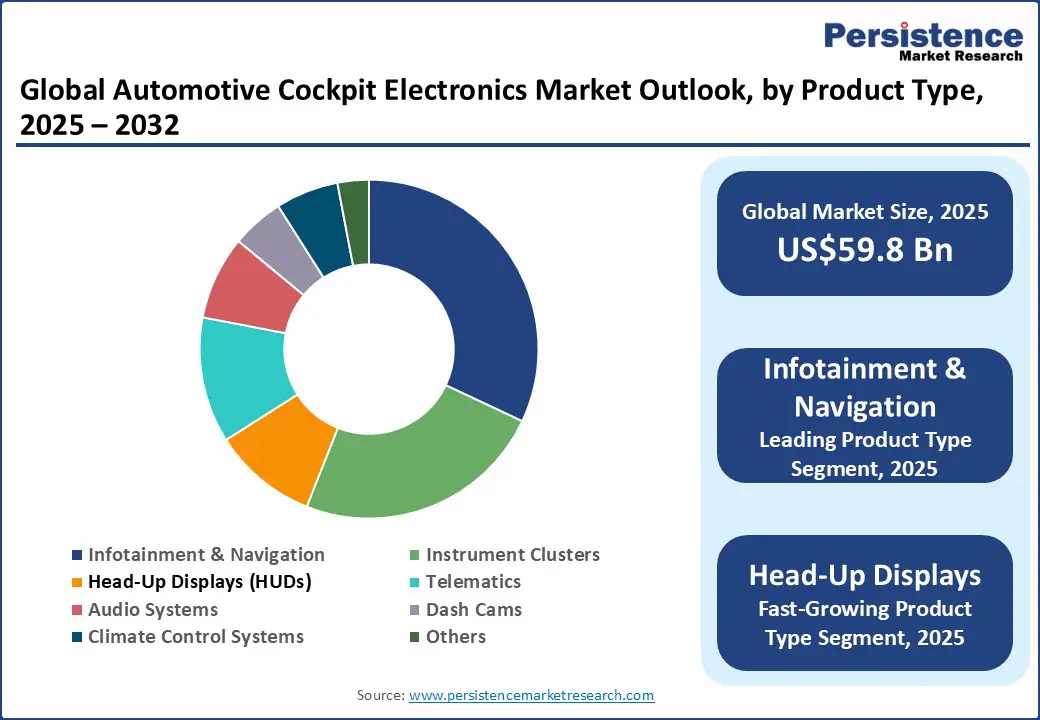

The global automotive cockpit electronics market size is likely to be valued at US$59.8 Bn in 2025 and is expected to reach US$91.3 Bn by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, driven by rapid technological advancements in ADAS, rising demand for vehicle connectivity and digitalization, increasing adoption of electric and autonomous vehicles.

Key Industry Highlights

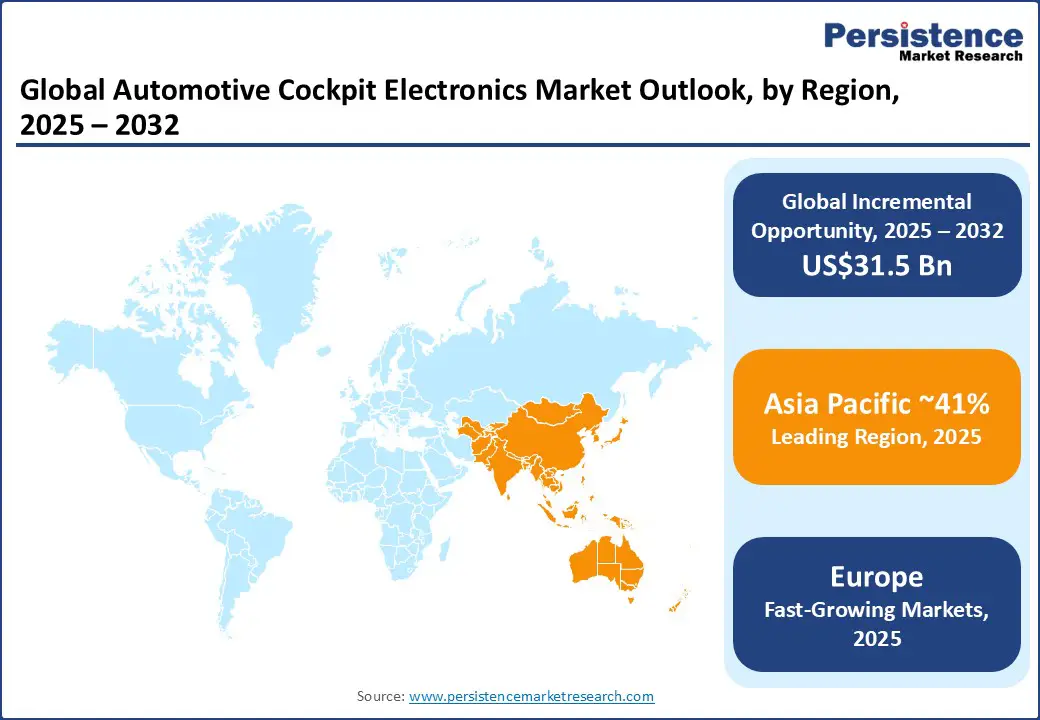

- Leading Region: Asia Pacific holds a significant market share, capturing around 41% of the global market in 2025, fueled by strong automotive manufacturing, EV penetration, and rapid adoption of connected cockpit technologies.

- Fastest-growing Region: Europe is becoming a key growth region, with a projected 5.8% CAGR, driven by strict safety regulations, the rise of advanced driver-assistance systems (ADAS), and increasing consumer demand for connected cockpit technologies.

- Leading Vehicle Type: Passenger vehicles hold the largest market share at nearly 65%, driven by the widespread adoption of infotainment systems, digital instrument clusters, and safety-focused cockpit technologies that have become standard features in the latest car models.

- Dominant Product Type: Infotainment & Navigation leads the market with a dominant share of ~32%, fueled by growing consumer expectations for seamless connectivity, intuitive touchscreen interfaces, and highly personalized in-vehicle digital experiences.

| Key Insights | Details |

|---|---|

| Automotive Cockpit Electronics Market Size (2025E) | US$59.8 Bn |

| Market Value Forecast (2032F) | US$91.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Mandates and Digital Innovation Accelerate the Global Adoption of Cockpit Electronics

The automotive cockpit electronics market growth is propelled by strong regulatory enforcement aimed at improving road safety and vehicle intelligence. The European Union’s General Safety Regulation mandates advanced driver distraction warning systems, requiring driver monitoring technologies in all new type approvals from July 2024 and across all new vehicles by July 2026. Euro NCAP has also added driver monitoring to its five-star safety rating criteria, creating significant pressure on automakers to deploy advanced cockpit electronics that enhance compliance, safety, and consumer trust.

The International Organization of Motor Vehicle Manufacturers (OICA) reported that global vehicle sales rose from 82.9 million in 2022 to 95.2 million in 2024. This rebound in production and sales underscores the growing opportunity for cockpit electronics, as manufacturers align vehicle platforms with both safety compliance and consumer demand for connected, intuitive, and digitally enhanced driving experiences. The combination of regulation and rising vehicle volumes is set to drive sustained growth in the decade ahead.

Supply Chain Vulnerabilities and Cybersecurity Risks Hinder Cockpit Electronics Expansion

Significant challenges, such as semiconductor supply shortages and rising cybersecurity threats, are evident. The industry’s heavy reliance on advanced microchips has exposed vulnerabilities, with disruptions in semiconductor supply chains leading to delayed vehicle production and constrained adoption of next-generation cockpit systems.

At the same time, the rapid integration of connected features and over-the-air updates has elevated cybersecurity risks, compelling automakers to invest heavily in data protection and compliance with evolving standards. These risks not only increase development timelines and costs but delay large-scale deployment across mass-market vehicles, limiting the pace of global market growth despite strong consumer and regulatory demand.

Digital Integration and Policy-Driven Innovation Unlock New Growth Avenues in Cockpit Electronics

The automotive cockpit electronics market is set to benefit from rapid advancements in digitalization, with connected displays, AI-enabled interfaces, and voice-controlled systems becoming central to in-vehicle experiences. Growing consumer demand for personalization and seamless connectivity is reshaping the design of cockpit systems, while sustainability considerations are encouraging the use of energy-efficient electronics and lightweight materials. These factors are accelerating the shift toward smarter and greener cockpit architectures. Support for this transformation is visible in both policy initiatives and industry actions.

The EU's Vision Zero program aims for zero road fatalities by 2050 and supports the integration of advanced safety technologies in cockpits. Leading manufacturers, including BMW and Tesla, are investing in augmented reality head-up displays and centralized digital cockpits to enhance driver interaction and safety. These collaborations between regulators and automakers position cockpit electronics as essential for the automotive industry's shift toward connected and sustainable mobility.

Category-wise Analysis

Product Type Insights

Infotainment and navigation systems dominate the product landscape with ~32% share, driven by consumer demand for connected experiences, seamless smartphone integration, and OEM strategies that position these platforms as the backbone of digital cockpits.

Head-up displays record the fastest growth at an estimated 7.7% CAGR as augmented reality overlays and safety-focused user interfaces are increasingly adopted in premium and electric vehicle lineups. Telematics is strengthening through regulatory frameworks such as eCall and fleet management mandates, accelerating the adoption of remote diagnostics and connected services.

Audio systems, dash cams, and climate controls play supportive roles by supporting in-cabin entertainment, insurance-linked safety monitoring, and efficient energy management. Collectively, policy incentives, software consolidation, and shifting consumer expectations are transforming vehicle interiors into integrated, software-centric cockpit ecosystems.

Vehicle Type Insights

Passenger vehicles account for the largest share at nearly 65%, supported by the widespread installation of infotainment, digital clusters, and safety-oriented cockpit systems that are now standard across the latest car models. Their dominance is driven by consumer demand for comfort, connectivity, and regulatory-backed safety features.

Electric vehicles are experiencing booming growth with a CAGR of ~9.8%. This surge is driven by automakers' emphasis on integrating advanced digital interfaces, head-up displays, and AI-powered telematics to enhance efficiency and improve the driver experience.

Light and heavy commercial vehicles also contribute meaningfully, supported by fleet digitalization initiatives and stricter safety mandates, though adoption rates remain more gradual. Collectively, the mix of established passenger car demand and accelerating EV adoption underscores how cockpit electronics are shaping the evolution of global mobility.

Regional Insights

Asia Pacific Automotive Cockpit Electronics Market Trends - Innovation-Led Growth and Policy-Backed Adoption

Asia Pacific is expected to lead the global market with a 41% share in 2025, powered by robust vehicle production, electrification, and consumer demand for connected experiences.

China remains at the forefront, where cockpit digitization is accelerating through collaborations such as Baidu’s partnership with Geely to advance next-generation infotainment for EVs, reflecting the integration of big tech into automotive ecosystems. In 2023, SAIC Motor also introduced AR-based head-up display systems in select premium models, signaling rapid adoption of advanced interfaces.

Japan sustains its position with strict safety regulations, which prompted Toyota’s rollout of expanded digital cluster offerings across hybrid and EV lineups to meet consumer and compliance needs. South Korea is bolstered by technology-driven OEMs, with Hyundai and Kia unveiling connected cockpit platforms that integrate AI assistants and AR HUDs in recent launches.

India, meanwhile, is emerging strongly under government-backed EV schemes, highlighted by Tata Motors’ 2023 initiative to localize cockpit electronics production for its EV range. Collectively, these developments underscore the Asia Pacific’s dominance, driven by scale, innovation, and policy alignment.

North America Automotive Cockpit Electronics Market Trends - Digital Cockpit Transformation through EV Synergy and Connected Ecosystems

North America is projected to hold about a 21% share of the market in 2025, shaped by high consumer preference for connected infotainment, advanced telematics, and in-cabin personalization. The U.S. leads the region, with major automakers driving cockpit innovation.

General Motors launched its Ultifi software platform in 2023 to enable over-the-air upgrades and personalized digital experiences, underscoring the transition to software-defined vehicles. Similarly, Ford partnered with Google to embed Android Automotive OS into future models, ensuring deeper integration of navigation, voice assistants, and cloud connectivity.

Tesla continues to influence cockpit design trends with its minimalist, screen-dominated layouts, while Stellantis announced an expansion of its STLA SmartCockpit platform, developed with Foxconn, to accelerate EV-centric cockpit solutions.

Canada adds momentum with government-backed EV adoption targets, fostering demand for advanced cockpit electronics in electric mobility programs. With strong OEM investments, partnerships with tech companies, and growing EV penetration, North America is shaping itself as a hub for digital cockpit transformation driven by connectivity and electrification.

Europe Automotive Cockpit Electronics Market Trends - Safety Mandates and Premium OEM Integration

Europe is likely to be the fastest-growing region of the global market in 2025, with a CAGR of 5.8%. This growth is supported by a strong base of premium OEMs and regulatory initiatives that emphasize safety and sustainability.

Germany leads the region, where manufacturers such as BMW and Mercedes-Benz have expanded digital cockpit offerings with larger AR-based head-up displays in recent 2023 launches, reflecting rising consumer expectations for immersive in-cabin technology. In addition, Continental introduced a next-generation integrated digital cluster platform in 2023, strengthening the region’s supplier ecosystem.

France and Italy are contributing with policies supporting electrification, which in turn accelerates demand for cockpit digitization in EV models. The U.K. has also witnessed growth as Jaguar Land Rover rolled out new infotainment platforms with over-the-air update capabilities, aligning with the trend toward software-defined vehicles.

Meanwhile, the European Union’s push for the General Safety Regulation (GSR), effective in 2024, mandating advanced driver-assistance features, is indirectly boosting the integration of telematics and advanced clusters. These combined dynamics are firmly positioning Europe as a frontrunner in defining the future of cockpit electronics.

Competitive Landscape

The global automotive cockpit electronics market is experiencing strong competition as manufacturers focus on modular designs, software-defined platforms, and strategic partnerships. This drive leads to faster innovation and broader adoption, especially with the rise of electrification and connectivity.

Competition is increasingly focused on capturing future mobility opportunities rather than competing solely on price. Suppliers and distributors are crucial in localizing sourcing and enhancing semiconductor pipelines, which strengthens supply chains and supports smoother rollouts in a growth-friendly environment.

Key Industry Developments

- In July 2025, Minda Corporation Limited, the flagship company of the Spark Minda Group, announced its strategic collaboration with Qualcomm Technologies, Inc. to develop smart and advanced cockpit solutions for the Indian automotive market.

- In December 2024, a leading supplier introduced its "Emotional Cockpit" display concept at CES 2025, featuring Swarovski elements and AI interaction to enhance driver engagement. This innovation showcases the trend of merging luxury design with intelligent electronics for immersive in-car experiences.

- In April 2024, a leading automotive supplier announced a joint venture in Hefei with a major Chinese automaker to establish a “Cockpit of the Future” operation, aiming for sustainable cockpit module production and targeting over €1 Bn (US$1.07 Bn) in sales by 2029. The collaboration focuses on advanced human-machine interfaces and eco-friendly materials to align with China’s growing EV ecosystem.

Companies Covered in Automotive Cockpit Electronics Market

- Visteon Corporation

- Panasonic Corporation

- Harman International Industries

- Clarion Co., Ltd

- Alpine Electronics, Inc

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Garmin Ltd.

- Hyundai Mobis

- Aptiv plc

- Valeo S.A.

- Pioneer Corporation

- Faurecia

- Infineon Technologies AG

Frequently Asked Questions

The automotive cockpit electronics market is expected to reach US$59.8 Bn in 2025.

Regulatory mandates for safety, rising consumer demand for connected features, and rapid digital innovation are accelerating the global adoption of cockpit electronics.

The automotive cockpit electronics market is estimated to rise at a CAGR of 5.2% from 2025 to 2032.

Seamless digital integration, coupled with policy-driven innovation, is unlocking new growth avenues in the cockpit electronics market, enabling smarter, safer, and more immersive in-vehicle experiences.

The major players dominating the automotive cockpit electronics market are Visteon Corporation, Panasonic Corporation, Harman International Industries, Clarion Co., Ltd, Alpine Electronics, Inc., and Continental AG.