- Specialty & Fine Chemicals

- Lactic Acid Market

Lactic Acid Market Size, Share, and Growth Forecast 2026 - 2033

Lactic Acid Market by Feedstock (Corn, Sugarcane, Cassava, Yeast Extract, 2nd Gen. Sources, Other Crops), by Application (Food & Beverages, Pharmaceuticals, Personal Care, Industrial, Biodegradable Plastics/PLA, Others), Production Method (Fermentation, Chemical Synthesis), and Regional Analysis for 2026 - 2033

Lactic Acid Market Size and Trend Analysis

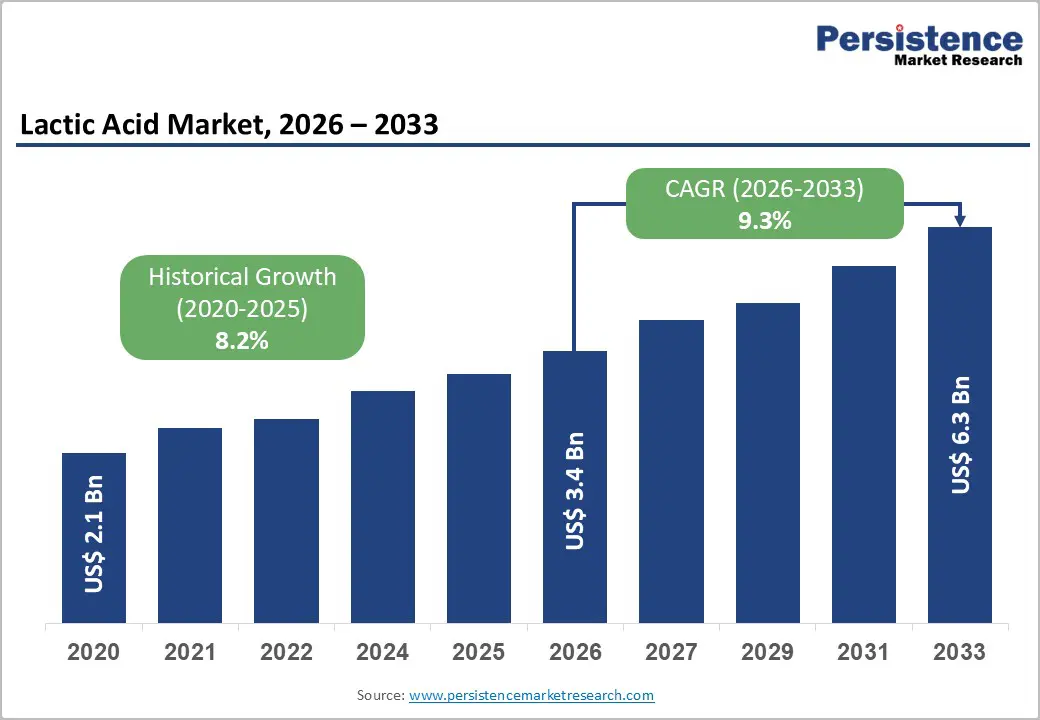

The global Lactic Acid market size is supposed to be valued at US$ 3.4 billion in 2026 and is projected to reach US$ 6.3 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

The market's strong and accelerating growth trajectory is anchored in the global transition to bio-based, biodegradable materials, driven by legislative bans on single-use petroleum plastics, the rapid commercial scale-up of Polylactic Acid (PLA) bioplastics consuming lactic acid as their primary monomer feedstock, and expanding pharmaceutical and food preservation applications leveraging lactic acid's natural biocompatibility and multifunctional chemistry.

Key Industry Highlights:

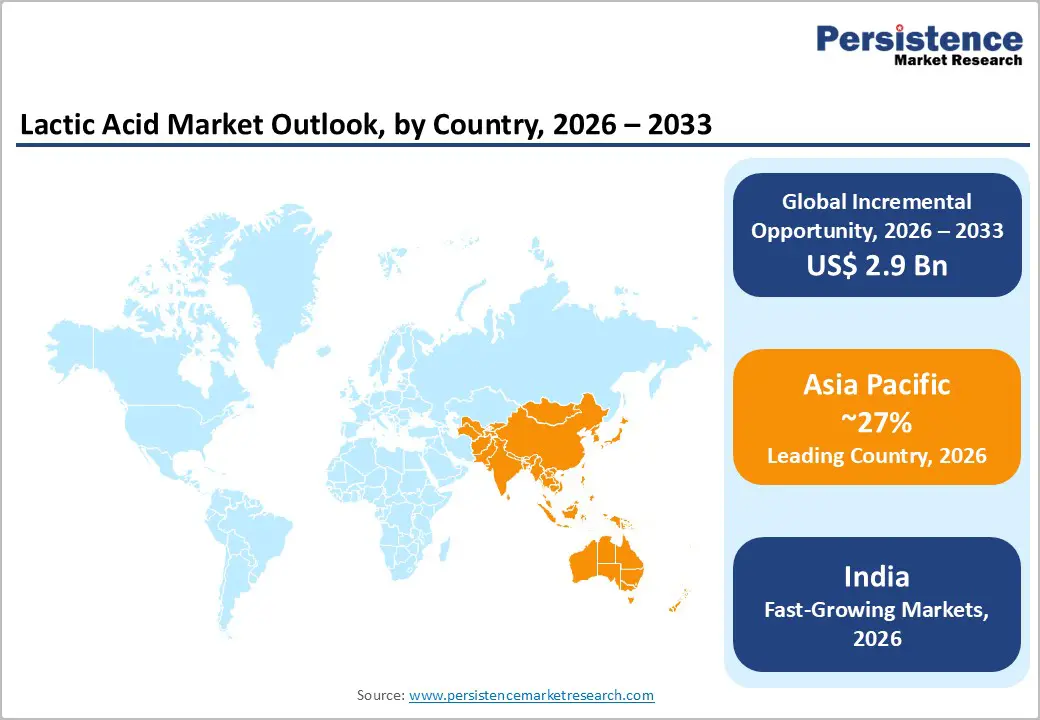

- Leading Region: Asia Pacific leads the global Lactic Acid market in volume, anchored by COFCO's world-scale corn fermentation capacity, Corbion's 125,000-tpa Thailand plant commissioned in 2024, China NDRC's national plastic ban stimulating domestic PLA demand, and NatureWorks LLC's second Asia Pacific PLA facility under development with PTT Global Chemical in Thailand.

- Fastest Growing Country: Thailand's emergence as a global integrated lactic acid-PLA production hub, India's expanding pharmaceutical PLGA procurement, and Corbion's TotalEnergies Corbion joint venture Rayong operations makes these countries as fastest growing market.

- Dominant Application: Biodegradable Plastics (PLA) is the dominant Application segment with approximately 38% revenue share, confirmed by multiple industry analyses, anchored by the EU Single-Use Plastics Directive, China NDRC plastic ban, Ellen MacArthur Foundation's 1,000+ brand signatory commitments to compostable packaging, and PLA's 68% lower GHG emissions profile versus petroleum plastics sustaining structural demand growth.

- Dominant Production Process: Fermentation is the dominant and commercially preferred Production Method with approximately 70% revenue share, driven by its 60% lower carbon footprint vs. chemical routes, renewable feedstock alignment with EU Green Deal and U.S. BioPreferred policy frameworks, and Corbion's circular fermentation technology demonstrating industry-leading sustainability performance at world-scale commercial deployment in Thailand.

- Opportunity: Second-generation feedstock lactic acid and circular waste valorization represent the key market opportunity, with Cellulac Ltd.'s food waste-to-lactic acid platform, DOE BETO 2G fermentation R&D investment, and the EU Circular Economy Action Plan creating favorable policy and commercial conditions for waste-derived lactic acid production that eliminates food crop competition and generates carbon-negative production economics.

| Key Insights | Details |

|---|---|

|

Lactic Acid Market Size (2026E) |

US$ 3.4 Billion |

|

Market Value Forecast (2033F) |

US$ 6.3 Billion |

|

Projected Growth CAGR (2026–2033) |

9.3% |

|

Historical Market Growth (2020–2025) |

8.2% |

Market Dynamics

Drivers - Rise in Global Demand for PLA Bioplastics Fueled by Plastic Ban Legislation and Circular Economy Policies

The global bioplastics industry's rapid and structurally sustained expansion, driven by governments worldwide enacting legislation to eliminate single-use petroleum-based plastics from packaging, food service, agriculture, and textile applications, is the single most powerful demand driver propelling the lactic acid market to above-average growth through the forecast period, as PLA manufactured from polymerized lactic acid is the world's most commercially scaled biodegradable thermoplastic alternative. The European Union's Single-Use Plastics Directive (SUPD), banning ten categories of single-use plastic products across all 27 EU member states from July 2021, and the China NDRC's national plastic restriction policy banning non-degradable plastic bags and straws in major cities and postal delivery applications from 2021 are collectively mobilizing commercial demand for PLA packaging, agricultural film, and disposable product alternatives at an unprecedented scale.

Per peer-reviewed life cycle assessment data, PLA production generates approximately 68% fewer GHG emissions than conventional polyethylene and polypropylene, making it a technically and commercially compelling sustainability solution for brands, retailers, and packaging converters facing carbon disclosure and scope 3 emissions reduction pressure under frameworks including the Science Based Targets initiative (SBTi). NatureWorks LLC (Blair, Nebraska, USA), the world's largest PLA manufacturer, and TotalEnergies Corbion (Rayong, Thailand), producing Luminy® PLA via the 50/50 joint venture between TotalEnergies and Corbion, together represent the world's two dominant commercial platforms consuming lactic acid at world-scale volumes for PLA polymer production.

Expanding Food Preservation and Pharmaceutical Applications Generating Diversified Non-PLA Lactic Acid Demand

Beyond its dominant PLA bioplastics application, lactic acid's multifunctional chemistry, encompassing natural food preservation, pH regulation, flavor enhancement, pharmaceutical excipient functionality, and biodegradable polymer synthesis for medical device and drug delivery applications, is generating structurally diversified demand across food & beverage, pharmaceutical, and personal care end-use sectors that collectively provide a robust multi-sector commercial foundation sustaining lactic acid market growth independently of bioplastics demand cycles. The U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) have both granted GRAS (Generally Recognized as Safe) and approved food additive status to lactic acid across a broad spectrum of food and beverage applications, including as an acidulant in beverages, a preservative in meat products, a pH control agent in bakery and dairy products, and a mineral bioavailability enhancer in infant nutrition formulations.

The U.S. National Institutes of Health (NIH) and pharmaceutical research literature in journals including the Journal of Controlled Release extensively document Polylactic-co-glycolic acid (PLGA), synthesized from lactic acid and glycolic acid, as one of the most clinically validated FDA-approved biodegradable polymers for controlled drug release implants and injectable microsphere depot formulations. Corbion's lactic acid derivative portfolio for pharmaceutical applications and Futerro's lactide and PLA product lines for biomedical use are expanding this high-value pharmaceutical application category at above-average revenue growth rates compared to commodity food-grade lactic acid.

Restraints - Feedstock Price Volatility and Agricultural Commodity Supply Chain Instability Impacting Fermentation-Based Production Economics

The global lactic acid market, with approximately 70% of production based on microbial fermentation of agricultural sugar and starch feedstocks is exposed to the price volatility of its primary feedstock commodities, particularly corn, sugarcane, and cassava. The U.S. Department of Agriculture (USDA)'s commodity price monitoring data document significant multi-year price swings in corn and sugarcane markets driven by weather events, geopolitical supply disruptions, biofuel demand competition, and speculative commodity trading, creating cost basis volatility for lactic acid manufacturers that reduces operating margin predictability and complicates long-term supply contract pricing. Corn price spikes of 40–60% witnessed during the 2021–2022 agricultural commodity price surge, partly attributable to the Russia-Ukraine conflict's impact on global grain markets, directly elevated production costs for Corn-based lactic acid manufacturers in North America and China, compressing margins at major producers.

Technical and Economic Challenges in Second-Generation Feedstock Scale-Up Constraining Sustainable Production Expansion

The lactic acid industry's aspiration to transition toward second-generation (2G) feedstocks, utilizing lignocellulosic agricultural waste streams including corn stover, wheat straw, sugarcane bagasse, and forestry residues as fermentation substrates, faces persistent technical and economic scale-up challenges that are limiting the near-term commercial deployment of truly circular, non-food-competitive production pathways. Lignocellulosic biomass pretreatment and enzymatic hydrolysis to release fermentable sugars involves complex and capital-intensive process steps, with enzyme costs, inhibitor compound generation during pretreatment, and lower sugar yield efficiency compared to starch or sucrose feedstocks, creating unfavorable production economics relative to first-generation corn and sugarcane-based processes at commercial scale. The U.S. Department of Energy (DOE)'s Bioenergy Technologies Office (BETO) has invested substantially in 2G biochemical conversion R&D, but commercially viable 2G lactic acid production at scale remains a 2028–2033 horizon technology for most industry participants, constraining near-term sustainable production expansion claims.

Opportunities - PLA Bioplastics Capacity Expansion and Packaging Industry Transition Creating Decade-Scale Structural Demand Growth

The ongoing global commercial scale-up of PLA bioplastics production capacity, anchored by NatureWorks LLC's commissioning of its second global PLA manufacturing facility in Thailand (with a targeted capacity of 75,000 tons per year announced in partnership with PTT Global Chemical) and TotalEnergies Corbion's Luminy® PLA production in Rayong, Thailand, is creating a decade-scale structural demand growth opportunity for lactic acid producers that positions the most competitively cost-structured and sustainably certified manufacturers for above-average revenue expansion through 2033 and beyond. Per TotalEnergies Corbion's 2025 Life Cycle Assessment of Luminy® PLA, conducted using 2024 actual production data, the bioplastic generates substantially lower carbon footprint than petrochemical alternatives, providing PLA brand owners with credible verified environmental performance data supporting commercial adoption.

The Ellen MacArthur Foundation's New Plastics Economy Initiative, which has secured commitments from over 1,000 organizations representing 20%+ of global plastic packaging production to make all plastic packaging reusable, recyclable, or compostable by 2025, represents a commercially committed demand pool for PLA packaging solutions that directly translates into structural lactic acid feedstock procurement growth. Cargill (a 50% owner of NatureWorks LLC) and Corbion are the lactic acid producers most directly positioned to capture this structural PLA capacity expansion opportunity through their existing downstream integration into the global bioplastics value chain.

Agricultural Waste-Based Lactic Acid and Circular Economy Applications Opening New High-Growth Market Segments

Peer-reviewed research published in scientific journals, including a 2025 article in PMC (PubMed Central) titled "Sustainable Lactic Acid Production from Agricultural Waste", confirms rapidly growing scientific and commercial interest in producing lactic acid from lignocellulosic agricultural residues, food processing waste streams, and municipal organic waste as circular economy feedstocks that eliminate competition with food crops, reduce production cost dependency on agricultural commodity prices, and generate carbon-negative production footprints when integrated with renewable energy systems. Cellulac Ltd., an Irish biotechnology company specializing in the conversion of dairy and food processing waste streams into lactic acid and PLA, represents an emerging business model that leverages waste valorization economics to produce competitively priced sustainable lactic acid for food-grade and bioplastics applications.

The European Union's Circular Economy Action Plan, adopted by the European Commission in March 2020 as part of the European Green Deal, explicitly identifies bio-based chemicals produced from waste feedstocks as a priority category for industrial innovation support, creating a favorable policy and funding environment for circular economy lactic acid production investments. Danimer Scientific, which develops biopolymer materials including PHA (Polyhydroxyalkanoate) compounds that can be blended with PLA for enhanced biodegradability, and Futerro (a joint venture of Galactic and Total Corbion PLA) are both investing in novel circular feedstock and advanced polymer technology platforms that represent the next generation of lactic acid value chain development.

Category-wise Analysis

By Feedstock Insights

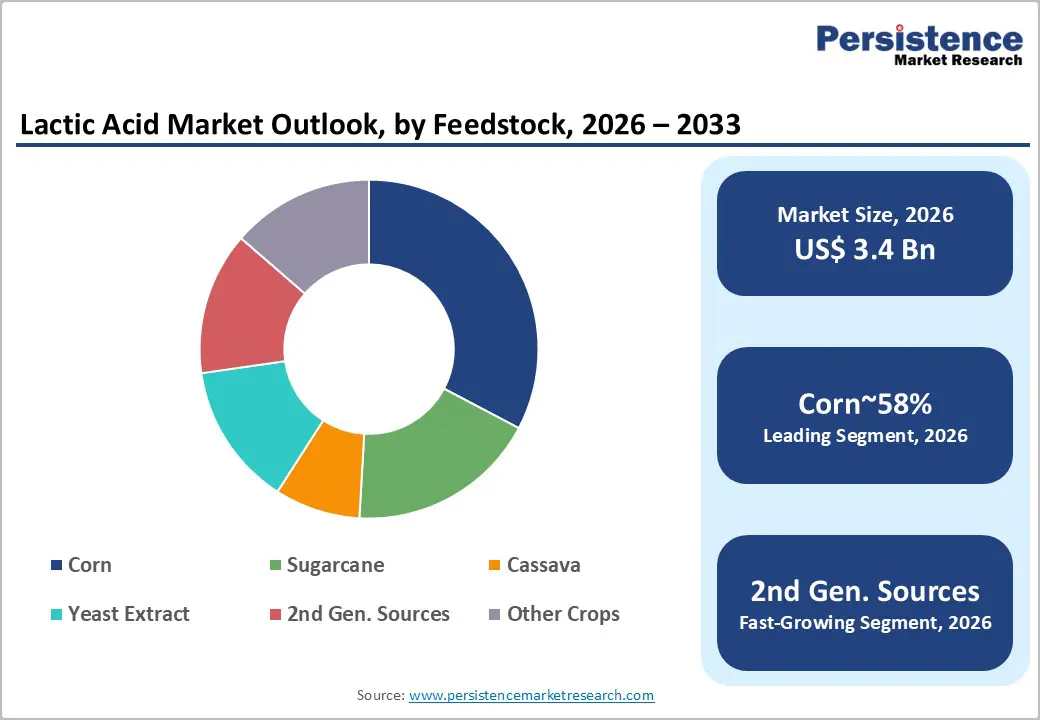

Corn leads the global Lactic Acid market by feedstock, accounting for approximately 58% of total feedstock segment revenue in 2026, a dominant position anchored in corn's global agricultural abundance, its high starch content providing efficient fermentable sugar yields per tons of processed biomass, its extensive established industrial wet-milling infrastructure in North America and China, and the cost-competitiveness of corn-derived glucose syrup as the primary fermentation substrate for the world's leading lactic acid producers. The USDA documents the United States as producing over 380 million metric tons of corn annually, with a substantial fraction processed through wet milling to produce glucose syrup for fermentation-based biochemical production including lactic acid.

Cargill, Ingredion, and Archer Daniels Midland (ADM), three of the world's largest corn wet milling companies, supply glucose feedstocks to lactic acid fermentation operations either through internal integration or long-term supply agreements with dedicated lactic acid manufacturers. Sugarcane holds the second-largest feedstock share at approximately 22%, particularly dominant in Brazil, Thailand, and India where sugarcane sucrose provides a cost-competitive fermentation substrate integrated with regional sugar industry infrastructure. Cassava is the leading feedstock in Southeast Asian production geographies, particularly Thailand and Vietnam.

By Application Insights

Biodegradable Plastics (PLA) leads the global Lactic Acid market by application, commanding approximately 38% of total application segment revenue in 2026, driven by global sustainability legislation and brand owner packaging commitments. PLA production consumes the largest single-application volume of lactic acid, with each tonne of PLA requiring approximately 1.0–1.1 tons of purified lactic acid as the primary monomer feedstock, generating direct proportional demand linkage between PLA capacity expansion and lactic acid procurement.

NatureWorks LLC's Ingeo™ biopolymer and TotalEnergies Corbion's Luminy® PLA are the world's two leading commercial PLA brands consuming the majority of global food-grade and polymerization-grade lactic acid. Food & Beverages represents the second-largest application at approximately 29% of revenue, driven by FDA GRAS and EFSA approved use of lactic acid as an acidulant, preservative, and flavor compound across beverages, dairy, bakery, and meat processing applications, with Corbion's PURAC® lactic acid serving as the globally recognized food-grade commercial standard.

By Production Method Insights

Fermentation leads the global lactic acid market by production method, commanding approximately 70% of total production method segment revenue in 2026, anchored in fermentation's sustainability credentials, renewable feedstock compatibility, lower environmental impact profile generating approximately 60% less carbon footprint than petroleum-based chemical routes, and the commercial availability of highly efficient proprietary lactic acid-producing bacterial strains including Lactobacillus species that achieve >95% theoretical yield on glucose substrates in optimized industrial fermentation processes.

Corbion's Thailand lactic acid plant, commissioned in 2024 with 125,000 tons per year capacity utilizing novel circular fermentation technology, and COFCO's Chinese corn-based fermentation facilities represent the world's two largest fermentation-based lactic acid production operations. Chemical Synthesis holds approximately 30% of production method revenue, primarily serving high-purity pharmaceutical PLGA applications where racemic DL-lactic acid produced via chemical routes meets specific pharmaceutical grade specifications, and is documented by Persistence Market Research as the fastest-growing production method segment driven by pharmaceutical PLGA demand growth.

Regional Insights

North America Lactic Acid Market Trends

North America is a leading regional market for lactic acid, anchored by the United States' position as the world's largest corn-producing country with USDA-documented annual output exceeding 380 million metric tons, its concentration of world-leading PLA bioplastics manufacturing capacity through NatureWorks LLC (partially owned by Cargill) in Blair, Nebraska, and its extensive food and pharmaceutical industry ecosystem that sustains diversified lactic acid demand across multiple high-value end-use application categories. The U.S. FDA's GRAS designation framework for food-grade lactic acid and the EPA's bio-based product procurement preference programs under the BioPreferred Program, which mandates federal agency procurement preference for bio-based products including lactic acid derivatives, create a supportive regulatory and institutional procurement environment for domestic lactic acid market growth.

Archer Daniels Midland (ADM) (headquartered in Chicago, Illinois) and Ingredion (headquartered in Westchester, Illinois) serve as critical corn wet-milling feedstock suppliers to the North American lactic acid fermentation industry, while Cargill's investment in NatureWorks LLC represents the most significant North American strategic commitment to the lactic acid-to-PLA value chain. The U.S. Inflation Reduction Act (IRA)'s advanced manufacturing production credit provisions and the U.S. Department of Energy (DOE) Bioenergy Technologies Office (BETO)'s funding for bio-based chemical innovation are generating policy tailwinds supporting domestic lactic acid and PLA industry investment through the forecast period. Danimer Scientific (headquartered in Bainbridge, Georgia) is developing next-generation biopolymer blends incorporating PLA derivatives that represent emerging premium North American lactic acid application markets.

Europe Lactic Acid Market Trends

Europe is the world's most regulatory-driven regional market for lactic acid, propelled by the EU Single-Use Plastics Directive, the European Green Deal's Circular Economy Action Plan, and the EU Bioeconomy Strategy, which collectively create the most favorable policy ecosystem globally for bio-based and biodegradable chemical demand growth. Corbion (headquartered in Amsterdam, Netherlands), the world's second-largest lactic acid producer and a global leader in food-grade and polymerization-grade lactic acid, operates its primary European lactic acid production operations while also supplying the TotalEnergies Corbion joint venture's Luminy® PLA production in Thailand. Galactic (headquartered in Brussels, Belgium) and Futerro (a Galactic-Total Corbion PLA joint venture) serve European food, pharmaceutical, and biopolymer customers with specialty lactic acid and lactide products.

Germany's chemical industry, anchored by BASF SE (headquartered in Ludwigshafen), is investing in bio-based chemical platform development that incorporates lactic acid derivatives for polymer, surfactant, and specialty chemical applications aligned with the EU Green Deal industrial transformation agenda. The European Bioplastics Association documented that European bioplastics production capacity reached approximately 1.3 million tons in 2023, with PLA representing one of the largest volume bio-based biodegradable polymer categories, generating consistent lactic acid demand growth. Evonik Industries AG (headquartered in Essen, Germany) applies pharmaceutical-grade lactic acid in its RESOMER® PLGA polymer product line, one of the world's most widely used FDA-cleared biodegradable polymer platforms for parenteral drug delivery applications, sustaining premium pharmaceutical-grade lactic acid demand in the European market.

Asia Pacific Lactic Acid Market Trends

Asia Pacific is the largest and fastest-growing regional market for lactic acid globally, anchored by China's dominant position as the world's largest lactic acid producer and consumer, Thailand's emergence as a major global lactic acid and PLA production hub following Corbion's new 125,000-tonne plant commissioning, and India's expanding food processing and pharmaceutical industry demand. China's lactic acid industry, with domestic producers including COFCO (the world's largest agricultural processing corporation by revenue), Shanxi Sanwei Group, and Musashino Chemical (China) Co., Ltd. collectively operating multi-hundred-thousand-tonne annual production capacity from corn fermentation, is the world's largest single national production and consumption geography for lactic acid, serving domestic food, pharmaceutical, and rapidly growing PLA packaging application markets. China NDRC's national plastic ban implementation and the Ministry of Ecology and Environment's biodegradable plastics standards are generating domestic PLA demand growth that directly stimulates Chinese lactic acid procurement.

Thailand has emerged as Asia Pacific's most strategically significant new lactic acid production geography, with Corbion's landmark 2024 facility commissioning in Rayong leveraging Thailand's competitive sugarcane feedstock costs and the TotalEnergies Corbion adjacent PLA polymerization operations to create an integrated lactic acid-to-PLA production ecosystem of global commercial scale. India's pharmaceutical API manufacturing industry, the world's largest by generic drug export volume, is a growing consumer of food-grade and pharmaceutical-grade lactic acid for fermentation culture media, PLGA synthesis, and pharmaceutical excipient applications, with domestic chemical companies including Cellulac Ltd.'s Indian supply chain partners serving the domestic market.

Competitive Landscape

The global Lactic Acid market is moderately consolidated at the large-scale production tier, with Corbion, NatureWorks LLC (Cargill), COFCO, and Galactic commanding leading positions through world-scale fermentation production assets, vertically integrated downstream PLA polymer operations, and decades of food-grade and polymerization-grade lactic acid technical application expertise. TotalEnergies Corbion differentiates through its integrated lactic acid-to-PLA value chain and the Luminy® PLA brand's LCA-verified sustainability credentials.

BASF SE and Evonik compete in premium pharmaceutical PLGA segments. Emerging business model trends include waste-to-lactic acid circular production (Cellulac), 2G feedstock fermentation R&D investments (Futerro, Danimer Scientific), and long-term strategic supply agreements with major CPG brand PLA packaging commitments. China's COFCO and Shanxi Sanwei Group compete on volume-driven cost efficiency serving domestic food and industrial markets.

Key Market Developments:

- In February 2025, Corbion announced successful commissioning and ramp-up of its 125,000-tonne per year lactic acid plant in Rayong, Thailand, the world's largest single-site lactic acid facility leveraging novel circular production technology with industry-leading low emissions profile per its 2025 Life Cycle Assessment publication.

- In October 2024, TotalEnergies Corbion published a comprehensive independently verified Life Cycle Assessment (LCA) of Luminy® PLA using 2024 actual production data, confirming its substantially lower carbon footprint versus conventional petroleum plastics and providing brand owner customers with verified environmental performance documentation supporting commercial PLA adoption commitments.

- In June 2024, NatureWorks LLC progressed engineering and permitting for its second global PLA manufacturing facility in Thailand in partnership with PTT Global Chemical, targeting a production capacity of approximately 75,000 tons per year to serve rapidly growing Asia Pacific and global PLA bioplastics packaging demand from the region's most cost-competitive feedstock location.

Companies Covered in Lactic Acid Market

- NatureWorks LLC

- TotalEnergies Corbion

- BASF SE

- Galactic

- Corbion

- Futerro

- COFCO

- Musashino Chemical (China) Co., Ltd.

- Danimer Scientific

- Cellulac Ltd.

- Evonik

- Shanxi Sanwei Group

- Cargill

- Ingredion

- Archer Daniels Midland

Frequently Asked Questions

The global Lactic Acid market is estimated to be valued at US$ 3.4 Billion in 2026 and is projected to reach US$ 6.3 Billion by 2033, registering a forecast CAGR of 9.3% from 2026 to 2033. The market recorded a historical CAGR of 8.2% between 2020 and 2025, driven by PLA bioplastics capacity expansion, escalating plastic ban legislation across EU and China, and diversified food, pharmaceutical, and personal care application demand growth.

The key drivers are the EU Single-Use Plastics Directive and China NDRC's national plastic ban policy driving commercial PLA bioplastics adoption, with PLA generating 68% fewer GHG emissions versus petroleum plastics, and Corbion's commissioning of the world's largest 125,000-tpa lactic acid facility in Thailand in 2024 confirming industry confidence in structural demand growth, supported by expanding food preservation and pharmaceutical PLGA applications adding diversified non-bioplastics demand across the forecast period.

Corn leads the Feedstock segment with approximately 58% revenue share in 2026, anchored by the USDA's documented 380+ million tonne U.S. annual corn output providing abundant fermentable glucose, the established industrial wet-milling infrastructure of Cargill, Ingredion, and ADM, and corn's superior starch content delivering high fermentation sugar yields. Sugarcane holds second position at approximately 22%, particularly dominant in Thailand, Brazil, and India integrated with regional sugar industry infrastructure.

Asia Pacific leads the global Lactic Acid market in volume, anchored by COFCO's world-scale corn fermentation operations across China, Corbion's landmark 125,000-tpa Thailand facility commissioned in 2024, China NDRC's biodegradable plastics mandate driving domestic PLA demand, and NatureWorks LLC's second PLA production facility under development in Thailand with PTT Global Chemical, collectively confirming the region's dominant and accelerating commercial leadership.

The most significant opportunity is PLA bioplastics capacity expansion and circular waste-to-lactic acid production, with the Ellen MacArthur Foundation's 1,000+ brand compostable packaging commitments, EU Circular Economy Action Plan supporting waste-derived bio-based chemical investment, and Cellulac Ltd.'s food waste fermentation platform and Futerro's advanced lactide technology collectively positioning next-generation circular lactic acid producers for premium margin capture in the rapidly growing sustainable packaging and biopolymer value chain.

The leading companies include Corbion (PURAC®, Amsterdam), NatureWorks LLC (Ingeo™, Plymouth USA), TotalEnergies Corbion (Luminy® PLA, Rayong Thailand), COFCO (Beijing), Galactic (Brussels), Futerro, BASF SE (Ludwigshafen), Evonik Industries AG (RESOMER®, Essen), Shanxi Sanwei Group, Musashino Chemical (China) Co., Ltd., Cargill, Ingredion, Archer Daniels Midland, Danimer Scientific, and Cellulac Ltd., spanning the global spectrum of fermentation producers, downstream PLA manufacturers, and specialty pharmaceutical lactic acid derivative suppliers.