- Non-food Packaging

- Jumbo Bags Market

Jumbo Bags Market Size, Share, and Growth Forecast, 2026 - 2033

Jumbo Bags Market By Bag Type (Type A, Type D, Others), Capacity (750-1500 kg, Above 1500 kg, Others), Application, and Regional Analysis for 2026 - 2033

Jumbo Bags Market Size and Trends Analysis

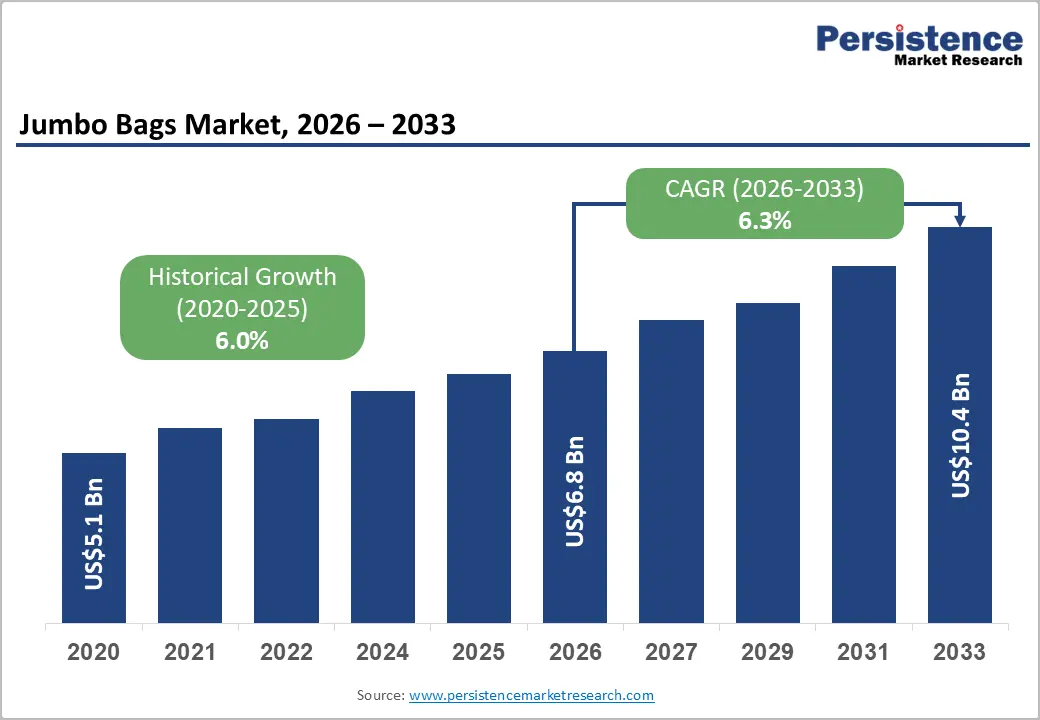

The global jumbo bags market size is likely to be valued at US$6.8 billion in 2026 and is expected to reach US$10.4 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033, driven by rising bulk-handling requirements across chemicals, agriculture, and construction industries, alongside a gradual shift away from rigid and single-use packaging formats.

Capacity additions in the Asia Pacific strengthen global supply availability, while evolving safety and quality standards influence purchasing decisions. Volatility in polypropylene resin pricing and ongoing regulatory updates continue to shape cost structures and product specifications. Overall, the market remains attractive for manufacturers prioritizing sustainable materials, UN-certified solutions for hazardous goods, and regionally optimized low-cost production models.

Key Industry Highlights

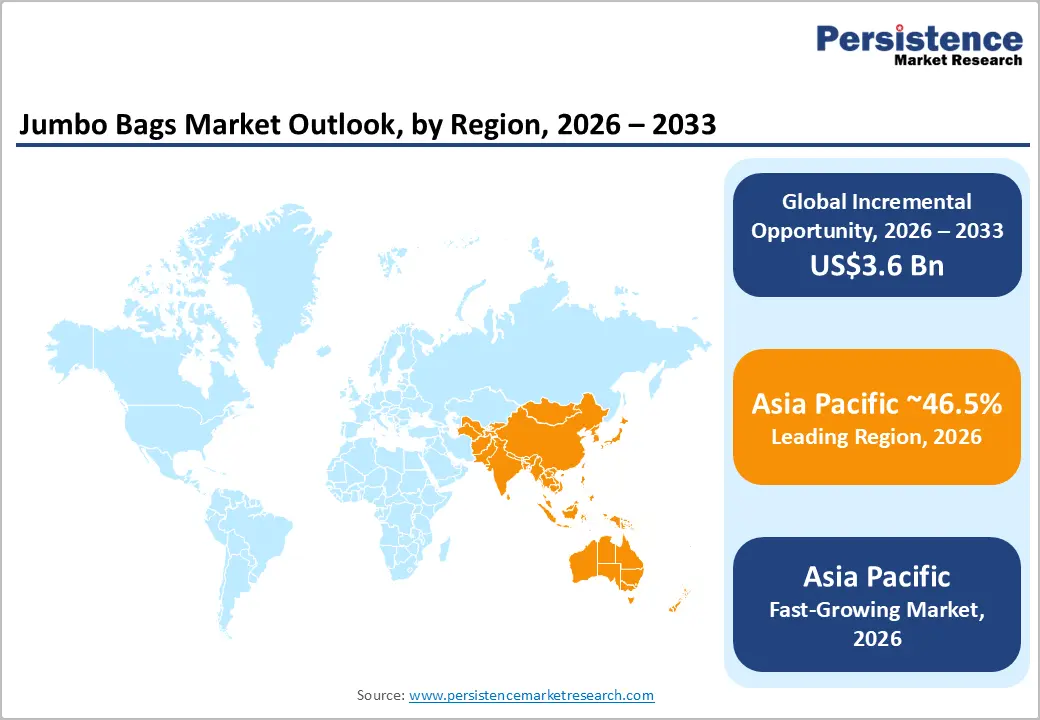

- Leading Region: Asia Pacific leads the market with a 46.5% market share, supported by large-scale manufacturing capacity, cost-competitive production, and strong export orientation across China, India, and ASEAN economies.

- Fastest-growing Region: Asia Pacific is also the fastest-growing regional market, driven by rising infrastructure development, expanding chemical and agricultural exports, and increasing adoption of UN-certified jumbo bags for international trade.

- Investment Plans: Manufacturers are prioritizing investments in certified production lines, automated weaving and cutting systems, anti-static fabric technologies, and integration of recycled polypropylene, particularly to meet export-market safety and sustainability requirements.

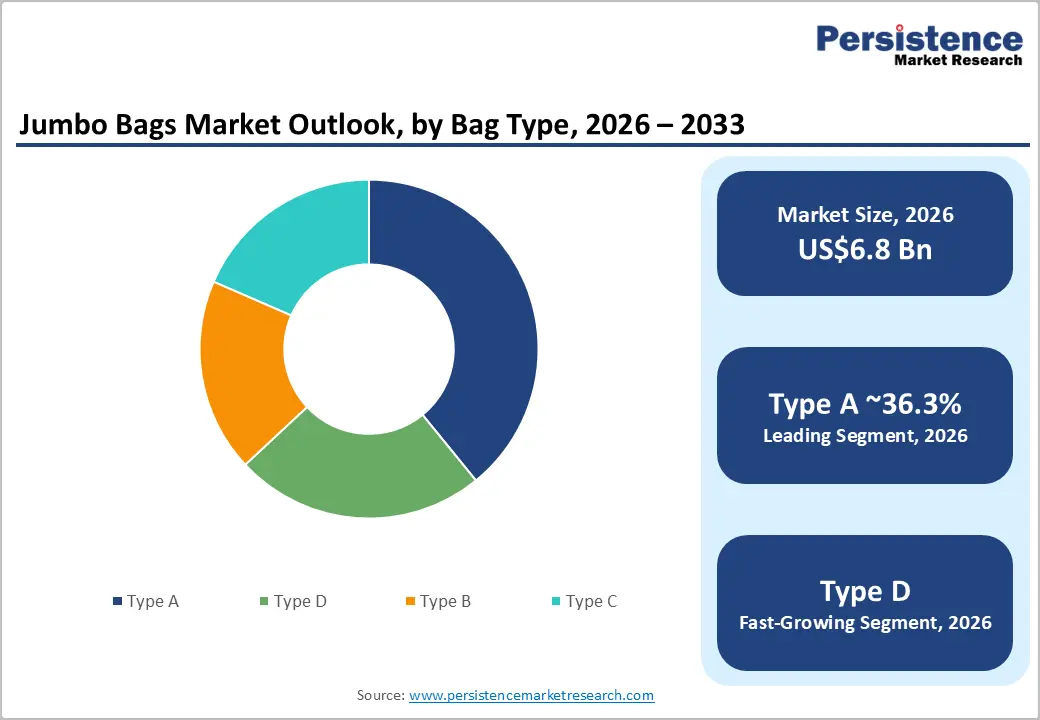

- Dominant Bag Type: Type A jumbo bags are estimated to dominate the market with a 36.3% share, reflecting widespread use in non-hazardous bulk materials across construction, agriculture, and basic industrial applications.

- Leading Application: Building and construction is expected to remain the largest end-use segment, accounting for 38.4% of the market, driven by sustained demand for cement, aggregates, and dry construction materials in infrastructure projects.

| Key Insights | Details |

|---|---|

| Jumbo Bags Market Size (2026E) | US$6.8 Bn |

| Market Value Forecast (2033F) | US$10.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Manufacturing and Commodity Trade Growth in the Asia Pacific

Rapid industrialization and export-oriented manufacturing growth across China, India, and ASEAN economies have significantly increased bulk shipments of cement, fertilizers, minerals, and industrial intermediates. These materials are typically transported and stored using jumbo bags due to their cost efficiency and handling advantages. Asia Pacific has emerged as the largest regional contributor to global jumbo bag demand, accounting for approximately 46.5% of total volume, reflecting strong domestic consumption and export activity. This regional concentration sustains high-volume demand for standard Type A bags while accelerating adoption of UN-certified and higher-specification variants for international trade. As infrastructure investment and industrial output expand, the Asia Pacific continues to underpin global volume growth.

End-use Expansion in Chemicals, Food, and Agriculture

The chemicals, fertilizers, and food-ingredient sectors are scaling bulk logistics operations to support increasing production and cross-border trade. Jumbo bags offer advantages in handling efficiency, contamination control, and cost per unit transported, making them the preferred packaging format for these industries. Chemicals and fertilizers represent consistent high-volume demand, while food and agriculture increasingly require liner-equipped and food-grade certified bags. This combination of volume stability and specification upgrades supports mid- to high-single-digit growth rates in jumbo bag consumption, reinforcing long-term demand visibility for manufacturers serving these end-use sectors.

Regulatory and Standards Tightening

Updates to flexible intermediate bulk container standards, including revisions to ISO 21898 and stricter enforcement of UN certification for hazardous materials, are raising minimum safety and performance requirements. Manufacturers must invest in improved raw materials, testing protocols, and traceability systems to remain compliant. While this increases production complexity, it also creates opportunities for differentiation for certified suppliers. Demand for higher-value bag types, including Type C and Type D jumbo bags, is accelerating as customers prioritize operational safety, regulatory compliance, and risk mitigation in bulk material handling.

Barrier Analysis - Raw Material Price Volatility

Polypropylene and polymer additives account for a significant share of the costs of jumbo bag production. Global resin price volatility, driven by fluctuations in crude oil prices, energy costs, and supply chain disruptions, directly impacts manufacturer margins. Smaller producers face working capital constraints and limited ability to hedge raw material exposure. Industry analysis indicates that a sustained 10-15% increase in polypropylene resin prices can reduce gross margins by several percentage points, delaying capital investment in automation and quality upgrades. This volatility introduces pricing uncertainty and heightens competitive pressure in commodity-grade segments.

Standards and Logistics Fragmentation

Variations in national interpretations of UN packaging rules and inconsistent enforcement of ISO and regional standards increase compliance costs for manufacturers operating across borders. Export-oriented suppliers often need to maintain multiple certifications and documentation systems, raising unit costs and extending product development timelines. For small and mid-sized exporters, this regulatory fragmentation raises the break-even volume required to justify investment in certified production lines. As a result, compliance complexity can limit market entry and slow innovation, particularly for high-value jumbo bag formats.

Opportunity Analysis - Sustainable and Recycled-Content Jumbo Bags

Packaging waste regulations and corporate sustainability commitments are driving demand for jumbo bags made with recycled polypropylene or alternative fiber blends. Buyers increasingly require documented recycled content, traceability, and compliance with food-contact and safety standards. Manufacturers that invest in validated recycled-material supply chains can secure premium contracts, particularly in Europe and North America. Industry assessments suggest that sustainable jumbo bags could account for a low double-digit share of incremental market value over the next five to seven years, offering a meaningful growth avenue beyond commodity segments.

Product Premiumization for High-Value End-Uses

UN-certified jumbo bags, conductive and anti-static Type C and Type D variants, and multi-layer liner systems for food and pharmaceutical applications command significantly higher average selling prices. Suppliers that provide engineering support, customized spout designs, integrated liners, and traceability solutions can secure long-term supply agreements. Premium product lines can achieve ASPs 20-60% higher than standard Type A bags, enabling margin expansion even during periods of elevated raw material costs. This trend favors manufacturers with strong technical and quality assurance capabilities.

Category-wise Analysis

Bag Type Insights

Type A Jumbo Bags are anticipated to maintain 36.3% share, with their market leadership anticipated to remain stable over the forecast period due to their broad applicability in non-hazardous bulk materials. Their low unit cost, simple woven polypropylene construction, and ease of handling make them the preferred packaging solution for cement, sand, grains, and mineral products. Large-scale users in construction and agriculture favor Type A bags as they integrate seamlessly into automated filling and palletization systems.

For example, cement producers and grain exporters across Asia Pacific and the Middle East rely heavily on Type A bags to support high-throughput logistics. Manufacturers continue to prioritize capacity expansion for this category to achieve economies of scale, reinforcing price competitiveness and sustaining their leadership position.

Type D jumbo bags represent the fastest-growing bag type, with demand accelerating due to rising safety requirements for handling flammable, combustible, and electrostatically sensitive powders. Growth is especially pronounced in specialty chemicals, lithium-ion battery materials, pigments, and pharmaceutical intermediates, where electrostatic discharge risks are tightly regulated. For instance, chemical manufacturers in Europe and North America are increasingly shifting from Type C to Type D bags to reduce dependence on grounding and operational complexity.

Ongoing investments in certified anti-static yarns and conductive fabric technologies enable suppliers to offer higher-value solutions, supporting premium pricing and stronger margins. As regulatory scrutiny intensifies, Type D bags are expected to gain further traction in high-risk industrial environments.

Application Insights

The building and construction sector is expected to account for the largest share of the jumbo bags market, at approximately 38.4% of total demand. This dominance is driven by ongoing consumption of cement, aggregates, fly ash, and dry mortars. Jumbo bags are widely preferred in large-scale infrastructure and commercial projects due to their high load-bearing strength, ease of stacking, and ability to minimize material loss. Infrastructure programs in emerging economies, including road, housing, and industrial corridor developments, continue to drive bulk material movement.

For example, contractors across India and Southeast Asia increasingly prefer jumbo bags over traditional sacks to improve site efficiency and reduce labor handling costs. Long-term supply contracts and standardized specifications further support repeat procurement and volume stability in this segment.

Food products and agriculture represent the fastest-growing end-use segment, supported by expanding global trade in bulk grains, oilseeds, sugar, and processed food ingredients. Growth is driven by stricter food safety regulations and the increasing use of food-grade liners, UV-stabilized fabrics, and laminated jumbo bags to preserve product quality during storage and transit. Grain exporters in North America and Eastern Europe, for instance, are adopting liner-fitted jumbo bags to meet hygiene and traceability standards required by international buyers.

Rising demand for value-added agricultural exports is also increasing average unit selling prices, thereby encouraging manufacturers to develop specialized, compliance-focused solutions for this segment.

Regional Insights

North America Jumbo Bags Market Trends - Compliance-Driven Demand for UN-Certified, High-Reliability Bulk Packaging

North America represents a mature, value-driven jumbo bags market, where purchasing decisions are guided less by unit cost and more by regulatory compliance, operational reliability, and supply assurance. The U.S. accounts for the majority of regional consumption, driven by sustained demand from the chemicals, mining, agriculture, and construction sectors. Large-scale industrial users prioritize UN-certified packaging, traceability systems, and consistent tensile performance, which supports higher average selling prices compared to global averages. This environment favors established suppliers with integrated testing, certification, and quality-control infrastructure.

Regional market dynamics are strongly influenced by investments in automation and safety compliance. Leading packaging groups such as Greif and Berry Global have expanded their bulk packaging portfolios in North America through automation upgrades and advanced material handling capabilities, improving throughput consistency and labor efficiency. These investments align with tighter Occupational Safety and Health Administration (OSHA) requirements and hazardous material handling regulations, particularly for chemicals and mineral powders. Mining operators in the U.S. and Canada increasingly specify anti-static and reinforced jumbo bags to reduce workplace risk and material loss.

Sustainability initiatives are also reshaping procurement behavior. North American buyers are gradually incorporating recycled polypropylene content and reconditioning programs, driven by corporate ESG commitments rather than regulatory mandates. Companies such as LC Packaging, with established reuse and recycling programs, are gaining traction among agricultural exporters and specialty chemical producers. As supplier consolidation continues, scale advantages and compliance capabilities are reinforcing the dominance of multinational manufacturers, while smaller regional players increasingly operate as niche or contract suppliers.

Europe Jumbo Bags Market Trends - Regulation-led Circularity and Technical Differentiation in Jumbo Bags

Europe is a regulation-intensive and compliance-led market, where jumbo bag demand is shaped by harmonized safety standards, circular economy policies, and sustainability mandates. Germany and the U.K. anchor regional demand through their strong chemical manufacturing, industrial processing, and agricultural export bases, while France and Spain contribute significantly through construction materials and food-grade bulk packaging. Buyers across the region consistently require UN certification, food-contact compliance, and documented lifecycle traceability, increasing the technical complexity and value of jumbo bags sold.

The European regulatory framework actively encourages reuse, reconditioning, and recycled-content integration, creating favorable conditions for circular business models. Industry leaders such as LC Packaging and FlexSack have expanded reconditioning and closed-loop recycling initiatives across Western Europe, allowing end users to reduce packaging waste while maintaining compliance with safety standards. These programs are particularly relevant for agricultural cooperatives and chemical distributors operating under Extended Producer Responsibility (EPR) regimes.

Investment trends across Europe prioritize testing infrastructure, material innovation, and certification readiness. Manufacturers increasingly allocate capital toward in-house laboratories, electrostatic discharge testing, and food-grade liner development to meet evolving EU standards. As a result, competition is less price-driven and more focused on technical differentiation and compliance depth. This regulatory alignment supports stable long-term demand but raises entry barriers, reinforcing the position of established, compliance-capable suppliers.

Asia Pacific Jumbo Bags Market Trends - Export-Oriented Manufacturing Scale with Rising Global Compliance Alignment

Asia Pacific is projected to lead the market with 46.5% share in 2026, reflecting its role as the world’s primary manufacturing and export hub for bulk packaging. The region benefits from competitive production costs, abundant raw material availability, and proximity to high-growth end-use industries. China dominates both production capacity and domestic consumption, supported by its extensive chemical, construction, and mineral processing industries.

India has also emerged as a critical exporter, supplying jumbo bags to North America, Europe, and the Middle East. Indian manufacturers such as Umasree Texplast, Rishi FIBC, and Big Bags International have expanded certified production lines and invested in UN-approved testing to meet export-market requirements. These upgrades are directly linked to the rising demand from global chemical and food customers seeking cost-efficient yet compliant sourcing alternatives. ASEAN economies, including Vietnam and Indonesia, contribute through mining and agricultural exports, where jumbo bags are essential for bulk commodity logistics.

While regulatory enforcement varies across the region, export-driven quality convergence is accelerating. Suppliers serving international markets increasingly align with European and North American standards, investing in food-grade liners, anti-static fabrics, and traceability systems. This transition is gradually lifting regional average selling prices and shifting competition toward quality and reliability rather than pure cost leadership. As infrastructure and industrial activity expand, Asia Pacific is expected to remain both the largest and fastest-growing regional market, underpinned by manufacturing scale and evolving compliance expectations.

Competitive Landscape

The global jumbo bags market is moderately fragmented, combining global packaging groups with numerous regional manufacturers. Large players leverage multi-plant networks and value-added services, while local suppliers dominate commodity volumes. Consolidation is more pronounced in North America and Europe, particularly in certified and premium segments, whereas Asia Pacific remains fragmented but scale-driven.

Leading strategies include product premiumization, regional cost leadership, and sustainability-driven differentiation. Competitive advantage increasingly depends on certification capability, supply reliability, and bundled technical services.

Key Industry Developments

- In April 2025, Gravis introduced its Sustainabulk 100% recycled FIBC bulk bags, reflecting a stronger industry focus on sustainability and circular-economy packaging solutions for bulk transport applications. These bags provide a lower-carbon alternative while maintaining strength and performance.

- In February 2025, United Bags, Inc. completed the acquisition of BAG Corp, expanding its FIBC product offerings and broadening its presence in the global bulk packaging market. This strategic move enhances distribution capabilities and supports a wider range of jumbo bag solutions across chemicals, agriculture, and construction sectors.

Companies Covered in Jumbo Bags Market

- Umasree Texplast

- Rishi FIBC Solutions

- Big Bags International

- LC Packaging

- Greif

- Berry Global

- FlexSack

- Conitex Sonoco

- Taihua Group

- Yixing Huafu Plastic

- Jumbo Bag Limited

- Sackmaker J&HM Dickson

- Intertape Polymer Group

- Emmbi Industries

- Gopala Polyplast

- BAG Corp

- Palmetto Industries

- Kanpur Plastipack

Frequently Asked Questions

The global jumbo bags market is likely to be valued at US$6.8 billion in 2026.

By 2033, the jumbo bags market is expected to reach US$10.4 billion.

Key trends include premiumization toward UN-certified and Type D jumbo bags, rising adoption of food-grade liners and laminated fabrics, growing focus on sustainable and recycled polypropylene materials, and increasing automation and quality testing investments by manufacturers.

By bag type, Type A jumbo bags remain the leading segment due to their cost efficiency and wide applicability in non-hazardous bulk materials. By end-use, the building and construction segment dominates the market, accounting for 38.4% of the market share, primarily for cement, aggregates, and construction inputs.

The jumbo bags market is projected to grow at a CAGR of 6.3% between 2026 and 2033.

Major players include Greif, LC Packaging, Rishi FIBC Solutions, Berry Global, and Conitex Sonoco.