- Food Packaging

- Japan Disposable Cutlery Market

Japan Disposable Cutlery Market Size, Share, and Growth Forecast, 2026 - 2033

Japan Disposable Cutlery Market by Product Type (Spoon, Knife, Others), Cutlery Type (Wrapped Cutlery, Dispensed Cutlery, Others), Fabrication Process, End-user, and Zone Analysis for 2026 - 2033

Japan Disposable Cutlery Market Size and Trends Analysis

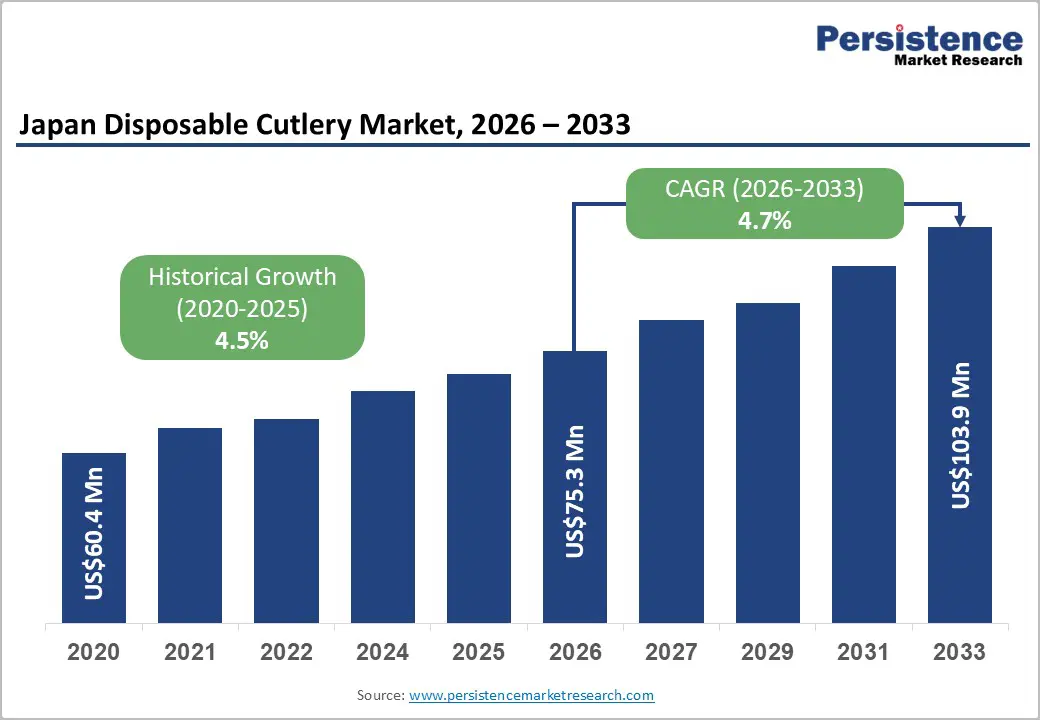

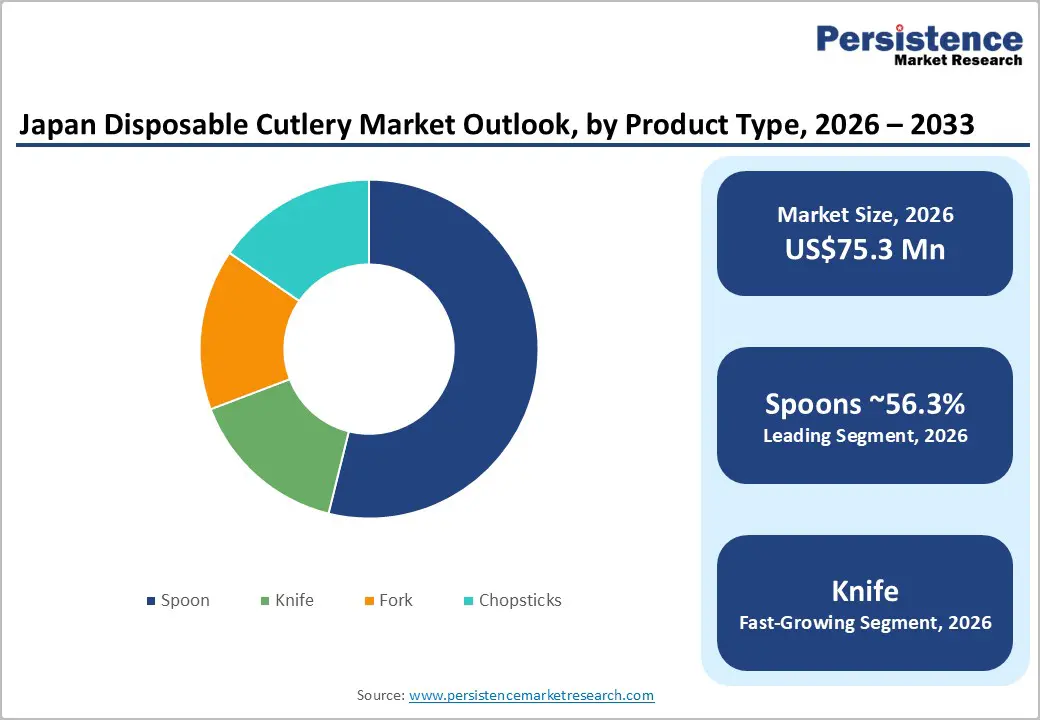

The Japan disposable cutlery market size is likely to be valued at approximately US$75.3 million in 2026 and is expected to reach around US$103.9 million by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by rising urbanization, a strong convenience-store culture, and high consumption of ready-to-eat meals.

A major growth driver is the sustained expansion of food delivery and takeaway services, driven by changing lifestyles, long working hours, and increasing reliance on quick-service restaurants. The Japanese disposable cutlery market comprises single-use forks, spoons, knives, and chopsticks made from plastic, paper, wood, and biodegradable materials, catering primarily to foodservice outlets, takeaway chains, convenience stores, and home-delivery platforms. The market operates within a highly structured retail and foodservice ecosystem, in which hygiene, convenience, and packaging efficiency play critical roles in purchasing decisions.

Key Industry Highlights:

- Investment Plans: Focus on biodegradable and plant-based cutlery production facilities, automation of wrapped and dispensed cutlery manufacturing, and partnerships with convenience store chains to expand distribution.

- Dominant Product Type: Spoons are expected to account for 56.3% of revenue, with the highest usage in soups, desserts, and ready-to-eat meals, supporting stable demand across foodservice and takeaway channels.

- Leading Cutlery Type: Wrapped cutlery is estimated to account 54.6% revenue share, preferred for hygiene and contamination prevention in food delivery and takeaway services, maintaining strong adoption among restaurants and convenience stores.

| Key Insights | Details |

|---|---|

| Japan Disposable Cutlery Market Size (2026E) | US$75.3 Mn |

| Market Value Forecast (2033F) | US$103.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Sustainability-Driven Innovation in Eco-Friendly Cutlery

Regulatory pressure combined with Japan’s strong sustainability culture is reshaping demand patterns in the disposable cutlery market. The Plastic Resource Circulation Act, along with voluntary reduction targets adopted by major foodservice operators, is accelerating the replacement of conventional plastic cutlery with biodegradable disposable cutlery, wooden single-use utensils, and bagasse-based cutlery solutions. Unlike the generic sustainability shifts observed globally, Japan’s market emphasizes product functionality alongside environmental compliance, prompting manufacturers to develop moisture-resistant compostable cutlery suitable for soups, bento meals, and convenience foods. This has led to the acceptance of premium pricing among restaurants and retailers, who view eco-friendly cutlery as a brand-differentiation tool rather than a cost burden.

Growth of Urban Food Delivery Culture and Hygienic Convenience Demand

Urban lifestyle dynamics and Japan’s highly developed convenience food ecosystem further reinforce market growth. The dominance of konbini (convenience store) meal consumption, coupled with rising demand for food-delivery packaging, has increased the need for lightweight, hygienic, and standardized disposable cutlery formats. Long working hours and smaller household sizes sustain high consumption of ready-to-eat meals, making single-use cutlery for takeaway and home delivery a necessity rather than an option. For example, leading convenience chains have expanded the use of plant-based disposable cutlery across private-label meal offerings, aligning hygiene expectations with national waste-reduction goals while maintaining operational efficiency.

Barrier Analysis - Functional Limitations of Compostable Cutlery for Hot and Oily Foods

Product performance expectations within Japan’s foodservice sector impose a structural barrier to the adoption of disposable cutlery, particularly non-plastic alternatives. Many biodegradable disposable cutlery and plant-based single-use utensils struggle to meet the functional demands of Japanese cuisine, which frequently involves hot broths, oily foods, and heavier meal portions such as ramen, udon, and rice bowls. Inconsistent heat resistance and structural rigidity of compostable cutlery can lead to bending or breakage during use, affecting customer experience and discouraging repeat procurement by quick-service restaurants and convenience stores that rely on operational consistency.

Rising Adoption of Reusable Cutlery Reducing Per-Capita Usage

Evolving consumer behavior is also reshaping demand dynamics for single-use utensils across urban Japan. A growing segment of environmentally conscious consumers and corporate cafeterias is favoring reusable personal cutlery sets and hybrid semi-durable utensils, particularly in office districts and university campuses. This shift reduces per-capita consumption of disposable cutlery for takeaway meals, especially in controlled environments where reuse is practical. As sustainability awareness deepens, the discretionary use of single-use cutlery is increasingly avoided in favor of low-waste alternatives, thereby limiting volume growth beyond core food delivery and convenience store applications.

Opportunity Analysis - Application-Specific Cutlery for Japanese Cuisine Formats

Innovation focused on functionality tailored to Japanese eating habits creates a strong growth pathway for the disposable cutlery market. There is a rising demand for heat-resistant disposable cutlery for ramen and soup-based meals, oil-tolerant single-use utensils for fried and bento foods, and chopstick-spoon hybrid disposable formats that align with local dining preferences. Foodservice operators increasingly seek differentiated cutlery that enhances meal usability and presentation rather than treating it as a low-value accessory. This opens opportunities for manufacturers to introduce application-specific disposable cutlery designed for convenience stores, delivery platforms, and quick-service restaurants with standardized menus.

Seasonal, Branded, and Event-Driven Cutlery Premiumization

Japan’s event-centric consumption culture also offers a distinct opportunity through customized and seasonally themed disposable cutlery. Demand is increasing for festival-specific single-use utensils, branded disposable cutlery for corporate catering, and private-label cutlery solutions for convenience chains, in which aesthetics and cultural relevance influence purchasing decisions. Short product life cycles and limited-edition designs allow suppliers to command higher margins while strengthening partnerships with foodservice clients. For example, disposable cutlery customized for seasonal festivals and promotional food campaigns has gained traction among large convenience store operators, supporting repeat orders and long-term supply agreements.

Category-wise Analysis

Product Type Insights

Within the Japan disposable cutlery market, spoons are expected to represent the largest product segment, accounting for an anticipated 56.3% market share in the mid-forecast period. Their leadership is driven by unmatched versatility across Japan’s dominant meal formats, including soups, rice bowls, desserts, and convenience-store-ready meals. Spoons are routinely included with bento boxes, noodle dishes, and delivery meals, making them a default utensil across foodservice and retail channels. Their consistent compatibility with multiple materials, plastic, wooden, and compostable alternatives, also allows foodservice operators to transition toward sustainable options without disrupting usage patterns, reinforcing sustained volume demand.

Knives are emerging as the fastest-growing product segment, supported by changes in menu composition and dining formats. Growth is tied to the expansion of Western and fusion cuisines, premium convenience meals, and delivery-based casual dining, all of which increasingly feature grilled meats, sandwiches, and cut-style foods. Foodservice operators are placing greater emphasis on functional disposable knives with improved cutting strength, particularly those made from injection-molded materials or reinforced biodegradable materials.

As consumer expectations for the dining experience rise, disposable knives are evolving from optional add-ons to essential inclusions for specific meal categories. A relevant example is the increased use of disposable knives with reinforced blades in the delivery of meals featuring grilled proteins sold through urban convenience stores and cloud kitchens.

Cutlery Type Insights

Wrapped cutlery is expected to hold the leading position, with an estimated 54.6% market share in 2026. Individually wrapped utensils align strongly with Japan’s high hygiene standards, particularly in food delivery, takeaway, and convenience-store environments, where multiple handling points are common. Wrapped formats reduce contamination concerns during transportation and storage and support brand presentation through printed sleeves. Their dominance is reinforced by consumer preference for visible cleanliness and consistency, making wrapped cutlery the standard choice for large foodservice chains and delivery platforms.

Dispensed cutlery is the fastest-growing cutlery format, driven by the rapid adoption of self-service and semi-automated foodservice models. Restaurants, cafeterias, and convenience outlets are increasingly deploying sanitized dispenser systems that allow customers to take utensils on demand, reducing unnecessary distribution and material waste. This model supports operational efficiency while aligning with sustainability initiatives aimed at minimizing excess packaging. An example is urban quick-service outlets that combine kiosk ordering with dispensing biodegradable cutlery, enabling hygiene control while reducing per-meal packaging.

Competitive Landscape

The Japan disposable cutlery market is moderately fragmented, with a mix of domestic manufacturers, packaging specialists, and global disposable tableware suppliers competing across price, material innovation, and supply reliability. Local players maintain a strong presence due to their deep understanding of Japanese foodservice requirements, quality standards, and distribution networks, particularly within convenience stores and catering channels. Competition is increasingly shaped by the ability to offer application-specific cutlery, such as heat-resistant spoons or reinforced disposable knives, while meeting evolving sustainability expectations without compromising performance.

Strategic differentiation in the market centers on material innovation, private-label manufacturing, and long-term supply contracts with foodservice chains and convenience retailers. Leading companies are expanding portfolios of biodegradable and compostable cutlery, investing in improved strength and usability to address functional gaps of eco-friendly alternatives. Partnerships with quick-service restaurants, cloud kitchens, and large retailers play a critical role in securing volume stability, while customization, seasonal branding, and efficient logistics are emerging as key competitive levers in Japan’s demand-driven and quality-focused market environment.

Key Industry Developments:

- In February 2025, FamilyMart commercialized Kaneka’s plant-based, biodegradable polymer Green Planet™ for eco-friendly disposable spoons and forks, rolling it out across 16,500 stores nationwide as part of its “BLUE GREEN” sustainability initiative to reduce plastic waste.

Companies Covered in Japan Disposable Cutlery Market

- Daiwa Can Company

- Toyo Aluminium Group

- Nippon Paper Industries

- Huhtamaki Oyj

- Dart Container Corporation

- Duni Group

- Genpak Co., Ltd.

- Showa Denko Packaging

- Eco-Products Co., Ltd.

- Tairyu Co., Ltd.

Frequently Asked Questions

The Japan disposable cutlery market is estimated to be valued at US$75.3 million in 2026.

By 2033, the Japan disposable cutlerymarket is expected to reach around US$100-104 million.

Key trends include rising adoption of biodegradable and plant-based disposable cutlery, increasing use of wrapped cutlery for hygiene assurance, growth of dispensed cutlery systems in self-service environments, and demand for application-specific utensils designed for soups, bento meals, and delivery-focused menus.

By product type, spoons represent the leading segment, accounting for 56.3% of market share, due to their versatility across Japanese meal formats such as soups, rice bowls, desserts, and ready-to-eat convenience foods.

The market is projected to grow at a CAGR of approximately 4.7% between 2026 and 2033.

Major players include Daiwa Can Company, Toyo Aluminium Group, Nippon Paper Industries (Food & Packaging Division), Huhtamaki Oyj, and Dart Container Corporation.