- Healthcare Services

- Infection Surveillance Solutions Market

Infection Surveillance Solutions Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Infection Surveillance Solutions Market by Component (Software, Services), Deployment Mode (On-Premise, Web-Based) End-user (Hospitals, Clinics, Long Term Care Facilities, Specialty Centers, Others) and Regional Analysis from 2026 to 2033

Infection Surveillance Solutions Market Share and Trends Analysis

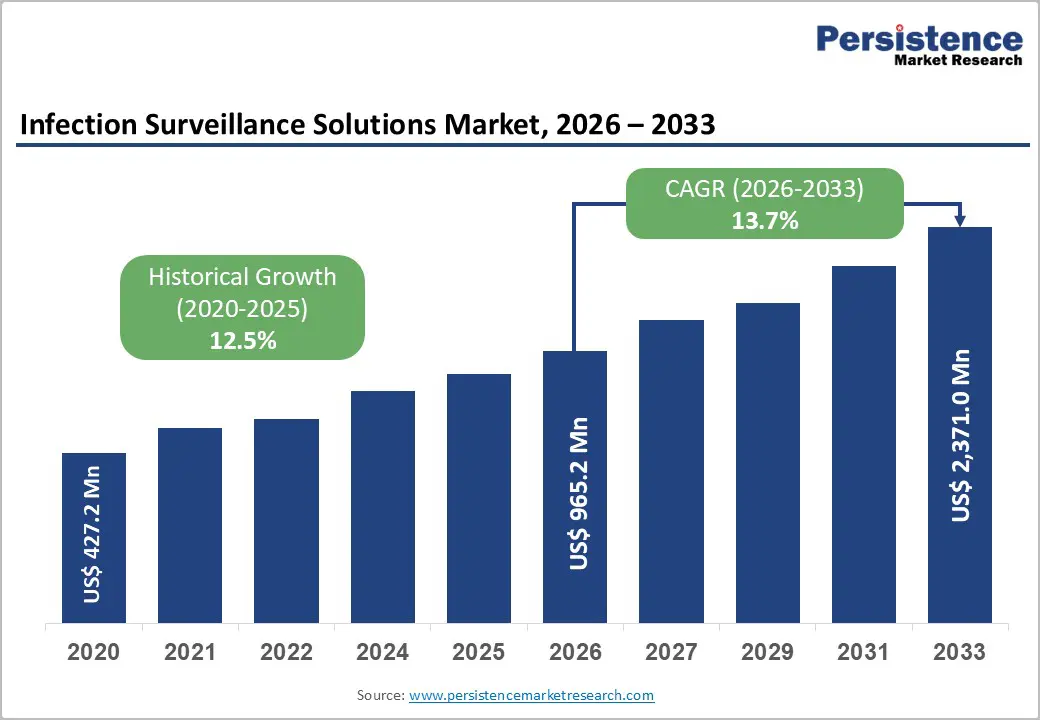

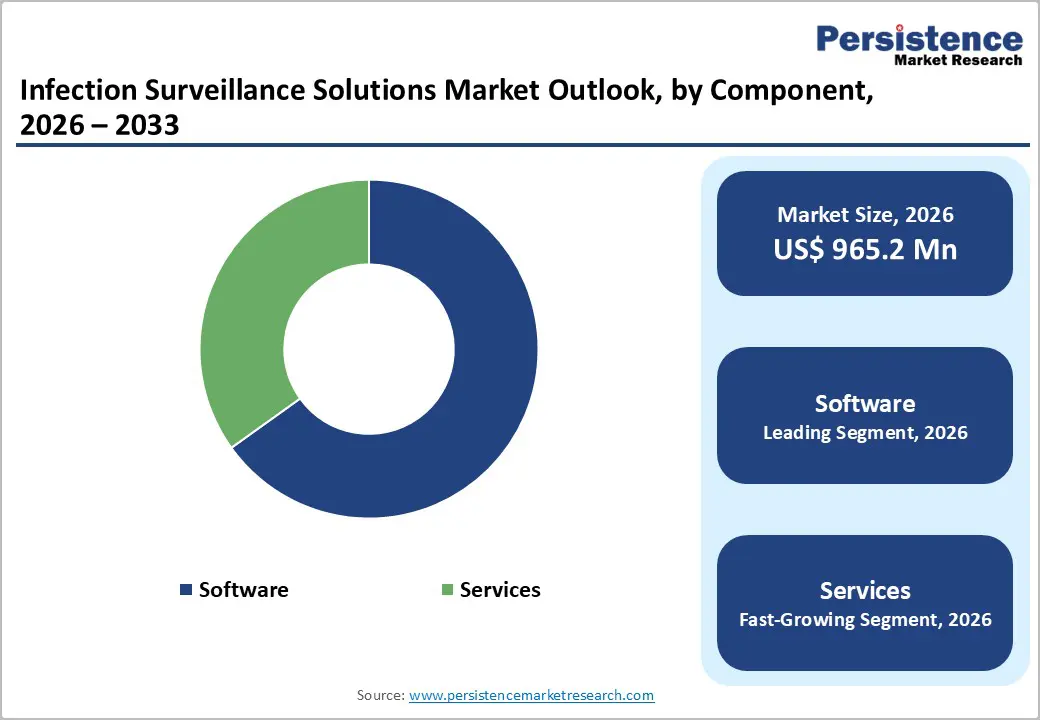

The global infection surveillance solutions market size is likely to be valued at US$ 965.2 million in 2026 to US$ 2,371.0 million by 2033 growing at a CAGR of 13.7% during the forecast period from 2026 to 2033.

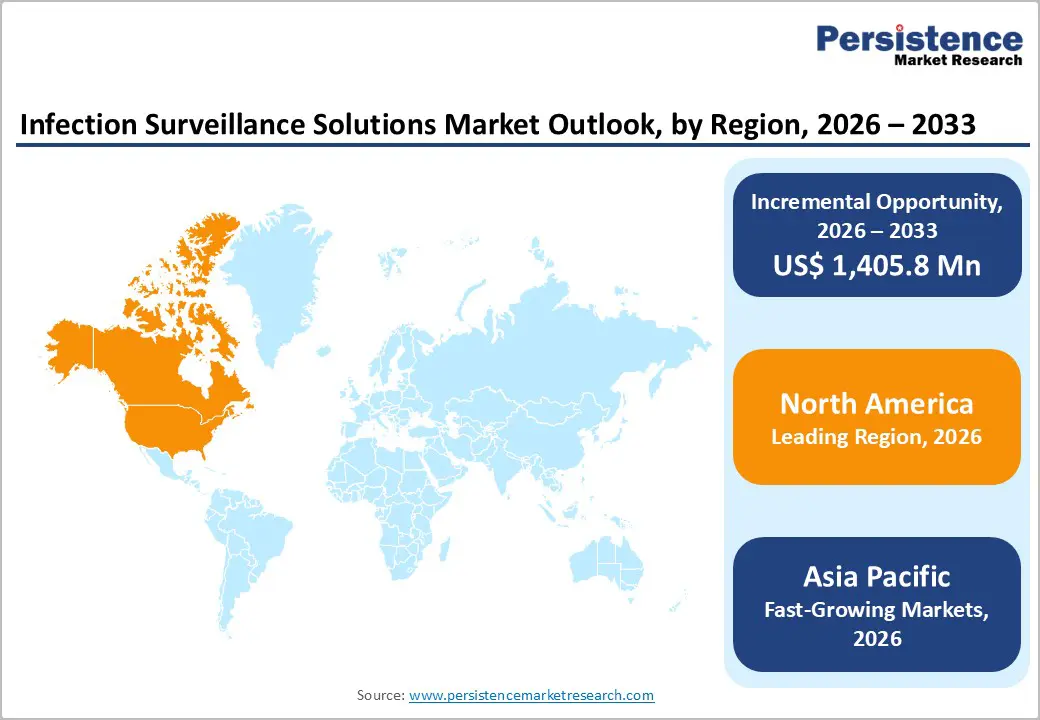

The infection surveillance solutions market is witnessing steady growth, driven by the rising incidence of hospital-acquired infections (HAIs), increasing patient admissions, and stricter infection control regulations across healthcare facilities. North America dominates the market owing to advanced healthcare IT infrastructure, early adoption of digital surveillance platforms, and strong regulatory oversight. Asia-Pacific is the fastest-growing region, driven by rapid healthcare digitization, expanding hospital networks, government initiatives to improve patient safety, and growing awareness of data-driven infection-monitoring solutions.

Key Industry Highlights:

- Dominant Segment: Software solutions lead the market with an estimated 65.1% share in 2025, driven by widespread adoption of automated surveillance platforms, real-time data analytics, integration with EHR systems, and strong demand for early detection and reporting of hospital-acquired infections across acute and tertiary care settings.

- Dominant Region: North America dominates with approximately 45.3% share in 2025, supported by advanced healthcare IT infrastructure, strict infection control regulations, and high adoption of digital health solutions. Asia-Pacific is the fastest-growing region, driven by rapid hospital expansion, healthcare digitization initiatives, and rising focus on patient safety and infection monitoring.

- Market Drivers: Growth is driven by increasing incidence of HAIs, rising hospital admissions, regulatory mandates for infection reporting, growing adoption of electronic health records, and the need for real-time, data-driven infection prevention and control strategies.

- Market Opportunity: Key opportunities include cloud-based and AI-enabled surveillance platforms, predictive analytics for outbreak prevention, expansion in emerging healthcare markets, integration with telehealth systems, and growing demand for scalable solutions among small and mid-sized hospitals.

| Key Insights | Details |

|---|---|

| Global Infection Surveillance Solutions Market Size (2026E) | US$ 965.2 Mn |

| Market Value Forecast (2033F) | US$ 2,371.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 13.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.5% |

Market Dynamics

Driver - Rising Incidence of Hospital-Acquired Infections (HAIs)

The rising incidence of hospital-acquired infections (HAIs) remains a major challenge for healthcare systems and is a core driver for the adoption of infection surveillance solutions. According to data from the U.S. Centers for Disease Control and Prevention, on any given day, approximately one in 31 hospitalized patients in the United States has at least one HAI. Historical national estimates indicate that U.S. acute care hospitals report nearly 700,000 HAIs annually, contributing to tens of thousands of preventable deaths and billions of dollars in excess healthcare costs. These figures highlight the persistent risk of infections despite existing control measures, increasing the need for continuous, automated infection monitoring systems.

At a global level, the burden of HAIs further reinforces demand for infection surveillance solutions. The World Health Organization reports that roughly 5-10 percent of hospitalized patients worldwide acquire at least one healthcare-associated infection, with significantly higher rates observed in low- and middle-income countries. In Europe alone, an estimated 4 million patients develop at least one HAI each year in acute care hospitals. Such widespread incidence underscores gaps in early detection and infection control, driving healthcare providers to adopt real-time digital surveillance platforms to improve reporting accuracy, outbreak detection, and preventive decision-making.

Restraints - High Implementation and Maintenance Costs

High implementation and ongoing maintenance costs are a key restraint on the infection surveillance solutions market, as these platforms require substantial investments in software, infrastructure, and technical support. Data on electronic health record systems analogous to infection surveillance deployments shows that hospitals can face implementation costs ranging from $500,000 to over $5 million for mid- to large-sized facilities, with smaller clinics also spending tens of thousands of dollars to deploy and customize clinical IT systems. Beyond initial outlays, organizations must plan for recurring maintenance, support, and upgrades that often amount to 15-25 percent of initial software fees annually, increasing the total cost of ownership significantly. Such high financial commitments can deter particularly smaller and resource-limited providers from adopting advanced digital surveillance solutions.

In addition to software procurement, hospitals incur large IT operating expenses that constrain budget allocations for specialized surveillance systems. Public financial data indicate that the average U.S. hospital spends approximately $10.5 million annually on IT, accounting for about 2.3 percent of total operating expenses. These IT budgets must cover a broad array of needs, including hardware, network upgrades, staff training, cybersecurity, and compliance, leaving limited incremental funds available for new surveillance platforms. The complexity of integrating new systems with legacy infrastructure and ensuring ongoing security and regulatory compliance further increases administrative burden and costs. Consequently, even though infection surveillance solutions can improve patient outcomes, the high implementation and maintenance costs continue to restrain wider market adoption.

Opportunity - Expansion of Cloud-Based and Web-Based Surveillance Platforms

The expansion of cloud-based and web-based surveillance platforms presents a significant opportunity for the infection surveillance solutions market because healthcare providers increasingly seek scalable, flexible, and cost-efficient IT systems that support real-time data access and interoperability. Government and public health data indicate that more than 80 percent of U.S. hospitals now use cloud-based electronic health records, enabling clinicians and administrators to securely access patient information from any location, directly supporting infection-monitoring workflows. Cloud infrastructure also allows integration with analytics tools, facilitating automated reporting, faster outbreak detection, and improved compliance with public health reporting requirements. As healthcare digital transformation accelerates, cloud surveillance systems reduce dependence on costly on-premises servers and streamline data sharing across departments and facilities, driving broader adoption.

Wider cloud adoption is evident beyond EHRs, underscoring the opportunity for infection-surveillance solutions built on web platforms. For example, industry data show that over 70 percent of healthcare organizations have already implemented cloud services or plan to do so in the near term, driven by needs for scalability, data analytics, and collaborative care technologies. Cloud systems support secure storage and processing of large volumes of clinical data, essential for population-level infection tracking, predictive modeling, and AI-enabled risk scoring. By leveraging cloud deployment models, healthcare facilities can reduce initial IT capital investment, improve scalability to handle growing datasets, and accelerate deployment timelines for surveillance tools, particularly beneficial for small and mid-sized hospitals and emerging markets where IT budgets are constrained, and digital infrastructure is evolving rapidly.

Category-wise Analysis

By Component Insights

Software dominates with 65.1% share of the global market in 2025, because it enables real-time data collection, integration, analysis, and reporting that are essential for effective infection prevention and control. Healthcare facilities increasingly rely on software platforms that pull data from electronic health records, laboratory systems, and patient monitoring devices to generate automated alerts and dashboards. This capability improves the speed and accuracy of infection detection, supports compliance with regulatory reporting requirements, and enhances decision-making for clinical teams. In 2023, software accounted for over 60 percent of the overall market share, reflecting its critical role in transforming raw clinical data into actionable insights that help reduce healthcare-associated infections and improve patient outcomes.

By Deployment Mode Insights

The on-premise deployment model dominates the infection surveillance solutions market because healthcare providers prioritize control over sensitive clinical data and integration with existing IT infrastructure. Many hospitals, especially in the U.S., initially implemented electronic health records (EHRs) and critical clinical systems on-premise, with over 80 percent of hospitals using locally hosted EHRs, reflecting longstanding reliance on internal networks. On-premise surveillance platforms allow hospitals to maintain stricter data security, comply with HIPAA regulations, and integrate seamlessly with legacy systems. Despite growing cloud adoption, mission-critical infection monitoring tools remain on-site to ensure operational reliability, rapid access to real-time data, and tailored security policies. These factors reinforce on-premise systems as the preferred choice for large hospitals and healthcare networks, sustaining their market dominance.

Regional Insights

North America Infection Surveillance Solutions Market Trends

North America dominates the infection surveillance solutions market due to its advanced healthcare IT infrastructure and high adoption of digital health technologies. Nearly 96 percent of U.S. acute care hospitals have implemented certified electronic health record (EHR) systems, and a similar proportion of office-based physicians use EHRs, enabling seamless integration of infection surveillance software with clinical and laboratory data for real-time monitoring. Strong regulatory frameworks, including the CDC’s National Healthcare Safety Network (NHSN), mandate standardized infection reporting, encouraging hospitals to adopt robust surveillance platforms to ensure compliance and improve patient safety. High healthcare expenditure, ongoing IT investments, and a focus on reducing hospital-acquired infections further drive deployment of advanced surveillance solutions, consolidating North America’s leading position in the global market.

Europe Infection Surveillance Solutions Market Trends

Europe is a key region in the infection surveillance solutions market due to the high burden of healthcare-associated infections (HAIs) and strong public health infrastructure. According to the European Centre for Disease Prevention and Control (ECDC), an estimated 4.3 million patients acquire at least one HAI annually in EU/EEA hospitals, with respiratory, urinary tract, surgical site, and bloodstream infections being most common. On average, about 7 percent of hospitalized patients experience an HAI, highlighting ongoing infection risks despite established control measures. Well-developed surveillance networks, such as the European Antimicrobial Resistance Surveillance Network (EARS-Net) and HAI-Net, coordinate standardized infection tracking and reporting, creating demand for digital platforms that integrate with national systems, automate reporting, and enhance prevention strategies across hospitals and long-term care facilities.

Asia-Pacific Infection Surveillance Solutions Market Trends

Asia Pacific is the fastest-growing region in the infection surveillance solutions market due to rapid healthcare digitization and increasing focus on infection control. In India, the Ayushman Bharat Digital Mission has digitized over 110 million health records, creating a foundation for integrated clinical data systems that support infection monitoring. In China, government initiatives and hospital modernization programs are driving adoption of real-time clinical systems and infection surveillance platforms. Southeast Asian countries are also investing in digital tools for infection prevention and control to improve patient safety. Rising hospital admissions, expanding healthcare infrastructure, and growing awareness of hospital-acquired infections further accelerate demand. Combined with improving internet and IT infrastructure, these factors make Asia Pacific a high-growth market for infection surveillance solutions.

Competitive Landscape

Leading infection surveillance solution providers focus on software innovation, real-time analytics, and staff training, collaborating with hospitals and public health agencies. By improving early detection, automated reporting, and EHR integration, they enhance patient safety, reduce hospital-acquired infections, support compliance, and drive adoption, fueling growth in the global Infection Surveillance Solutions Market.

Key Industry Developments:

- In December 2025, BD (Becton, Dickinson and Company) expanded the BD MAX™ System menu by introducing new IVDR-certified VIASURE assays in partnership with Certest Biotec. The expansion followed European In Vitro Diagnostic Medical Device Regulation certification of two molecular assays developed by Certest for use on the automated BD MAX™ molecular platform.

- In October 2025, BD announced the launch of new AI-enabled solutions to drive connectivity across healthcare settings, introducing the BD Incada™ Connected Care Platform, a scalable, cloud-based system that unified data from BD’s medical devices into a single intelligent ecosystem.

- In September 2025, Baxter became the first manufacturer to achieve the Gold Resiliency Badge from the Healthcare Industry Resilience Collaborative (HIRC) for its IV solutions, nutrition solutions, and premix drugs categories. The award recognized Baxter’s strengthened supply chain practices in demand planning, logistics, risk management, and inventory oversight, reflecting its ability to better anticipate, respond to, and recover from disruptions.

Companies Covered in Infection Surveillance Solutions Market

- Becton Dickson & Company

- Baxter International

- Premier, Inc.

- Truven Health Analytics Inc. (IBM Watson)

- Gojo Industries, Inc.

- RL Solutions

- Wolters Kluwer N.V.

- Vigilanz Corporation

- BD Diagnostics

- ICNet Systems, Inc. (Baxter International)

- Vecna Technologies, Inc.

- bioMerieux, Inc.

- PeraHealth Inc.

- Cerner Corporation

- Others

Frequently Asked Questions

The global Infection Surveillance Solutions Market is projected to be valued at US$ 965.2 Mn in 2026.

Rising hospital-acquired infections, stringent regulations, healthcare IT adoption, patient safety focus, and advancements in analytics drive market growth.

The global Infection Surveillance Solutions Market is poised to witness a CAGR of 13.7% between 2026 and 2033.

Cloud-based platforms, AI analytics, emerging markets, real-time reporting, and adoption in non-acute care settings are key market opportunities.

Becton Dickson & Company, Baxter International, Premier, Inc., Truven Health Analytics Inc. (IBM Watson), Gojo Industries, Inc., RL Solutions.