- Advanced Materials

- India Sandwich Panel Market

India Sandwich Panel Market Size, Share, and Growth Forecast, 2025 - 2032

India Sandwich Panel Market by Material Type (Mineral Wool, Polyurethane (PUR), Expanded Polystyrene (EPS), Polyisocyanurate (PIR), Glass wool, and Rockwool), Application (Industrial, Commercial, and Residential), End-Use Industry (Building and Construction, Cold Storage and Refrigeration, Transport and Automotive, Industrial Warehousing, Retail & Commercial Spaces, Misc.), and Regional Analysis for 2025 - 2032

India Sandwich Panel Market Share and Trends Analysis

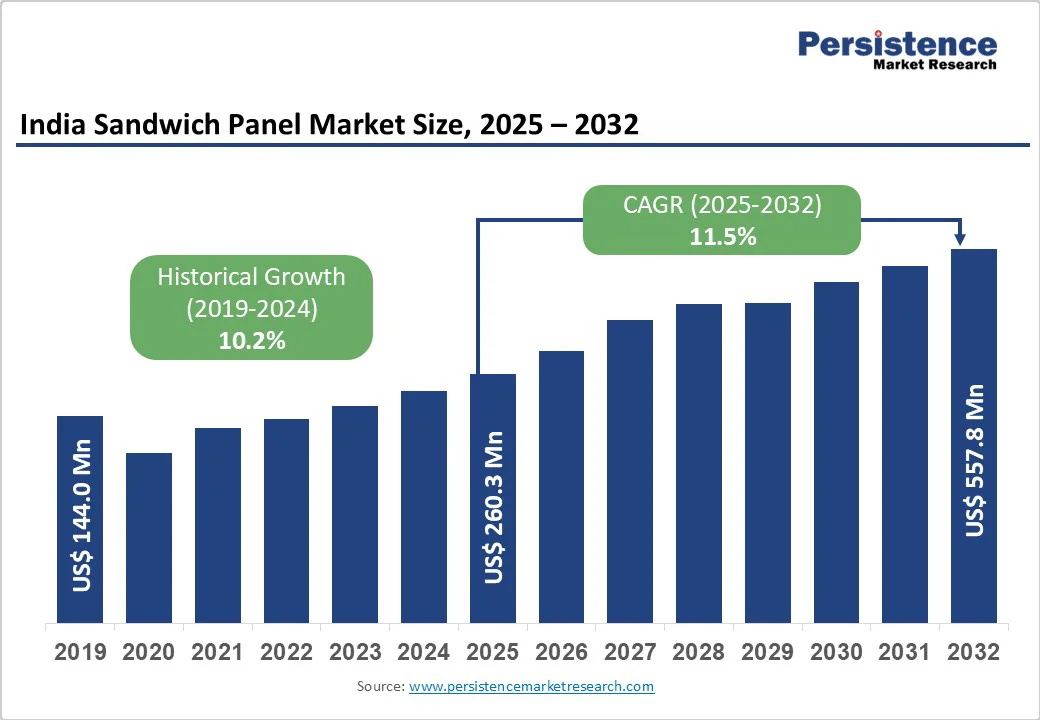

The India sandwich panel market size is likely to be valued at US$260.3 million in 2025, and is projected to reach US$557.8 million by 2032, growing at a CAGR of 11.5% during the forecast period 2025-2032. The rising emphasis on sustainable building practices and stringent government regulations promoting thermal insulation has significantly accelerated the adoption of sandwich panels across commercial, industrial, and residential applications.

Key Industry?Highlights

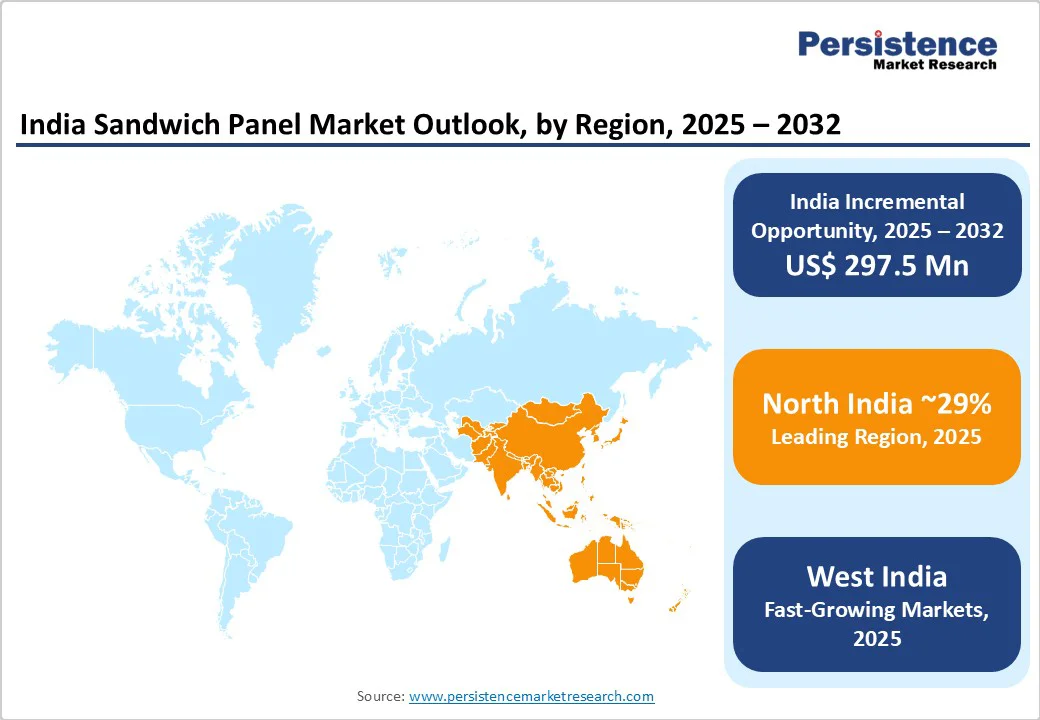

- Regional Leaders: West India is estimated to dominate the India sandwich panel market with a 28% share in 2025, driven by high industrial and cold-storage activity, proximity to key ports, and rapid urban infrastructure development.

- Leading Segments: Polyurethane (PUR) panels are poised to dominate the material segment, accounting for approximately 43% of the Indian sandwich panel market revenue share by 2025.

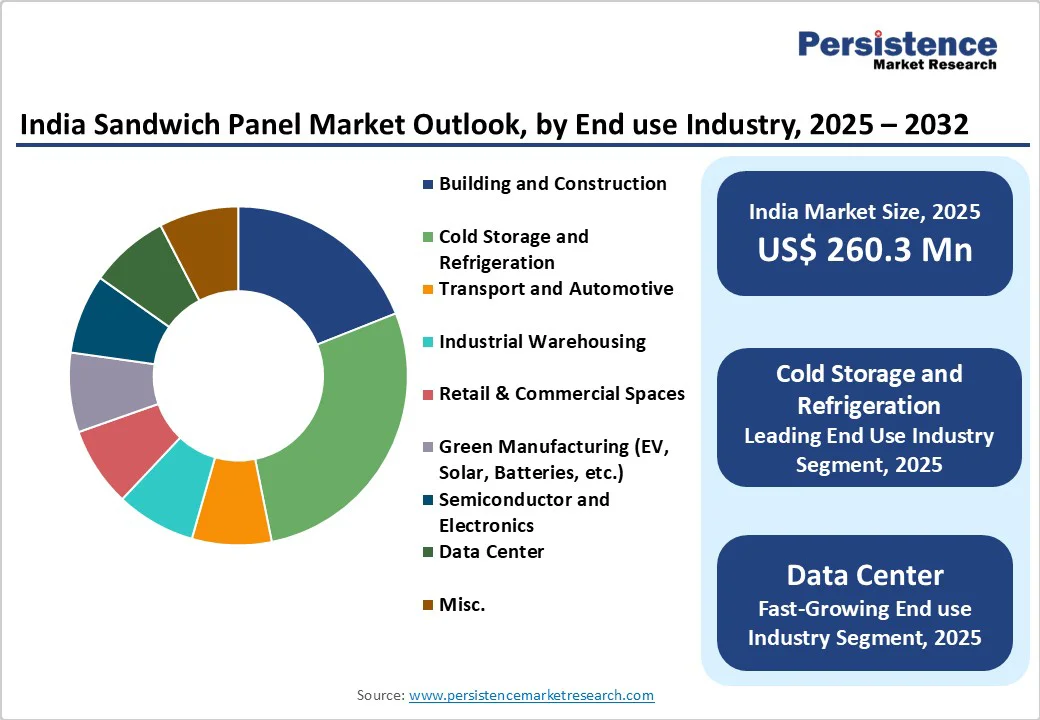

- Industry Applications: Cold storage applications are estimated to account for 29% market share in 2025, reflecting India’s expanding temperature-controlled infrastructure.

- Market Drivers: Rising demand from the cold chain, food processing, pharmaceuticals, industrial sheds, and green manufacturing facilities, with an emphasis on energy efficiency and rapid installation.

- Market Restraints: High raw material and manufacturing costs, fire safety concerns, regulatory compliance challenges, and price sensitivity among small projects.

| Key Insights | Details |

|---|---|

|

India Sandwich Panel Market Size (2025E) |

US$260.3 Mn |

|

Market Value Forecast (2032F) |

US$557.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

11.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Cold Chain Infrastructure Driving Market Growth

India is experiencing an unprecedented surge in its cold chain infrastructure, fueled by the booming e-commerce sector, food processing, and pharmaceutical industries. The rapid growth of India’s e-commerce market has led to an increasing demand for refrigerated warehouses and temperature-controlled storage facilities. The rising need to maintain perishable goods and temperature-sensitive pharmaceuticals during transit has made modular and insulated construction materials, such as sandwich panels, crucial. The lightweight nature of these panels results in lower structural support requirements, thereby reducing overall construction costs. Key government initiatives, such as the National Cold Chain Mission, with an ambitious target to integrate and modernize cold chain infrastructure across India, supplement this growth trend.

Another key factor is that India's growing digital economy, cloud adoption, and data localization policies have driven the rapid expansion of its data centers. The data center capacity is expected to triple from 1 GW in 2024 to 3 GW by 2027. These facilities require highly specialized building materials that offer stringent fire resistance, superior thermal insulation, and acoustic control to protect mission-critical hardware.

Polyisocyanurate (PIR) core sandwich panels with integrated moisture barriers and fire certifications compliant with Bureau of Indian Standards (BIS) and other international standards have found increasing preference in these projects. The panels’ acoustic damping helps minimize ambient noise affecting sensitive equipment, while their air-tightness contributes to maintaining controlled environments vital for uninterrupted data processing.

Fire Safety Concerns and Regulatory Compliance Challenges

Increasing incidents of industrial fires in India have intensified scrutiny over the fire performance of sandwich panels used in commercial, industrial, and residential buildings. While EPS and PUR panels offer excellent insulation, they are inherently combustible and can contribute to rapid fire spread under certain conditions. Regulatory authorities, including the BIS and local fire departments, have tightened fire safety requirements, particularly mandating Class A fire ratings for buildings with large occupancy or critical infrastructure functions.

This regulatory shift has driven demand towards mineral wool and PIR core sandwich panels, which offer non-combustible, fire-retardant properties and meet enhanced fire resistance standards, such as IS 401 and EN 13501-1. However, these fire-safe panels often carry a price premium of 20-30% more than conventional cores, posing challenges for cost-sensitive standalone warehouses and commercial buildings in Tier 2 and Tier 3 cities. Consequently, cost-versus-safety trade-offs and limited fire code enforcement in some regions slow down the widespread adoption of advanced fire-rated sandwich panels.

Green Manufacturing Hubs and PLI Scheme-Driven Industrial Investment

The Indian Government’s Production Linked Incentive (PLI) scheme, targeting key manufacturing sectors such as electric vehicle (EV) battery assembly, solar photovoltaic panel production, and electronics, has catalyzed over US$5 billion in new industrial investments, concentrated in Gujarat, Uttar Pradesh, and Telangana. These green manufacturing hubs demand modern building envelopes that emphasize energy efficiency, cleanroom capabilities, and rapid constructability.

Sandwich panels are central to fulfilling these needs, as they offer excellent thermal insulation, reducing operational energy costs by up to 25%, while also providing a hygienic, dust-free construction essential for electronics and battery production. The panels' modular nature enables flexible layouts and faster facility commissioning, which aligns well with the dynamic scale-up needs of emerging green industries. Companies are also increasingly exploring eco-friendly panel variants with recycled content and low Global Warming Potential (GWP) insulation cores to meet stringent environmental regulations and corporate sustainability goals. This focus on green manufacturing drives R&D efforts, elevating demand for next-generation sandwich panels that can support Industry 4.0 manufacturing environments.

Category-wise Analysis

Material Type Insights

Polyurethane (PUR) sandwich panels are anticipated to command approximately 43% of the sandwich panel market revenue share in 2025. This dominance stems from PUR's exceptional thermal insulation properties, achieving thermal conductivity values as low as 0.022 W/m·K and R-values exceeding R-7 per inch, making them ideally suited for India's diverse climate conditions ranging from tropical to temperate zones. The material's cost-effectiveness, combined with superior energy efficiency, has positioned it as the preferred choice across industrial, commercial, and cold storage applications.

The lightweight nature of PUR panels, with densities ranging from 35-45 kg/m³, facilitates rapid installation and reduces structural loading requirements, contributing to overall construction cost savings of 20-25% compared to traditional building materials. The excellent moisture resistance and dimensional stability of PUR make it particularly suitable for India's monsoon-prone regions, where humidity control is critical for building performance.

Application Insights

The industrial application is set to maintain market leadership with around 55% revenue share in 2025, driven by India's rapid industrialization and the establishment of manufacturing hubs across Gujarat, Maharashtra, Tamil Nadu, and Uttar Pradesh. The rise of organized retail chains and third-party logistics providers has led to the construction of over 3 million m² of industrial floor space annually. Sandwich panels are preferred for large-span roofing and wall systems, offering rapid installation, cost savings of up to 20%, and compliance with energy efficiency norms.

The rise of green manufacturing facilities, particularly in EV battery production and solar panel assembly, has created specialized demand for panels with enhanced fire resistance, cleanroom compatibility, and electromagnetic shielding properties. Industrial end-users are increasingly specifying panels that meet international standards, such as ISO 14001 for environmental management and OHSAS 18001 for occupational health and safety, reflecting the focus of the sector on compliance and operational excellence.

End-Use Industry Insights

Cold storage and refrigeration applications are expected to dominate with an estimated 29% market share in 2025, reflecting India's rising need for temperature-controlled infrastructure supporting food security, pharmaceutical distribution, and the rapidly expanding e-commerce sector. Its dominance aligns with India's cold storage capacity expansion from 37 million MT in 2020 to over 42 million MT in 2024, with government projections targeting 65 million MT by 2027 under the National Cold Chain Mission. The sector's growth is particularly pronounced in pharmaceutical applications, where stringent temperature requirements for vaccine storage and biologics distribution have created premium market opportunities for high-performance sandwich panels.

Regional Insights

West India Sandwich Panel Market Trends

West India is expected to lead India's sandwich panel market share with a commanding 28% in 2025, driven by concentrated industrial activity, robust infrastructure development, and strategic geographical advantages. The region’s dominance is supported by Gujarat and Maharashtra, which collectively host India's largest industrial corridors, major ports, and manufacturing hubs. Gujarat alone accounts for over 22% of India's chemical production. It houses 30% of the country's pharmaceutical manufacturing capacity, creating substantial demand for temperature-controlled storage and industrial building applications that require high-performance sandwich panels.

On the other hand, Maharashtra's industrial landscape, centered on its automotive assembly plants, IT parks, and logistics hubs, requires rapid construction solutions. The state government’s solar rooftop mandate for industrial buildings has further increased the use of reflective white-faced panels to optimize energy performance.

North India Sandwich Panel Market Trends

North India is anticipated to hold a substantial 27% share in the Indian sandwich panel market in 2025, driven primarily by its diversified industrial base, hosting leading automotive manufacturers, IT services companies, logistics operators, and cold storage facilities requiring advanced building envelope solutions. The National Capital Region (NCR) alone boasts over 1.2 million tons of cold storage capacity, with anticipated growth supported by e-commerce expansion and government initiatives under the National Cold Chain Mission.

Moreover, Uttar Pradesh's emergence as a manufacturing destination under the One District One Product (ODOP) scheme has created significant demand for industrial buildings utilizing sandwich panels for rapid construction. The state's food processing sector, contributing over 8.6% to India's total food production, requires specialized cold storage and processing facilities where sandwich panels provide essential thermal insulation and hygienic construction solutions.

East India Sandwich Panel Market Trends

East India represents the most significant emerging opportunity in the Indian sandwich panel market, positioned for accelerated growth driven by ambitious infrastructure development programs and industrial modernization initiatives. The region, encompassing West Bengal, Odisha, Bihar, and Jharkhand, has been strategically positioned under the Budget 2024-25 with allocations exceeding INR 26,000 crores for infrastructure development in Bihar alone, and INR 15,000 crores for Andhra Pradesh's Amaravati development, signaling unprecedented government commitment to regional transformation.

These developments are creating substantial demand for rapid construction solutions, with sandwich panels essential for industrial warehousing, cold storage facilities, and manufacturing complexes. The region's focus on developing steel clusters, automotive manufacturing, food processing, and renewable energy projects creates diverse end-use applications for sandwich panels across industrial, cold storage, and green manufacturing segments, positioning East India as a high-growth opportunity region for market participants.

Competitive Landscape

The Indian sandwich panel market is moderately consolidated, with the top ten players holding approximately 40-45% share. Leading companies such as Kingspan Jindal, EPACK Prefab, Alfa PEB, ArcelorMittal Construction, and Viraat Industries are focusing on capacity expansion, product innovation, and turnkey solutions.

Most of the top players are focusing on product differentiation through fire-rated, ultra-slim, and energy-efficient panels to capture institutional projects, whereas smaller players compete on price and customization. The market is anticipated to witness increased consolidation, technology adoption, and regional expansion, positioning major players for strong growth over the next few years.

Key Industry Developments

- In June 2025, EPACK Prefab inaugurated a new sandwich panel manufacturing facility in the Tirupati district, expanding its annual production capacity by 8 lakh sqm. With this addition, the company’s total sandwich panel capacity has reached 13.10 lakh sqm per annum. EPACK Prefab aims to capture a 30–35% share of the prefabricated sandwich panel market by the end of the current fiscal year.

- In June 2025, Rinac India Limited announced a strategic partnership with Epta India and opened a joint Experience Center in Bengaluru to strengthen its retail refrigeration & cold-chain offerings.

- In April 2025, Metecno India Private Limited emphasized energy-efficient insulated sandwich panels and new product positioning in India; Metecno India published a product/innovation feature highlighting sustainable insulated-panel solutions.

Companies Covered in India Sandwich Panel Market

- Rinac India Limited

- Metecno India Private Limited

- EPACK Prefab

- Kingspan Jindal

- ArcelorMittal Construction-India

- WonderPUF

- BNAL Prefabs Pvt Ltd.

- Lloyd Insulations (India) Limited

- ELEMENTS TECHNOFAB PVT. LTD

- Kross Innovations

- Syngery Thrislington

- Viraat Industries

- Alfa PEB Ltd.

- Beardsell

- Ice Make Refrigeration Ltd

- UMA PUF Panel

- Roofmate

- KoreaPuff

- Delta Infrastructure

- Zaron

- Suchi Foam

Frequently Asked Questions

The India sandwich panel market is projected to reach US$ 260.3 million in 2025.

Key drivers include rapid expansion of cold chain infrastructure, government initiatives on affordable housing, growth of e-commerce warehousing, and green manufacturing under PLI schemes.

The market is poised to witness a CAGR of 11.5% from 2025 to 2032.

Capitalizing on the incentives provided under India’s PLI schemes for the manufacturing sector and the development of eco-friendly panel variants with recycled content and low Global Warming Potential (GWP) insulation cores to meet stringent environmental regulations are key market opportunities.

Leading companies include Rinac India Limited, Metecno India Private Limited, EPACK Prefab, Kingspan Jindal, ArcelorMittal Construction-India, and Viraat Industries, etc.