- Medical Devices

- High Pressure Syringes Market

High Pressure Syringes Market Size, Share, and Growth Forecast, 2026 - 2033

High Pressure Syringes Market by Application (Radiology & Interventional Imaging, Cardiovascular Procedures, Oncology, Others), End-User (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers (ASCs), Others), Usage (Disposable, Reusable), and Regional Analysis for 2026-2033

High Pressure Syringes Market Share and Trends Analysis

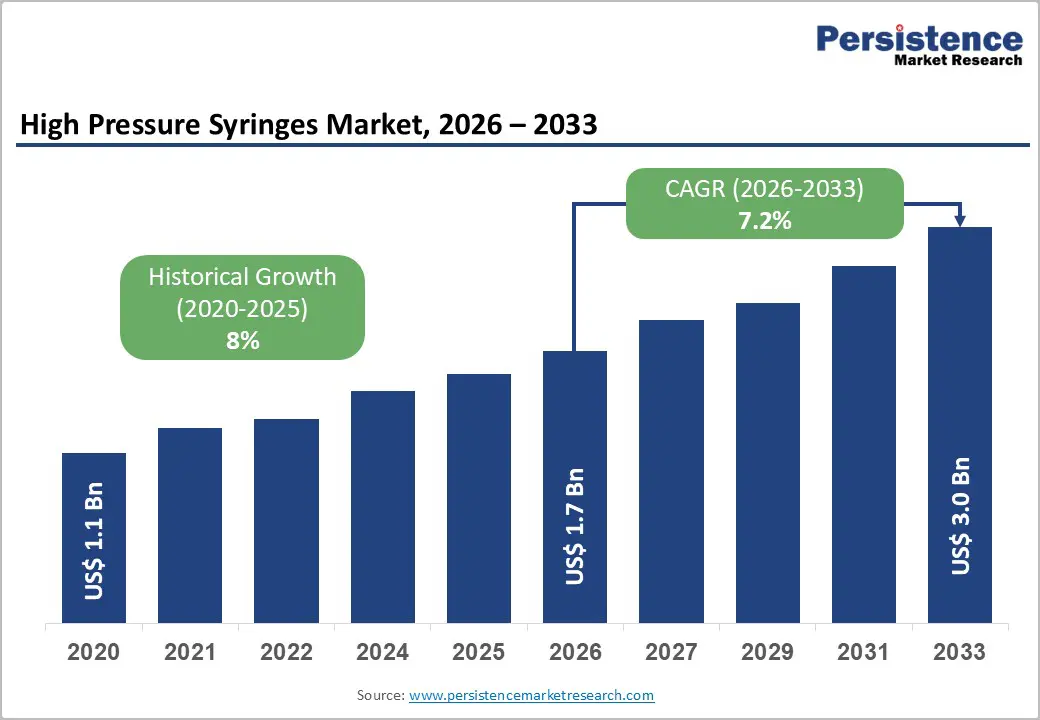

The global high-pressure syringes market size is likely to be valued at US$ 1.7 billion in 2026, and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 7.2% during the forecast period 2026−2033. The increasing burden of chronic diseases such as cardiovascular disorders (CVDs) and cancer is driving demand for advanced diagnostic procedures. Healthcare providers are relying on imaging modalities such as computed tomography (CT) and magnetic resonance imaging (MRI), where high-pressure syringes are delivering contrast media with precision and consistency. The global population is also aging, and older adults are experiencing higher disease incidence, which is increasing procedure volumes across hospitals and diagnostic centers.

Technology innovation is improving product performance and clinical workflow efficiency, which is accelerating adoption across healthcare systems. Manufacturers are introducing syringes with enhanced pressure tolerance, improved safety mechanisms, and compatibility with automated injector systems. Healthcare facilities are prioritizing accuracy, infection control, and procedural standardization, which is increasing the preference for advanced syringe solutions. Market participants are also focusing on regulatory compliance and product differentiation to strengthen competitive positioning. As diagnostic imaging demand continues to rise, the high-pressure syringes market is expected to sustain steady expansion over the forecast timeline.

Key Industry Highlights

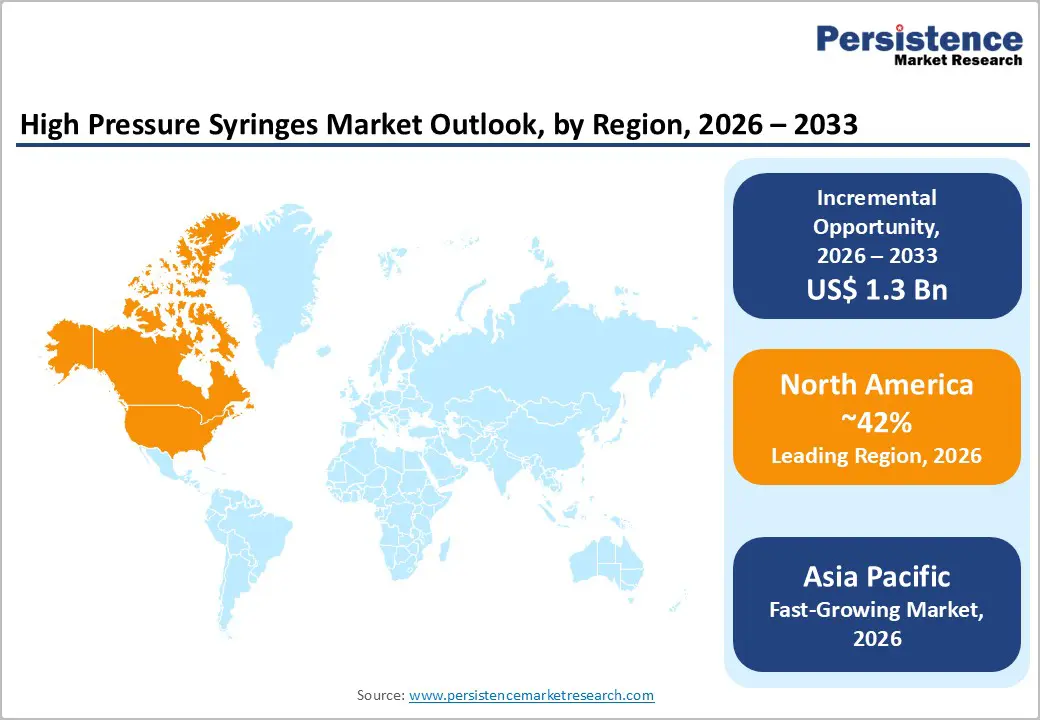

- Dominant Region: North America is expected to command around 42% market share in 2026, aided by a well-established healthcare infrastructure and early adoption of advanced medical technologies.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing through 2033, due to the rapid advancements in healthcare infrastructure and widening access to advanced diagnostic technologies.

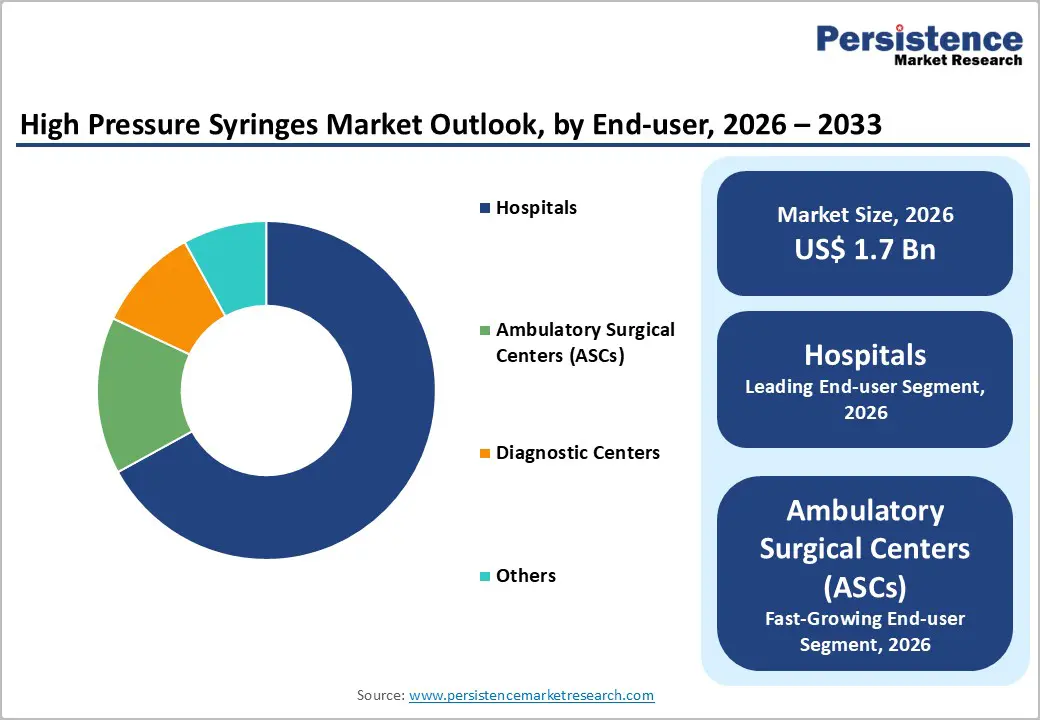

- End-User Dominance: Hospitals are slated to dominate with approximately 67% revenue share in 2026. Whereas ambulatory surgical centers (ASCs) are expected to be the fastest-growing over the 2026-2033 forecast period.

- Application Leadership: Radiology and interventional imaging are set to capture nearly 58% of the market revenues in 2026, while cardiovascular procedures are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Recent Development: A study published in BMJ Innovations showed that a novel high-pressure syringe achieves higher efficiency and lower material stress than conventional designs, improving safety and reliability in imaging procedures.

| Key Insights | Details |

|---|---|

| High Pressure Syringes Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Diagnostic Imaging Procedures

The global burden of chronic diseases is continuing to rise, and cardiovascular diseases are accounting for approximately 17.9 million deaths each year, according to the World Health Organization (WHO). The increasing prevalence of long-term conditions such as CVDs and cancer is driving demand for high-pressure syringes across diagnostic care pathways. Healthcare providers are using these devices to deliver contrast agents accurately during imaging procedures such as computed tomography (CT) angiography, cardiac catheterization, and interventional radiology. Patients with complex health conditions are undergoing repeated scans to monitor disease progression and evaluate treatment response, which is increasing procedural frequency in hospitals and specialty clinics. This clinical reliance is strengthening the need for dependable injection systems that can maintain consistent pressure delivery and patient safety standards.

The aging population is further expanding demand for diagnostic services, as older adults are facing higher risks of chronic illnesses that require continuous screening and monitoring. Developed healthcare markets are experiencing significant impact from demographic shifts, while emerging regions are also preparing for similar trends. The United Nations (UN) is projecting a substantial increase in the population aged 65 years and above by mid-century, which is expected to elevate demand for cardiovascular and oncology imaging. Technological advancements are improving syringe precision, durability, and operational efficiency, which is supporting broader adoption across healthcare facilities. These combined factors are sustaining steady market expansion through increasing procedure volumes and ongoing healthcare infrastructure investments.

Technological Advancements in Imaging Equipment

Advanced imaging technologies such as dual-energy CT and 3 Tesla (3T) MRI systems are increasing demand for precision high-pressure syringes. These devices are delivering contrast media at controlled flow rates to generate clear vascular visualization and accurate diagnostic output. Healthcare providers are relying on them for complex examinations where image clarity directly influences treatment decisions. Radiology departments across global healthcare facilities are adopting these solutions to manage rising procedure volumes and maintain workflow efficiency. Artificial intelligence (AI) is also transforming imaging protocols by enabling optimized contrast administration strategies, which is reinforcing the importance of advanced injection systems in modern diagnostics.

Modern syringe platforms are incorporating adjustable pressure controls, real-time monitoring, and automated safety mechanisms to improve both clinical outcomes and operational productivity. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) are authorizing devices that include integrated sensors and automatic protection features, which is establishing higher reliability standards across the industry. Hospitals and diagnostic centers are upgrading equipment inventories to comply with evolving performance expectations and patient safety requirements. This transition is improving diagnostic accuracy while also creating recurring procurement cycles for technologically advanced systems. Manufacturers are benefiting from sustained demand that is linked to innovation adoption and replacement needs.

Skilled Healthcare Workforce Shortages Limiting Technology Adoption

Workforce shortages are constraining market growth by limiting procedure capacity across imaging centers. Facilities that are operating below optimal utilization due to insufficient trained personnel are finding it difficult to justify investments in premium high-pressure injection systems. Many providers are extending the lifespan of legacy equipment that requires less specialized handling, which is delaying replacement cycles that typically stimulate market expansion. Manufacturers are also encountering reduced differentiation opportunities because advanced product features remain underused when clinical staff lack adequate training or time to implement complex protocols. This challenge is affecting ASCs and diagnostic imaging networks that are expanding into suburban regions, where recruiting experienced radiology technologists is proving difficult due to competition from large hospital systems offering higher compensation packages.

Healthcare facilities facing staffing constraints are often prioritizing cost control and operational simplicity, which is leading them to select basic injection platforms with user-friendly interfaces instead of technologically advanced solutions. This shift is narrowing the addressable market for premium product categories and slowing innovation adoption rates. Labor shortages are also increasing operational expenses through overtime payments and temporary staffing requirements, which is forcing providers to demand clear return on investment from new equipment purchases. Manufacturers that are not demonstrating measurable clinical and economic value through evidence-based data are experiencing longer sales cycles and higher price sensitivity among buyers. These pressures are compressing profit margins across the industry and are reinforcing the need for value-driven product positioning strategies.

Accelerating Shift toward Alternative Imaging Modalities and Dose-Reduction Protocols

Technological progress in diagnostic imaging is increasingly prioritizing radiation dose reduction and non-contrast techniques, which is lowering dependence on high-pressure contrast injection systems. Advanced CT reconstruction approaches such as iterative reconstruction and AI-driven noise reduction are enabling diagnostic image quality at significantly lower radiation exposure levels. This improvement is correlating with reduced contrast media requirements and lower injection pressure needs during procedures. Dual-energy CT is allowing virtual non-contrast image reconstruction, which is eliminating the need for contrast administration in selected clinical scenarios that previously required injection. Ultrasound innovations, particularly contrast-enhanced ultrasound (CEUS) that uses microbubble agents, are also providing alternative diagnostic pathways for vascular evaluation and organ perfusion assessment that were traditionally performed using CT angiography.

These technological transitions are reducing the total addressable market by decreasing contrast utilization per procedure and increasing the number of examinations that are completed without contrast administration. Regulatory authorities and healthcare payers are accelerating adoption of dose optimization protocols through reimbursement incentives and quality reporting frameworks. Programs such as the Medicare Hospital Outpatient Quality Reporting Program are incorporating radiation exposure metrics, which is encouraging healthcare facilities to minimize contrast-enhanced imaging when clinically appropriate alternatives are available. These policy and technology drivers are creating structural pressure on market volume growth regardless of overall imaging procedure expansion.

Integration of Smart Technologies and Connectivity

Internet of Medical Things (IoMT) platforms are integrating with high-pressure syringe systems to create new value opportunities across diagnostic workflows. Connected devices are capturing operational data in real time and are adjusting contrast delivery parameters according to patient-specific requirements. These systems are also predicting maintenance needs through performance analytics, which is improving equipment reliability and reducing unexpected downtime. Healthcare providers are benefiting from optimized workflow coordination, improved dosing accuracy, and enhanced procedural safety outcomes. Precision dosing capabilities are helping clinicians minimize complications during imaging procedures while maintaining diagnostic quality.

Value-based care models are further encouraging adoption of intelligent injection technologies that improve outcomes while reducing operational risks and resource wastage. Academic medical centers are leading early implementation efforts by evaluating smart syringe platforms that continuously monitor device performance and usage patterns. These solutions are reducing contrast media waste and equipment downtime through predictive alerts and automated system feedback. Manufacturers are developing premium product portfolios that align with digital health integration requirements and advanced hospital infrastructure standards. The convergence of connectivity, automation, and performance optimization is strengthening market expansion and positioning manufacturers for sustained growth within an increasingly technology-driven healthcare ecosystem.

Expansion in Point-of-Care and Mobile Imaging Applications

Mobile CT units and point-of-care imaging technologies are gaining traction following structural shifts in healthcare delivery after the pandemic period. These developments are creating new demand channels for compact and portable high-pressure syringe systems that can operate outside traditional hospital infrastructure. Healthcare providers are increasingly delivering diagnostic services across decentralized environments, which is requiring flexible equipment solutions that maintain performance standards in varied settings. Manufacturers are designing lightweight syringe models with battery-powered operation, simplified control interfaces, and enhanced portability features to address these needs. Such capabilities are enabling use in non-traditional care environments where space constraints limit the deployment of conventional systems.

Rural healthcare centers, military field hospitals, and urgent care facilities are requiring durable and reliable diagnostic tools that can support on-site imaging without infrastructure dependency. Underserved regions are benefiting from rugged device construction that withstands transportation stress and environmental variability. Ongoing innovation is reducing device weight while enabling wireless connectivity and remote monitoring functions, which is improving mobility and operational coordination. Healthcare personnel are learning to operate these systems quickly due to intuitive interface designs that support field deployment conditions. Healthcare networks are also investing in portable imaging kits to extend diagnostic coverage and improve response efficiency across distributed care models.

Category-wise Analysis

Application Insights

Radiology and interventional imaging are anticipated to dominate, accounting for approximately 58% of the high pressure syringes market revenue share in 2026. These applications include procedures such as CT angiography, cardiac catheterization, and interventional radiology, where clinicians are delivering high volumes of contrast agents at controlled pressure levels to achieve accurate visualization. Hospitals are relying on high-pressure syringes to support diagnostic precision and therapeutic effectiveness across complex imaging protocols. The widespread installation of CT scanners across global healthcare facilities is reinforcing segment leadership, as advanced imaging workflows require specialized injection systems to maintain consistency and safety. Healthcare facilities are maintaining adequate inventory levels to manage routine workloads efficiently, while interventional teams are prioritizing syringe designs that integrate smoothly with existing injector platforms to optimize procedural efficiency.

Cardiovascular procedures are expected to be the fastest-growing application segment through 2033, due to the rising burden of heart-related conditions and increasing procedural volumes. Clinicians are using high-pressure syringes in angiography, angioplasty, and other cardiac interventions to ensure accurate delivery of contrast media or therapeutic substances during treatment. This precision is supporting clear visualization and improving procedural outcomes in catheterization laboratories. Demographic factors such as aging populations, sedentary lifestyles, and increasing obesity prevalence are contributing to higher cardiovascular disease incidence, which is strengthening demand for reliable injection technologies. Technological advancements are improving device safety, pressure control, and operational efficiency, which is enhancing clinician confidence and patient recovery outcomes.

End-User Insights

Hospitals are set to lead by securing roughly 67% of the high pressure syringes market share in 2026. These facilities are managing the majority of diagnostic and interventional procedures that depend on high-pressure injection systems, which is creating consistent demand for reliable and high-performance devices. Large patient volumes are requiring hospitals to maintain efficient workflows, and advanced medical infrastructure is enabling them to perform complex imaging studies and minimally invasive interventions. Strong financial capacity is allowing hospitals to invest in premium syringe technologies that offer higher precision, integrated safety mechanisms, and compatibility with automated injector platforms.

ASCs are expected to be the fastest-growing end users during the forecast period from 2026 to 2033 due to the expansion of outpatient care models and cost-efficiency advantages. These facilities are providing surgical and diagnostic services in streamlined environments that reduce patient expenses, shorten recovery duration, and minimize infection exposure compared to inpatient settings. Increasing patient preference for outpatient procedures is raising demand for dependable injection systems that support imaging and interventional workflows. ASCs are adopting advanced medical technologies to enhance service quality and procedural turnaround time, while high-pressure syringes are enabling accurate contrast delivery during minimally invasive treatments. The ongoing shift toward outpatient care delivery is therefore strengthening segment expansion through improved accessibility, technological adoption, and workflow optimization.

Regional Insights

North America High Pressure Syringes Market Trends

North America is slated to command approximately 42% of the high pressure syringes market value in 2026, powered by a robust demand for diagnostic imaging and interventional procedures. The U.S. is driving most regional activity because of its advanced healthcare infrastructure and high procedural volumes that require precise injection systems. Healthcare providers are conducting frequent imaging studies and minimally invasive interventions, which is sustaining consistent equipment utilization. Policy and reimbursement factors are also supporting growth, as Medicare coverage expansion for preventive cardiovascular screening is increasing procedure volumes. Hospitals are replacing aging imaging equipment that was installed during earlier technology adoption cycles, which is creating demand for compatible and upgraded syringe systems.

The U.S. FDA is facilitating market entry through the 510(k) premarket notification pathway, which allows device approvals based on substantial equivalence to existing products. Reimbursement frameworks are supporting contrast-enhanced procedures, which is reducing financial barriers for healthcare facilities adopting new technologies. Market competition is concentrating around a limited number of major manufacturers that are focusing on innovation through connectivity features, radiation dose optimization, and contrast media waste reduction capabilities. Venture capital investment is increasingly targeting software platforms that optimize injection protocols using AI, while new entrants are developing digital integration tools compatible with installed imaging systems. These developments are indicating a broader transition toward connected healthcare ecosystems.

Europe High Pressure Syringes Market Trends

Europe is poised to remain a critical market for high-pressure syringes, despite stringent environmental requirements and healthcare standards. Germany is leading regional performance through its advanced medical device manufacturing capabilities and extensive diagnostic imaging networks, which are supporting population-wide screening and routine clinical assessments. The U.K. and France are aggressively implementing public healthcare modernization programs that are prioritizing the adoption of updated medical technologies, while Spain is strengthening diagnostic capacity by expanding testing infrastructure to improve patient outcomes. Healthcare providers across the region are operating within a complex regulatory environment shaped by the European Union Medical Device Regulation (EU MDR), which is requiring rigorous quality assurance processes and comprehensive clinical evidence for device approval and commercialization.

Regulatory expectations are favoring established manufacturers with proven compliance capabilities, while sustainability initiatives under the EU Green Deal are encouraging the development of reusable syringe components and structured recycling programs. Suppliers are evaluating closed-loop material recovery systems to reduce waste and improve environmental performance across product lifecycles. Procurement strategies are increasingly focusing on total cost of ownership, which is driving demand for long-term service agreements and durable equipment solutions that offer operational efficiency. Market participants are also expanding into Eastern European countries such as Poland and the Czech Republic, where European Union funding programs are supporting healthcare infrastructure development and improving access to diagnostic services in underserved regions.

Asia Pacific High Pressure Syringes Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for high-pressure syringes through 2033. This is primarily attributable to rapid healthcare expansion and rising diagnostic demand across multiple countries in the region. Spearheading this growth is China on the back of government-led healthcare reforms that are increasing hospital construction and expanding health insurance coverage for large population segments. Japan is maintaining a stable contribution by emphasizing high-quality medical devices and advanced engineering standards, while India is accelerating adoption through medical tourism growth and the expansion of private hospital networks in urban centers. Countries within the ASEAN are also advancing due to economic development and increasing middle-class demand for advanced diagnostic services. Urbanization is concentrating healthcare needs in metropolitan areas, and the rising incidence of lifestyle-related diseases is increasing imaging procedure volumes. Competitive manufacturing costs across the region are attracting medical device production investments, which is strengthening local supply chains and improving product accessibility.

Regulatory frameworks across Asia Pacific are varying significantly, which is influencing market entry strategies for manufacturers. Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) is enforcing strict approval standards, while several emerging markets are allowing faster commercialization through relatively flexible regulatory pathways. Global companies are collaborating with regional manufacturers, and domestic players are gaining market share by offering cost-effective solutions that meet the needs of smaller healthcare facilities. Strategic partnerships are enabling international firms to navigate regulatory complexity, establish localized production, and comply with domestic content requirements while avoiding import tariffs. Investments are increasingly flowing into joint ventures that support efficient market penetration and operational scalability.

Competitive Landscape

The global high-pressure syringes market structure is moderately consolidated and is dominated by Bayer, Bracco Imaging, Medtron, Guerbet Group, and Ulrich Medical. These companies control nearly 60% of the market revenues through strong product portfolios, established distribution networks, and long-standing relationships with healthcare providers. Competitive intensity remains high, and leading players are strengthening their positions through continuous product innovation, strategic collaborations, and merger and acquisition activities. Technological advancements are shaping the competitive landscape, as manufacturers are introducing new syringe systems with enhanced safety mechanisms, improved precision, and faster operational performance to align with evolving clinical requirements.

Market participants are also prioritizing differentiation through integrated solutions that combine hardware performance with digital capabilities, which is supporting long-term customer retention and brand loyalty. Companies are investing in research and development to address unmet clinical needs and regulatory expectations, while partnerships with healthcare institutions are facilitating product validation and adoption. Patients and providers are benefiting from advanced injection technologies that improve procedural accuracy and safety outcomes, which is reinforcing market acceptance. Competitive strategies are therefore continuing to drive industry evolution, and ongoing technological progress is expected to sustain adoption momentum across global healthcare systems.

Key Industry Developments

- In November 2025, Transatlantic began offering Transaflow® multi-patient syringe systems designed for contrast media administration in CT and MRI, with compatibility across common injector platforms and options for saline delivery based on clinical requirements. The systems emphasize hygienic safety through pathogen barriers, closed-system designs, and up to 24-hour usage capability, while supporting workflow efficiency and cost optimization in radiology environments.

- In July 2025, Antmed introduced a CT 200 ml/200 ml dual syringe kit designed for compatibility with multiple injector brands, aiming to improve efficiency, reliability, and safety in medical imaging procedures through streamlined preparation and single-use components. The solution supports faster contrast administration while reducing contamination risks and inventory complexity for healthcare facilities.

Companies Covered in High Pressure Syringes Market

- Bayer AG

- Bracco Imaging S.p.A.

- Medtron AG

- Guerbet Group

- Ulrich Medical

- Nemoto Kyorindo Co., Ltd.

- MEDRAD, Inc.

- Sino Medical Sciences Technology Inc.

- SciMed Life Systems

- Apollo RT Co., Ltd.

- Shenzhen Seacrown Electromechanical Co., Ltd.

- acist Medical Systems, Inc.

- Vivid Imaging, Inc.

- JMS Co., Ltd.

- Cook Medical

Frequently Asked Questions

The global high pressure syringes market is projected to reach US$ 1.7 billion in 2026.

The market is driven by increasing diagnostic imaging procedures for chronic diseases such as cancer and cardiovascular conditions.

The market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Major opportunities lie in emerging economies where the prevalence of chronic conditions is rapidly rising, smart syringe integration, and development of IoMT platforms.

Bayer AG, Bracco Imaging S.p.A., Medtron AG, Guerbet Group, and Ulrich Medical are some of the key players in the market.