- Food Ingredients & Additives

- Glaze and Icing Stabilizers Market

Glaze and Icing Stabilizers Market Size, Share, and Growth Forecast, 2026-2033

Glaze and Icing Stabilizers Market by Product Type (Hydrocolloids, Emulsifiers, Modified Starches, Protein-based Stabilizers), Application (Bakery, Confectionery, Desserts, Others), and Regional Analysis for 2026-2033

Glaze and Icing Stabilizers Market Share and Trends Analysis

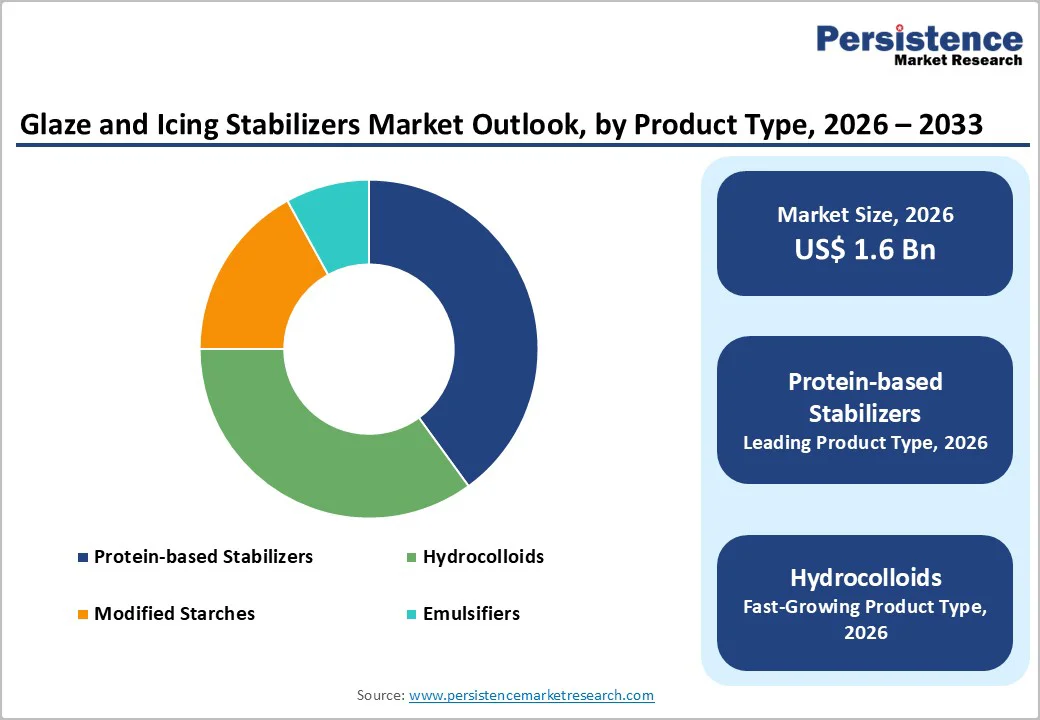

The global glaze and icing stabilizers market size is likely to be valued at US$ 1.6 billion in 2026 and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 5.3% for during the forecast period 2026-2033. This expansion reflects stronger consumption of packaged baked goods as consumers seek convenient, indulgent products that still deliver consistent quality. Food manufacturers increasingly rely on stabilizers to maintain texture, gloss, and shape in icings and glazes during processing, storage, and distribution, which reduces waste and protects brand perception. To capture this opportunity, suppliers should focus on solutions that perform reliably under freeze–thaw conditions, extended shelf life, and varied distribution climates. The demand for texture stability and visual appeal in desserts is also reinforcing the importance of food hydrocolloids and emulsifiers in industrial baking. These ingredients enable precise control of viscosity, aeration, and moisture retention, which helps bakeries standardize large-scale production while meeting sensory expectations in both traditional and better-for-you product lines. Increasing regulatory alignment on food additives, together with ongoing formulation innovation, supports broader global adoption by simplifying approvals and enabling cleaner-label offerings.

Key Industry Highlights

- Leading Product Type: Protein-based stabilizers are expected to command approximately 40% of market revenue in 2026, owing to their widespread application in traditional dairy, bakery, and dessert products.

- Fastest-Growing Product Type: Hydrocolloids are projected to be the fastest-growing with a CAGR of 5.8% from 2026 to 2033, driven by increasing adoption of plant-based protein alternatives.

- Dominant Application: Bakery applications are anticipated to account for nearly 48% of total consumption in 2026, while desserts are likely to record the fastest growth at 6.1% CAGR through 2033, supported by increasing chilled and frozen dessert consumption globally.

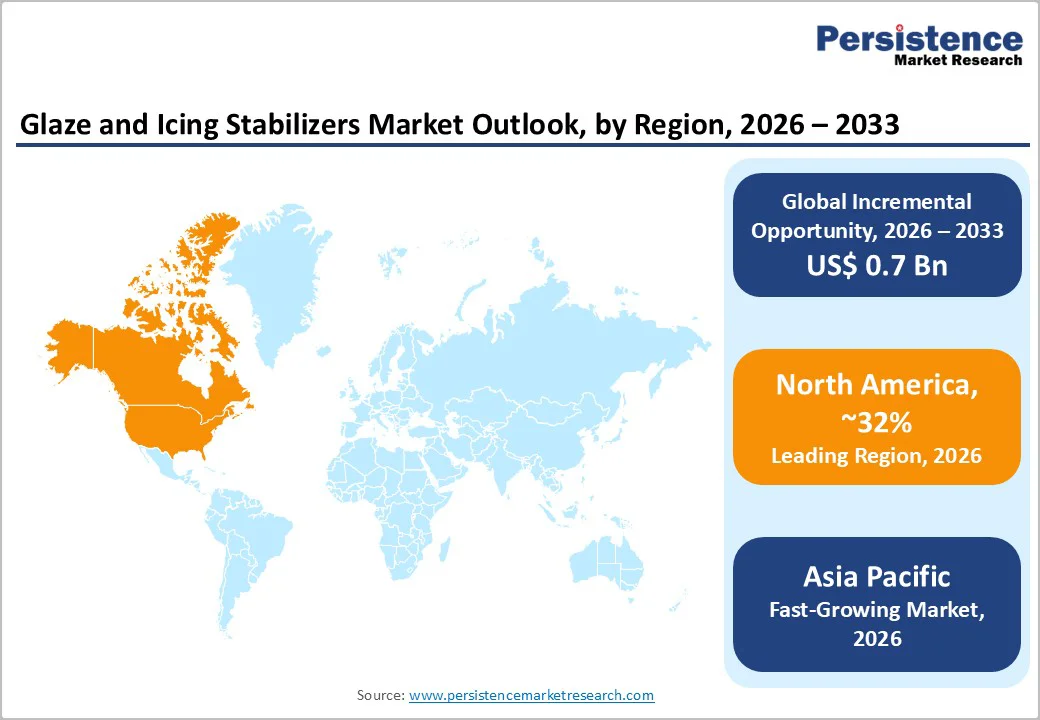

- Regional Leadership: North America is expected to command approximately 32% in 2026, while Asia Pacific is poised to be the fastest-growing market at 6.2% CAGR through 2033, driven by a widening acceptance of western-style baked goods.

| Key Insights | Details |

|---|---|

| Glaze and Icing Stabilizers Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Industrial Bakery Production and Demand for Functional Stabilizers

The growth of industrial bakeries and packaged desserts is driving strong demand for glaze and icing stabilizers, as manufacturers increasingly require precise texture control and visual consistency in high-volume production. Stabilizers such as modified starches and hydrocolloids are critical for preventing icing cracking, moisture migration, and gloss loss during storage and transportation, directly impacting product quality and reducing wastage. With processed foods contributing over 55% of daily caloric intake in developed economies, reliable stabilizer performance ensures operational efficiency and repeatable results across large batches, supporting recurring procurement and supplier stability.

Regulatory alignment and innovation further reinforce market adoption. Harmonized food additive standards simplify cross-border formulation and sourcing, while multifunctional, clean-label stabilizers combine emulsification, thickening, and moisture retention in a single ingredient system. These solutions enhance freeze-thaw stability, extend shelf life by up to 25%, and allow for consistent, glossy finishes that meet consumer expectations for premium bakery and confectionery products. The convergence of industrial growth, regulatory clarity, and ingredient innovation positions stabilizers as a core enabler of product differentiation and operational efficiency in the global bakery sector.

Raw Material Price Volatility and Regulatory Pressures

The glaze and icing stabilizers market growth is constrained by price volatility in critical raw materials such as gelatin, casein, starch derivatives, xanthan gum, and carrageenan. Gelatin prices have shown notable volatility due to fluctuations in the availability of raw materials such as pork and beef hides. These pressures have created significant regional price differences, with gelatin prices varying by as much as 19.4% between markets such as France and the United States. Similar volatility affects other stabilizers, driven by agricultural supply disruptions, climatic events, and global commodity fluctuations. These cost pressures directly impact stabilizer pricing and compress margins for small and mid-sized food manufacturers, particularly those producing baked goods and confectionery that rely on high-volume, consistent stabilizer procurement to maintain texture, moisture retention, and glossy finishes.

Evolving regulatory requirements and clean-label trends further restrict formulation flexibility. Increased scrutiny on labeling, especially in Europe, has limited the use of synthetic emulsifiers and mandated ingredient transparency. Manufacturers are investing in reformulation of legacy products, which can increase R&D expenditure by 10–15%, while still meeting consumer expectations for natural, plant-based stabilizers. Combined, raw material volatility and regulatory pressures create structural challenges that require strategic sourcing, ingredient innovation, and supply chain resilience to sustain profitability.

Growth Potential from Developing Economies and Clean-Label Innovation

Organized bakery and dessert products are anticipated to proliferate rapidly in Asia Pacific, Latin America, and the Middle East, where bakery markets are growing at rates exceeding 6% annually. Rising disposable incomes, urbanization, and the adoption of western-style baked goods are creating strong demand for cost-effective stabilizer systems tailored to regional formulations and climatic conditions. Industrial bakeries and confectionery manufacturers are increasingly seeking reliable ingredients that ensure consistent texture, moisture retention, and visual appeal across high-volume production.

Simultaneously, clean-label and plant-based stabilizers present a lucrative opportunity for market players. Ingredients such as hydrocolloids and protein-derived stabilizers command price premiums of 15–20%, driven by consumer preference for recognizable and natural components. Premium and artisanal dessert applications in Europe and North America further support value-driven growth, requiring high-performance stabilizers that maintain texture precision without sensory compromise. Emerging markets and clean-label innovation provide a pathway for margin expansion, product differentiation, and sustainable revenue growth.

Category-wise Analysis

Product Type Insights

Protein-based stabilizers, including gelatin and casein, are expected to lead the product-type segment, commanding around 40% of the revenue share in 2026, driven by their proven functionality in dairy, bakery, and dessert formulations. Their ability to deliver reliable texture stabilization, moisture retention, and gloss control supports consistent quality in high-volume and premium applications. Research published in the journal Gels in August 2025 demonstrates the effectiveness of fish skin gelatin hydrolysate in improving texture, overrun, and melting resistance in frozen desserts, further reinforcing the continued relevance of protein-based systems. Such innovations highlight the potential for more sustainable and functional protein stabilizers across glaze, icing, and dessert applications. Adoption remains strongest in mature markets where sensory performance and formulation reliability are critical.

Hydrocolloids are projected to be the fastest-growing product type, expanding at a CAGR of 5.8% from 2026 to 2033, supported by the soaring demand for plant-based and clean-label stabilizers. Nature-derived solutions such as CP Kelco’s Nutrava® citrus fiber and KELCOGEL® gellan gum exemplify this shift, offering water-binding, thickening, and stabilization while enabling simplified ingredient labels. These hydrocolloids are increasingly used as vegan alternatives to gelatin in bakery fillings, dessert gels, and confectionery coatings. The growth is particularly strong in Asia Pacific and Europe, where manufacturers are actively reformulating away from animal-derived ingredients. Modified starches, emulsifiers, and niche systems continue to complement hydrocolloids by addressing cost efficiency and specialized processing needs.

Application Insights

The bakery segment is projected to account for around 48% of the glaze and icing stabilizers market revenue share in 2026, making it the largest application category. High-volume production of cakes, pastries, donuts, and glazed breads drives demand for stabilizers to ensure texture consistency, moisture retention, and visual appeal. Industrial bakeries rely on these ingredients to prevent icing cracking and gloss loss, maintaining batch-to-batch uniformity. The segment benefits from rising packaged and ready-to-eat bakery consumption, especially in North America and Europe, while reducing product wastage and supporting operational efficiency across large-scale production.

The desserts segment is expected to be the fastest-growing application, with a CAGR of 6.1% from 2026 to 2033, fueled by the enormous demand for chilled, frozen, and premium desserts worldwide. Stabilizers are essential for controlled viscosity, smooth texture, and freeze-thaw stability, ensuring product quality. Confectionery applications grow moderately due to use in decorative coatings and fillings, while the other category covers niche, low-volume products. Increasing demand for premium, visually consistent, and clean-label desserts supports robust segment expansion and adoption.

Regional Insights

North America Glaze and Icing Stabilizers Market Trends

North America is expected to account for approximately 32% of the glaze and icing stabilizers market share in 2026. The regional market benefits from a mature bakery and dessert ecosystem, high industrial production intensity, and clear regulatory oversight under the U.S. Food and Drug Administration (FDA), enabling consistent use of approved stabilizers. Large-scale bakeries depend on stabilizers to deliver uniform texture, moisture control, and glossy finishes across mass production. Clean-label reformulation and premium dessert positioning continue to accelerate adoption. Demand is further supported by strong consumption of ready-to-eat and packaged bakery products.

Competition is led by multinational ingredient suppliers and specialized formulators focused on innovation, sustainability, and performance optimization. In 2025, for instance, Ashland Global Holdings, Inc. strengthened its North American strategy by promoting plant-derived and responsibly sourced stabilizers for confectionery and dessert coatings, aligning product portfolios with the environmental, social, & governance (ESG) targets of major food manufacturers. This initiative highlights the growing influence of traceability and sustainable sourcing on procurement decisions. Continued investment in multifunctional, clean-label stabilizers reinforces North America’s leadership in the global glaze and icing stabilizers market.

Europe Glaze and Icing Stabilizers Market Trends

Europe is likely to remain a key market, led by countries such as Germany, the U.K., France, and Spain. Regulatory harmonization under the European Food Safety Authority (EFSA) ensures consistent additive standards, simplifying formulation and cross-border sourcing. Stabilizers play a critical role in texture stabilization, shelf-life extension, and visual consistency across bakery and dessert products. Consumer demand for clean-label and sustainable ingredients continues to shape adoption trends. Artisanal bakery traditions and the popularity of premium desserts support steady growth. Industrial bakeries are increasingly adopting multifunctional stabilizers to meet evolving quality and performance expectations.

A mature industrial infrastructure, strong retail networks, and advanced production capabilities supporting innovation are factors favoring the market here. Manufacturers are investing in plant-based and multifunctional stabilizers to comply with regulations while maintaining product quality. Sustainability initiatives, ingredient transparency, and premium product demand reinforce Europe’s position as a mature and strategic market in the global glaze and icing stabilizers industry.

Asia Pacific Glaze and Icing Stabilizers Market Trends

Asia Pacific is projected to be the fastest-growing regional market for glaze and icing stabilizers, projected to expand at a CAGR of 6.2% from 2026 to 2033, driven by rapid industrial bakery expansion and modernization of retail networks. Key markets include China, India, and ASEAN countries, where rising disposable incomes, urbanization, and westernization of diets boost bakery and dessert consumption. High-volume industrial bakeries increasingly use stabilizers to maintain texture, moisture, and visual appeal. Cost-competitive manufacturing and operational efficiency encourage adoption of multifunctional stabilizers.

Regulatory frameworks are evolving and increasingly aligned with global standards, supporting broader stabilizer usage. Rising consumer demand for premium, clean-label, and plant-based products drives growth in both packaged and artisanal desserts. Investments in local manufacturing, capacity expansion, and innovation strengthen supply chains and adoption rates. The combination of high growth, expanding infrastructure, and evolving consumer preferences positions Asia Pacific as a critical growth hub for the market.

Competitive Landscape

The global glaze and icing stabilizers market structure is moderately consolidated, with leading players, including Cargill, Ingredion, DuPont, Kerry Group, and Tate & Lyle, collectively holding a significant share of global revenue. These established companies leverage their extensive food industry relationships, regulatory expertise, and integrated ingredient portfolios to maintain a competitive edge. They continuously invest in R&D for clean-label, multifunctional, and plant-based stabilizers, enabling product differentiation across bakery, dessert, and confectionery applications. Innovation in texture enhancement, moisture retention, and visual consistency remains a key focus to meet evolving consumer expectations.

Regional and niche competitors, such as CP Kelco and Givaudan, focus on specialized stabilizer segments and specific geographic markets. Entry barriers include regulatory compliance, quality certification requirements, and supply chain reliability. However, growing demand for clean-label formulations and plant-based solutions allows ingredient innovators and smaller companies to gain traction through partnerships, co-development, and customized solutions. Market consolidation is expected to increase gradually as global leaders acquire smaller firms to expand geographically and technologically, while collaboration between ingredient producers and food manufacturers accelerates innovation.

Key Industry Developments

- In August 2025, Vantage launched Perma-Frost No-Boil, an agar-based icing stabilizer, for commercial frosted baked goods. It eliminates the boiling step, cuts development time by up to 50%, reduces energy costs, and enhances production efficiency while maintaining quality.

- In July 2025, Tate & Lyle showcased an expanded hydrocolloid portfolio at IFT FIRST 2025, introducing advanced pectin and gum systems specifically designed to enhance texture, stability, and consistency in glazes and icings. These ingredients support bakery and dessert manufacturers in achieving improved mouthfeel, batch-to-batch uniformity, and clean-label compliance.

- In March 2025, Cargill launched a new line of plant-based, clean-label stabilizers at the AAHAR 2025 exhibition in India, including functional blends and texture systems derived from citrus peels and legumes. The launch also highlights a cost-effective pectin alternative and dent corn-based modified starch, addressing consumer demand for healthier, natural ingredients.

Companies Covered in Glaze and Icing Stabilizers Market

- Cargill, Inc.

- Ingredion Incorporated

- Tate & Lyle PLC

- Kerry Group plc

- DuPont de Nemours, Inc.

- Archer Daniels Midland Company

- CP Kelco

- Ashland Global Holdings, Inc.

- Palsgaard A/S

- Corbion N.V.

Frequently Asked Questions

The global glaze and icing stabilizers market is projected to reach US$ 1.6 billion in 2026.

Rising industrial bakery production, growing consumption of packaged desserts, demand for consistent texture and visual appeal, and increasing adoption of clean-label and multifunctional stabilizers are driving market growth.

The market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Emerging bakery and dessert markets in Asia Pacific and Latin America, rising demand for plant-based and clean-label ingredients, and premium dessert applications represent major growth opportunities.

Cargill, Ingredion, Tate & Lyle, Kerry Group, DuPont Nutrition & Biosciences, ADM, and CP Kelco are some of the leading global players.