- Advanced Materials

- Glass Reinforced Vinyl Ester Market

Glass Reinforced Vinyl Ester Market Size, Share, and Growth Forecast 2026-2033

Glass Reinforced Vinyl Ester Market by Resin Type (Bisphenol A, Novolac, Brominated Vinyl Ester, Other), Application (Pipes & Tanks, Marine Components, Automotive Parts, Building & Construction Materials, Electrical & Electronics Components, Other), End-use Industry (Chemical, Wastewater Treatment, Oil & Gas, Power Generation, Other), and Regional Analysis for 2026-2033

Glass Reinforced Vinyl Ester Market Size and Trend Analysis

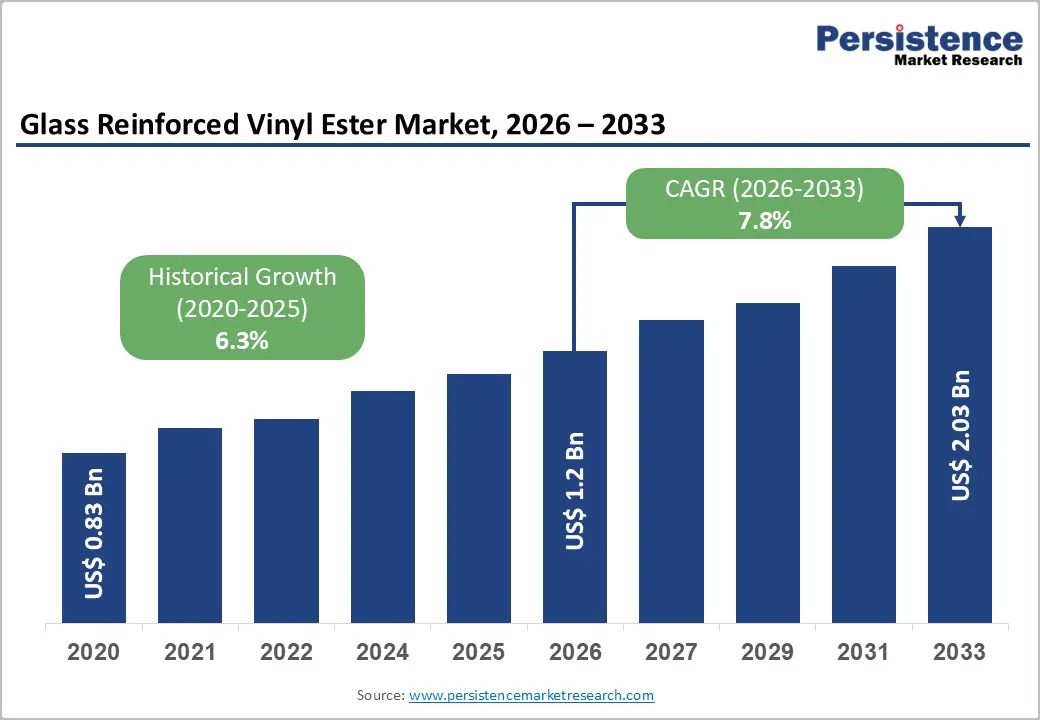

The global Glass Reinforced Vinyl Ester market size is supposed to be valued at US$ 1.2 Bn in 2026 and is projected to reach US$ 2.0 Bn by 2033, growing at a CAGR of 7.8% between 2026 and 2033.

The market is driven by accelerating investments in critical infrastructure modernization, particularly in wastewater treatment facilities and industrial manufacturing across emerging economies. Simultaneously, the global shift toward renewable energy deployment, coupled with stringent environmental regulations mandating corrosion-resistant materials in marine and chemical processing sectors, creates sustained demand for high-performance vinyl ester composites. Additionally, the electric vehicle revolution is fostering innovation in advanced composites for battery thermal management and structural protection, further expanding application scope across automotive and energy storage verticals.

Key Market Highlights

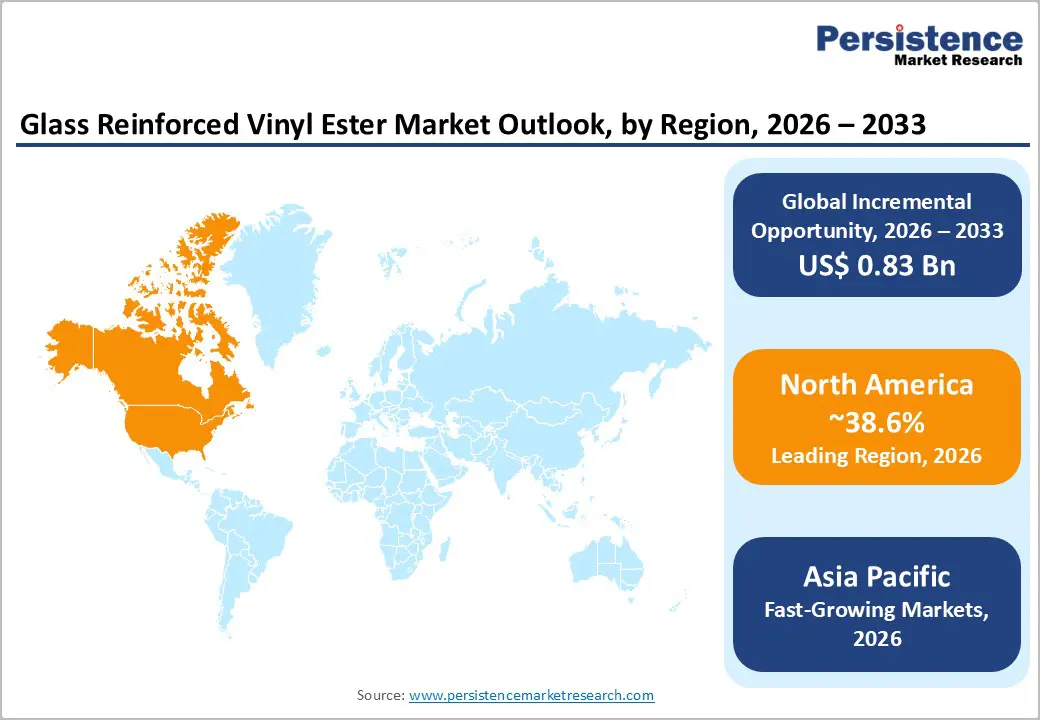

- Leading Region: North America dominates the Glass Reinforced Vinyl Ester Market with approximately 38.6% global market share, driven by stringent regulatory frameworks, advanced manufacturing infrastructure, and robust industrial demand across chemical processing, marine, and renewable energy sectors requiring high-performance corrosion-resistant composites.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing geographic region, expanding at 9.6% CAGR through 2033, propelled by rapid industrialization in China, massive wastewater treatment infrastructure investments in India under the National Mission for Clean Ganga, and emerging automotive lightweight composite applications across the region.

- Dominant Segment: Pipes and Tanks application segment commands approximately 43% market share, reflecting sustained demand for corrosion-resistant solutions in chemical storage, wastewater treatment, oil and gas operations, and industrial manufacturing applications where vinyl ester's chemical resistance properties provide superior value.

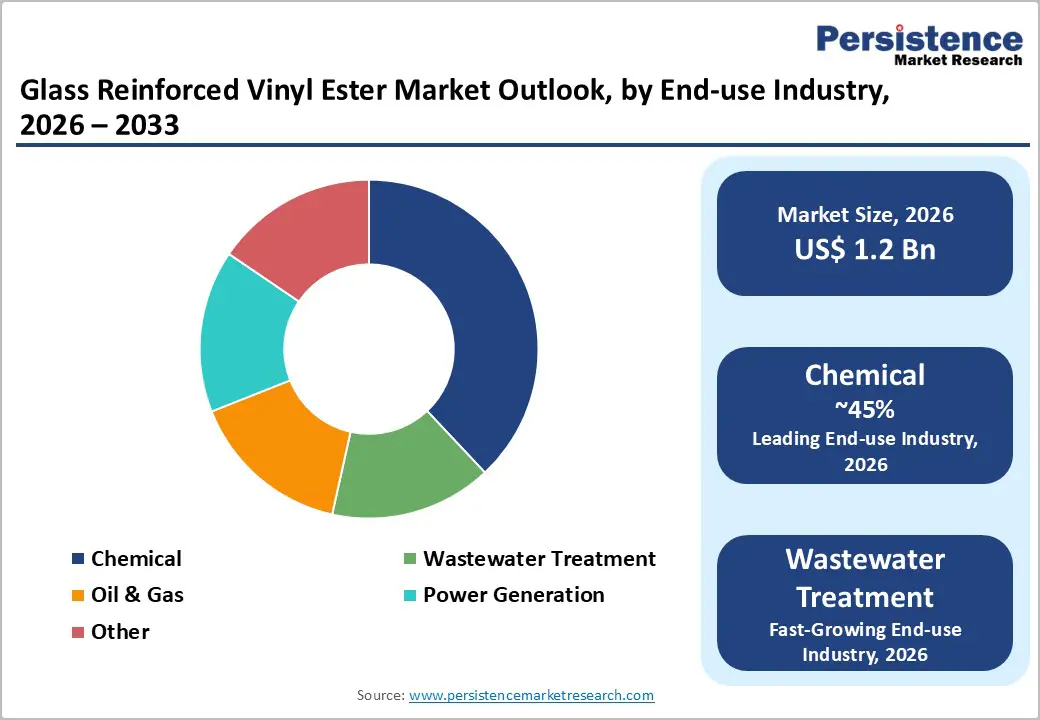

- Fastest Growing Segment: Wastewater Treatment emerges as the fastest-growing application segment, expanding at 6% CAGR during 2026-2033, driven by urbanization pressures, stricter environmental discharge regulations, and substantial public investment in municipal sewage infrastructure modernization globally.

- Key Market Opportunity: Offshore wind energy expansion and electric vehicle battery thermal management systems represent the highest-potential growth opportunities for market participants, as global renewable energy deployment and EV electrification acceleration drive unprecedented demand for lightweight, durable, corrosion-resistant composite materials through 2033.

| Key Insights | Details |

|---|---|

| Glass Reinforced Vinyl Ester Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth CAGR (2026-2033) | 7.8% |

| Historical Market Growth (2020-2025) | 6.3% |

Market Dynamics

Market Drivers

Rising Global Water and Wastewater Infrastructure Investments

Global governments are significantly increasing investments in water treatment infrastructure, driven by rapid urbanization, population growth, and stringent environmental compliance requirements. In India, the National Mission for Clean Ganga has approved 203 sewerage projects, delivering a treatment capacity of 6,255 million liters per day. Complementary initiatives such as the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) and Jal Jeevan Mission have mobilized substantial public and private funding.

The pipes and tanks segment accounts for approximately 44.7% of vinyl ester applications, owing to its superior resistance to acids, alkalis, and corrosive industrial effluents. Industrial water and wastewater infrastructure spending in India is projected to reach US$ 2.87 billion in 2024 and expand considerably through 2033, sustaining demand for durable, chemically resistant piping and storage solutions uniquely enabled by vinyl ester composites.

Growing Demand from Oil, Gas, and Power Generation Sectors

The oil and gas sector is increasingly utilizing vinyl ester-based composite pipes and vessels due to their superior performance in harsh, high-pressure environments containing sour gases, saline water, and chemical additives. These composite pipes deliver up to 80% weight reduction compared to carbon steel while ensuring exceptional leak-before-break characteristics and fatigue resistance under cyclic pressure conditions.

Standard polyester and vinyl ester resins can withstand continuous service temperatures of up to 180°F, making them highly suitable for offshore and upstream operations. Furthermore, power generation facilities employing flue gas desulphurization (FGD) systems depend on vinyl ester resin components for stack liners and absorber vessels. The widespread adoption of FGD technology, particularly in coal-fired plants across Asia, significantly drives material demand, reducing SO? emissions by as much as 64% in operational plants.

Market Restraints

Volatile Raw Material Costs and Supply Chain Disruptions

Vinyl ester resin formulation depends critically on styrene, creating direct exposure to petrochemical price volatility and supply constraints. Raw material cost fluctuations, compounded by geopolitical trade barriers and transportation disruptions, disproportionately impact small and medium-sized enterprises lacking financial resilience.

Manufacturing concentration in specific geographic regions heightens supply chain fragility, while competing feedstock demand from alternative industries creates cyclical price pressures. These dynamics elevate production costs unpredictably, constraining market expansion and limiting accessibility for price-sensitive industrial customers across developing economies.

Stringent Environmental and VOC Emission Regulations

European Union legislation restricting volatile organic compounds (VOCs) and hazardous air pollutants (HAPs) has effectively eliminated spray-up processing methods, historically accounting for a significant share of composites production. Styrene emission limits, compliance testing requirements, and manufacturing facility certifications impose substantial regulatory compliance costs.

The U.S. Environmental Protection Agency (EPA) and Occupational Safety and Health Administration (OSHA) enforce stringent material performance and worker safety standards, necessitating expensive reformulation, testing, and facility modifications. These regulatory burdens disproportionately disadvantage smaller manufacturers and emerging market producers, consolidating market share among compliance-capable multinational corporations while temporarily suppressing market growth in regulated jurisdictions.

Market Opportunities

Offshore Wind Energy Expansion and Renewable Infrastructure Development

Global renewable energy capacity additions are accelerating substantially, with offshore wind farms expanding across North America and European coastal regions requiring specialized, high-performance materials. Wind turbine blade manufacturing increasingly incorporates glass fiber reinforced composites using vinyl ester and epoxy resin matrices, leveraging superior mechanical strength-to-weight ratios and extended durability under extreme environmental stresses.

Leading manufacturers, including Ashland Global Holdings and Swancor Holding Company Limited, are actively developing next-generation vinyl ester formulations optimized for extended turbine blade lifespans. The technological shift toward larger, more efficient turbine designs drives material consumption per unit significantly higher, while government renewable energy targets across countries like India, China, and European nations create sustained demand visibility through the 2030s.

Electric Vehicle Battery Thermal Management and Emerging Lightweight Composite Applications

The electric vehicle industry is driving significant demand for advanced composite materials designed to enhance thermal runaway mitigation and crash protection. Modern battery pack housings increasingly incorporate hybrid composite structures utilizing vinyl ester polymer matrices reinforced with glass and carbon fibers.

Original equipment manufacturers are investing in composite battery enclosure technologies to achieve weight reduction, improved energy efficiency, thermal protection, and structural integrity. Concurrently, bio-based and sustainable vinyl ester formulations are gaining prominence as companies align with sustainability goals and regulatory standards. These advancements position market participants for accelerated growth as EV adoption reaches 30–40% of global vehicle sales by 2033.

Category-wise Insights

Resin Type Analysis

Bisphenol A (DGEBA) epoxy vinyl ester resins hold a dominant position in the market, accounting for nearly 55% share due to their status as the industry benchmark for diverse applications. Formulations such as Derakane 411-350 deliver exceptional chemical resistance, superior adhesion, and proven mechanical reliability across legacy manufacturing processes.

Regulatory endorsements from the U.S. Environmental Protection Agency (EPA) and Occupational Safety and Health Administration (OSHA confirm their suitability for hazardous industrial environments, while the American Composites Manufacturers Association (ACMA) validates compliance for marine applications under U.S. Coast Guard standards. This leadership is reinforced by established production infrastructure, mature supply chains, and comprehensive technical support from major suppliers, including INEOS Composites, Polynt-Reichhold, and Scott Bader. Their unmatched cost-performance balance ensures sustained market dominance throughout the forecast period.

Application Analysis

Pipes and tanks constitute the largest application segment, representing approximately 43% of market share, primarily driven by substantial investments in industrial chemical storage, wastewater treatment infrastructure, and oil and gas operations. Vinyl ester offers exceptional resistance to hydrochloric acid, sulfuric acid, sodium chloride, and various industrial solvents, providing a distinct advantage over polyester alternatives in highly corrosive environments.

Industry bodies such as the American Water Works Association (AWWA) and the U.S. Department of Energy (DOE) emphasize the critical need for durable, chemical-resistant piping systems to prevent environmental contamination and structural failures. Advances in continuous filament winding technology enable precise glass-to-resin ratios, producing lighter yet stronger pipes for high-pressure water transmission and irrigation networks. Regulatory mandates, including U.S. Coast Guard requirements for marine fuel tanks, further reinforce stable demand.

End-use Industry Analysis

The chemical processing industry remains the leading end-user segment, accounting for approximately 38% of market share due to vinyl ester’s critical role in manufacturing corrosion-resistant equipment. Producers in specialty chemicals and petrochemicals rely on fiber-reinforced plastics for storage tanks, piping systems, and processing vessels capable of withstanding aggressive chemical environments. Epoxy novolac-based vinyl ester resins, such as the Derakane 470 series, deliver superior thermal and chemical resistance, ensuring durability against solvents, acids, and oxidizing agents like chlorine and bleach, essential for chlor-alkali production, specialty polymers, and agrochemical applications.

Wastewater treatment represents the fastest-growing segment, expanding at over 6% CAGR during 2026–2033, driven by urbanization and stringent discharge regulations. Additionally, oil and gas operations and power generation facilities increasingly adopt vinyl ester composites for high-pressure, fatigue-resistant applications and FGD systems.

Regional Insights

North America Glass Reinforced Vinyl Ester Trends

North America holds a leading position in the global glass-reinforced vinyl ester market, accounting for approximately 38.6% share, supported by advanced technology, strict regulatory compliance, and diversified industrial applications. The U.S. market is driven by regulatory mandates and infrastructure modernization. Enforcement of performance standards by the EPA and OSHA promotes the adoption of premium composites, while U.S. Coast Guard requirements sustain fiber-reinforced plastic demand.

The American chemical industry, generating over US$ 500 billion annually, remains a key growth driver. Additionally, renewable energy initiatives, particularly wind turbine manufacturing backed by DOE funding, stimulate innovation. Mexico’s expanding marine and oil and gas sectors further enhance regional growth prospects.

Europe Glass Reinforced Vinyl Ester Trends

Europe represents a mature yet moderately declining market, holding approximately 28–32% of global share and facing structural challenges such as stringent regulations and rising manufacturing costs. Germany, historically the largest producer with an annual capacity of 225,000 tons, recorded a 13% year-over-year decline in 2024. EU environmental policies restricting VOCs and hazardous air pollutants have eliminated spray-up processing, compelling manufacturers to adopt costlier resin transfer molding (RTM) and filament winding techniques.

The European Federation of Reinforced Plastics (AVK) reported GRP pipes and tanks output at 104 kilotonnes in 2024, signaling sector-wide contraction despite ongoing infrastructure investments. The UK, France, and Spain maintain strong bases in marine, wind energy, and construction, while growing emphasis on bio-based vinyl ester formulations aligned with EU Green Deal objectives creates opportunities in premium segments.

Asia Pacific Glass Reinforced Vinyl Ester Trends

Asia Pacific is projected to be the fastest-growing region in the glass-reinforced vinyl ester market, with a CAGR of 9.6% during 2026–2033. This growth is fueled by rapid industrialization, large-scale infrastructure modernization, and expanding renewable energy projects. China dominates regional consumption, driven by rising demand in wind turbine blade manufacturing, automotive lightweight composites, and chemical processing equipment.

Strategic investments in petrochemical infrastructure further enhance opportunities for high-performance vinyl ester adoption. India represents the highest-growth market, with consumption expected to rise at 7.1% CAGR through 2031, supported by major wastewater treatment initiatives under programs such as the National Mission for Clean Ganga and AMRUT. Japan maintains steady demand at 5.7% CAGR, while Southeast Asian hubs like Vietnam, Thailand, and Indonesia attract multinational manufacturers, reinforcing Asia Pacific’s position as the global production epicenter.

Competitive Landscape

Market Structure Analysis

The glass-reinforced vinyl ester market is moderately consolidated, with leading multinational manufacturers controlling approximately 60% of the global share, while regional players and emerging suppliers serve niche segments. INEOS Composites, Polynt-Reichhold Group, and Scott Bader Company Ltd. dominate as technology leaders, leveraging advanced research, integrated supply chains, and strong customer relationships. Market leaders pursue vertical integration strategies, acquiring feedstock suppliers and downstream specialists to enhance profitability. Companies such as BASF SE, Hexion Inc., and Sika AG utilize diversified chemical portfolios to cross-sell vinyl ester systems, while Mitsubishi Corporation, Royal DSM, and Kraton Corporation focus on strategic partnerships and joint ventures. Asian manufacturers, including Swancor Holding Co., Ltd., compete aggressively on cost and delivery speed. Competitive advantage increasingly depends on technical support, customized formulations, regulatory compliance, and supply chain resilience rather than price alone.

Key Market Developments

- February 2024: Reichhold announces DION® 31040-00 vinyl ester resin optimized for high-performance maritime, industrial, and transportation applications, addressing market demand for next-generation corrosion-resistant systems.

- September 2024: Superlit GRP Pipes selected for Manyas Plain Sol Sahil Irrigation Project in Turkey, supplying 10 kilometers of continuous filament winding-produced GRP pipes for major agricultural infrastructure expansion, demonstrating market momentum.

- January 2025: Future Pipe Industries awarded a major contract to supply GRE pipelines for 520 well completions in Dubai, specifically replacing conventional steel infrastructure to enhance operational durability in challenging subsurface conditions.

Top Companies in Glass Reinforced Vinyl Ester Market

INEOS Composites (Dublin, Ohio, U.S.) maintains global market leadership following the acquisition of Ashland's composites polymer business through an integrated portfolio spanning Derakane epoxy vinyl ester resin systems, advanced composite solutions, and technical support infrastructure serving marine, chemical processing, wind energy, and infrastructure markets. The company's technological platform encompasses DGEBA and epoxy novolac-based formulations, catering to corrosion-resistant and high-temperature applications globally.

Polynt-Reichhold Group (headquartered in Italy) represents the second-largest global player with approximately 15-18% market share, leveraging integrated manufacturing, established customer relationships, and product innovation in unsaturated polyester and vinyl ester resins. The recent introduction of DION 31040-00 demonstrates a commitment to next-generation formulations addressing maritime, industrial, and transportation sectors requiring superior performance characteristics.

Scott Bader Company Ltd. (Northamptonshire, U.K.), an employee-owned global manufacturer established in 1921, captures approximately 10-12% market share through specialty vinyl ester resin portfolios, advanced composites, structural adhesives, and functional polymers serving aerospace, marine, automotive, and industrial sectors. The company's technical expertise in customized resin formulation and application support establishes competitive differentiation in premium market segments.

Companies Covered in Glass Reinforced Vinyl Ester Market

- Ashland Global Holdings Inc.

- Polynt-Reichhold Group

- Scott Bader Company Ltd.

- Interplastic Corporation

- Hexion Inc.

- BASF SE

- Mitsubishi Corporation

- Royal DSM

- Sika AG

- Kraton Corporation

- Swancor Holding Co., Ltd.

- INEOS Composites

- AOC

Frequently Asked Questions

The glass reinforced vinyl ester market is valued at US$ 1.2 billion in 2026 and is projected to reach US$ 2.0 billion by 2033, representing a 7.8% compound annual growth rate throughout the forecast period, driven by increasing infrastructure investments, renewable energy deployment, and industrial modernization initiatives globally.

The market is primarily driven by substantial global infrastructure investments in wastewater treatment facilities, growing renewable energy (wind turbine) demand, expanding oil and gas operations requiring corrosion-resistant materials, electric vehicle electrification accelerating composite battery thermal management adoption, and stringent environmental regulations mandating high-performance, durable materials across marine, chemical processing, and industrial sectors.

Pipes and tanks application segment commands the largest market share at approximately 43%, driven by sustained demand for corrosion-resistant solutions in chemical storage systems, industrial wastewater treatment infrastructure, oil and gas pipeline applications, and power generation facilities implementing FGD emission control systems.

North America maintains the dominant regional position, commanding approximately 38.6% global market share, supported by stringent regulatory compliance requirements (EPA/OSHA standards), advanced manufacturing capabilities, substantial industrial chemical industry demand, and consistent government support for wind energy and infrastructure modernization initiatives.

Offshore wind energy expansion and electric vehicle battery thermal management systems represent the highest-potential growth opportunities, as accelerating global renewable energy deployment and rapid EV electrification create unprecedented demand for lightweight, durable, corrosion-resistant composite materials offering superior performance characteristics through 2033.

INEOS Composites, Polynt-Reichhold Group, and Scott Bader Company Ltd. function as the dominant global manufacturers, supplemented by significant regional players including Hexion Inc., BASF SE, Swancor Holding Co., Ltd., Interplastic Corporation, and Sika AG, each pursuing specialized market segmentation and geographic expansion strategies.