- Executive Summary

- Global Flooring and Carpets Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Flooring and Carpets Market Outlook: Flooring Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Flooring Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- Market Attractiveness Analysis: Flooring Type

- Global Flooring and Carpets Market Outlook: Material Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Material Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- Market Attractiveness Analysis: Material Type

- Global Flooring and Carpets Market Outlook: Price Range

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Price Range, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- Market Attractiveness Analysis: Price Range

- Global Flooring and Carpets Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- Market Attractiveness Analysis: Application

- Global Flooring and Carpets Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- North America Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- North America Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- North America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- Europe Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- Europe Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- Europe Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- Europe Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- East Asia Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- East Asia Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- East Asia Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- East Asia Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- South Asia & Oceania Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- Latin America Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- Latin America Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- Latin America Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- Latin America Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- Middle East & Africa Flooring and Carpets Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Flooring Type, 2026-2033

- Carpets

- Tufting

- Woven

- Rugs

- Accent Rugs

- Area Rugs

- Other Rugs

- Artificial Grass

- Carpet Tiles

- Vinyl Flooring

- Laminate Parquet Flooring

- Concrete Flooring

- Wood Flooring

- Others

- Carpets

- Middle East & Africa Market Size (US$ Bn) Forecast, by Material Type, 2026-2033

- Synthetic Fibers

- Nylon

- Polyester

- Polypropylene

- Natural Fibers

- Wool

- Jute

- Other

- PVC

- Polyurethane

- Wood

- Stone

- Ceramic

- Other

- Synthetic Fibers

- Middle East & Africa Market Size (US$ Bn) Forecast, by Price Range, 2026-2033

- Economy

- Mid-Range

- Premium/Luxury

- Middle East & Africa Market Size (US$ Bn) Forecast, by Application, 2026-2033

- Residential

- Commercial Offices

- Retail

- Hospitality

- Healthcare and Hospitals

- Educational Institutes

- Automotive

- Industrial

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Mohawk Industries Inc

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Interface Inc.

- Beaulieu International Group N.V

- Tarkett S.A.

- Balta Group

- Shaw Industries Group, Inc.

- ALSORAYAI Group

- Forbo Holding AG

- Armstrong World Industries LLC

- Gerflor Group

- Milliken & Company Inc

- Betap Tufting B.V.

- Mannington Mills Inc.

- Karndean Designflooring

- Porcelanosa Group

- Pergo (Pfleiderer Group)

- Congoleum Corporation

- Polyflor Ltd.

- Mohawk Industries Inc

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Home Care & Utilities

- Flooring and Carpets Market

Flooring and Carpets Market Size, Share, and Growth Forecast 2026 - 2033

Flooring and Carpets Market by Flooring Type (Carpets, Rugs, Artificial Grass, Carpet Tiles, Vinyl Flooring, Laminate Parquet Flooring, Concrete Flooring, Wood Flooring, Others), Material Type (Synthetic Fibers, Natural Fibers, Wood, Stone, Ceramic, Other), Price Range (Economy, Mid-Range, Premium/Luxury), Application (Residential, Commercial Offices, Retail, Hospitality, Healthcare and Hospitals, Educational Institutes, Automotive, Industrial, Others), by Regional Analysis, 2026 - 2033

Flooring and Carpets Market Size and Trend Analysis

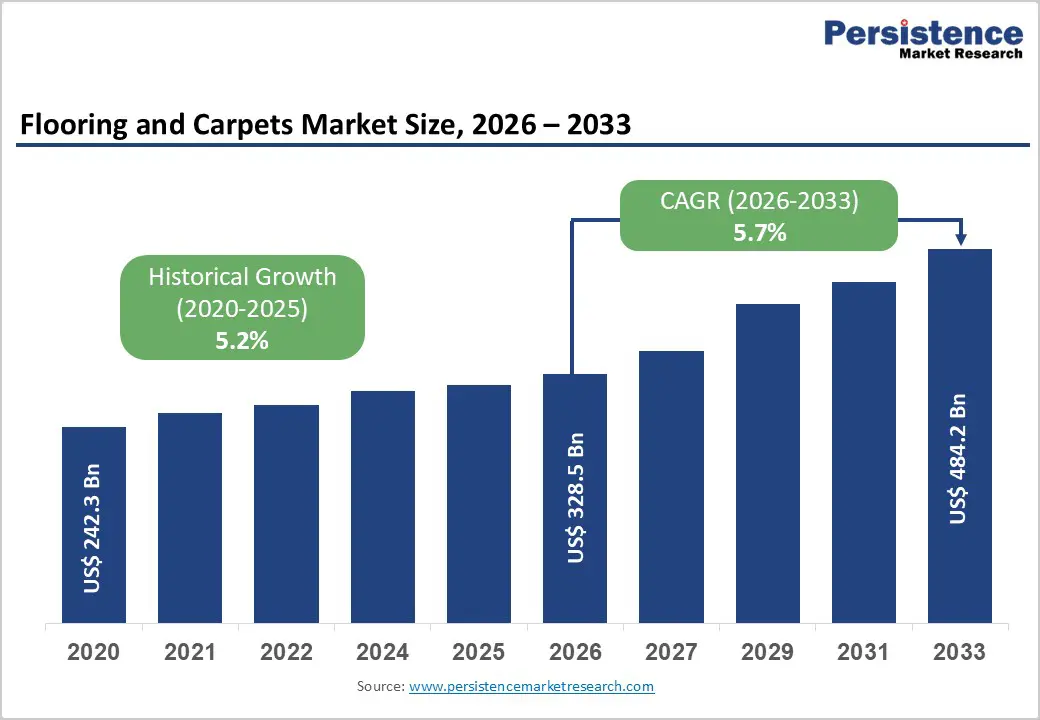

The global flooring and carpets market size is expected to be valued at US$ 328.5 billion in 2026 and projected to reach US$ 484.2 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

This robust expansion is primarily driven by accelerating global construction activity, a post-pandemic surge in residential renovation spending, and the rising preference for aesthetically differentiated, sustainable flooring solutions across both developed and emerging economies. According to the Global Construction Perspectives and Oxford Economics, global construction output is forecast to grow by 42% to reach USD 15.2 trillion by 2030, directly underpinning demand for flooring products across residential, commercial, and institutional segments. Parallel shifts in consumer preferences toward low-VOC, recyclable, and bio-based flooring materials, reinforced by tightening environmental regulations in the European Union and North America, are further reshaping product development priorities and driving premiumization trends across the value chain.

Key Industry Highlights

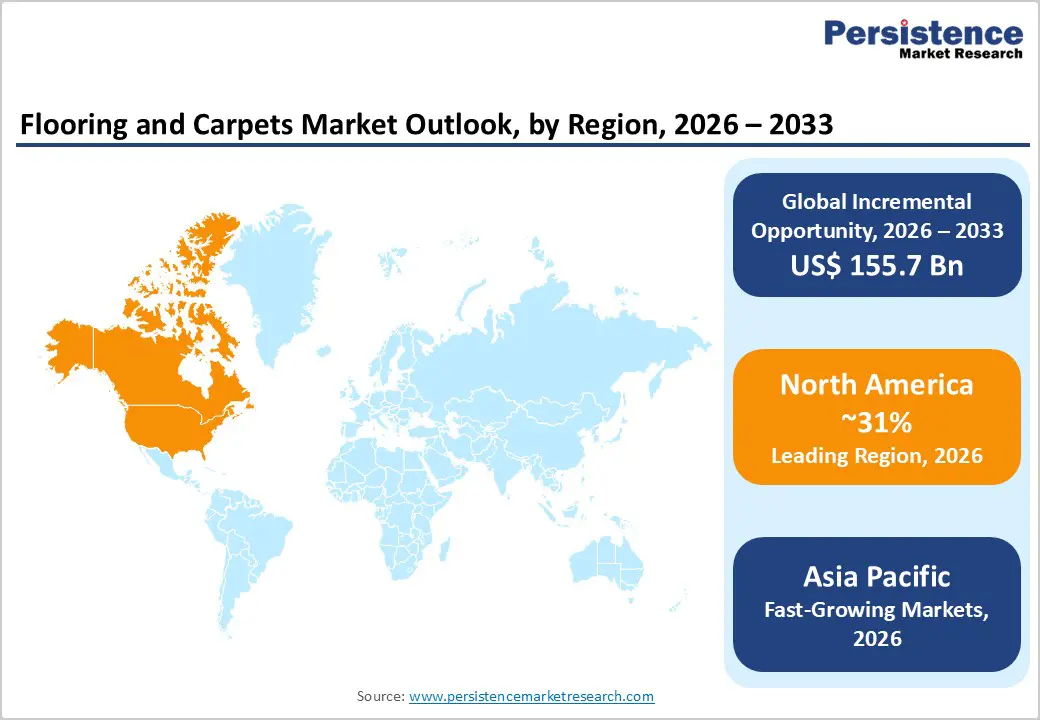

- Leading Region: North America leads the global flooring and carpets market with approximately 31% share in 2025, driven by U.S. residential renovation spending exceeding USD 480 billion annually and stringent CARB VOC compliance requirements reshaping product standards.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, propelled by China’s urbanization agenda, India’s PMAY housing programme targeting 20+ million new units, and ASEAN’s expanding role as a global flooring manufacturing and consumption hub.

- Dominant Segment: Vinyl flooring dominates the flooring type category with approximately 24% share in 2025, benefiting from LVT’s superior durability, waterproofing, and realistic aesthetics across residential renovation and commercial refurbishment applications globally.

- Fastest Growing Segment: Premium/luxury flooring is the fastest-growing price segment, driven by rising disposable incomes, booming hospitality construction pipelines exceeding 1.1 million hotel rooms globally, and growing consumer aspiration for engineered hardwood, natural stone, and designer area rugs.

- Key Opportunity: Key market opportunity lies in LVT and resilient flooring innovation for healthcare and commercial segments, where FloorScore and GREENGUARD Gold certifications provide significant specification advantages in LEED-certified construction, generating premium pricing power for compliant manufacturers.

| Key Insights | Details |

|---|---|

|

Flooring and Carpets Market Size (2026E) |

US$ 328.5 Billion |

|

Market Value Forecast (2033F) |

US$ 484.2 Billion |

|

Projected Growth CAGR (2026–2033) |

5.7% |

|

Historical Market Growth (2020–2025) |

5.2% |

Market Dynamics

Market Growth Drivers

Surging Residential Construction and Renovation Activity Globally

Escalating residential construction output and a sustained wave of home renovation expenditure represent the most powerful demand drivers for the global flooring and carpets market. The U.S. Census Bureau reported that private residential construction spending in the United States reached approximately USD 900 billion in 2023, with flooring constituting one of the highest-value interior finishing categories. Simultaneously, the Joint Center for Housing Studies at Harvard University (JCHS) estimated that U.S. home improvement spending exceeded USD 480 billion in 2023, with floor covering replacements ranking among the top five renovation categories by expenditure. In Europe, the European Construction Industry Federation (FIEC) documented sustained growth in residential retrofitting investment, particularly driven by EU energy efficiency directives requiring whole-building refurbishments. Across Asia Pacific, rapid urbanization, particularly in India, China, Vietnam, and Indonesia, is generating massive new housing stock requiring flooring installation, creating a structurally growing demand base for all product categories.

Growing Emphasis on Sustainable and Healthy Indoor Environments

Heightened consumer and regulatory focus on indoor air quality and environmental sustainability is profoundly reshaping product demand dynamics in the flooring and carpets market. The U.S. Environmental Protection Agency (EPA) identifies indoor air pollutants, including volatile organic compounds (VOCs) emitted by conventional flooring adhesives and synthetic materials, as a priority health risk, with indoor air quality estimated to be 2–5 times more polluted than outdoor air on average. This has accelerated demand for low-VOC, FloorScore-certified, and Cradle to Cradle-certified flooring products. The European Chemicals Agency (ECHA) has progressively restricted SVHC (Substances of Very High Concern) in flooring materials under REACH regulations, compelling manufacturers to reformulate products. Leading producers including Tarkett S.A. and Interface Inc. have responded with ambitious circular economy programmes, such as Interface’s ReEntry recycling initiative, that are increasingly influencing commercial procurement decisions in corporate real estate and healthcare segments.

Market Restraints

Volatility in Raw Material Prices and Supply Chain Disruptions

The flooring and carpets industry remains significantly exposed to raw material price volatility, particularly for petrochemical-derived inputs including nylon, polyester, polypropylene, and PVC, which collectively underpin the majority of synthetic flooring production. The U.S. Bureau of Labor Statistics (BLS) reported that producer prices for plastics materials and synthetic resins rose by over 30% between 2020 and 2022 before partially correcting, creating significant margin compression for mid-tier manufacturers. Supply chain disruptions, including port congestion, container shortages, and energy price spikes, further elevated input and logistics costs. Smaller independent flooring manufacturers with limited hedging capacity or backward integration have been disproportionately affected, constraining their ability to invest in product innovation or capacity expansion.

Skilled Labour Shortages in Flooring Installation

The professional flooring installation sector faces a structural skilled labour deficit that is constraining market growth, particularly in North America and Western Europe. The Floor Covering Industry Foundation (FCIF) in the U.S. has documented a persistent shortage of certified flooring installers, with the gap between qualified demand and available workforce estimated at tens of thousands of professionals. The U.S. Bureau of Labor Statistics (BLS) projects that flooring installer occupations will see employment growing at approximately 4% through 2032, yet training programme enrolments have not kept pace with industry demand. This shortfall results in longer project lead times, elevated labour costs, and in some cases, the deferral of renovation and construction projects, all of which dampen the velocity of flooring product installations and weigh on industry revenue realization.

Market Opportunities

Rising Demand for Luxury Vinyl Tile (LVT) and Resilient Flooring in Commercial Segments

Luxury vinyl tile (LVT) and broader resilient flooring categories represent one of the most significant growth opportunities for market participants over the 2026–2033 forecast period. The World Floor Covering Association (WFCA) has consistently identified LVT as the fastest-growing flooring category by volume in North America, driven by its exceptional durability, waterproof properties, low maintenance requirements, and increasingly realistic wood and stone aesthetics enabled by advanced digital printing technologies. The commercial segment, encompassing healthcare facilities, educational institutions, hospitality venues, and corporate offices, is exhibiting particularly strong LVT adoption, as facility managers prioritize life-cycle cost efficiency over upfront procurement price. The U.S. Green Building Council (USGBC) notes that LVT products certified under FloorScore and GREENGUARD Gold programmes are gaining substantial specification advantages in LEED-certified construction projects. Manufacturers investing in rigid-core LVT product lines and click-lock installation systems are positioned to capture outsized share in this high-growth category.

Customization and Digitalization in Premium and Hospitality Flooring Segments

The convergence of advanced digital printing technology, modular carpet tile systems, and mass customization manufacturing platforms is creating a compelling new revenue opportunity for flooring producers targeting the premium and hospitality segments. Global hotel construction pipelines remain robust, with STR Global reporting over 1.1 million hotel rooms under construction or in planning globally as of 2024, each requiring bespoke flooring specification and replacement cycles averaging 7–10 years. Leading companies including Interface Inc., Milliken & Company, and Shaw Industries Group are leveraging generative design software and digital inkjet printing to offer project-specific carpet patterns with minimum order quantities previously uneconomical for smaller installations. This democratization of custom flooring design significantly expands the addressable market within the premium segment, enabling providers to capture higher per-square-metre revenues. Simultaneously, the growth of direct-to-consumer e-commerce channels, with augmented reality (AR) room visualization tools, is driving premium rug and area rug sales growth in the residential segment.

Category-wise Insights

Flooring Type Analysis

Vinyl flooring, encompassing luxury vinyl tile (LVT), luxury vinyl plank (LVP), and sheet vinyl, is the leading product segment in the global flooring and carpets market, commanding an estimated market share of approximately 24% in 2025. This dominant position reflects the category’s unmatched combination of water resistance, dimensional stability, ease of maintenance, and cost-effectiveness relative to natural alternatives. The Resilient Floor Covering Institute (RFCI) in the United States has documented consistent year-on-year volume growth for resilient flooring categories, with LVT specifically displacing traditional ceramic tile and laminate in key refurbishment applications. In Europe, the European Resilient Flooring Manufacturers’ Association (ERFMI) reported that resilient flooring accounted for the highest share of new commercial flooring installations in 2022. Meanwhile, wood flooring represents the fastest-growing segment, propelled by biophilic design trends and premiumization in residential and hospitality construction.

Material Type Analysis

Synthetic fibers, encompassing nylon, polyester, and polypropylene, constitute the dominant material type in the global flooring and carpets market, with an estimated combined market share of approximately 38% in 2025. Nylon remains the premium choice within this cluster, valued for its superior durability, resilience, and soil-resistance properties that make it the preferred specification for high-traffic commercial carpet applications. The Carpet and Rug Institute (CRI) in the U.S. reports that nylon-based carpets continue to dominate commercial hospitality and healthcare procurement due to their ability to meet stringent performance standards including the NSF/ANSI 140 Sustainable Carpet Assessment Standard. Polyester, meanwhile, has captured growing residential market share owing to significant improvements in fiber stain resistance and the increasing availability of GRS (Global Recycled Standard)-certified recycled PET variants. PVC is the fastest-growing material driven by LVT adoption across commercial and residential renovation projects globally.

Price Range Analysis

The mid-range price segment leads the global flooring and carpets market, accounting for an estimated 46% of total market value in 2025, reflecting the broad consumer base that prioritizes a balance between quality, aesthetics, and affordability in both residential renovation and new construction contexts. According to the National Association of Home Builders (NAHB) in the U.S., the majority of new residential construction projects specify flooring products in the USD 3–8 per square foot installed range, a price band that squarely encompasses the mid-range segment for carpet, LVT, and laminate categories. Retail home improvement chains such as The Home Depot and Lowe’s report that mid-range flooring products consistently account for the highest volume and revenue share of their floor covering departments. The premium/luxury segment is the fastest-growing price tier, driven by rising disposable incomes, hospitality refurbishment activity, and heightened consumer aspiration for natural stone, engineered hardwood, and designer rug products.

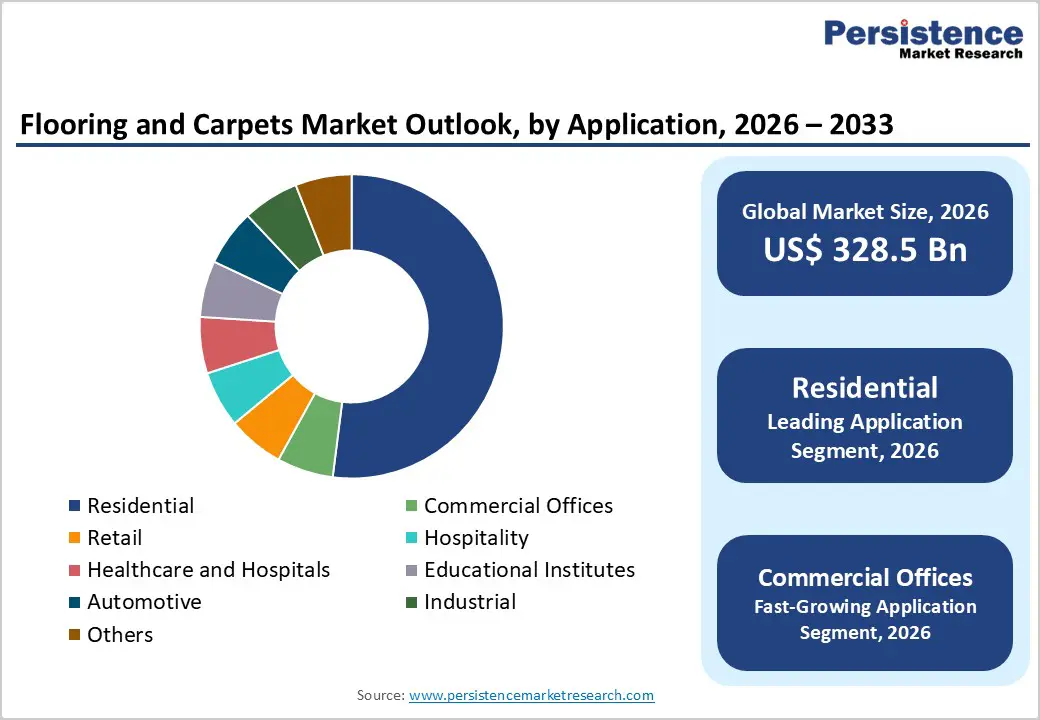

Application Analysis

The residential application segment leads the global flooring and carpets market with an estimated share of approximately 52% in 2025, underpinned by the sheer volume of global housing stock requiring periodic flooring replacement and the sustained pace of new residential construction across both mature and emerging markets. The United Nations Human Settlements Programme (UN-Habitat) estimates that the world needs to build approximately 96,000 housing units per day between 2015 and 2030 to meet urbanization-driven demand, a construction imperative that directly translates into structurally high flooring product demand. Post-pandemic behavioral shifts, including the widespread adoption of hybrid work models that increased time spent at home, have also elevated homeowner willingness to invest in premium interior surfaces, further boosting residential flooring expenditure per unit. The commercial offices segment is among the fastest-growing applications, driven by large-scale post-pandemic corporate real estate refurbishments incorporating biophilic and wellness-oriented interior design principles.

Regional Insights

North America Flooring and Carpets Market Trends and Insights

North America holds the leading position in the global flooring and carpets market, accounting for an estimated 31% share in 2025, anchored by the United States which remains the world’s largest single-country flooring market. The U.S. Floor Covering Weekly reported total U.S. floor covering shipments valued at over USD 31 billion in 2022, with residential replacement activity constituting the largest demand driver. The National Association of Realtors (NAR) documented over 5 million existing home sales in 2023, each representing a potential flooring upgrade or replacement opportunity. Regulatory momentum under programmes such as the California Air Resources Board (CARB) Phase 2 standards, among the world’s strictest VOC emission limits for flooring products, continues to drive product reformulation and green certification adoption across the industry.

Landmark corporate sustainability commitments by leading U.S. manufacturers are further reshaping the competitive landscape. Shaw Industries Group, a Berkshire Hathaway subsidiary, has publicly committed to achieving zero waste to landfill and carbon neutrality across its operations, while Mohawk Industries Inc. has introduced the SmartStrand and EverStrand recycled-content carpet lines that have gained significant market traction. Innovation in digital visualization tools and direct-to-consumer e-commerce platforms is also reducing traditional retail friction in flooring purchase decisions, expanding the addressable consumer base.

Europe Flooring and Carpets Market Trends and Insights

Europe represents the second-largest regional market for flooring and carpets, with Germany, the United Kingdom, France, and the Netherlands collectively constituting the core demand centres. The European Flooring Industry (CEN/TC 134) standardization framework provides regulatory harmonization across member states, facilitating cross-border trade and enabling manufacturers to pursue pan-European distribution strategies. Germany’s robust construction and renovation sector, supported by KfW Bank Group subsidies for energy-efficient building refurbishment under programmes aligned with the EU Energy Performance of Buildings Directive (EPBD), generates sustained demand for premium flooring solutions compatible with underfloor heating systems, a specification increasingly common in northern European residential construction.

The United Kingdom’s flooring market is characterized by strong carpet heritage, with Balta Group and Betap Tufting B.V. maintaining significant production presences in European markets, alongside rapidly growing LVT and engineered wood segments. Tarkett S.A. and Forbo Holding AG are prominent pan-European players leveraging circular economy credentials and take-back programmes to differentiate in environmentally sensitive commercial procurement processes. The European Green Deal and EU Ecodesign Regulation are progressively tightening sustainability requirements for flooring products sold in EU markets, compelling accelerated R&D investment in bio-based and fully recyclable product architectures.

Asia Pacific Flooring and Carpets Market Trends and Insights

Asia Pacific is the fastest-growing regional market for flooring and carpets, with China, India, Southeast Asia, and Japan representing the primary growth engines over the 2026–2033 forecast period. China remains the world’s largest flooring manufacturer and a rapidly growing domestic consumer, with the China National Building Material Group and numerous regional players serving an urbanizing population of over 1.4 billion. The country’s 14th Five-Year Plan has prioritized the construction of affordable urban housing, with the government targeting the construction of tens of millions of subsidized housing units, each requiring flooring installation, across Tier 2 and Tier 3 cities.

India presents one of the most compelling growth opportunities globally, with the Ministry of Housing and Urban Affairs (MoHUA) reporting over 11 million housing units constructed under the Pradhan Mantri Awas Yojana (PMAY) scheme through 2024, with an expanded pipeline targeting an additional 20 million units in subsequent phases. The Association of Southeast Asian Nations (ASEAN) region, particularly Vietnam, Indonesia, Malaysia, and Thailand, is simultaneously experiencing rapid flooring manufacturing capacity expansion, as global brands seek cost-competitive production bases alternative to China. Japan’s market, while more mature, is exhibiting renewed demand for premium tatami alternatives and resilient flooring in the context of earthquake-resilient construction standards enforced by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT).

Competitive Landscape

The global flooring and carpets market demonstrates a moderately consolidated structure at the premium tier, where a limited number of multinational manufacturers command significant global revenues through diversified product portfolios and strong brand positioning. However, the broader market remains highly fragmented, characterized by numerous regional mills, contract manufacturers, and niche specialty producers serving localized residential and commercial demand. Competitive intensity is shaped by scale advantages in procurement, automation-driven manufacturing efficiencies, and extensive dealer and retail networks.

Leading participants increasingly pursue vertical integration strategies spanning raw material sourcing, in-house fiber production, advanced finishing technologies, and proprietary distribution channels to safeguard margins and ensure supply stability. Sustainability has become a central strategic pillar, with investments in recycled content integration, closed-loop take-back systems, environmental product declarations (EPDs), and low-VOC certifications to secure commercial project specifications. Simultaneously, digital transformation initiatives, including online visualization tools, omnichannel retailing, and smart factory deployment, are redefining customer engagement and operational competitiveness across global markets.

Key Developments

- November, 2025: Tarkett launched its Resonant Spaces Ethos carpet tile collection designed to enhance work environments with improved acoustics, comfort, and design flexibility for commercial interiors.

- August, 2025: Interface launched its Stellar Horizons space-inspired carpet tile collection, featuring six cosmic-themed styles designed for commercial flooring applications with recycled and bio-based materials.

- August, 2025: Milliken launched its Renasci™ resilient flooring, made from about 80% reclaimed carpet and 20% soft plastic waste, offering a fully recyclable, low-carbon alternative to traditional flooring products.

Companies Covered in Flooring and Carpets Market

- Mohawk Industries Inc.

- Interface Inc.

- Beaulieu International Group N.V.

- Tarkett S.A.

- Balta Group

- Shaw Industries Group, Inc.

- ALSORAYAI Group

- Forbo Holding AG

- Armstrong World Industries LLC

- Gerflor Group

- Milliken & Company Inc.

- Betap Tufting B.V.

- Mannington Mills Inc.

- Karndean Designflooring

- Porcelanosa Group

- Pergo (Pfleiderer Group)

- Congoleum Corporation

- Polyflor Ltd.

Frequently Asked Questions

The global flooring and carpets market is estimated to be valued at US$ 328.5 billion in 2026.

Growth is driven by rising residential construction and renovation spending, along with increasing demand for low-VOC and sustainable flooring materials.

North America leads the market with an estimated 31% share in 2025, supported by strong U.S. residential and commercial renovation activity.

Luxury vinyl tile (LVT) and resilient flooring for commercial applications represent the most significant growth opportunity.

Leading players include Mohawk Industries, Shaw Industries, Interface, Tarkett, Forbo, Beaulieu International Group, Balta Group, Armstrong World Industries, Gerflor, Milliken, ALSORAYAI Group, and Mannington Mills.