- Sensors & Controls

- Flood Warning Systems Market

Flood Warning Systems Market Size, Share, and Growth Forecast 2026 - 2033

Flood Warning Systems Market by Component (Sensors, Software, Communication Devices, Data Management Systems, Integration Platforms), by Technology (Hydrological Modelling, Remote Sensing, IoT & Telemetry Platforms, Data Analytics & Nowcasting), Flood Type (Riverine (Fluvial) Flood Systems, Flash Flood Warning Systems, Coastal / Storm Surge Systems, Urban (Pluvial) Flooding), End-user, Regional Analysis, 2026 - 2033

Flood Warning Systems Market Size and Trend Analysis

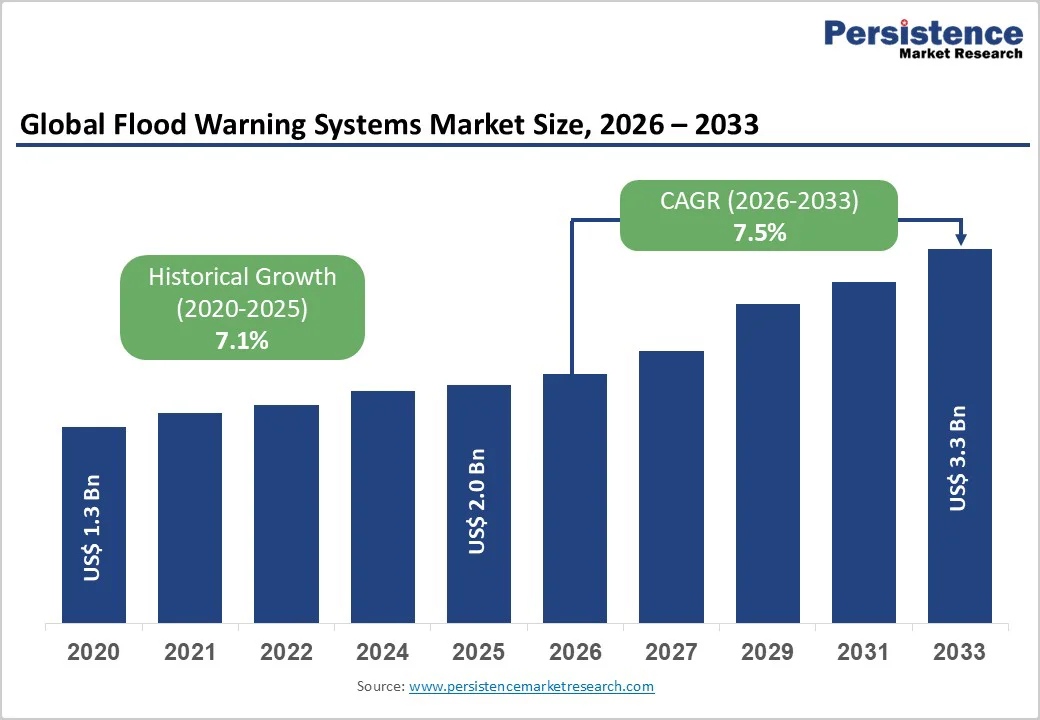

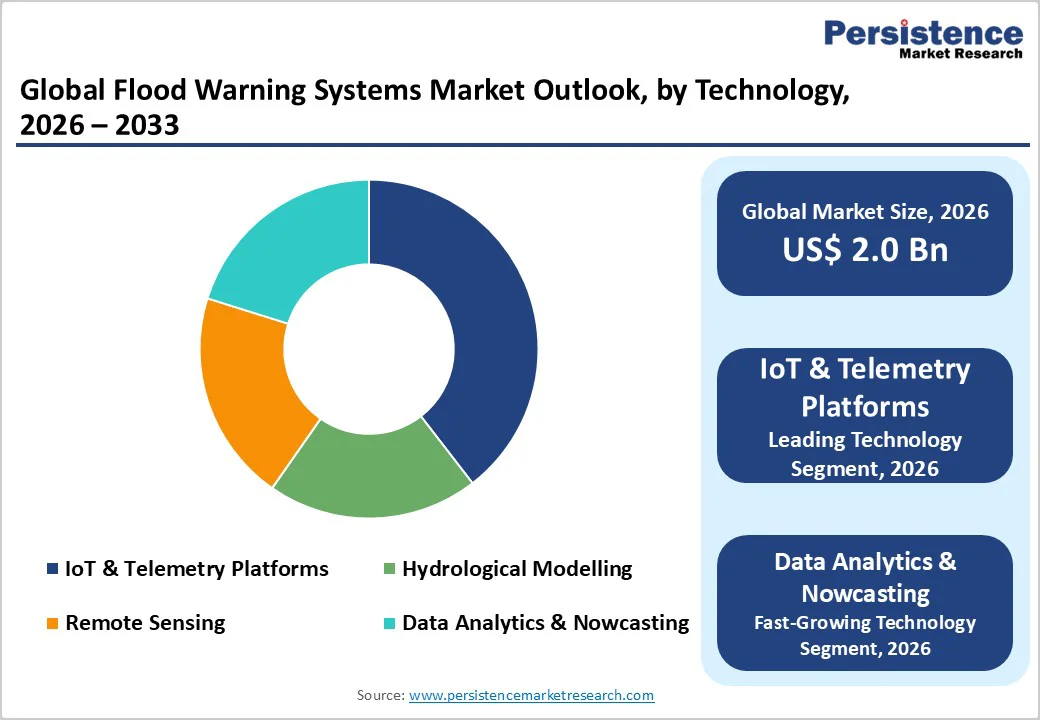

The global flood warning systems market size is likely to be valued at US$2.0 billion in 2026 and projected to reach US$3.3 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033. This robust expansion is driven by escalating climate change impacts, including the increased frequency and intensity of flooding worldwide, coupled with substantial governmental and private-sector investments in infrastructure modernization.

The market growth is further propelled by technological advancements in artificial intelligence and machine learning, as well as the integration of the Internet of Things (IoT), which enables more accurate flood prediction and real-time monitoring, allowing organizations to provide critical warnings that save lives and minimize economic losses. According to recent global data, 605 extreme weather events occurred in 2024, displacing 824,500 people, underscoring the urgent need for advanced flood-warning infrastructure across all regions.

Key Industry Highlights

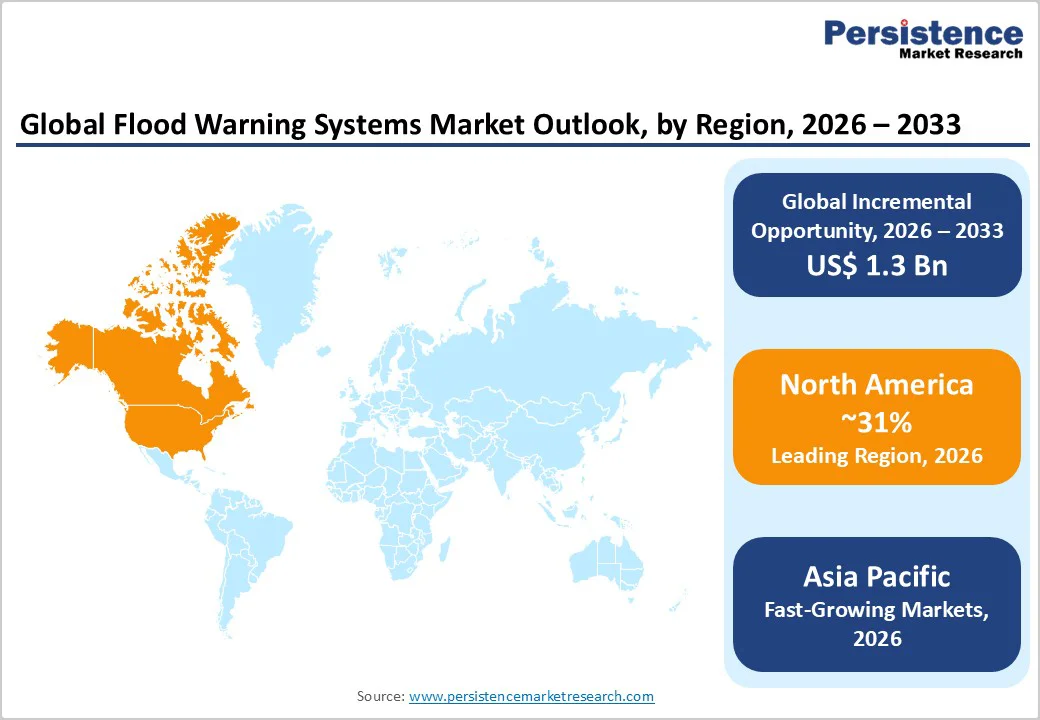

- Leading Region: North America holds about a 31% share in 2025, supported by advanced infrastructure, strong federal funding, and extensive sensor networks across U.S. River Forecast Centers and municipal early warning systems.

- Fastest Growing Region: Asia Pacific is expected to achieve a 9.5% CAGR to 2033, driven by intensifying monsoons, rapid urbanization in flood-prone zones, and government programs strengthening disaster resilience across China, India, Japan, and Southeast Asia.

- Dominant Segment from Component Category: Software accounts for roughly 42% of the market in 2025, reflecting rising dependence on hydrological modelling, analytics, alert platforms, and digital twin systems that form the computational core of modern flood warning infrastructure.

- Fastest Growing Segment from Technology Category: Data analytics and nowcasting record 8.8% CAGR through 2032, propelled by demand for real-time precipitation nowcasts, hydrodynamic modelling, and predictive intelligence supporting faster, more accurate flood-risk decision making.

- Key Market Opportunity: Flash-flood warning solutions grow at a 9.5% CAGR through 2032, requiring dense urban sensors, real-time nowcasting, automated alerts, and integrated emergency response systems to address increasingly frequent high-intensity rainfall events.

| Key Insights | Details |

|---|---|

|

Flood Warning Systems Market Size (2026E) |

US$2.0 billion |

|

Market Value Forecast (2033F) |

US$3.3 billion |

|

Projected Growth CAGR(2026-2033) |

7.5% |

|

Historical Market Growth (2020-2025) |

7.1% |

Market Dynamics

Drivers - Climate Change and Extreme Weather Events Intensification

The increasing frequency and severity of flooding incidents driven by climate change represent the primary growth catalyst for the flood warning systems market. Data from 2024 reveals that climate change contributed to devastating floods affecting millions, with 15 of 16 studied flood events being driven by climate change-amplified rainfall. The fundamental physics of warming demonstrates that a warmer atmosphere holds approximately 7% more moisture per degree Celsius, directly translating to heavier precipitation and heightened flood risks.

Governments and enterprises worldwide are recognizing that traditional flood management approaches are insufficient, prompting substantial capital allocation toward state-of-the-art monitoring and early warning infrastructure. Asia Pacific remained the world’s most disaster-hit region in 2023, with floods and storms causing the highest casualty counts and economic losses, underscoring critical investment requirements for flood-warning technologies across vulnerable geographies.

Government Mandates and Regulatory Framework Development

Government initiatives and regulatory requirements are catalyzing market expansion as nations establish legal frameworks mandating flood risk assessment and the deployment of early warning systems. The European Union’s Floods Directive (2007/60/EC) mandates that member states assess flood risks, map vulnerable areas, and implement coordinated mitigation measures in six-year cycles, with the current implementation cycle covering 2022-2027. In the United States, the National Weather Service has operated nationwide River Forecast Centers for over 50 years, while recent trends indicate increased state and municipal investments in localized flood early warning systems.

The U.S. National Weather Service issued record numbers of flash flood warnings in 2025, approaching levels unseen in nearly four decades, triggering heightened demand for advanced monitoring technologies. These regulatory requirements establish baseline demand for sensors, data management systems, communication devices, and integration platforms, directly expanding the addressable market for flood warning solution providers.

Restraints - High Capital Investment Requirements and Infrastructure Gap

Implementing comprehensive flood warning systems demands substantial upfront capital investment, particularly in developing economies where resources are constrained, and infrastructure requires modernization from foundational levels. A complete system deployment requires the acquisition of sophisticated sensor networks, SCADA communication infrastructure, hydrological modelling software, cloud-based data management platforms, and integration services, with total system costs ranging from millions to billions of dollars, depending on geographic coverage and technological sophistication.

In regions such as South Asia, Southeast Asia, and Sub-Saharan Africa, approximately 90% of mountainous flood-prone areas face severe financing constraints that limit the adoption of advanced monitoring technologies. The economic burden of deploying and maintaining these systems creates significant barriers for lower-income countries where flood prevention must compete with other critical infrastructure priorities.

Technical Complexity and Data Integration Challenges

The heterogeneous nature of flood warning system components, encompassing diverse sensor types, communication protocols, forecasting methodologies, and dissemination channels, creates substantial technical complexity that hinders rapid deployment and scalability. Integration of real-time sensor data from multiple sources, including weather stations, satellite imagery, radar systems, and hydrological models, requires sophisticated data assimilation techniques and computational resources. Communication infrastructure in remote and flood-prone areas often lacks reliability, with unreliable wireless connectivity, limited satellite coverage, and vulnerable infrastructure preventing timely data transmission. Technical gaps in seamless data integration across jurisdictions, particularly in transboundary river basins, compound these challenges, as demonstrated by flood management complexities in regions such as the Danube River Basin and the Indus Basin, where coordination failures have historically exacerbated flood damages.

Opportunity - Artificial Intelligence and Machine Learning Integration for Enhanced Forecasting

Significant opportunities exist in leveraging advanced machine learning algorithms and artificial intelligence to enhance flood prediction accuracy and extend forecast lead times beyond traditional hydrological modelling capabilities. Google’s AI-based global flood-forecasting system has successfully extended forecast reliability from 0 to approximately 5 days across multiple regions, and the technology is now operational in 80 countries, covering areas where 460 million people reside. Machine learning models excel at identifying complex non-linear relationships within high-dimensional environmental datasets, demonstrating superior performance compared to conventional statistical approaches in regions with sparse hydrological data.

The Ministry of Environment in the Republic of Korea has deployed 223 AI-based flood-forecasting locations using advanced Long Short-Term Memory (LSTM) models that learn from historical and real-time data to predict water levels at 10-minute intervals, showcasing the transformative potential of AI integration. Companies developing proprietary machine learning platforms tailored to regional flood characteristics, incorporating predictive capabilities and automated warning dissemination, stand to capture significant market share as organizations prioritize early warning accuracy.

Urban Flood Management and Pluvial Flood Monitoring Systems Expansion

The accelerating urbanization, projected to reach 68% of the global population by 2050, creates substantial market opportunities for urban pluvial flood warning systems designed to address flash flooding in densely populated areas. Urban flooding, triggered by intense rainfall that overwhelms drainage infrastructure capacity rather than riverine overflow, requires specialized sensor networks, real-time hydrodynamic modelling, and rapid-response alert mechanisms that are distinct from riverine flood systems. Low-cost IoT sensor networks using LoRa (Long Range) and MQTT (Message Queuing Telemetry Transport) enable the deployment of distributed water-level monitoring across city stormwater infrastructure, creating cost-effective early-warning capabilities for municipalities.

Rio de Janeiro, Brazil, successfully deployed Vaisala’s X-band weather radar in March 2023 to address critical measurement gaps, integrating high-resolution precipitation data into emergency operations centers to enhance urban flood forecasting. Cities globally are increasingly recognizing that traditional drainage systems are inadequate for climate-intensified precipitation events, driving investment in smart urban water infrastructure that integrates real-time monitoring with predictive modelling and automated response mechanisms.

Category-wise Analysis

Component Insights

Software remains the dominant component in the global flood warning systems market, accounting for roughly 42% of the market in 2025 due to its central role in processing, modelling, and disseminating critical flood intelligence. Modern software platforms integrate hydrological models, AI-driven analytics, and digital-twin environments to transform raw sensor inputs into actionable early warnings. As agencies deploy dense IoT-based sensor networks, software capabilities have become essential for managing high-frequency data streams, executing predictive algorithms, and distributing alerts across multiple communication channels. The rapid shift toward cloud-native architectures and embedded machine learning enhances scalability, automation, and accuracy, making software the strategic backbone of next-generation flood warning infrastructure globally.

Technology Insights

IoT and telemetry platforms lead the technology landscape, with around a 37% share in 2025, reflecting their essential role in enabling distributed, real-time flood-monitoring networks. These platforms integrate water-level sensors, rain gauges, flow meters, and atmospheric instruments into unified communication frameworks that continuously transmit data to cloud analytics engines. Their ability to operate across long distances, withstand harsh environments, and deliver high-frequency measurements significantly improves situational awareness. Edge processing capabilities at sensor nodes enable pre-filtering and anomaly detection, reducing bandwidth needs and improving system reliability during connectivity disruptions. By providing granular spatial visibility and faster response times, IoT telemetry has become the foundational technology supporting modern flood resilience initiatives.

Flood Type Insights

Riverine flood warning systems dominate the global market with about 45% share in 2025, supported by decades of institutional investment in river basin monitoring and regulatory frameworks governing hydrological risk management. These systems offer longer forecast windows, ranging from 24 hours to several days, allowing authorities to deploy staged alerts and coordinate evacuations effectively. Riverine modelling integrates upstream hydrology, catchment characteristics, soil moisture data, and meteorological inputs, making accuracy heavily reliant on robust sensor networks and cross-basin data exchange. Given the high population density along major rivers worldwide, riverine systems remain essential for protecting urban settlements, agricultural zones, and critical infrastructure from large-scale inundation events.

End-user Insights

Governments and civil defence agencies are the largest end-user group, representing nearly 48% of market demand in 2025, owing to their central role in safeguarding lives, property, and essential services during flood events. Public-sector bodies operate integrated flood forecasting centres, coordinate emergency communication networks, and manage infrastructure protection measures across cities, towns, and rural regions. Their investments typically span radar networks, telemetry grids, modelling software, and multi-agency alerting platforms, enabling them to support transportation departments, utilities, disaster management authorities, and local municipalities. As climate-driven flooding intensifies, governments continue to expand budgets for predictive analytics and real-time monitoring systems, reinforcing their global leadership in early warning deployment.

Regional Insights

North America Flood Warning Systems Market Trends

North America demonstrates robust adoption of flood warning systems, driven by advanced technological infrastructure, substantial government funding, and heightened climate change awareness among stakeholders. The United States allocates significant resources to maintaining and modernizing its National Weather Service River Forecast Center network, complemented by state and municipal investments in localized flood early-warning systems. Federal and state programs prioritize interoperability standards enabling seamless data exchange across jurisdictional boundaries, cybersecurity protocols protecting critical infrastructure, and integration with public alerting channels, including wireless emergency alerts and commercial media platforms.

The region holds 31% of the global market share. In comparison, the United States market represents approximately 92% of North American flood warning system spending, valued at approximately US$ 570 million in 2025 and projected to grow at a 5.1% CAGR through 2033. Significant investment momentum derives from hurricane intensity, tropical cyclone impacts, and flash flood frequency across vulnerable regions, including the Gulf Coast, Southeast, and Southwest. Texas, Louisiana, and Florida lead regional adoption of advanced flood monitoring systems, with state agencies implementing ALERT (Automated Local Evaluation in Real Time) systems that integrate precipitation, streamflow, and reservoir-level data for operational flood forecasting.

Europe Flood Warning Systems Market Trends

Europe emphasizes coordinated basin-scale flood risk management through cross-border data-sharing mechanisms and compliance with the EU Floods Directive, establishing harmonized standards for flood risk assessment, mapping, and early-warning system deployment across member states.

Investment focuses on pluvial and fluvial flood risk mitigation, with enhanced early-warning dissemination across multilingual communication channels to address diverse stakeholder populations. Urban adaptation projects integrate Sustainable Urban Drainage Systems (SUDS) data with green-blue infrastructure monitoring, connecting flood dashboards to municipal and transportation authorities for integrated risk communication.

Germany leads European adoption of flood warning systems, with a market valued at about US$180 million in 2025, growing at a 6.1% CAGR through 2033, reflecting substantial infrastructure modernization following catastrophic 2002 and 2013 flood events. United Kingdom markets emphasize stringent environmental regulations and climate change adaptation strategies, driving demand for reliable flood monitoring. France and Spain implement progressive flood management policies incorporating real-time monitoring integrated with environmental protection objectives, supporting market growth at a 6.4% CAGR, respectively, through the forecast period.

Asia Pacific Flood Warning Systems Market Trends

Asia Pacific is the fastest-growing regional market, with an anticipated CAGR of 9.5% between 2025 and 2032, driven by rising extreme weather, rapid urbanization in flood-prone regions, and government policies prioritizing disaster preparedness and community resilience. The area experiences disproportionate flood impacts relative to other natural hazards, with approximately 80% of 79 documented hydro-meteorological disasters in 2023 classified as flood and storm events, affecting over 2,000 people with 2 million directly impacted.

China emerges as the regional market leader with a flood warning system market valued at approximately US$300 million in 2025, projected to grow at a 9.0% CAGR through 2033, reflecting rapid urbanization in flood-prone areas and government policies emphasizing disaster preparedness. India is the fastest-growing market in Asia Pacific, with an estimated CAGR of 11.4% between 2025 and 2032, driven by rising flood frequency, government efforts to enhance flood risk management through agencies such as the Central Water Commission, and the adoption of satellite-based monitoring and AI-powered forecasting systems. Japan maintains advanced flood-monitoring infrastructure that incorporates Digital Twin technologies and AI-based forecasting systems, deployed at 223 locations, providing near-real-time river water-level predictions at 10-minute intervals.

Competitive Landscape

The global flood warning systems market exhibits a moderately consolidated competitive structure with leading technology providers commanding significant market share while innovation-focused startups capture emerging niches in specialized technologies. Multinational equipment manufacturers such as Siemens AG, Honeywell International Inc., and Vaisala Oyj leverage established relationships with government agencies, utilities, and transportation authorities to offer integrated solutions combining sensors, software, and integration services. These enterprises invest substantially in research and development to advance the integration of artificial intelligence, machine learning algorithms, and IoT platform capabilities.

Strategic initiatives emphasize the development of cloud-based software platforms that enable scalable deployment across multiple sites without requiring on-premises infrastructure, the integration of AI and machine learning capabilities to enhance forecasting accuracy, and the establishment of partnerships with system integrators and regional technology providers. Emerging technologies, including digital twins, edge computing, and satellite-based monitoring, generate incremental revenue opportunities as customers pursue more sophisticated operational capabilities.

Key Market Developments

- September 2025: Vaisala launched enhanced hail-forecasting in Xweather Protect, combining lightning detection and radar data to deliver 60-minute-advance alerts, supporting solar and infrastructure operators with rapid, automated protective decision-making.

- November 2024: Google extended its AI-driven Flood Hub platform to 80 countries, providing river-flood forecasts up to seven days ahead for 460 million people, improving accuracy especially in data-scarce African and Asian regions.

Companies Covered in Flood Warning Systems Market

- Siemens AG

- Honeywell International Inc.

- Vaisala Oyj

- Schneider Electric SE

- Campbell Scientific Inc.

- Teledyne Technologies Incorporated

- Sutron Corporation

- HWM-Water Ltd.

- Riverside Technology, Inc.

- Xylem Water Solutions

- Bharat Electronics Limited

- L3Harris Technologies, Inc.

- SEBA Hydrometrie GmbH & Co. KG

- Stevens Water Monitoring Systems, Inc.

- AWI

- Google Research (AI Forecasting)

- Vassar Labs

Frequently Asked Questions

The market is projected to reach US$ 3.3 billion by 2033, growing from US$ 2.0 billion in 2026 at a 7.5% CAGR.

Demand is driven by worsening climate-related floods, regulatory requirements, and advances in AI, ML, and IoT-based monitoring.

Riverine Flood Systems lead with about 45% share in 2025, while flash flood systems grow the fastest.

Asia Pacific shows the fastest growth with a projected 9.5% CAGR from 2025 to 2032.

The major opportunity lies in Flash Flood Warning Systems, expanding at 9.5% CAGR due to rising urban flood risks.

Key players include Siemens, Honeywell, Vaisala, Campbell Scientific, Teledyne, Xylem, SEBA Hydrometrie, Stevens Water, and Google Research.