- Industrial Machinery

- Fire Pump Market

Fire Pump Market Size, Share, and Growth Forecast 2026– 2033

Fire Pump Market by Product Type (Horizontal Split Case, Vertical Split Case, Others), Source (Diesel Engine, Electric Motor, Others), Application (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Fire Pump Market Size and Trends Analysis

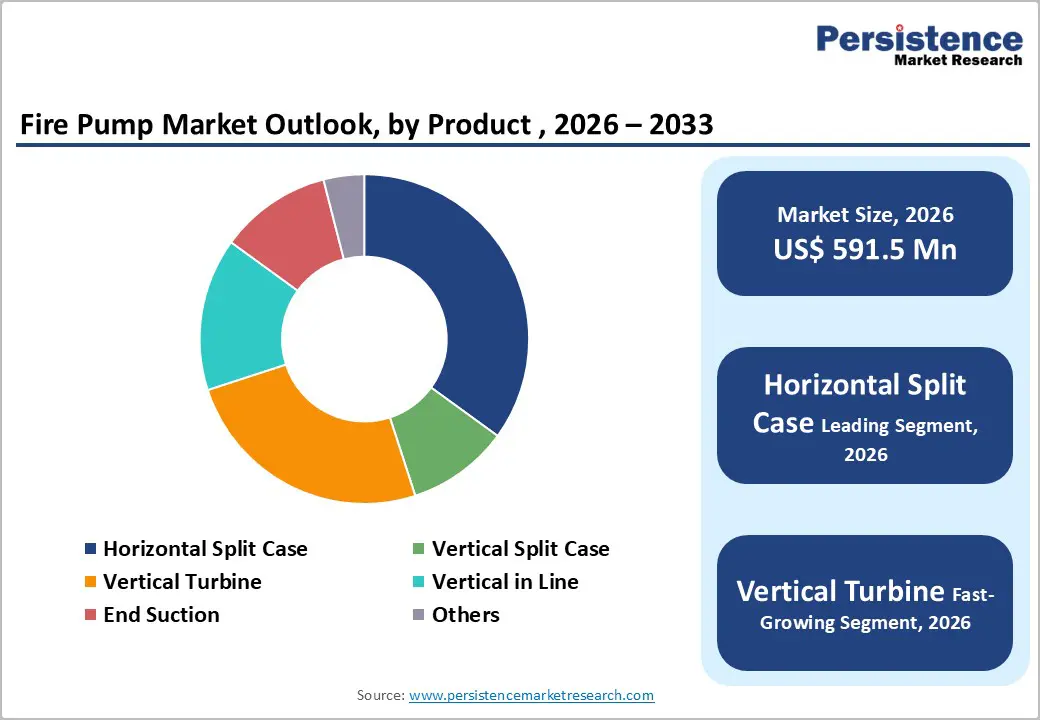

The global fire pump market size is likely to be valued at US$591.5 million in 2026 and is expected to reach US$757.7 million by 2033, growing at a CAGR of 3.6% during the forecast period from 2026 to 2033, driven by stricter fire-safety regulations across residential, commercial, and industrial buildings, alongside rapid urbanization and high-rise construction in both developed and emerging economies. Rising investments in critical infrastructure, such as airports, metro networks, data centers, logistics hubs, and public utilities, are driving demand for compliant fire protection systems. Growth is particularly fueled by high-risk industrial sectors such as oil & gas, power generation, chemicals, and manufacturing, where reliable and redundant fire water systems are essential.

Key Industry Highlights:

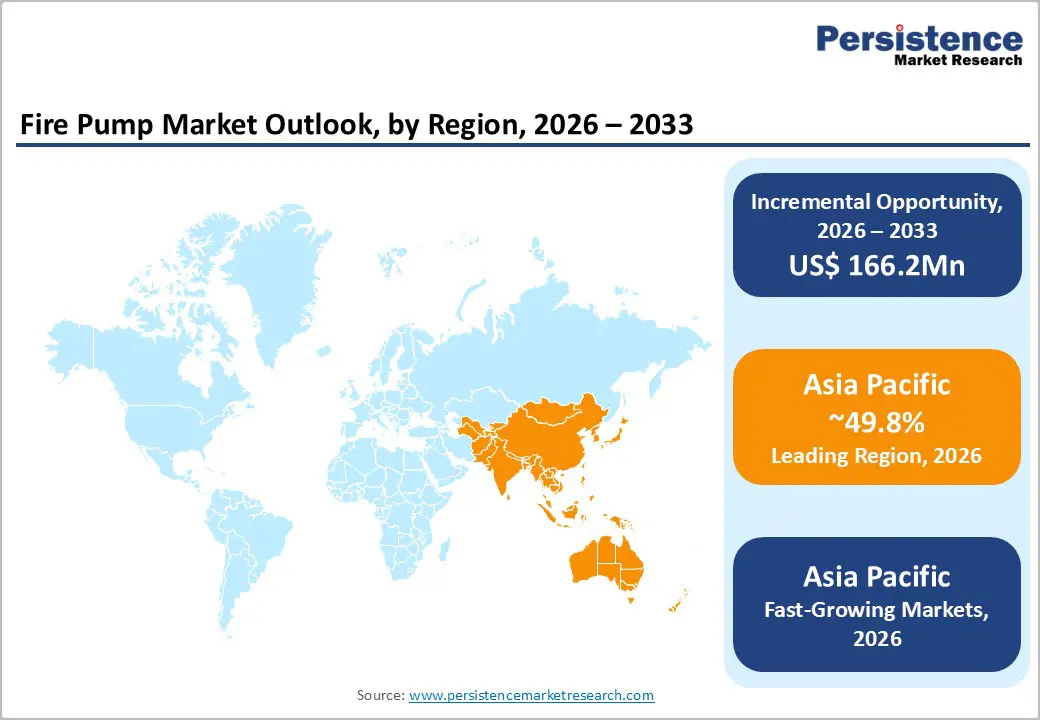

- Leading Region: Asia Pacific is expected to lead the market with around 49.8% share in 2026, driven by rapid urbanization, large-scale infrastructure development, and expanding industrial and commercial construction.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, driven by increasing adoption of advanced fire-safety systems, expanding manufacturing activities, and rising investments in metro networks, airports, and industrial corridors.

- Leading Product Type: Horizontal split case is anticipated to lead with a 40% revenue share, driven by its high reliability, easy maintenance, and suitability for high-flow applications in commercial, industrial, and infrastructure facilities.

- Leading Source Type: The electric motor segment is expected to lead, with 55% revenue share, driven by its lower operating costs, simpler maintenance, and strong adoption in commercial and institutional facilities with reliable power infrastructure.

- Leading Application Type: The commercial is projected to lead with about 50% revenue share, driven by stringent fire-safety codes, high pump capacities in offices, malls, hospitals, and public buildings, and ongoing retrofit activity in non-residential infrastructure.

| Key Insights | Details |

|---|---|

| Fire Pump Market Size (2026E) | US$591.5 Mn |

| Market Value Forecast (2033F) | US$757.7 Mn |

| Projected Growth CAGR (2026-2033) | 3.6% |

| Historical Market Growth (2020-2025) | 2.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancement and Digitalization of Fire Protection Systems

Technological advancements and the digitalization of fire protection systems are transforming the fire pump market, offering greater reliability, predictive maintenance, and smarter operational control. Modern fire pumps increasingly feature integrated sensors, cloud connectivity, and real-time monitoring platforms, allowing facility managers to remotely track pressure, flow rate, pump temperature, vibration patterns, and overall system readiness. These innovations minimize downtime by detecting faults early and automating compliance reporting for audits and inspections. Advanced analytics and AI-driven diagnostics help predict component wear, optimize testing schedules, and extend equipment lifespan. Remote access capabilities enhance response times and reduce on-site maintenance costs, particularly for large, multi-site facilities.

Digitalization is further driven by safety regulations, insurance requirements, and the shift toward smart buildings and industrial environments. Fire pump manufacturers are now offering intelligent panels with automated weekly testing, event logging, and seamless integration with building management systems (BMS) for centralized monitoring and control. Rising investments in data centers, metro rail networks, airports, and large industrial complexes are fueling demand for connected, cyber-secure fire pumping systems. Cybersecurity measures, redundancy protocols, and fail-safe designs are increasingly standard to ensure system reliability during emergencies.

High Upfront Costs and Capex Sensitivity

High upfront costs and capital expenditure sensitivity continue to be significant barriers in the fire pump market, especially for small and medium-sized enterprises and residential developers. Fire pump systems, particularly those designed for high-capacity industrial applications or high-rise commercial buildings, require substantial investments in equipment, installation, controllers, piping, and integration with broader fire protection infrastructure. These high capital requirements can result in project delays, downsizing of systems, or adoption of lower-spec alternatives, limiting market penetration in developing regions. The adoption of advanced or digitally monitored fire pumps is particularly affected, as their initial costs are higher than conventional systems.

Economic uncertainties, fluctuating construction activity, and tighter financial conditions further make end users cautious about committing capital to non-revenue-generating systems such as fire pumps, despite their essential safety function. High installation and lifecycle costs, including maintenance and periodic testing, add to ownership concerns. In many emerging markets, limited access to financing and weaker enforcement of fire-safety codes exacerbate these challenges, slowing adoption across residential, commercial, and industrial sectors. To address these barriers, vendors may need to offer flexible financing options, modular solutions, or phased deployment strategies to enhance accessibility and encourage broader market uptake.

Emerging Markets and Code Enforcement Catch?Up

Emerging markets are presenting significant growth opportunities for the fire pump industry, fueled by rapid urbanization, industrialization, and large-scale infrastructure development. Countries across Asia Pacific, the Middle East, and parts of Africa are witnessing a rise in high-rise residential buildings, commercial complexes, manufacturing facilities, and public infrastructure such as airports, metro networks, and ports. This growth is driving demand for reliable fire protection systems, including high-capacity pumps that comply with modern safety standards. Increased awareness of fire risks and the need for insurance-compliant systems further support market expansion, as businesses and public organizations prioritize safety and operational continuity.

Stronger enforcement of fire-safety codes in these regions is boosting the adoption of advanced fire pump systems, creating demand across residential, commercial, and industrial sectors. As building and infrastructure standards modernize, developers and facility managers are increasingly investing in compliant, high-capacity fire protection solutions, broadening the market’s potential. Government incentives, stricter inspections, and mandatory retrofitting of older structures are accelerating uptake, while OEMs are responding with modular, technologically advanced, and cost-effective systems.

Category-wise Analysis

Product Type Insights

The horizontal split-case segment is expected to lead, accounting for approximately 40% of the total revenue in 2026. Its popularity is driven by high reliability, ease of maintenance, and suitability for high-flow applications in medium- to large-scale commercial and industrial facilities. Horizontal split-case pumps are widely used in North America and Europe as standard solutions for sprinkler and hydrant systems, delivering both volume and value. For instance, Armstrong Fluid Technology’s 750?GPM vertical in-line and horizontal split-case pumps are commonly used in U.S. commercial complexes.

The vertical turbine segment is projected to be the fastest-growing product type, fueled by increasing demand in industrial, energy, and infrastructure projects that require high-capacity or deep-well pumping. Vertical turbine pumps are particularly suited for facilities sourcing water from tanks or underground reservoirs, including refineries, petrochemical plants, and large industrial sites. For example, Firefly Fire Pumps’ vertical turbine models are deployed in Indian industrial corridors and petrochemical facilities, while Sulzer’s vertical turbine pumps support water supply and firefighting systems in major Southeast Asian energy projects. Rising construction of high-rise buildings, industrial complexes, and large commercial facilities is further driving demand for these efficient and reliable pumps.

Source Type Insights

The electric motor segment is projected to dominate, capturing approximately 55% of the revenue share in 2026, driven by its widespread use in commercial and institutional buildings with reliable utility power and backup generators. These pumps are commonly installed in high-rise buildings, hospitals, airports, shopping malls, and educational institutions, providing dependable fire protection. For example, Xylem’s Bell & Gossett electric pumps are deployed in major U.S. hospital complexes, while Grundfos electric motor-driven pumps serve commercial skyscrapers in Singapore and office parks in Germany. Modern units often incorporate advanced digital controllers and automated testing, enabling facility managers to monitor pressure, flow, and system readiness remotely.

The electric motor segment is also expected to be the fastest-growing, driven by decarbonization initiatives, energy-efficiency regulations, and updated fire-safety codes in both developed and emerging markets. Features such as lower operating costs, minimal emissions, quiet operation, and long service life make these pumps particularly suited for large-scale commercial and industrial applications. For instance, Pentair electric pumps are used in U.S. data centers and logistics hubs, while Wilo electric fire pumps support industrial plants and high-rise residential projects in India. Integration with building management systems (BMS) and smart fire-safety networks further enhances operational efficiency and overall safety.

Application Type Insights

The commercial segment is expected to dominate, accounting for around 50% of revenue. This growth is driven by offices, retail spaces, hospitality venues, healthcare facilities, educational institutions, and public buildings, where strict fire-safety codes and high pump capacities per site generate strong demand. Continued urbanization, high-rise construction, and the refurbishment of older buildings, often requiring mandatory retrofitting with modern fire pump systems, further support this segment. For example, Pentair’s electric motor-driven fire pumps are installed in Singapore’s Marina Bay Sands complex to comply with commercial fire-safety standards.

The industrial segment is projected to be the fastest-growing application category, owing to high fire risks and the critical nature of operations. Regulatory requirements, insurance mandates, and ESG-driven risk management encourage operators to adopt robust, redundant, and high-capacity pumping systems, often combining diesel and electric pumps in hybrid or dual-drive configurations. Demand is particularly strong in large infrastructure, petrochemical, and energy projects that require deep-well, vertical turbine, and split-case high-flow pumps. For instance, Sulzer’s vertical turbine fire pumps are deployed in chemical plants and energy facilities in Malaysia to provide reliable, high-capacity industrial fire protection.

Regional Insights

North America Fire Pump Market Trends

North America is expected to remain a key market for fire pumps, driven by stringent regulatory requirements, including NFPA standards in the U.S. and national building and fire-safety codes in Canada, which ensure widespread adoption across commercial, institutional, and industrial facilities. The commercial segment, including offices, hospitals, malls, airports, and educational institutions, accounts for a major portion of demand, as these buildings require reliable sprinkler and standpipe systems with high-capacity pumps. For instance, Flowserve’s electric fire pumps are installed in U.S. airport terminals and large hospital complexes to provide NFPA-compliant fire protection.

Technological modernization is increasingly shaping the market, with cloud-connected fire pumps gaining popularity for real-time monitoring, automated diagnostics, and predictive maintenance, enhancing reliability and minimizing downtime. Energy-efficient electric-motor pumps with variable-speed drives and smart building integration are becoming standard, supporting sustainability objectives and regulatory compliance. In high-risk industrial and utility facilities, demand remains strong for robust centrifugal pumps capable of maintaining emergency water flow. Many sites are also adopting hybrid pump systems and smart control panels to improve redundancy and reduce operational risks.

Europe Fire Pump Market Trends

Europe continues to be a key market for fire pumps, driven by strict building and fire-safety regulations, widespread adoption in commercial and industrial infrastructure, and a strong focus on safety compliance across residential, public, and institutional facilities. Countries such as Germany, the U.K., France, and Italy lead in deploying high-capacity centrifugal pumps for sprinkler and standpipe systems, supported by well-established regulatory frameworks and insurance requirements. For example, KSB’s fire pumps are widely installed in German hospitals and commercial complexes to meet local fire-safety standards.

The market is also influenced by ongoing infrastructure modernization and retrofit projects, where older systems are upgraded to comply with updated codes. Industrial sectors, including petrochemicals, energy, and manufacturing, continue to invest in reliable fire pump systems to ensure operational safety and regulatory compliance. Europe’s focus on standardization, certification, and quality testing for fire protection equipment facilitates consistent adoption of advanced pumps across both urban and industrial settings. The uptake of IoT-enabled and digitally monitored fire pumps is increasing, enabling real-time performance tracking and predictive maintenance.

Asia Pacific Fire Pump Market Trends

Asia Pacific is expected to dominate the fire pump market, capturing approximately 49.8% of the revenue share in 2026, driven by rapid urbanization, large-scale industrialization, and the expansion of commercial and public infrastructure in countries such as China, India, Japan, and ASEAN nations. The construction of high-rise residential and commercial buildings, along with airports, metro systems, ports, and industrial corridors, is fueling strong demand for high-capacity fire pumps, particularly horizontal split-case and vertical turbine designs. For example, Grundfos’ horizontal split-case pumps are widely deployed in commercial skyscrapers and airport projects in Singapore to meet stringent fire-safety standards.

The region is also projected to be the fastest-growing market for fire pumps, supported by increasing technological adoption. Electric motor-driven pumps, hybrid systems, and advanced controllers are increasingly integrated into infrastructure projects to enhance reliability, operational efficiency, and energy compliance. Industrial sectors such as petrochemicals, power generation, and manufacturing continue to require robust, redundant pumping systems capable of maintaining emergency water flow under critical conditions. Rising industrial and infrastructure investments in India and ASEAN countries are particularly driving growth in vertical turbine and hybrid fire pump systems, supporting large-scale, high-risk projects such as energy plants and industrial corridors.

Competitive Landscape

The global fire pump market is moderately fragmented, characterized by a mix of OEMs, regional suppliers, and niche specialists competing across different geographies and application segments. Leading companies such as Pentair, Xylem, Grundfos, Flowserve Corporation, and Sulzer Ltd. maintain a strong market presence through extensive product portfolios, established distribution networks, and technology-driven innovations. These firms are increasingly investing in R&D to develop smart, IoT-enabled fire pumps and energy-efficient solutions that align with evolving regulatory and sustainability requirements.

Competition in the market is largely driven by continuous R&D and product innovation, including IoT-enabled fire pumps, energy-efficient electric-motor systems, and modular pump solutions. Companies are expanding their offerings to serve applications ranging from compact residential units to high-capacity industrial pumps while providing value-added services such as predictive maintenance, remote monitoring, and robust after-sales support. Strategic partnerships and acquisitions are also being leveraged to enhance regional presence and reduce lead times, for example, by consolidating distribution channels or integrating fire pump supply with broader water or utility pump contracts in industrial and municipal sectors.

Key Industry Developments:

- In August 2025, Armstrong Fluid Technology expanded its Vertical-In-Line fire pump line with the new 5x4x10PF model, capable of 750?GPM, featuring Design Envelope technology for connected intelligence, performance monitoring, and automated alerts. The pump’s progressive start control eliminates pressure peaks, minimizes water hammer, and protects pipe integrity, ensuring a reliable water supply and enhanced occupant safety.

- In June 2025, Armstrong Fluid Technology launched a 750?GPM 5x4x10PF Vertical-In-Line fire pump in the U.S., featuring its Design Envelope technology for performance tracking, integrated alerts, and remote monitoring. The pump is engineered to prevent pressure spikes, reduce water hammer, and lower mechanical stress on pipes through a controlled startup sequence. Its design eliminates the need for external pressure-reducing valves and drain lines, simplifying installation and reducing material and labor costs.

Companies Covered in Fire Pump Market

- Pentair

- Grundfos

- NAFFCO

- Flowserve

- Sulzer

- Kirloskar Brothers

- SPP Pumps

- Peerless Pump Company

- Armstrong Fluid Company

- Rosenbauer

Frequently Asked Questions

The global fire pump market is valued at US$591.5 million in 2026 and expected to reach US$757.7 million by 2033, reflecting robust growth.

Key demand drivers include stricter fire safety regulations and enforcement, ongoing urbanization and industrial expansion, and modernization of aging building and industrial assets, all of which require compliant fire water systems with certified pumps.

The commercial segment currently leads in terms of installed base and annual demand, reflecting high regulatory requirements for offices, retail, healthcare, education, and public buildings.

Asia Pacific leads the market with around 49.8% share, driven by rapid urbanization, large-scale infrastructure development, and expanding industrial and commercial construction.

A major opportunity in the fire pump market lies in electrification and digitalization, driving the adoption of electric and hybrid fire pumps and enabling revenue growth through IoT-enabled monitoring, automated testing, and predictive maintenance services, particularly for large commercial and industrial asset portfolios.