- Executive Summary

- Global Finance Cloud Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Price Trend Analysis, 2025

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Finance Cloud Market Outlook: Component

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Component, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- Market Attractiveness Analysis: Component

- Global Finance Cloud Market Outlook: Deployment Model

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Deployment Model, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Market Attractiveness Analysis: Deployment Model

- Global Finance Cloud Market Outlook: Organization Size

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Organization Size, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Market Attractiveness Analysis: Organization Size

- Global Finance Cloud Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- Market Attractiveness Analysis: End-use Industry

- Global Finance Cloud Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- Europe Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- East Asia Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- South Asia & Oceania Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- Latin America Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- Middle East & Africa Finance Cloud Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Component, 2026-2033

- Solutions

- Services

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Deployment Model, 2026-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Organization Size, 2026-2033

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government & Public Sector

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Oracle Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- SAP SE

- Microsoft Corporation

- Salesforce, Inc.

- IBM Corporation

- Workday, Inc.

- Sage Group plc

- Intuit Inc.

- Anaplan, Inc.

- Workiva Inc.

- BlackLine, Inc.

- Coupa Software Inc.

- Xero Limited

- Fiserv, Inc.

- Oracle Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Hardware & Software IT Services

- Finance Cloud Market

Finance Cloud Market Size, Share, and Growth Forecast 2026 - 2033

Finance Cloud Market by Component (Solutions, Services), by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), by Organization Size (Small & Medium Enterprises (SMEs), Large Enterprises), by End-use Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecommunications, Retail & E-commerce, Healthcare, Manufacturing, Government & Public Sector, Others), by Regional Analysis, 2026 - 2033

Finance Cloud Market Size and Trend Analysis

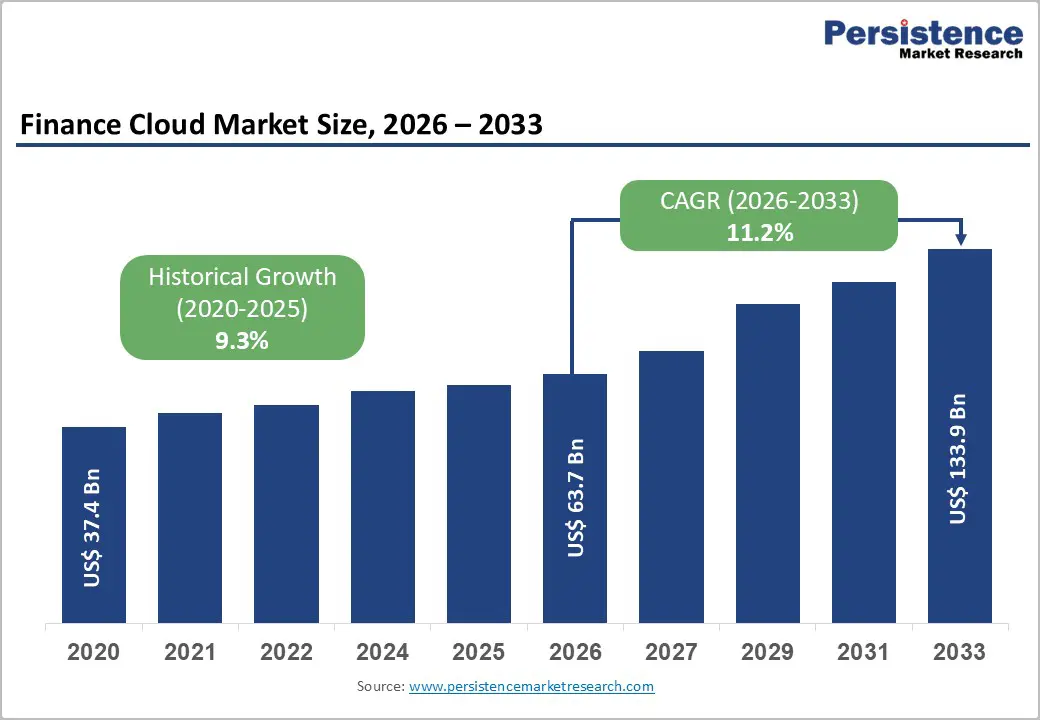

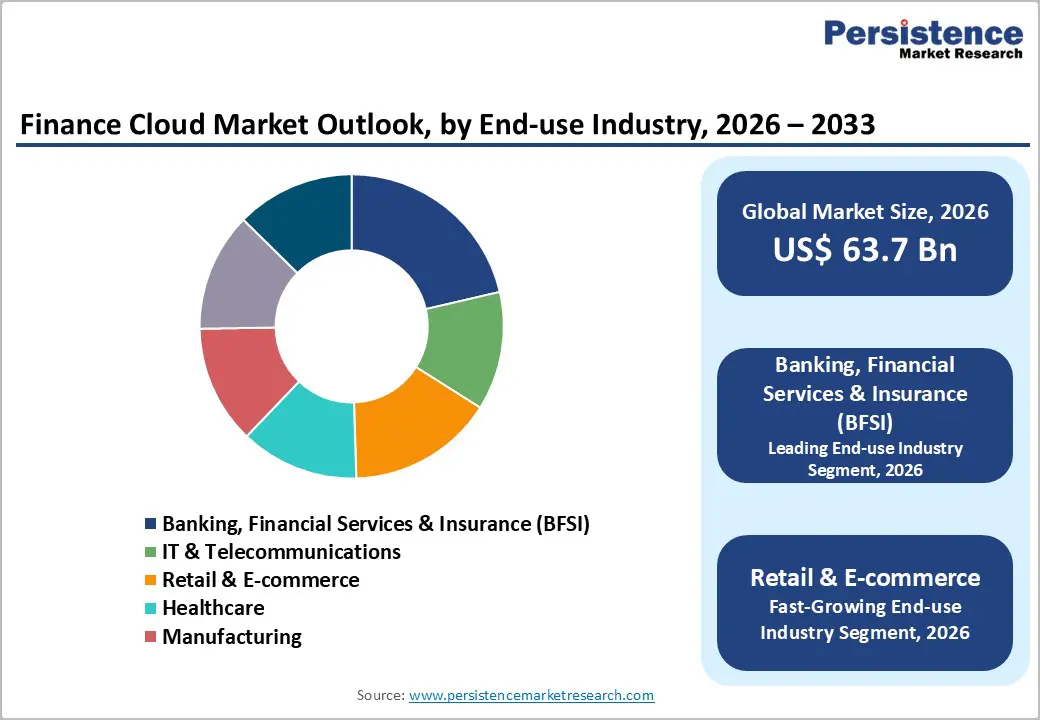

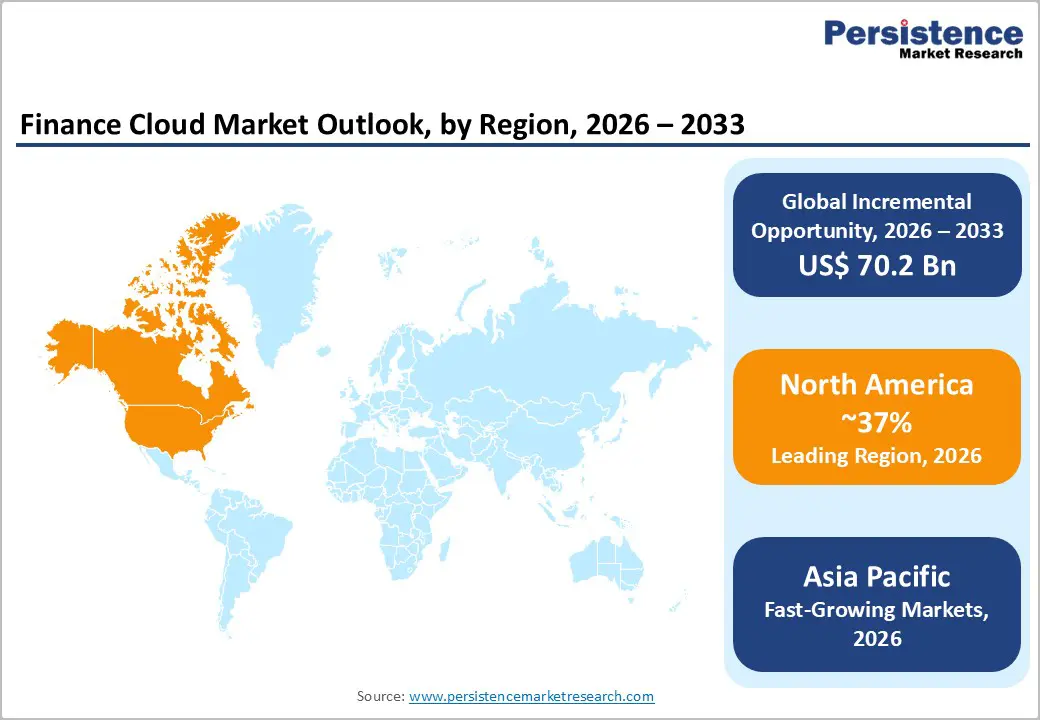

The global Finance Cloud Market size is expected to be valued at US$ 63.7 billion in 2026 and projected to reach US$ 133.9 billion by 2033, growing at a CAGR of 11.2% between 2026 and 2033. The market is expanding as financial institutions accelerate digital transformation and modernize legacy IT infrastructure to support digital banking, real-time analytics, and data-driven financial management.

Growing demand for scalable cloud platforms enables organizations to improve operational efficiency, enhance customer experiences, and reduce infrastructure costs. Additionally, strict regulatory frameworks such as GDPR and SOX are encouraging secure cloud adoption for compliance and risk management. Increasing investments in cloud-based financial platforms and automation technologies continue to strengthen the adoption of finance cloud solutions worldwide.

Key Industry Highlights:

- Leading Region: North America leads with a 37% share in 2025, supported by strong financial infrastructure and early adoption of advanced cloud technologies.

- Fastest Growing Region: Asia Pacific, holding 32% share in 2025, is the fastest-growing region due to rapid fintech expansion, digital banking adoption, and rising cloud investments.

- Leading Component: Solutions lead with 62% share in 2025, driven by demand for integrated financial management, compliance automation, and analytics platforms.

- Leading Deployment Model: Public cloud dominates with 55% share in 2025, supported by scalability, cost efficiency, and growing use in financial data processing.

- Key Opportunity: AI, machine learning, and blockchain integration in finance cloud platforms creates opportunities through predictive analytics, automation, and advanced financial insights.

| Key Insights | Details |

|---|---|

|

Finance Cloud Market Size (2026E) |

US$ 63.7 billion |

|

Market Value Forecast (2033F) |

US$ 133.9 billion |

|

Projected Growth CAGR(2026-2033) |

11.2% |

|

Historical Market Growth (2020-2025) |

9.3% |

Market Dynamics

Drivers - Accelerating Digital Transformation in Financial Institutions Driving Adoption of Scalable Cloud-Based Financial Platforms

Financial institutions worldwide are rapidly adopting cloud technologies to support digital transformation and deliver seamless, technology-driven financial services. Cloud infrastructure enables real-time transaction processing, faster product deployment, and enhanced operational agility. With rising competition from digital banks and fintech platforms, organizations are prioritizing cloud environments that support data analytics, automation, and integrated financial systems to improve decision-making and customer engagement.

Additionally, finance cloud platforms support advanced technologies such as artificial intelligence, machine learning, and predictive analytics for fraud detection and customer insights. These capabilities help financial institutions enhance security, optimize operations, and personalize services. As banks and financial service providers modernize legacy IT infrastructure, cloud-based financial platforms are becoming a critical foundation for building efficient, scalable, and innovation-driven financial ecosystems.

Growing Regulatory and Compliance Requirements Encouraging Adoption of Secure Cloud Financial Management Systems

Financial institutions operate in highly regulated environments where compliance with global and regional standards is essential. Regulations such as Basel III, PCI DSS, GDPR, and SOX require secure data management, transparency in financial reporting, and strict monitoring of financial transactions. Finance cloud platforms help organizations meet these requirements by automating compliance management, providing secure data storage, and built-in monitoring capabilities.

Cloud-based financial systems also provide encrypted data environments, audit-ready documentation, and centralized regulatory reporting tools, simplifying compliance processes. By reducing manual intervention and improving data governance, finance cloud solutions help institutions minimize regulatory risks and penalties. As regulatory frameworks continue to evolve globally, organizations are increasingly adopting cloud-based financial platforms to maintain compliance while improving operational efficiency and security.

Restraints - Ongoing Data Security and Privacy Concerns Limiting Full Adoption of Cloud-Based Financial Platforms

Despite significant improvements in cloud security technologies, concerns about data breaches and cyber threats continue to restrain adoption in the finance cloud market. Financial institutions handle highly sensitive financial and customer data, making them cautious about migrating critical workloads to cloud environments. Risks associated with unauthorized access, cyberattacks, and potential data leaks remain key barriers for many organizations.

Additionally, strict privacy regulations and internal security policies require financial firms to maintain high levels of data protection and governance. Concerns about data residency, third-party access, and system vulnerabilities prompt many institutions to adopt hybrid or phased cloud strategies rather than a full migration. These cautious approaches slow the overall pace of finance cloud adoption across the global financial services sector.

Integration Challenges with Legacy Financial Systems: Increasing Complexity of Cloud Migration

Many financial institutions continue to rely on complex legacy IT systems that were not designed to operate within modern cloud environments. Integrating these older systems with cloud-based financial platforms often requires extensive customization, system redesign, and data restructuring. As a result, migration processes can become time-consuming, technically challenging, and costly for organizations.

Legacy infrastructure also limits interoperability between existing applications and new cloud technologies, creating operational disruptions during transition phases. Financial institutions must carefully manage system upgrades, data transfers, and application compatibility to avoid service interruptions. These integration challenges can delay digital transformation initiatives, particularly for organizations with deeply embedded legacy banking and financial management systems.

Opportunity - Expanding Adoption of Hybrid Cloud Models in Emerging Economies Creating New Growth Avenues for Financial Platforms

Hybrid cloud deployment is emerging as a major opportunity for finance cloud providers, particularly in developing economies where organizations seek a balance between security, flexibility, and cost efficiency. Hybrid environments allow financial institutions to maintain sensitive data on private infrastructure while leveraging public cloud scalability for analytics, applications, and digital financial services.

In many emerging markets, rapid fintech development, digital banking expansion, and government-led digitalization initiatives are accelerating the need for scalable financial technology infrastructure. Hybrid cloud solutions enable banks and financial service providers to modernize operations while meeting local regulatory and data sovereignty requirements. This growing digital finance ecosystem is creating strong opportunities for cloud providers offering flexible and region-specific financial cloud solutions.

Integration of Artificial Intelligence and Machine Learning Enabling Advanced Financial Analytics and Automation

The integration of artificial intelligence and machine learning within finance cloud platforms presents a significant opportunity for market growth. These technologies enable financial institutions to perform predictive analytics, automate complex financial processes, and enhance risk management capabilities. AI-driven insights also support fraud detection, credit assessment, and customer behavior analysis, improving operational efficiency and decision-making.

Finance cloud platforms equipped with AI and advanced analytics tools allow organizations to process large volumes of financial data in real time. This capability supports personalized financial services, faster transaction processing, and more accurate forecasting. As financial institutions increasingly prioritize intelligent automation and data-driven strategies, the demand for AI-enabled finance cloud platforms is expected to grow substantially.

Category-wise Analysis

Component Insights

Solutions dominate the finance cloud market, accounting for around 62% of the share in 2025 as financial institutions prioritize integrated platforms for managing financial operations, compliance, and analytics. These solutions combine capabilities such as enterprise resource planning, financial reporting, customer relationship management, and automated regulatory compliance. Their ability to centralize financial data and streamline processes makes them essential for organizations seeking efficient and scalable financial management systems.

Services are expected to be the fastest-growing component as organizations increasingly require consulting, system integration, and ongoing support for cloud adoption. Financial institutions often rely on specialized service providers to assist with cloud migration, platform customization, and operational optimization. As finance cloud implementations become more complex, demand for managed services and technical expertise continues to rise.

Deployment Model Insights

Public cloud leads the deployment model segment with about 55% share in 2025, supported by its scalability, cost efficiency, and accessibility. Financial institutions increasingly deploy financial applications on public cloud platforms to handle large transaction volumes, enable real-time analytics, and reduce infrastructure investments. The flexibility offered by public cloud environments allows organizations to scale computing resources quickly in response to changing financial workloads.

Hybrid cloud is emerging as the fastest-growing deployment model as financial institutions seek a balance between security and operational flexibility. Hybrid environments allow sensitive financial data to remain within private infrastructure while leveraging public cloud capabilities for analytics and application development. This model supports regulatory compliance and data governance while enabling organizations to modernize financial operations with greater agility.

Organization Size Insights

Large enterprises account for approximately 68% of the finance cloud market share in 2025, driven by their substantial investments in digital transformation and cloud-based financial infrastructure. These organizations operate complex financial ecosystems that require advanced platforms for financial planning, compliance management, and risk monitoring. Their significant IT budgets enable large-scale cloud deployments and integration with global financial systems.

Small and medium-sized enterprises are expected to be the fastest-growing segment as cloud technology becomes more accessible and cost-effective. Finance cloud platforms allow SMEs to adopt advanced financial management tools without heavy upfront infrastructure investments. Increasing availability of subscription-based cloud solutions is helping smaller organizations streamline accounting, financial reporting, and operational management.

Industry Insights

The banking, financial services, and insurance sector holds around 45% share of the finance cloud market in 2025, reflecting the sector’s strong reliance on secure and scalable financial technology infrastructure. Financial institutions use cloud platforms to support digital banking services, manage large volumes of transactions, and ensure regulatory compliance. Cloud-based systems also enhance operational efficiency and enable real-time financial analytics.

The retail and e-commerce sector is expected to be the fastest-growing end-use industry due to increasing digital payment adoption and expanding online financial ecosystems. Businesses in this sector require cloud-based financial platforms to manage high transaction volumes, payment processing, and financial reporting. Growing demand for seamless digital payment systems continues to drive finance cloud adoption in retail environments.

Regional Insights

North America Finance Cloud Market Trends and Insights

North America dominates the finance cloud market, accounting for approximately 37% of the global share in 2025. The region benefits from a highly developed financial ecosystem, strong regulatory frameworks, and early adoption of advanced cloud technologies. Major financial institutions in the United States and Canada are investing heavily in cloud-based platforms to enhance operational efficiency, strengthen cybersecurity, and support digital banking services across large customer bases.

The presence of leading technology providers and financial institutions further accelerates innovation in finance cloud solutions. Banks and financial service providers across the region increasingly utilize cloud-based platforms for trading systems, risk analytics, and real-time transaction processing. Continuous investment in artificial intelligence, automation, and financial technology infrastructure continues to strengthen the region’s leadership in cloud-based financial management systems.

Europe Finance Cloud Market Trends and Insights

Europe represents a significant market for finance cloud adoption, supported by strong regulatory policies and digital transformation initiatives across financial institutions. Countries such as Germany, the United Kingdom, and France are leading the adoption of cloud-based financial platforms to modernize banking infrastructure, improve regulatory reporting, and strengthen financial data governance across institutions.

The region is projected to grow at a CAGR of around 12.8% during the forecast period as financial organizations accelerate cloud migration strategies. Strict regulatory frameworks and regional data protection policies are encouraging the adoption of secure and compliant cloud environments. Financial institutions across Europe are also investing in hybrid cloud architectures to balance operational flexibility with regulatory and data sovereignty requirements.

Asia Pacific Finance Cloud Market Trends and Insights

Asia-Pacific accounts for around 32% of the global finance cloud market and is one of the most dynamic regions for digital financial innovation. Rapid digital banking adoption, expanding fintech ecosystems, and rising investments in financial technology infrastructure are driving strong demand for cloud-based financial platforms across major economies, including China, India, Japan, and Southeast Asian countries.

The region is experiencing rapid growth as financial institutions modernize legacy banking systems and adopt cloud technologies to manage increasing digital transactions. Government initiatives supporting digital payments, financial inclusion, and fintech development are accelerating cloud adoption. Financial organizations across Asia-Pacific are leveraging cloud platforms to improve transaction-processing efficiency, enhance financial analytics, and support large-scale digital financial services.

Competitive Landscape

The finance cloud market is moderately consolidated, with a group of established technology providers dominating global adoption through continuous innovation and platform expansion. Leading vendors focus on strengthening their cloud-based financial management ecosystems by integrating advanced capabilities such as artificial intelligence, automation, and regulatory compliance tools. Strategic investments in research and development, along with platform upgrades, enable providers to enhance security, scalability, and analytics capabilities for financial institutions.

At the same time, new and emerging providers are entering the market with specialized software-as-a-service financial solutions tailored for small and medium-sized enterprises. These solutions emphasize flexibility, subscription-based pricing, and simplified deployment models. Growing demand from organizations seeking cost-effective cloud financial management tools is encouraging innovation and increasing competition across the global finance cloud ecosystem.

Key Developments:

- In June 2025, Oracle introduced an AI-enhanced finance cloud platform designed to improve financial forecasting, budgeting, and scenario planning. The update integrates advanced analytics and automation features, enabling financial institutions and enterprises to generate real-time insights and strengthen data-driven decision-making capabilities.

- In April 2024, AWS launched a finance-focused version of its FSx cloud storage service designed to meet strict financial industry compliance requirements. The solution supports secure data management, high-performance computing workloads, and scalable infrastructure tailored for financial analytics and transaction-intensive environments.

- In November 2024, Microsoft Azure expanded its sovereign cloud offerings across Europe to address growing data sovereignty and regulatory compliance needs. The expansion enables financial institutions to host sensitive financial data within regional cloud infrastructures while maintaining strong security, governance, and regulatory alignment.

Companies Covered in Finance Cloud Market

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Salesforce, Inc.

- IBM Corporation

- Workday, Inc.

- Sage Group plc

- Intuit Inc.

- Anaplan, Inc.

- Workiva Inc.

- BlackLine, Inc.

- Coupa Software Inc.

- Xero Limited

- Fiserv, Inc.

Frequently Asked Questions

The global finance cloud market is valued at US$ 63.7 billion in 2026, supported by growing adoption of cloud-based financial management platforms across enterprises.

Increasing digital transformation and regulatory compliance requirements in the BFSI sector, which holds 45% share in 2025, are major demand drivers.

North America leads the market with 37% share in 2025, driven by advanced financial infrastructure and early adoption of cloud technologies.

Integration of AI-driven analytics and automation within finance cloud solutions, particularly in the solutions segment holding 62% share in 2025, presents strong growth opportunities.

Major players include Oracle, SAP, Microsoft, Amazon Web Services, and IBM, offering advanced cloud-based financial platforms and services globally.